United States

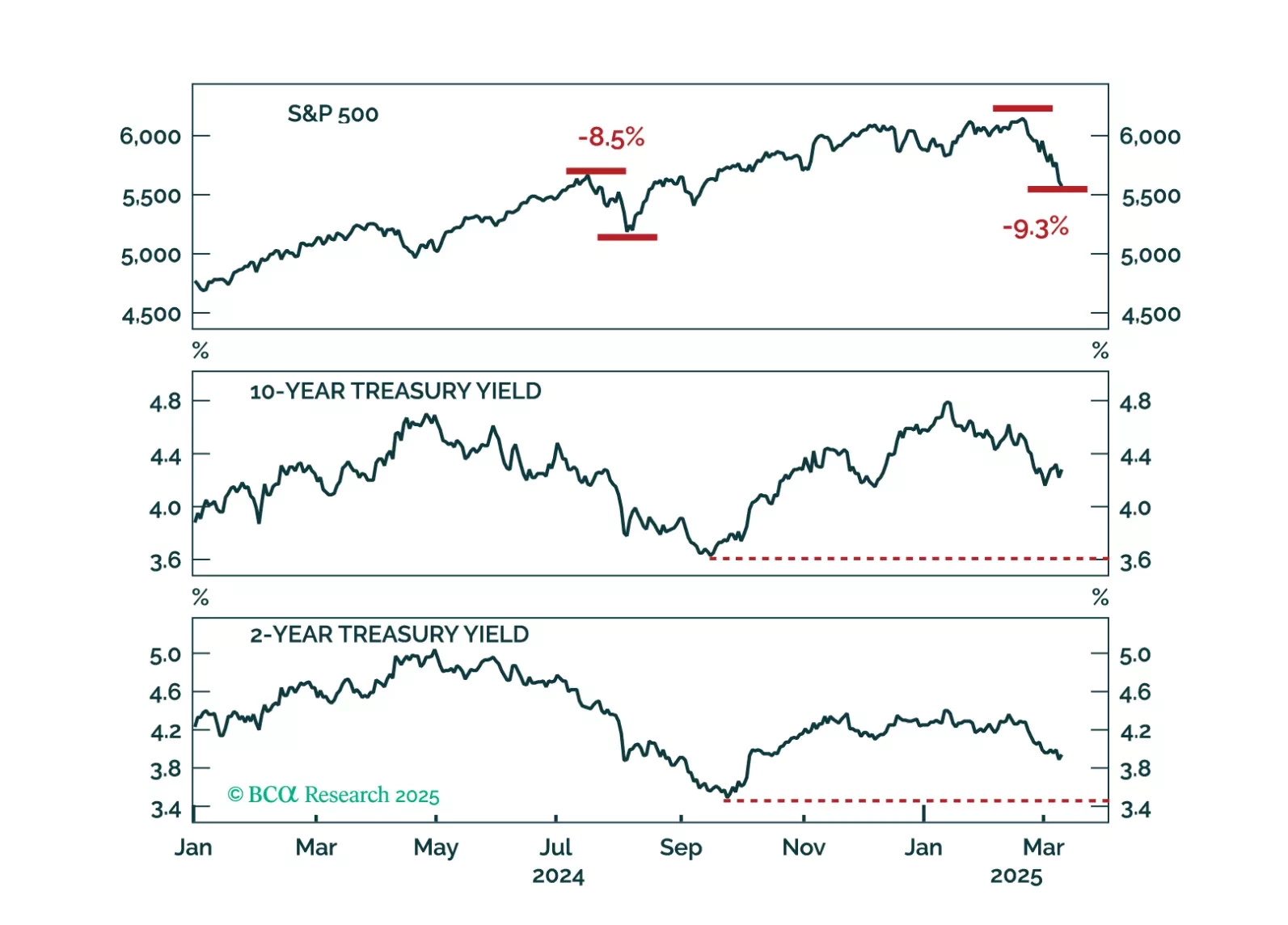

A falling stock market and sticky bond yields represent the worst of both worlds for investors. We interrogate why bond yields haven’t dropped more given the large selloff seen in equities.

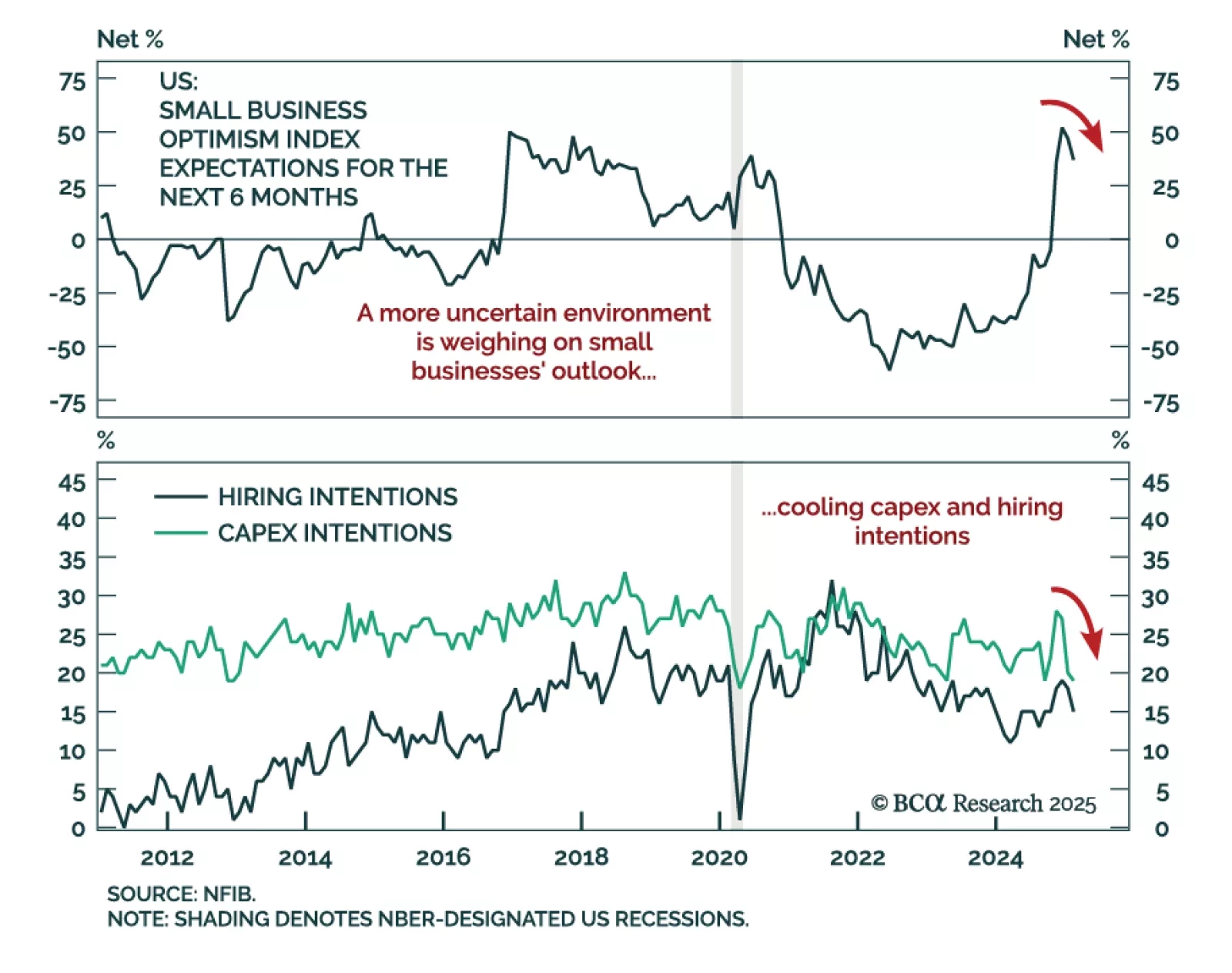

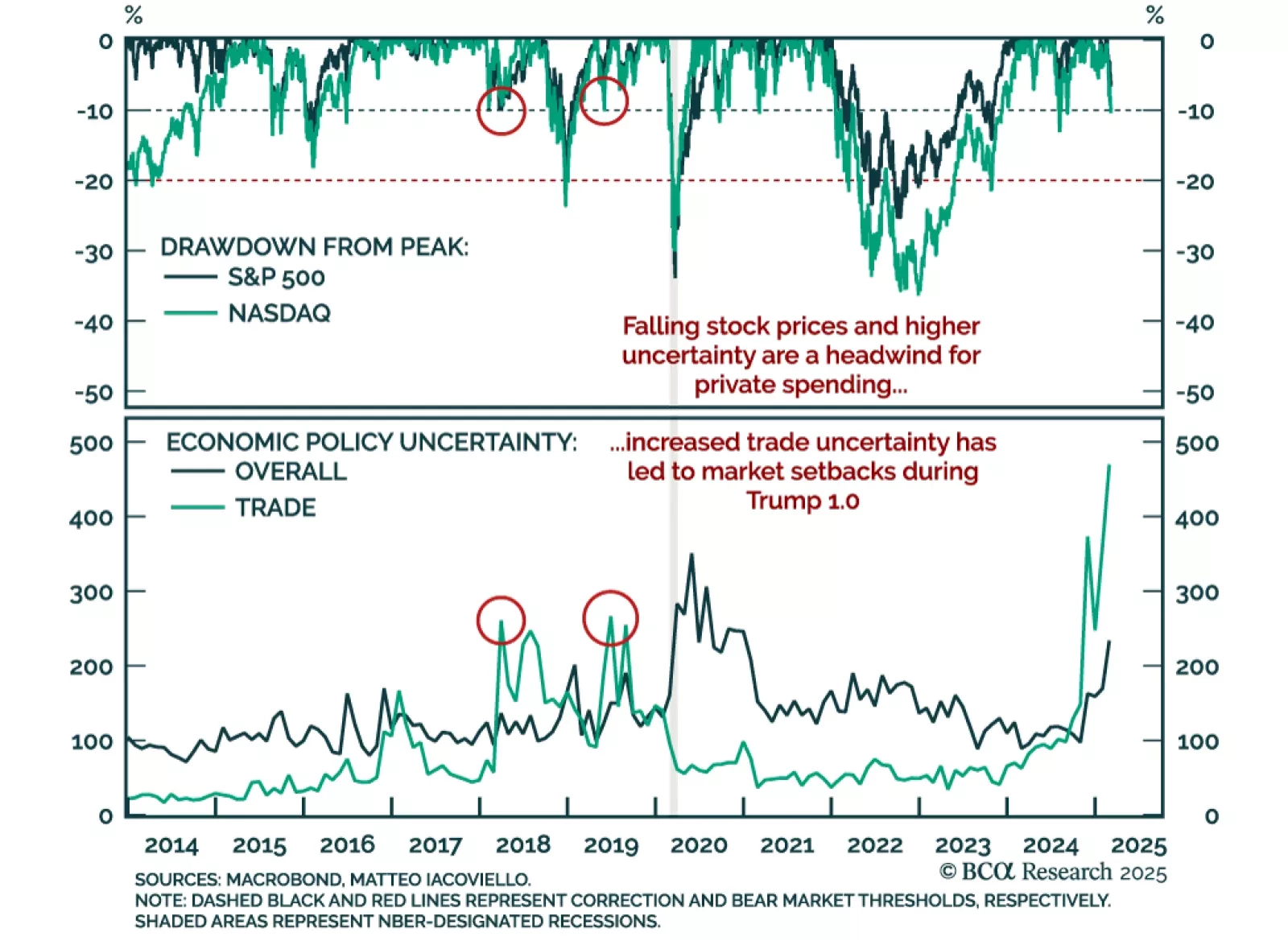

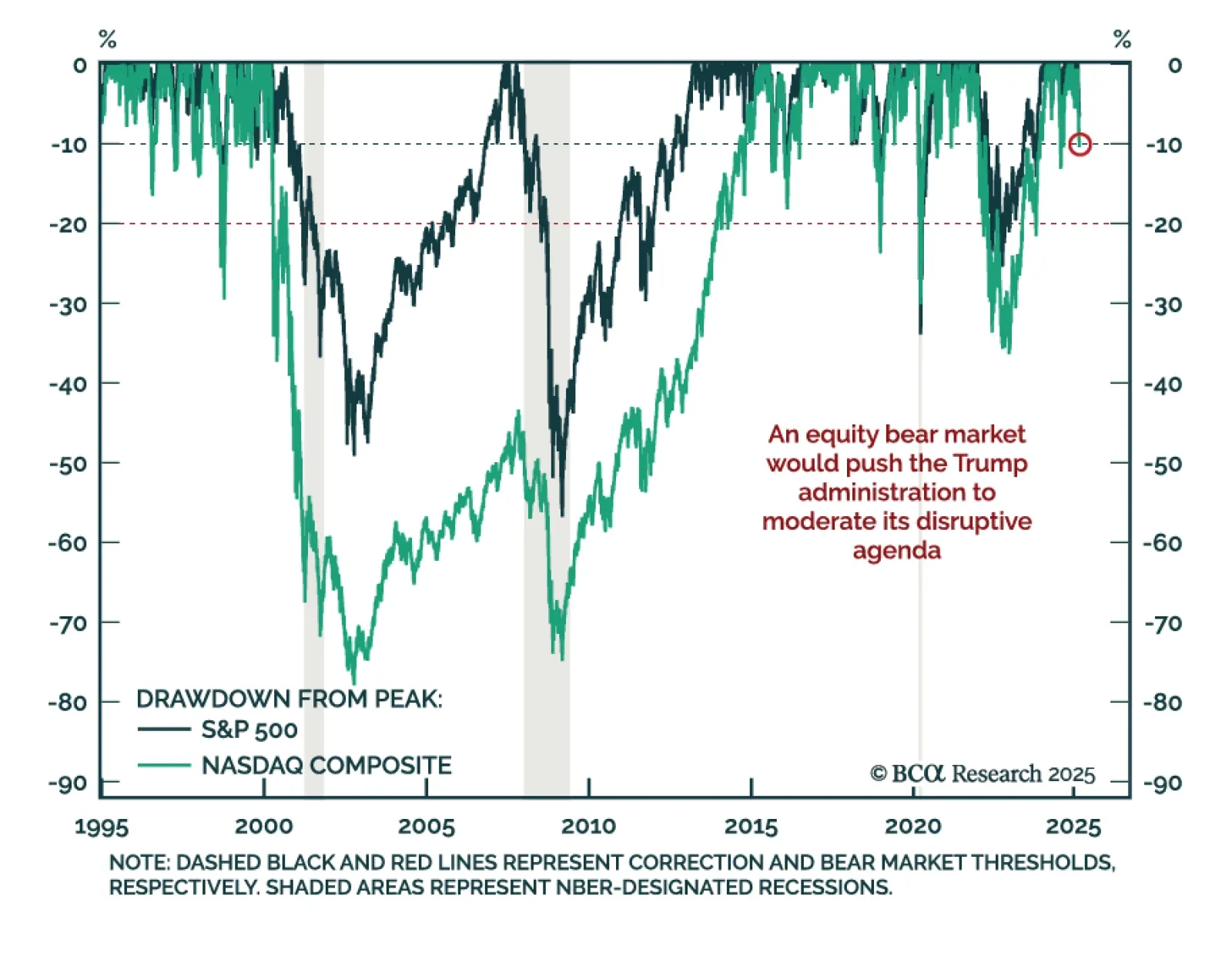

Although there may be a method to DOGE’s 100-mile-an-hour madness, we think the worries and uncertainty stoked by it and on-again, off-again tariff measures have increased the probability of a recession while bringing forward its start date. We are therefore tactically downgrading equities to underweight and upgrading fixed income and cash to overweight. Investors should pursue a defensive posture.

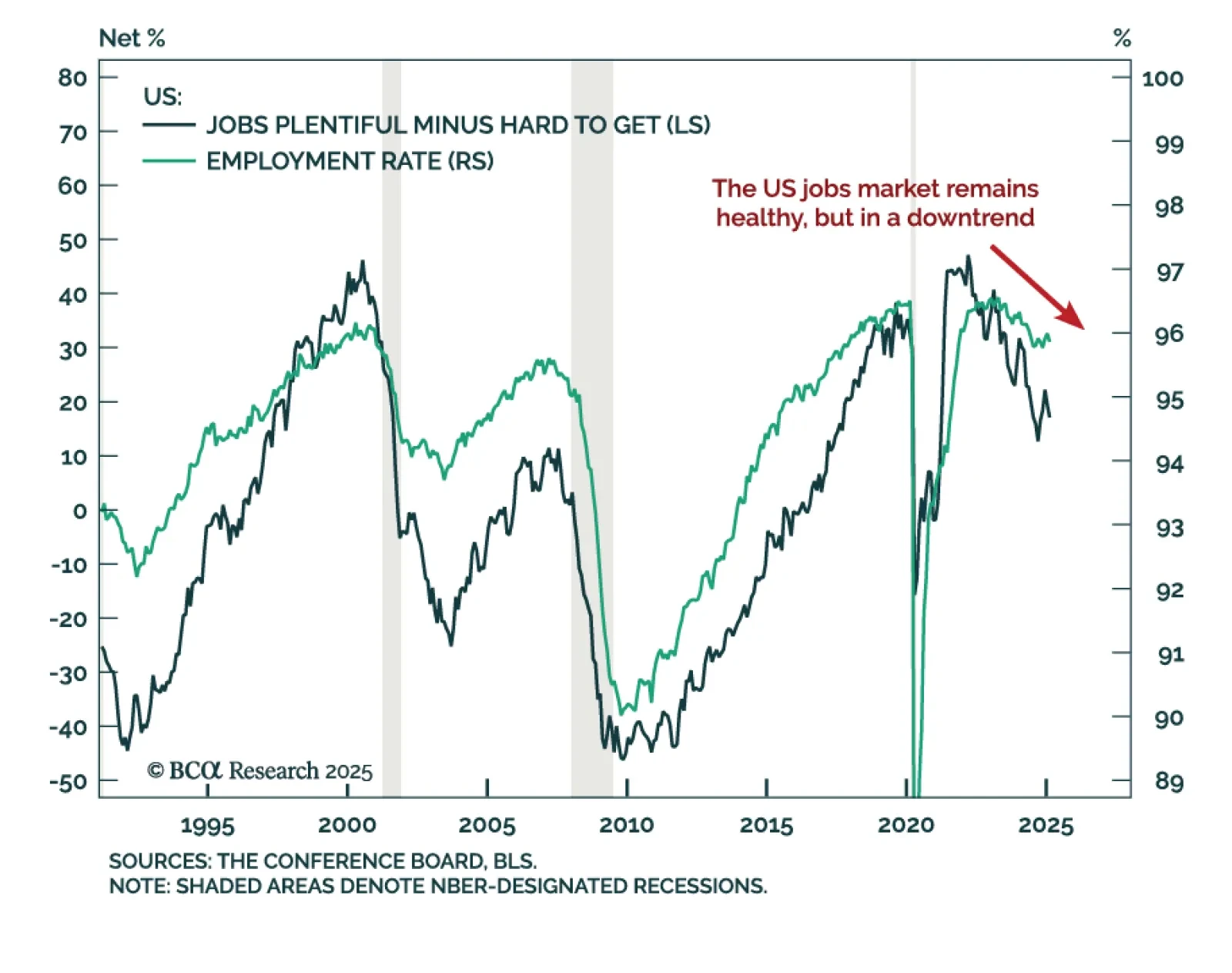

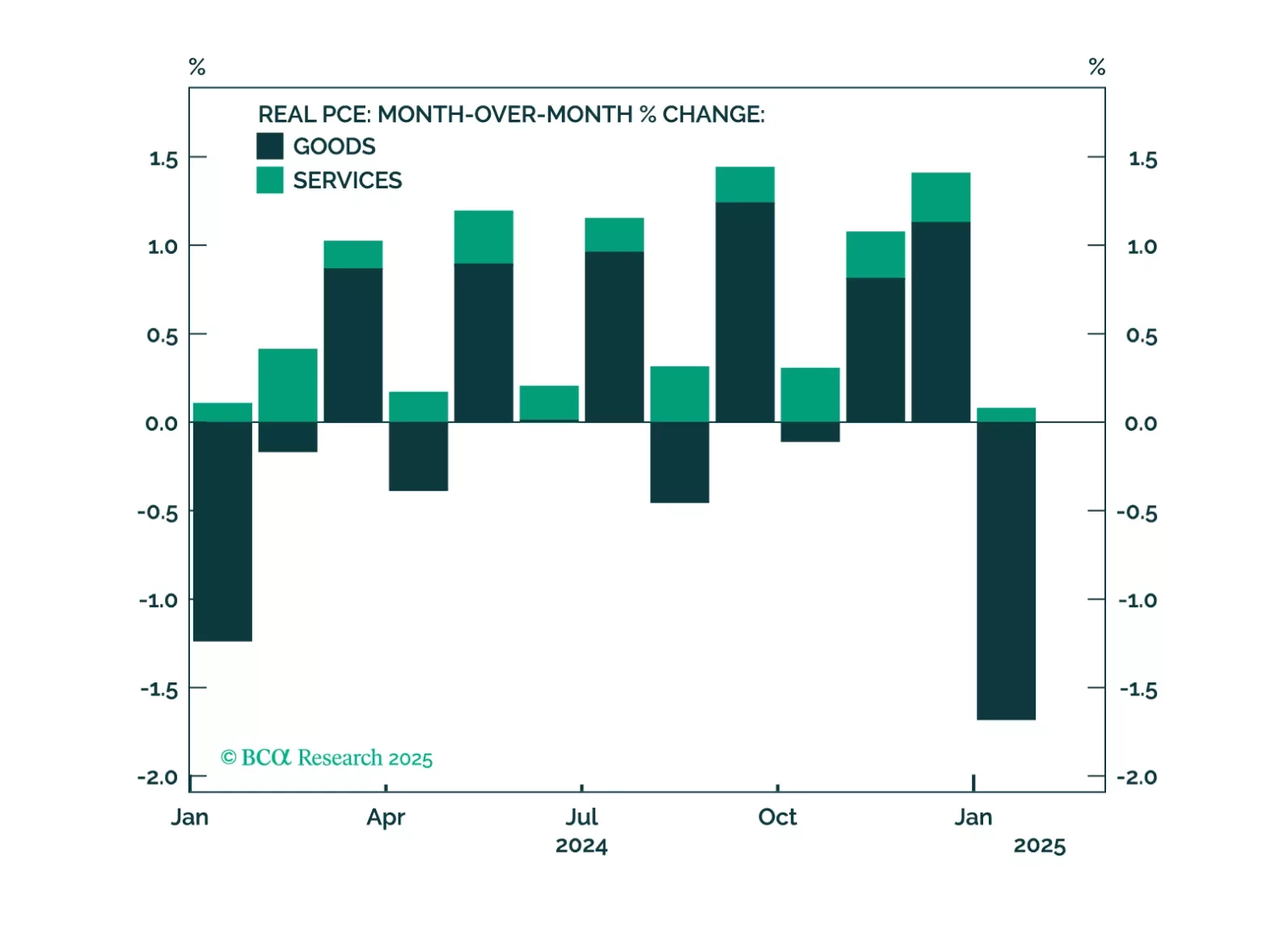

This morning’s employment report showed solid job growth, but recent consumer spending indicators are more concerning. The risk of recession starting within the next few months has increased. We suggest some important indicators for investors to track in the current environment.

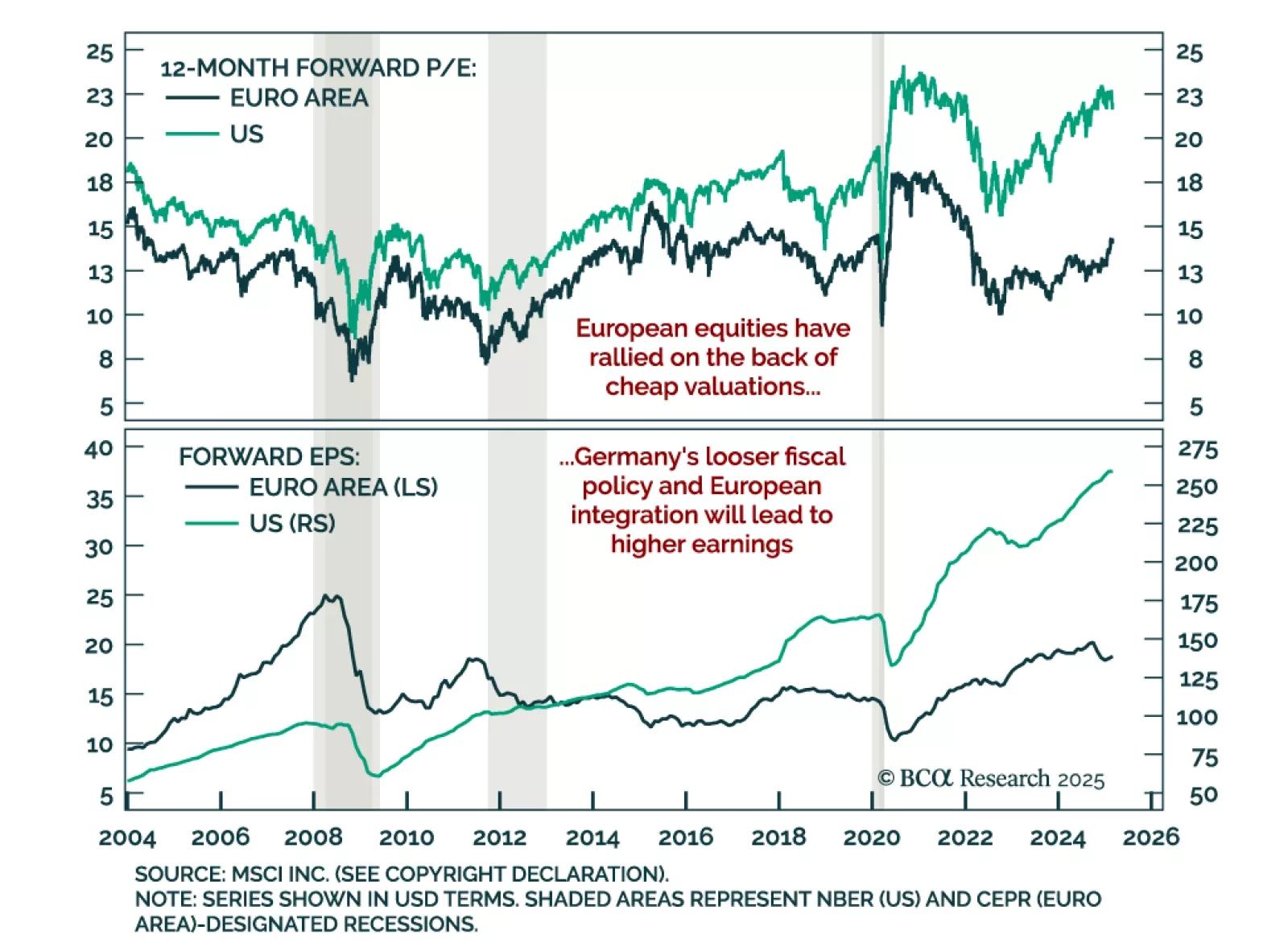

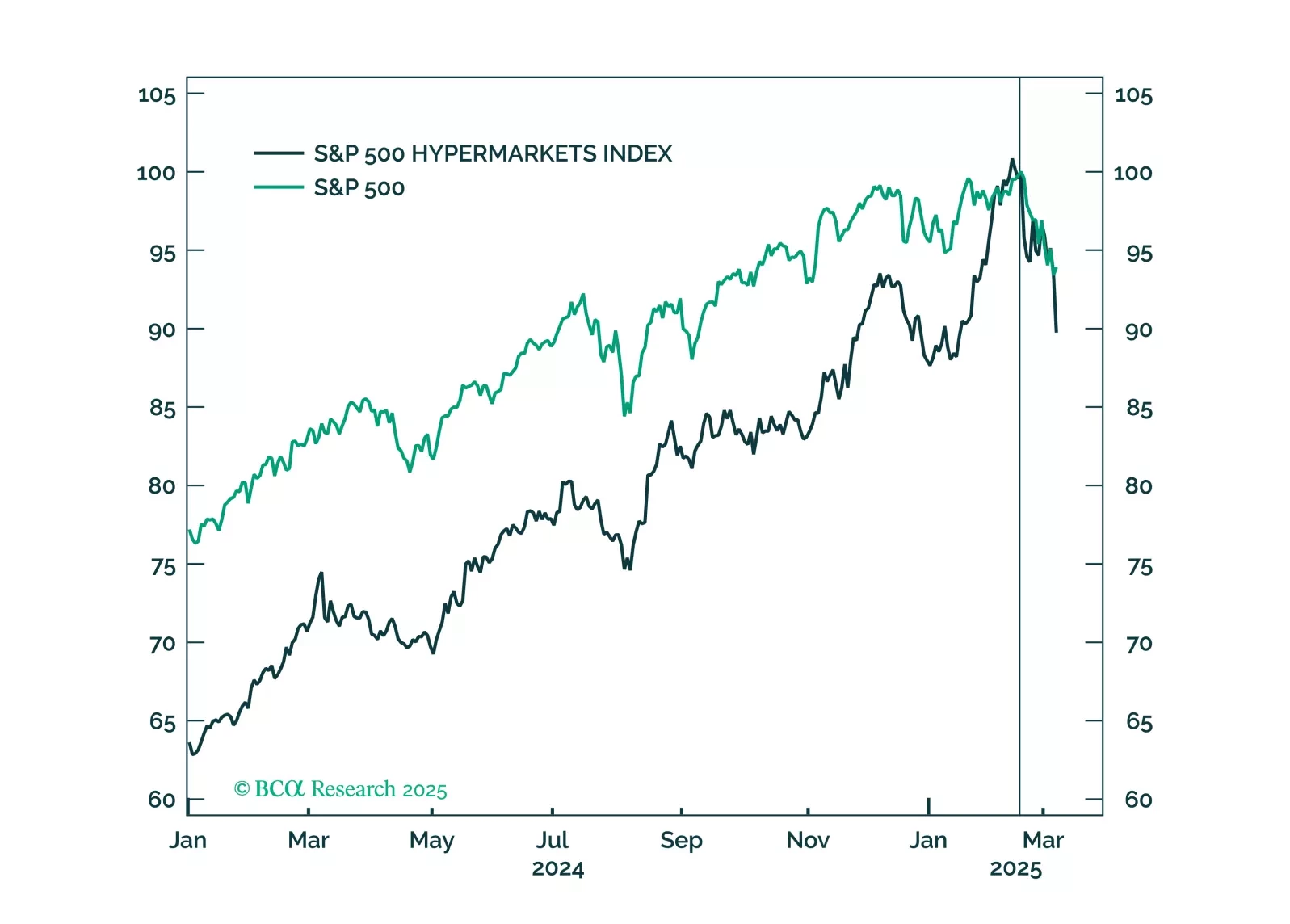

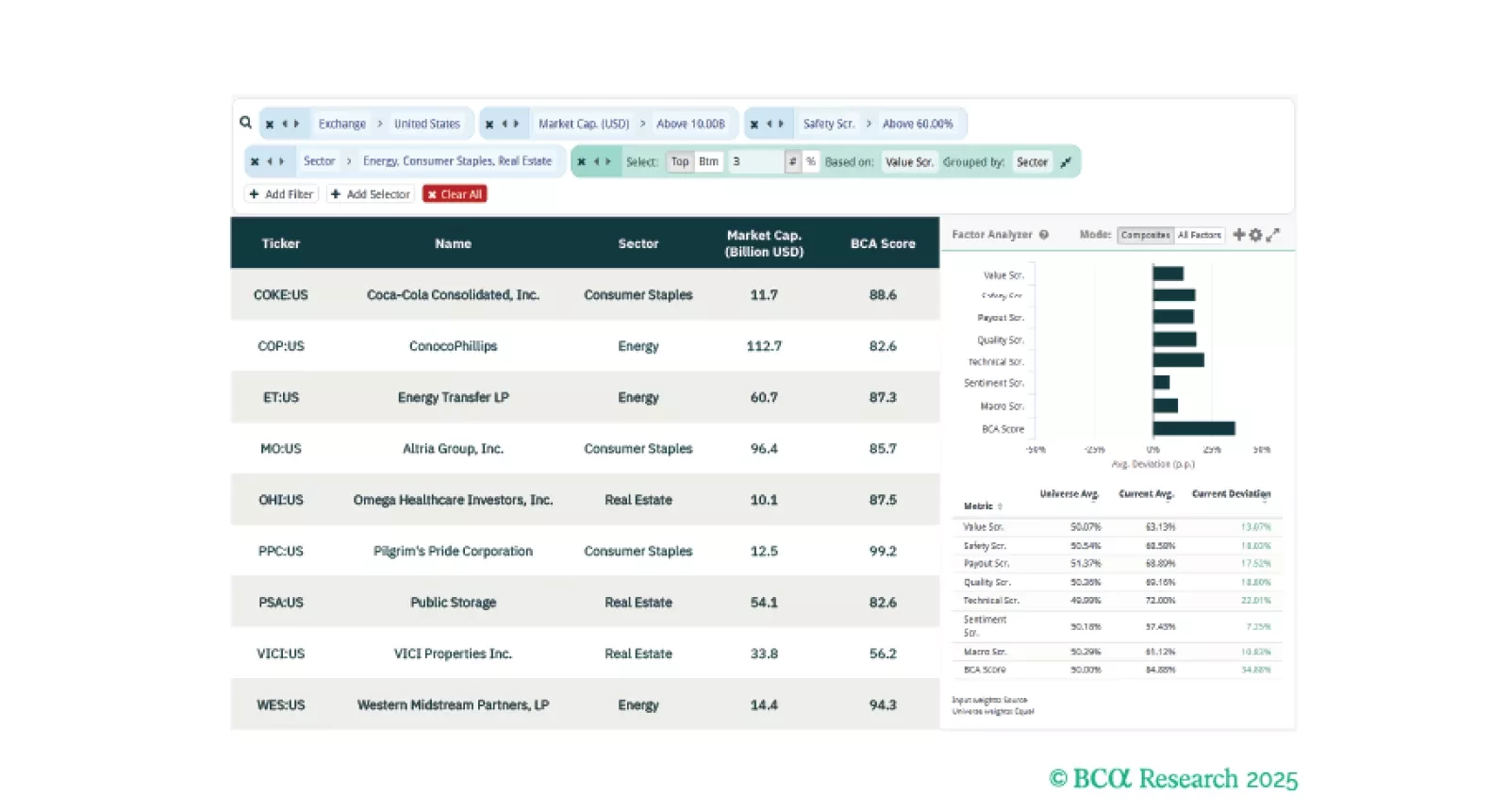

This week, our three screeners cover equity plays in US defensives, US Tech, and European Small Cap Value.