United States

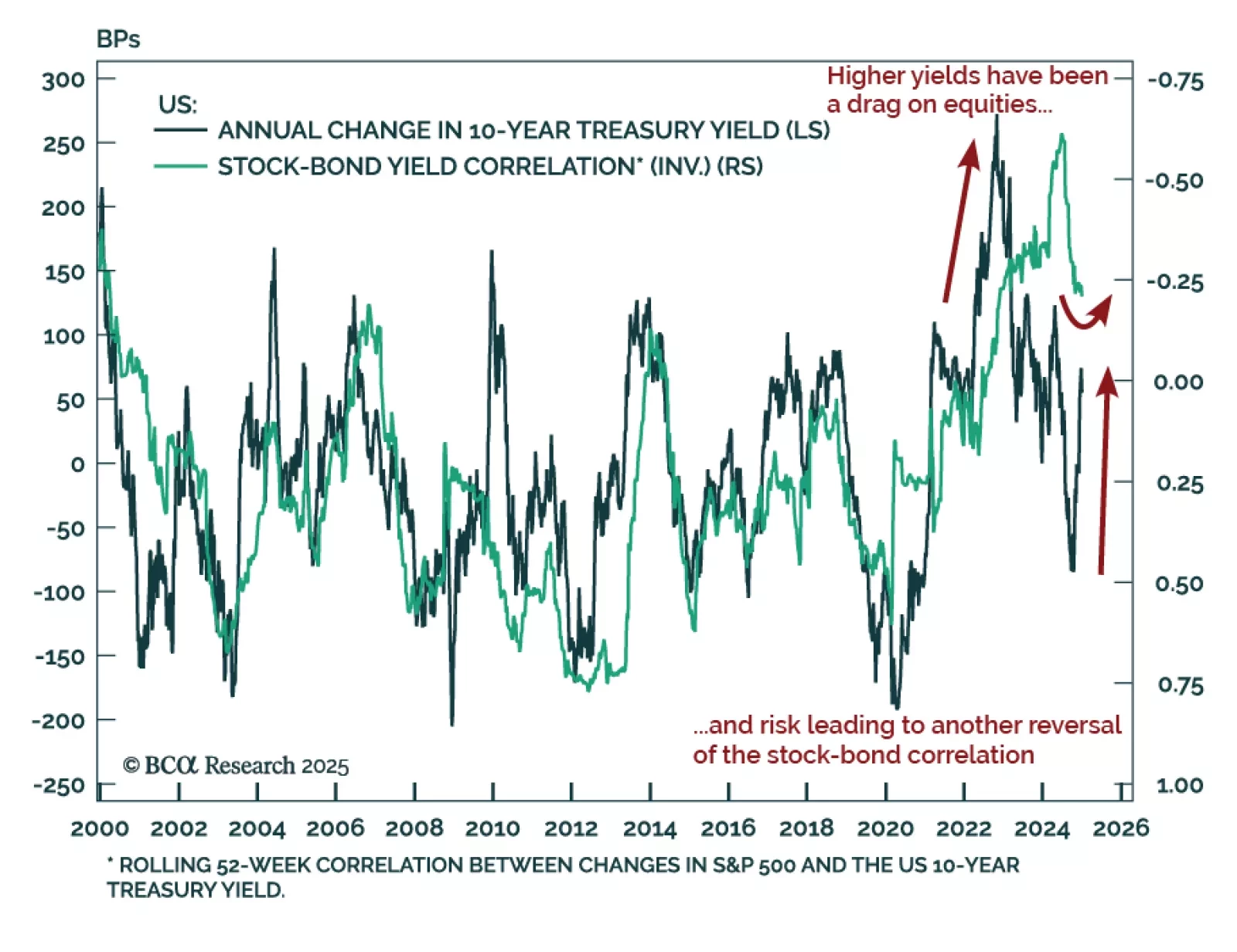

The post-COVID inflation impacted the most important cross-asset relationship: the stock-bond correlation. Higher inflation expectations pushed yields higher, leading to a correction in bond and stock prices. As price pressures receded, bond yields fell and…

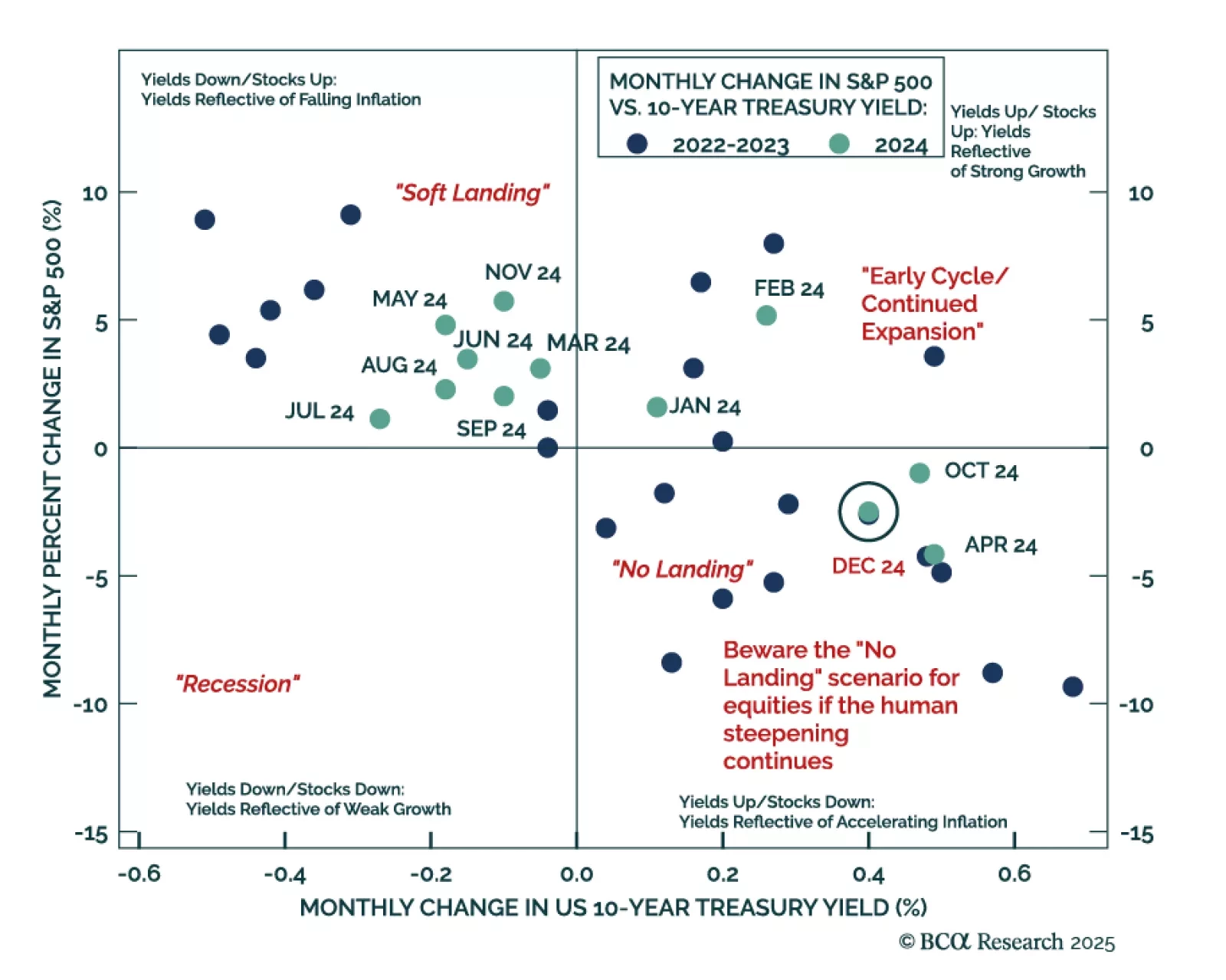

Our GeoMacro strategists published their Alpha Report, outlining their view that President Trump will have to pare back his fiscal ambitions to avoid a bond market riot. The long end of the US bond market continues to sell off, reinforcing our…

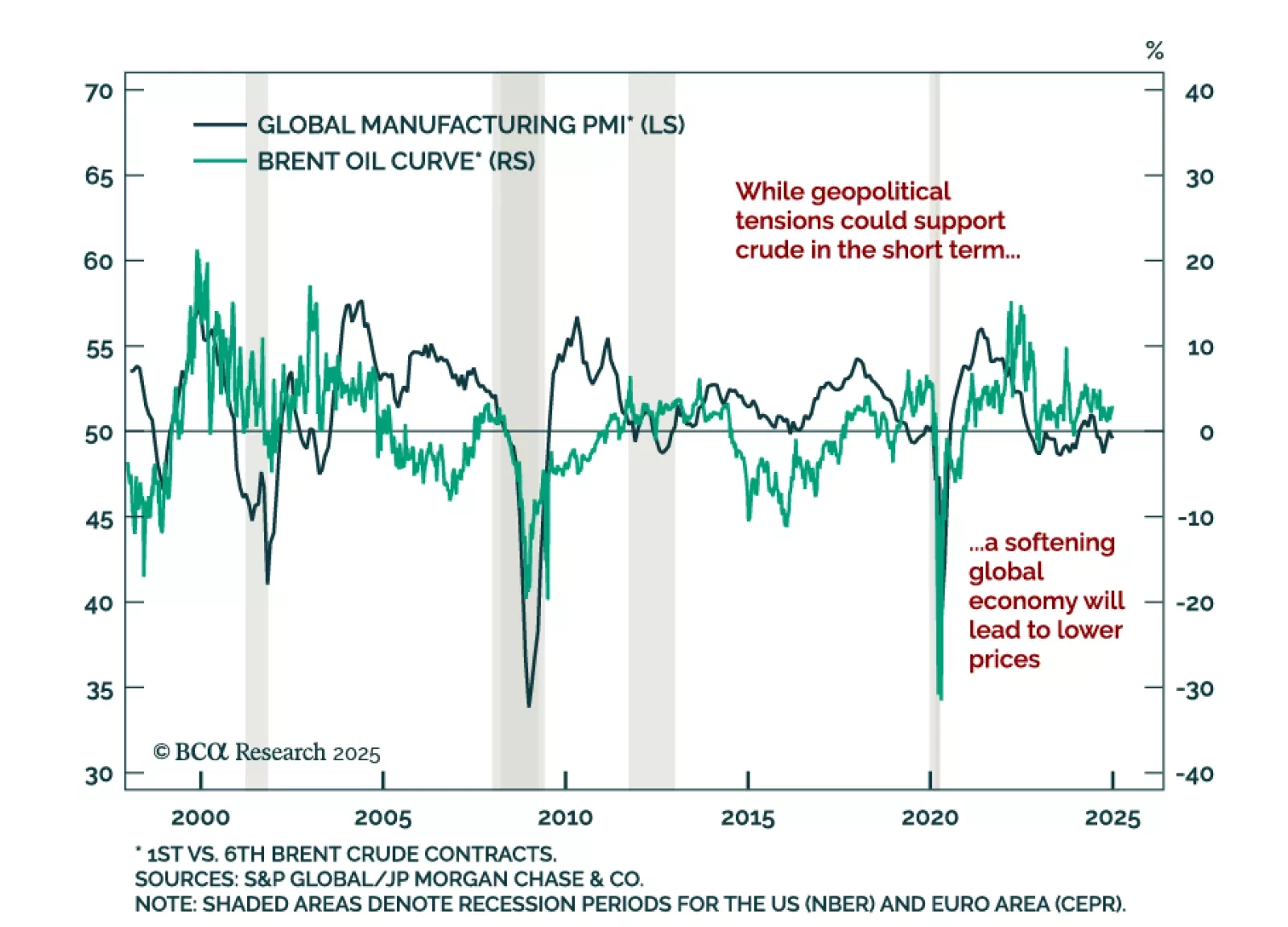

Oil prices have broken out above resistance from a tight trading range since the holidays. We attribute this latest rally to geopolitical tremors more than a vote of confidence from markets on global growth given softening data. The global economy is…

Our Portfolio Allocation Summary for January 2025.

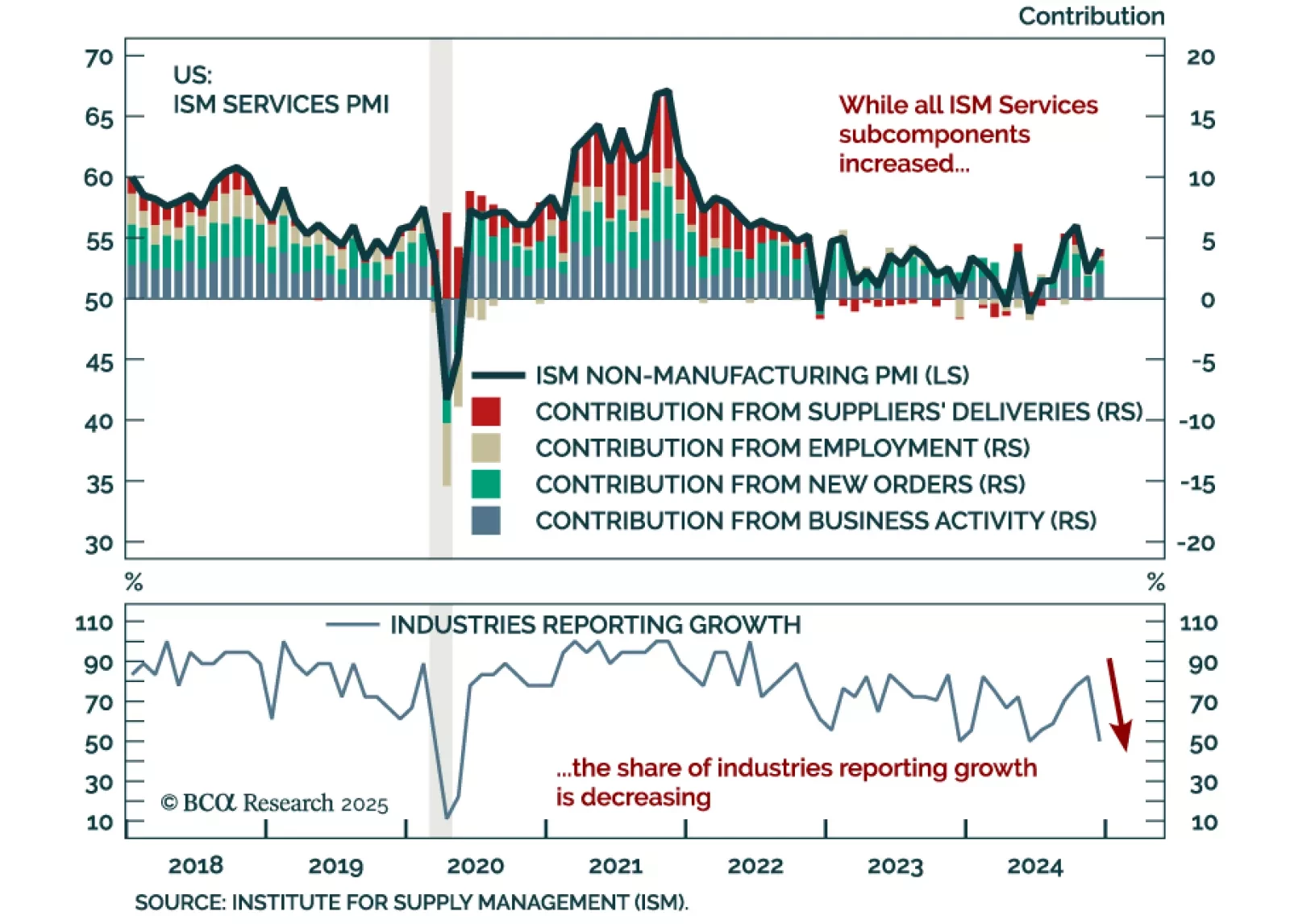

The December ISM Services PMI beat estimates, increasing to 54.1 from 52.1 in November. All subcomponents increased except for employment, which nonetheless remains in expansion. The prices paid component was especially strong, increasing to 64.4 from…

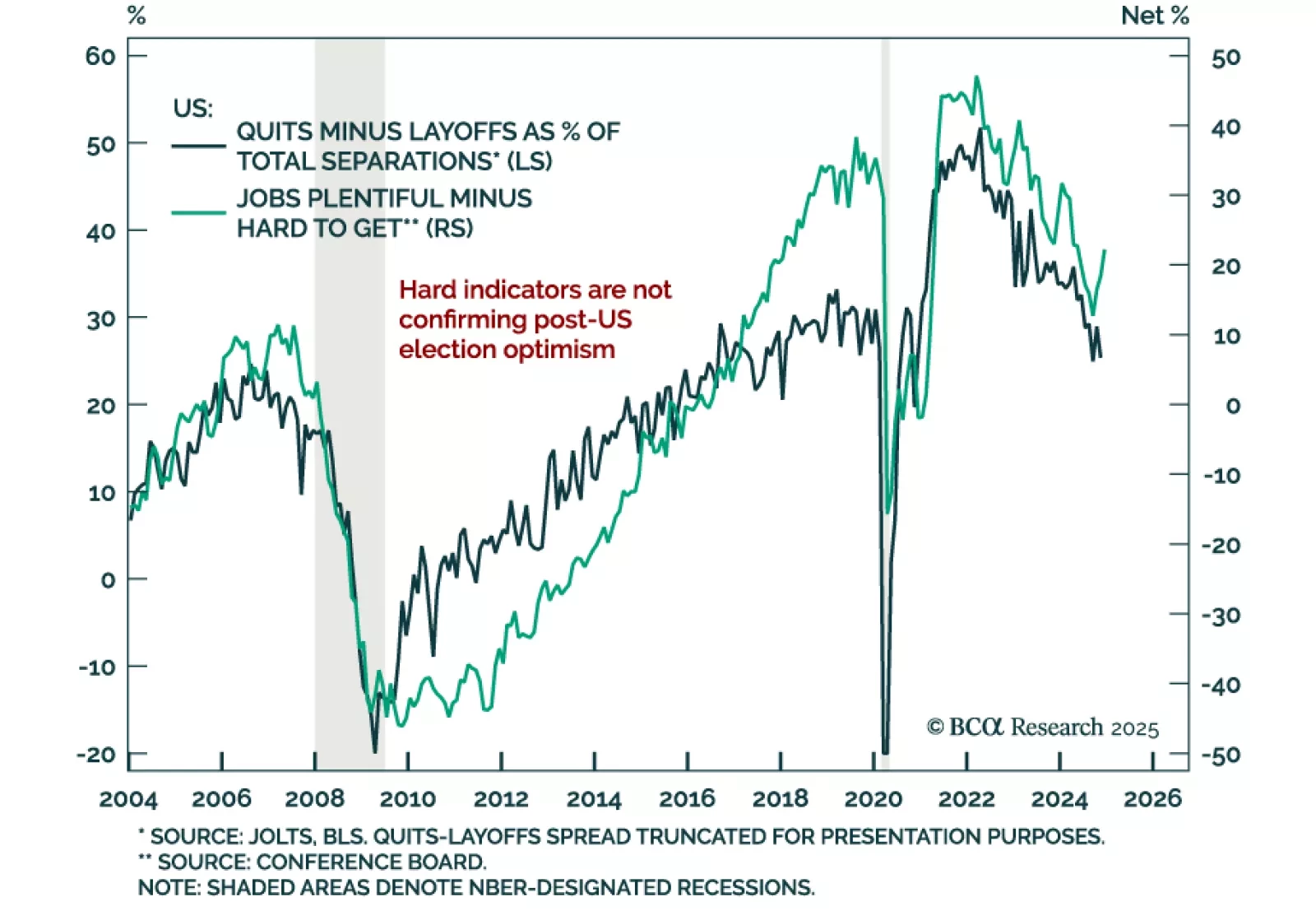

Job openings once again beat expectations in November, increasing to 8.1m from 7.8m in October. However, hires and quits decreased and layoffs increased. The gap between quits and layoffs, a leading indicator of labor market demand, ticked down. The jobs gap,…

Our Global Asset Allocation strategists published their monthly tactical asset allocation report, where they illustrate booming expectations in the US will be self-limiting. For the first time since 2022, US GDP growth is expected to start the year above…

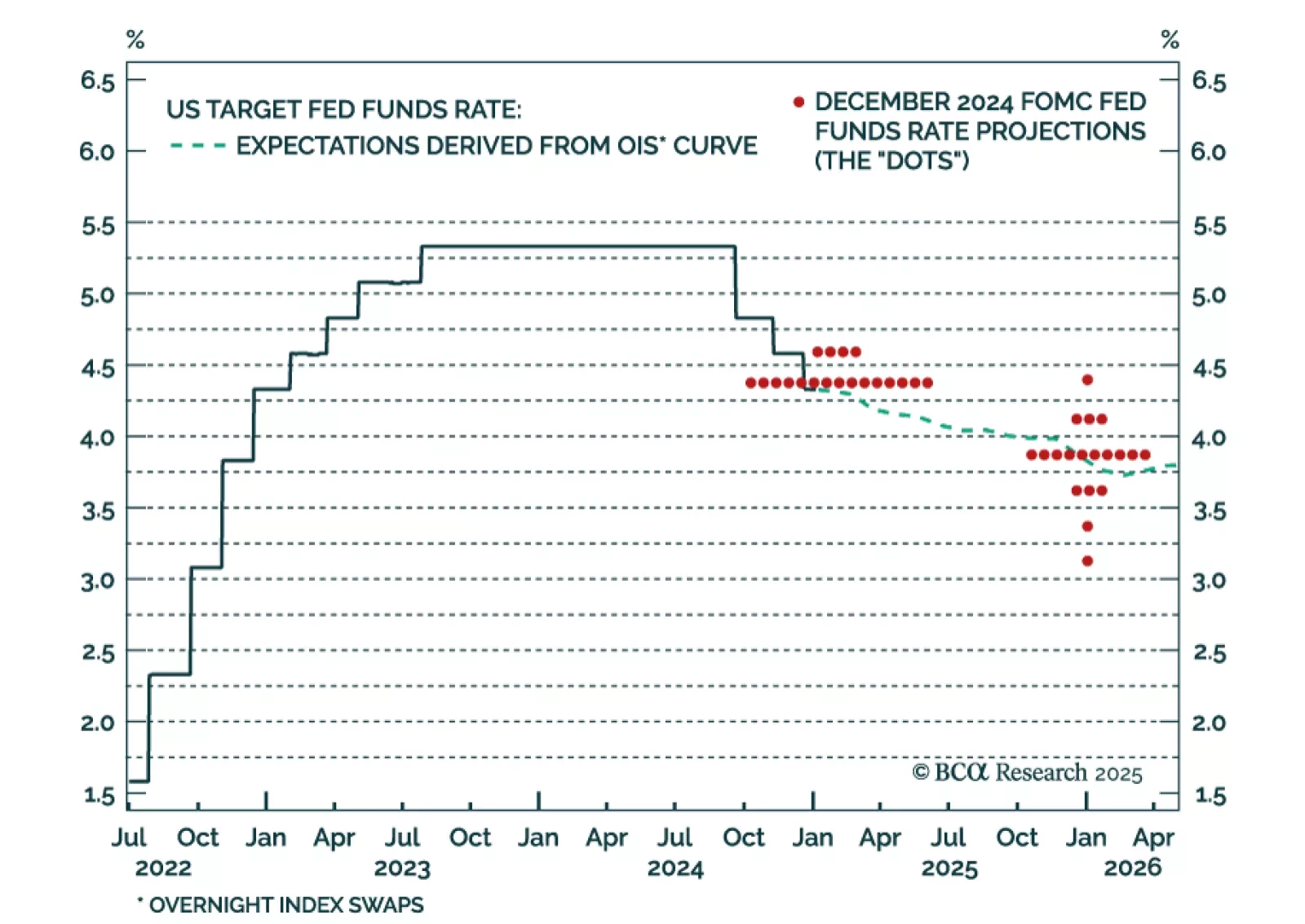

Our US Bond Strategy team published their outlook for the Fed in 2025. They expect more cuts than the 50 bps signaled by the Fed at its December meeting. Core PCE inflation is tracking well below the Fed’s 2.5% forecast, while unemployment could exceed…

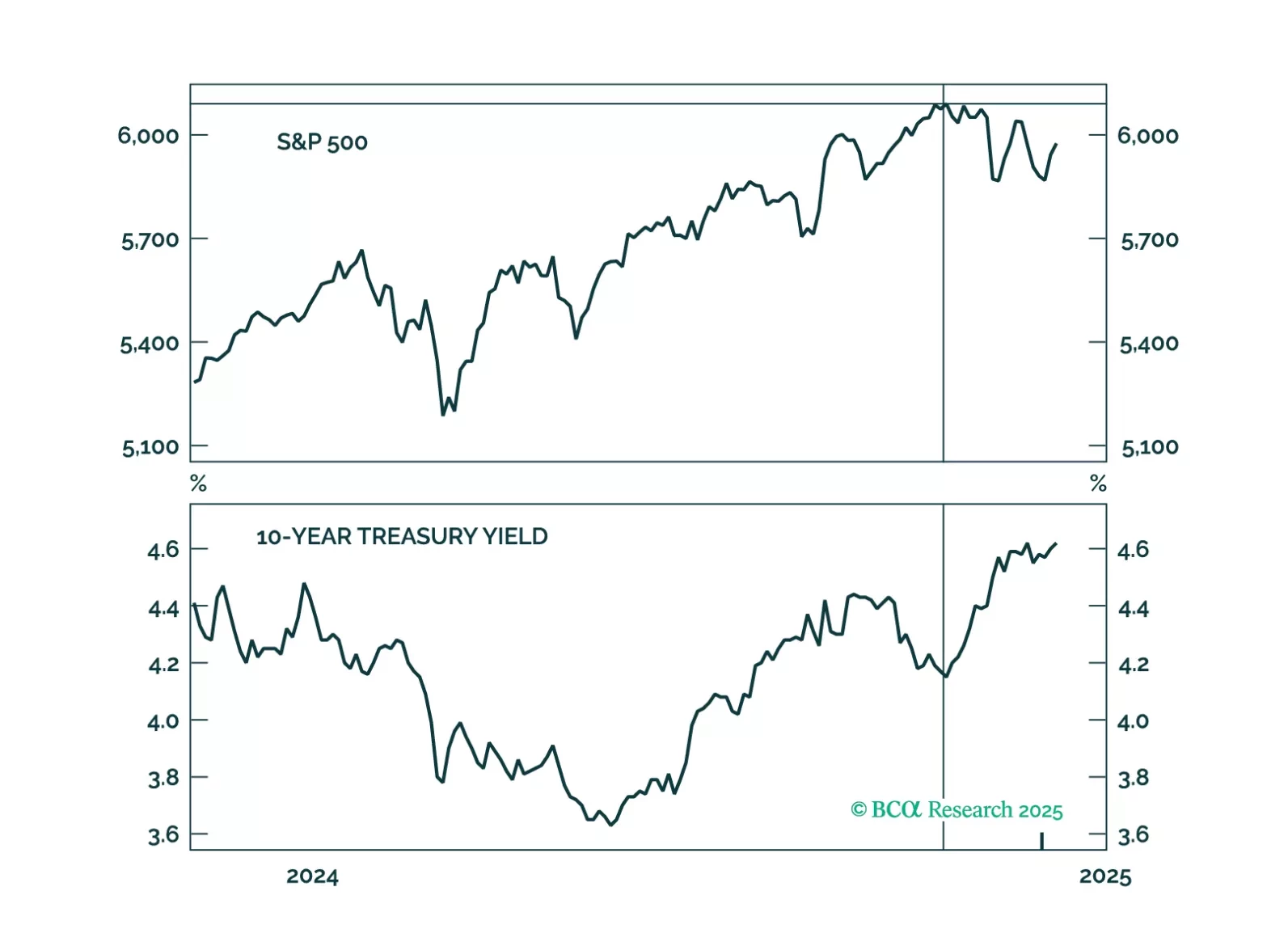

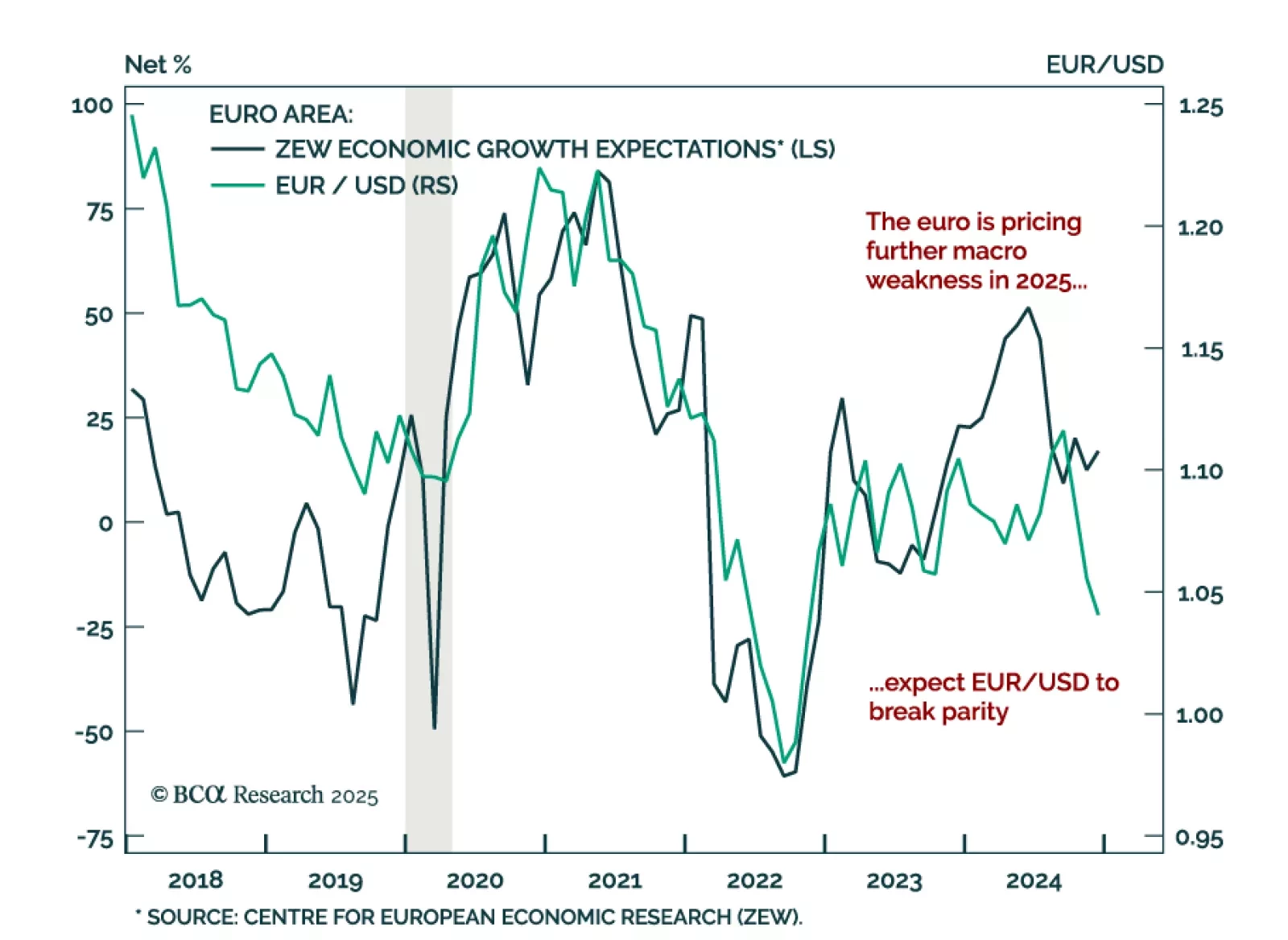

The euro broke the support level of its 2-year trading range against the USD, extending the strong dollar trend witnessed since September of last year. This trend will continue in Q1 2025. Despite global yields rallying in late 2024, the Bund-Treasury…

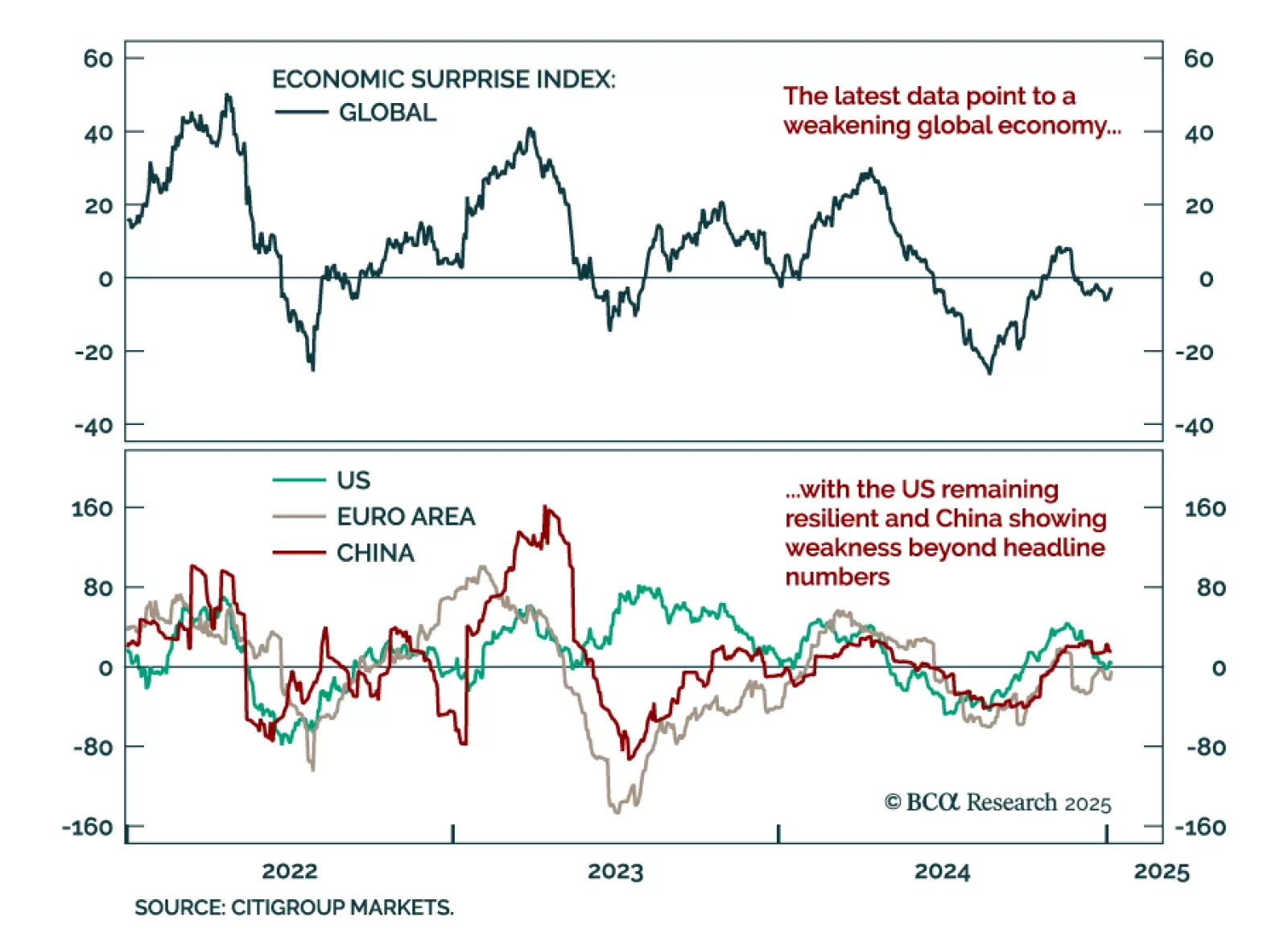

Economic data released over the holiday period extended recent trends, reflecting a softening global economy with resilient US growth, and an ailing manufacturing sector. The December global manufacturing PMI declined to 49.6 after reaching the 50 level…