United States

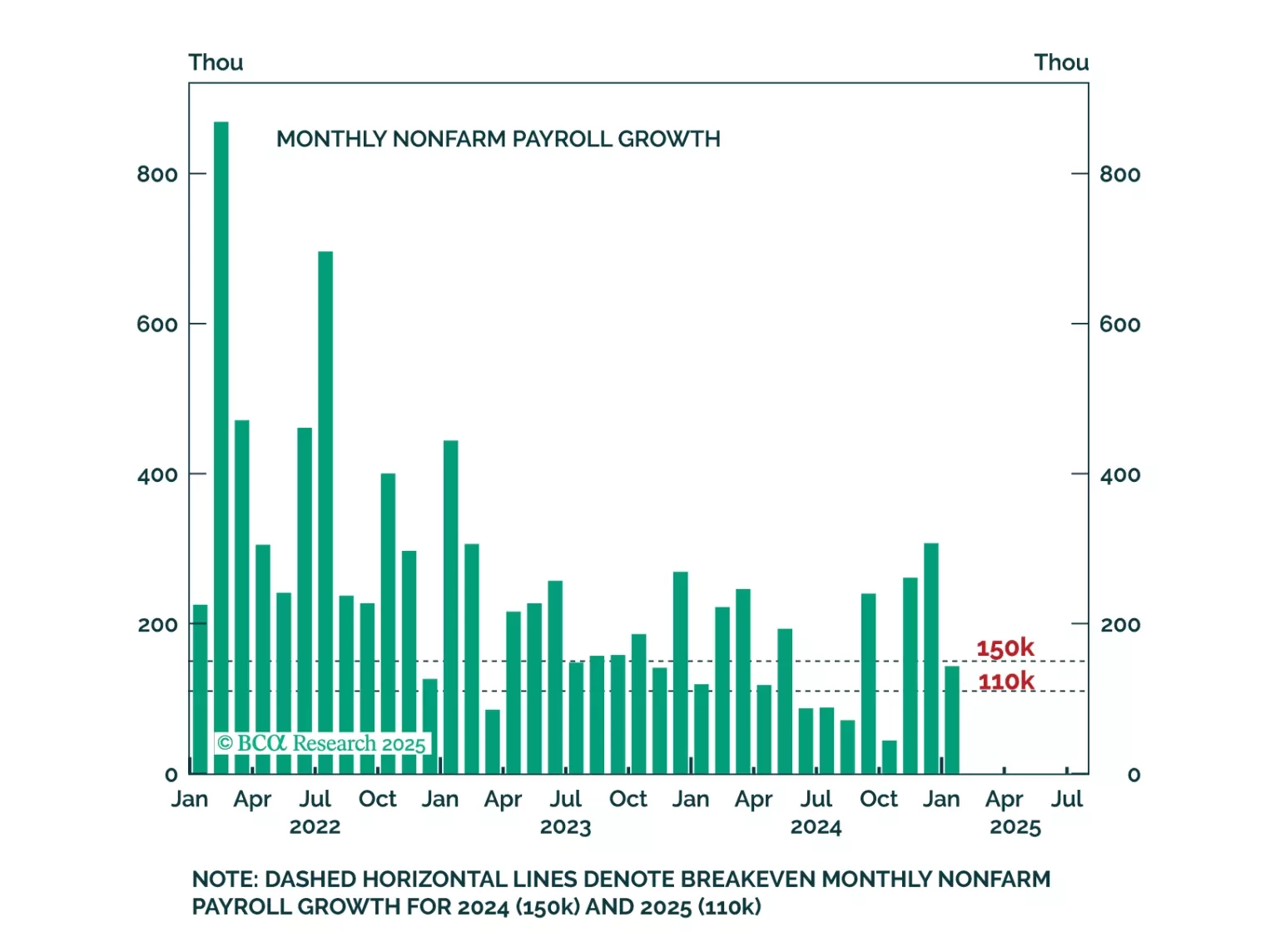

Some thoughts on this morning's employment data and Treasury Secretary Bessent's recent attempts to talk down the 10-year Treasury yield.

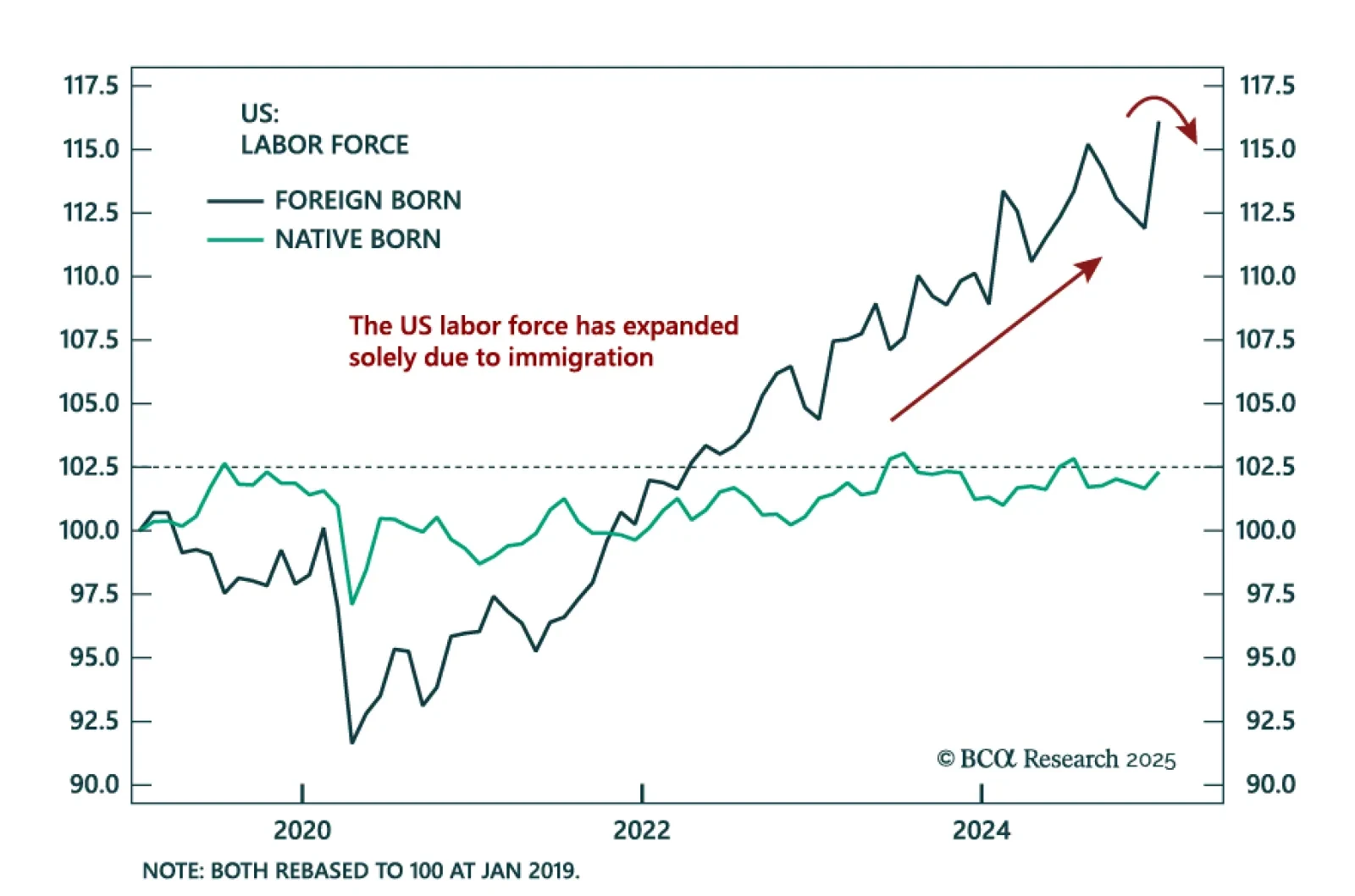

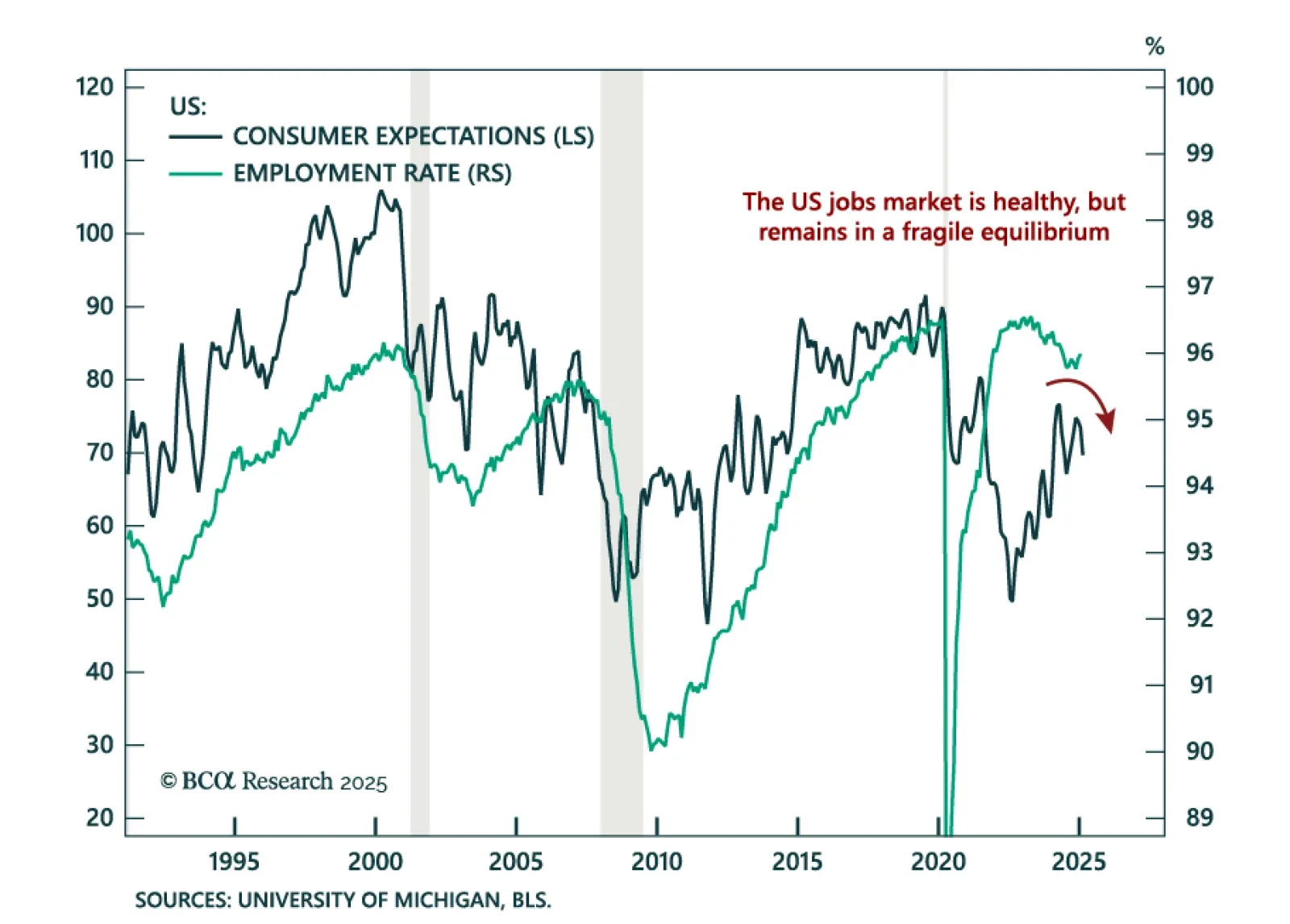

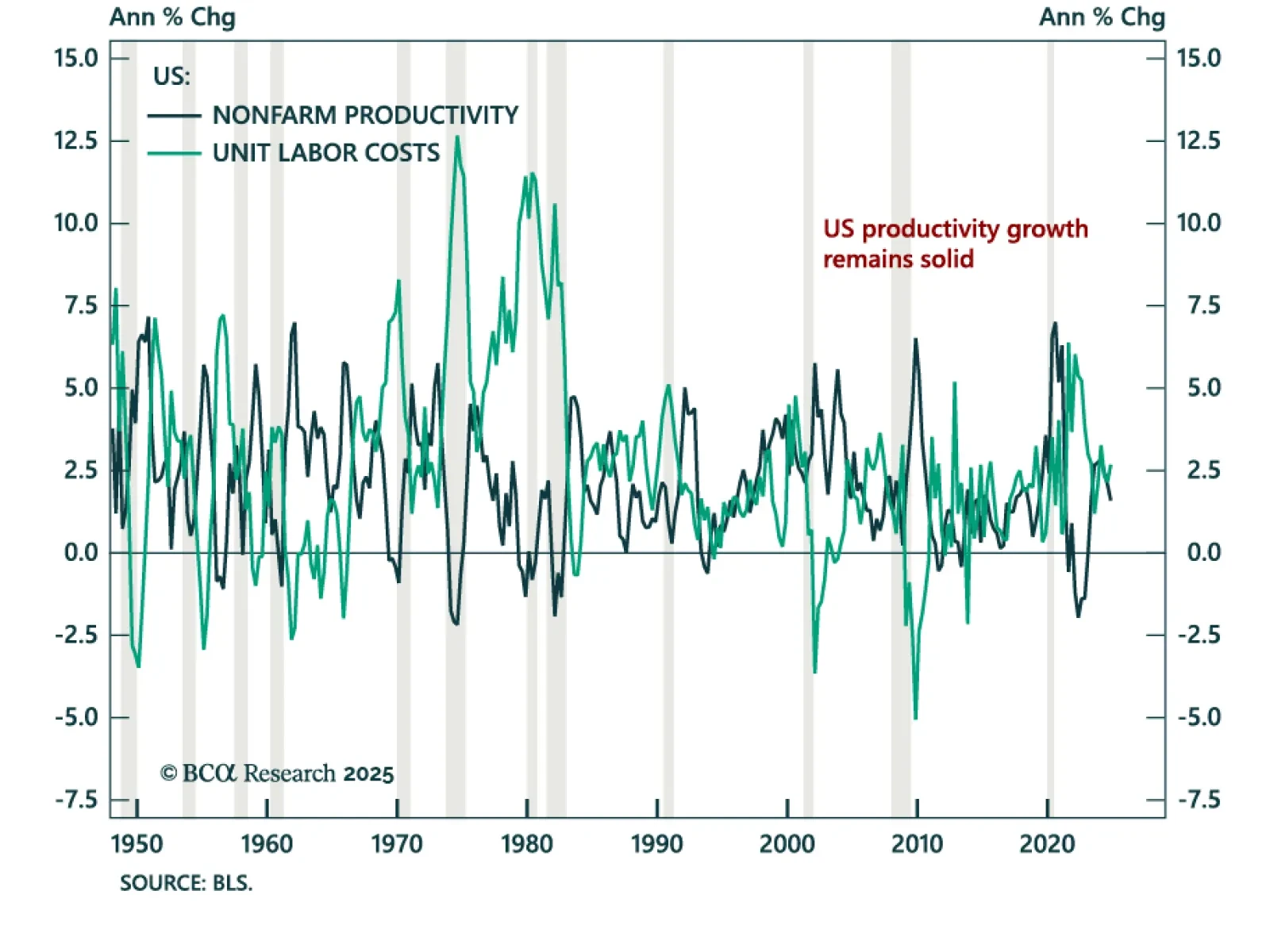

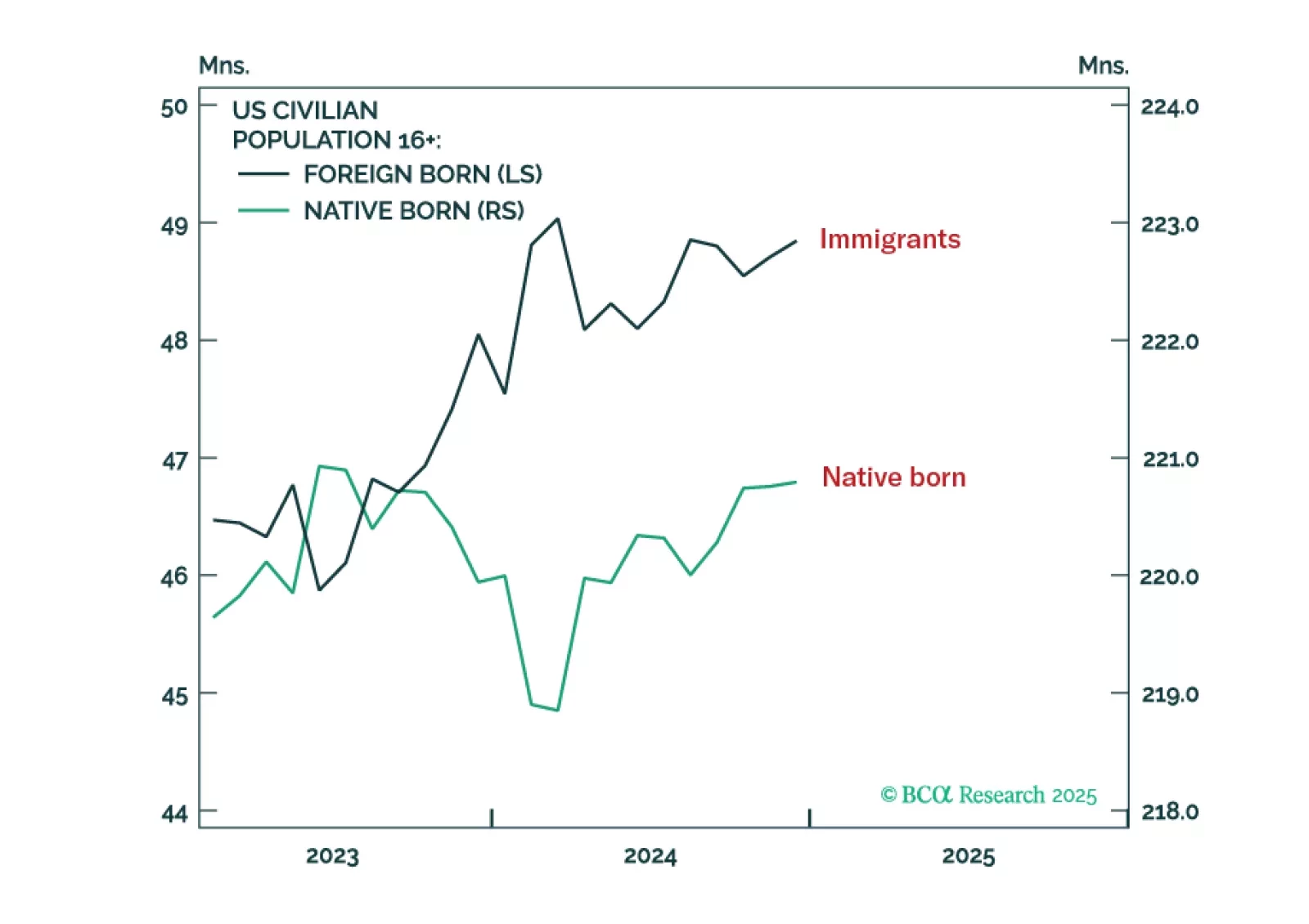

All the growth in the US labour supply since mid-2023 has come from immigration. This means if net immigration comes to a grinding halt, as Trump wants, it will hurt economic growth as well as keep the labour market supply-constrained. An increase in productivity growth could save the day, both to maintain growth and to kill inflation. Yet hopes that AI is about to usher an imminent and sustained boost to productivity growth are misplaced. Hence, expect a slowdown in US growth combined with inflation stuck close to 3 percent, a combination that I call a ‘mini stagflation’. We go through the investment implications. Plus: Tactically overweight Portugal versus Europe.