United States

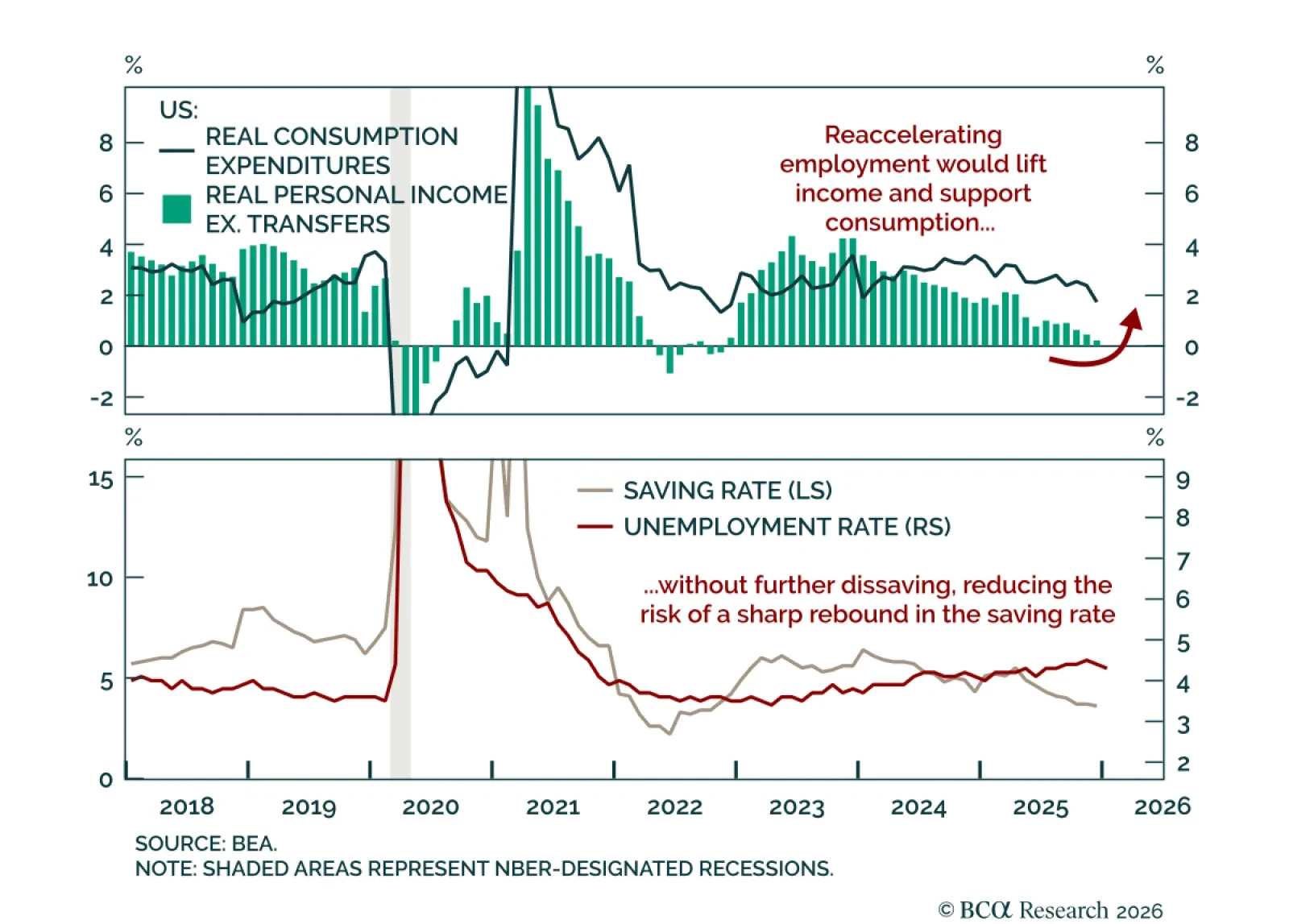

The December US Personal Income and Outlays report sent mixed signals. Real consumption slowed to 0.1% m/m from 0.2% in November, in line with expectations, while real income excluding transfers fell 0.1%. Spending was supported by dissaving, with the saving…

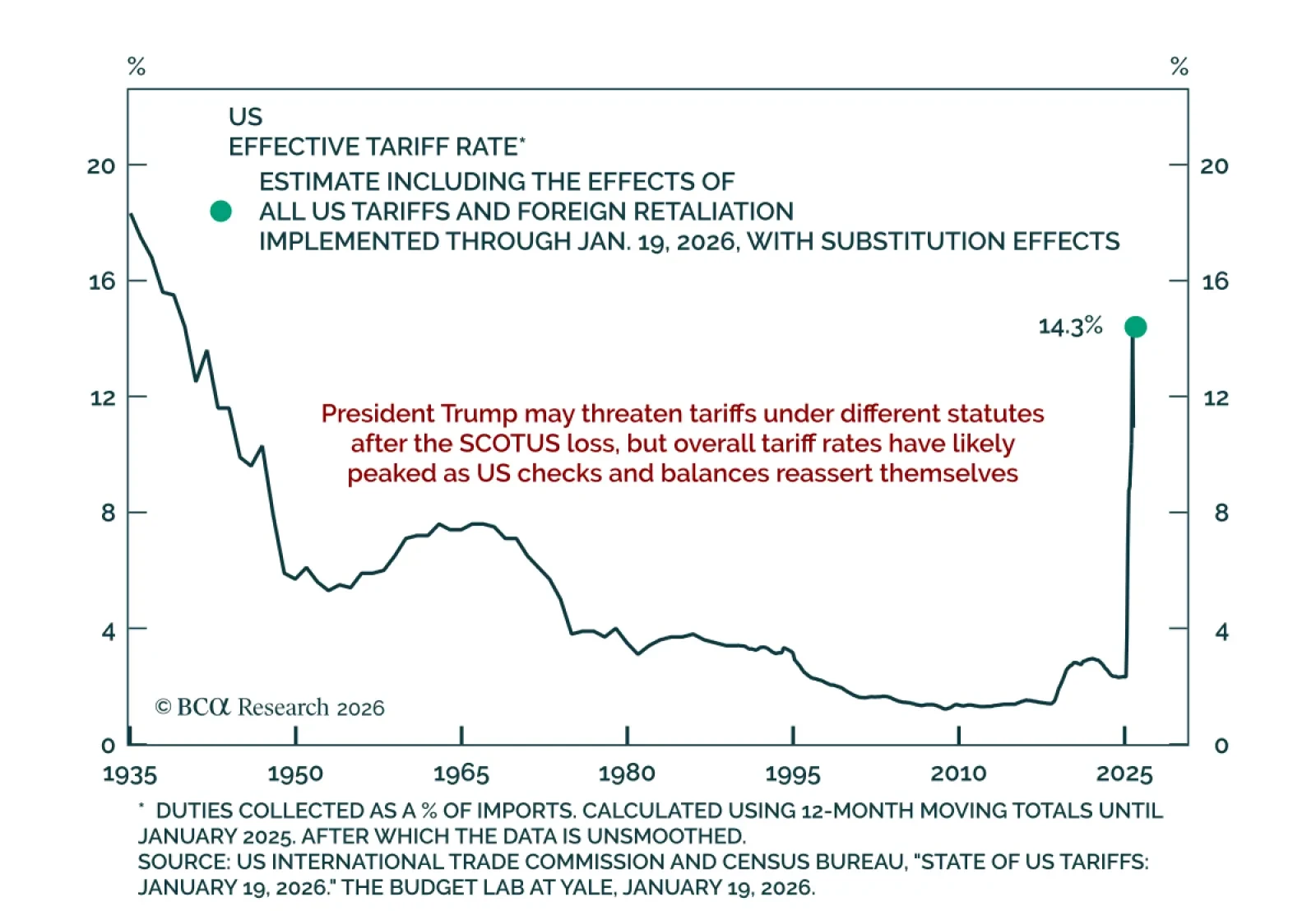

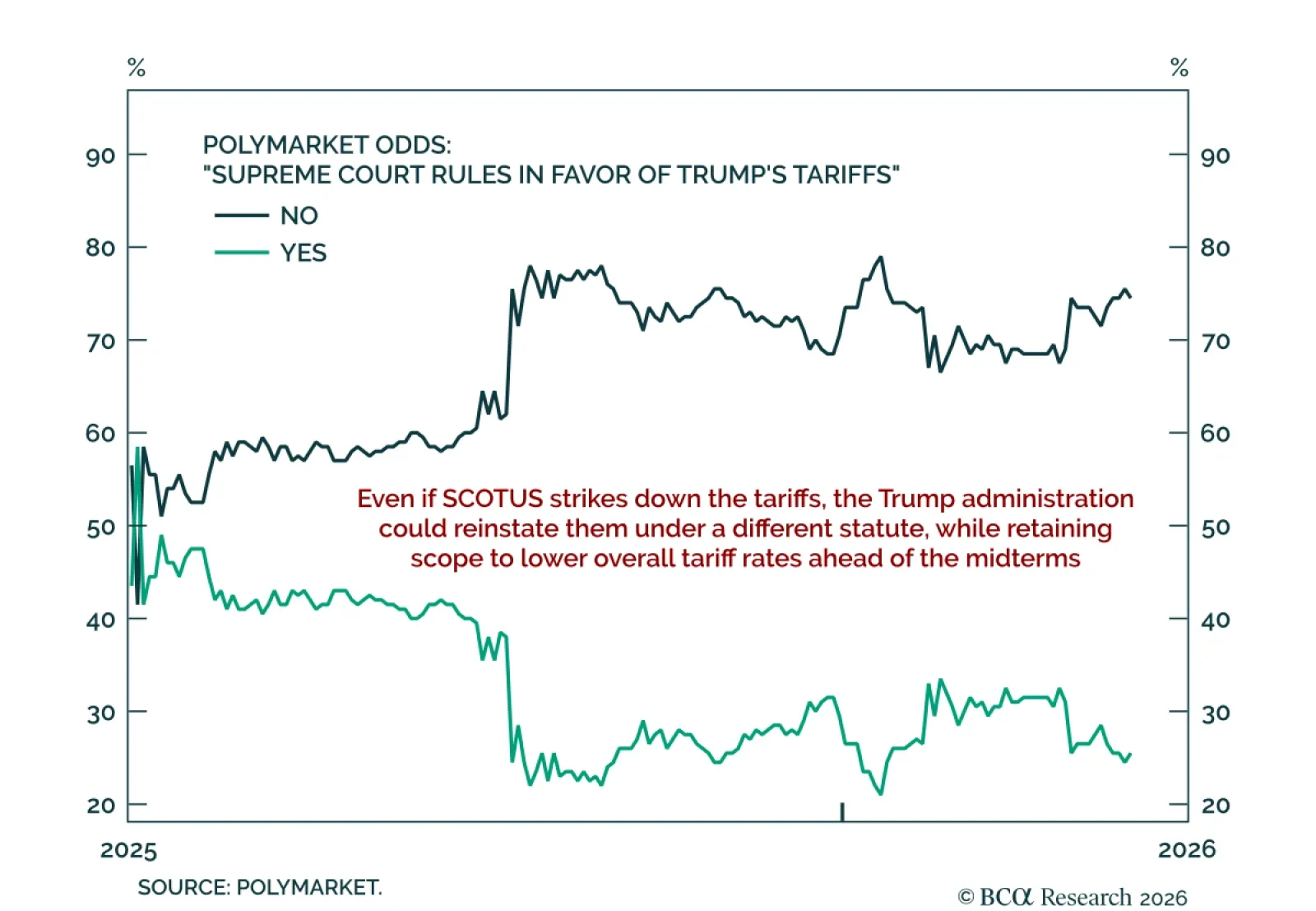

US checks and balances are still in place. The Supreme Court ruled against the Trump administration's use of sweeping tariffs under the International Emergency Economic Powers Act (IEEPA). Our US and Geopolitical strategists see different implications for the…

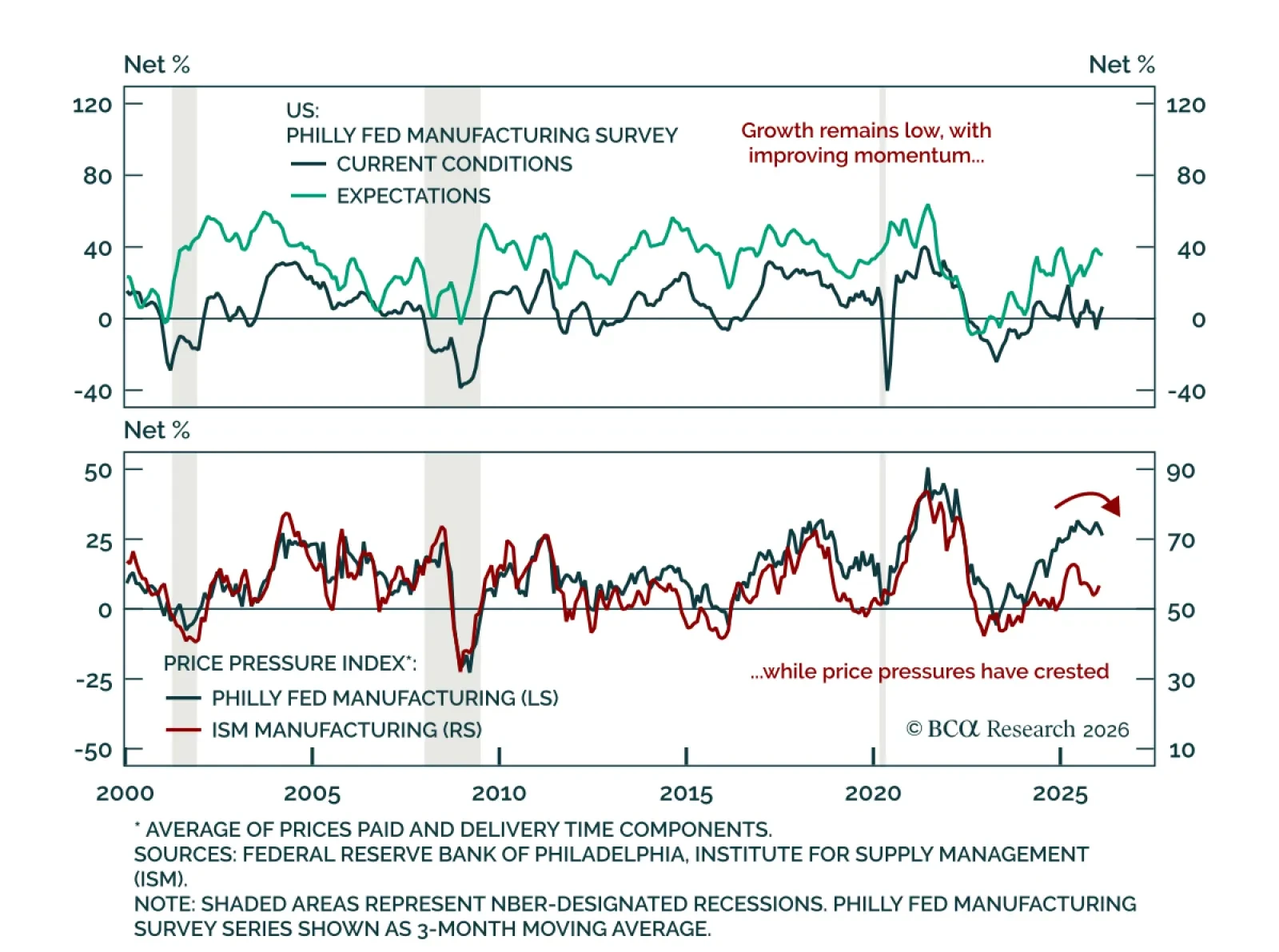

The February Philly Fed survey signaled expanding manufacturing activity alongside disinflationary pressures. The index rose to 16.3 from 12.6, beating estimates, and the general expectations measure also ticked up. Monthly manufacturing surveys are volatile,…

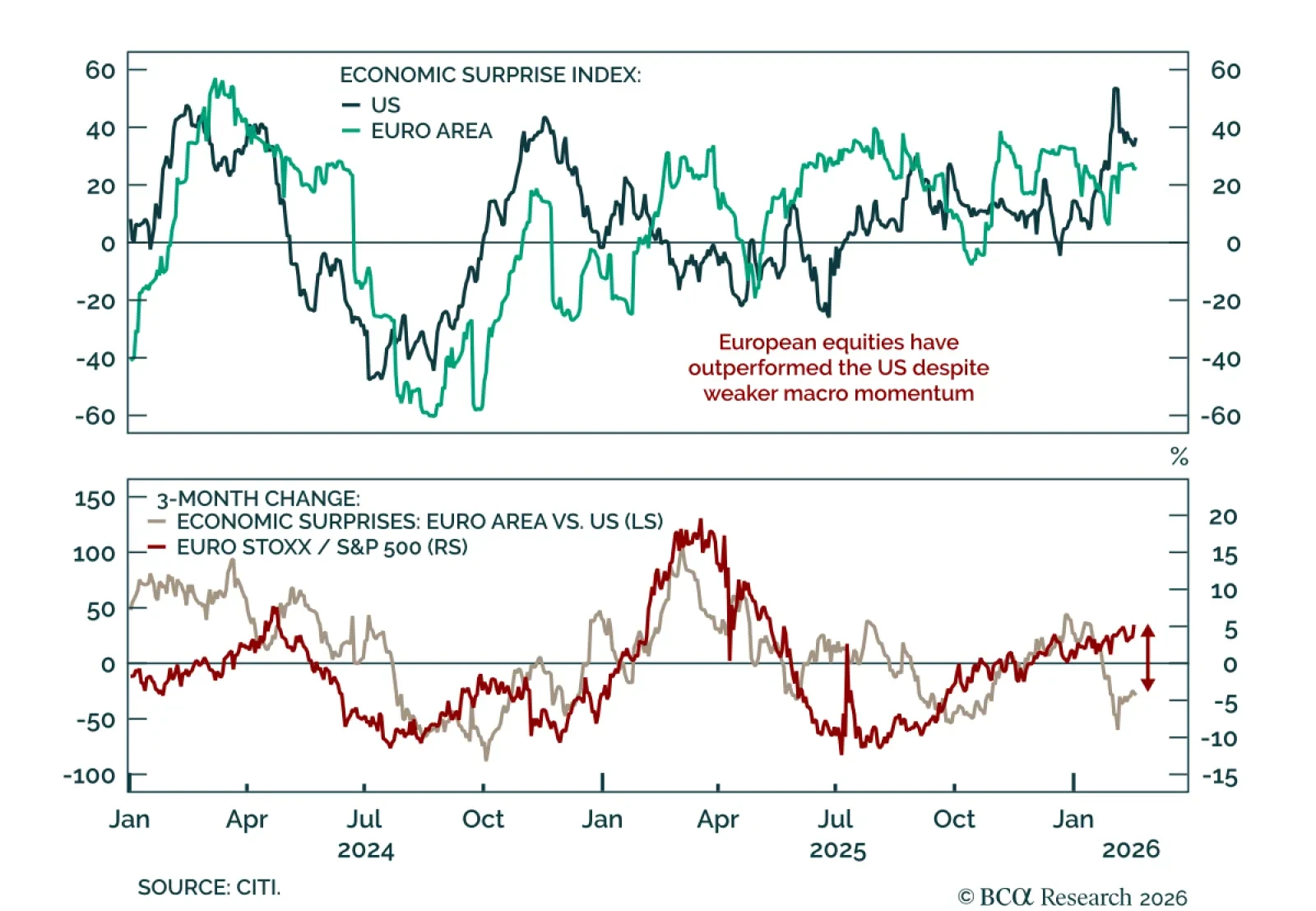

Relative macro momentum suggests scope for US tactical equity outperformance versus Europe. Just as macro momentum drives cross-asset returns, relative momentum helps explain cross-country equity performance. A simple measure is the difference in economic…

A Supreme Court strike-down of tariffs could still leave scope for President Trump to reinstate them under different statutes, while allowing a net reduction in tariff rates ahead of the midterms. Barring any major data surprise or US strikes on Iran, the…

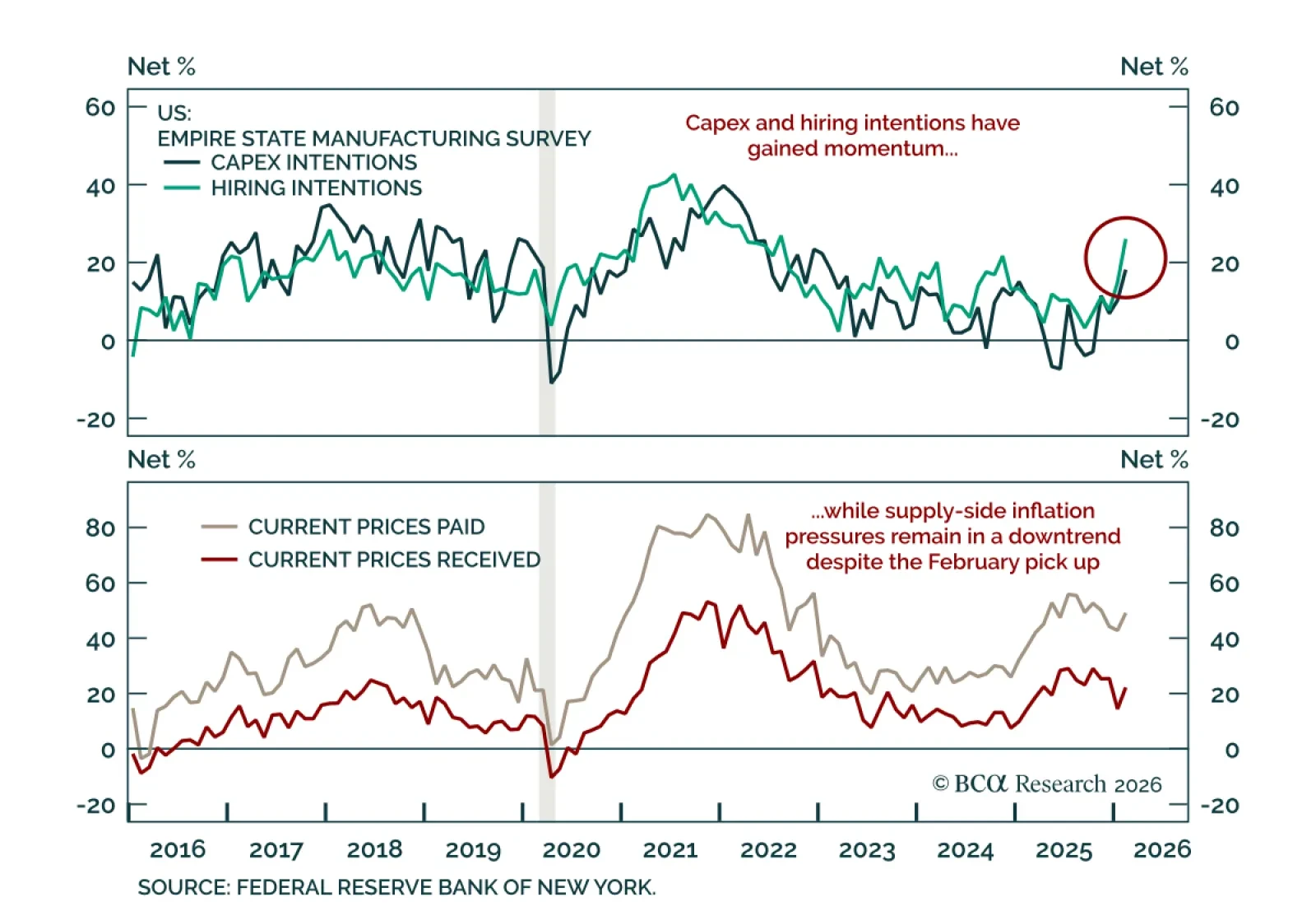

The February Empire survey points to expanding manufacturing activity, adding to signs of improving macro momentum. The headline index was little changed at 7.1 and slightly beat estimates. New orders moderated but remained in expansion, while shipments…

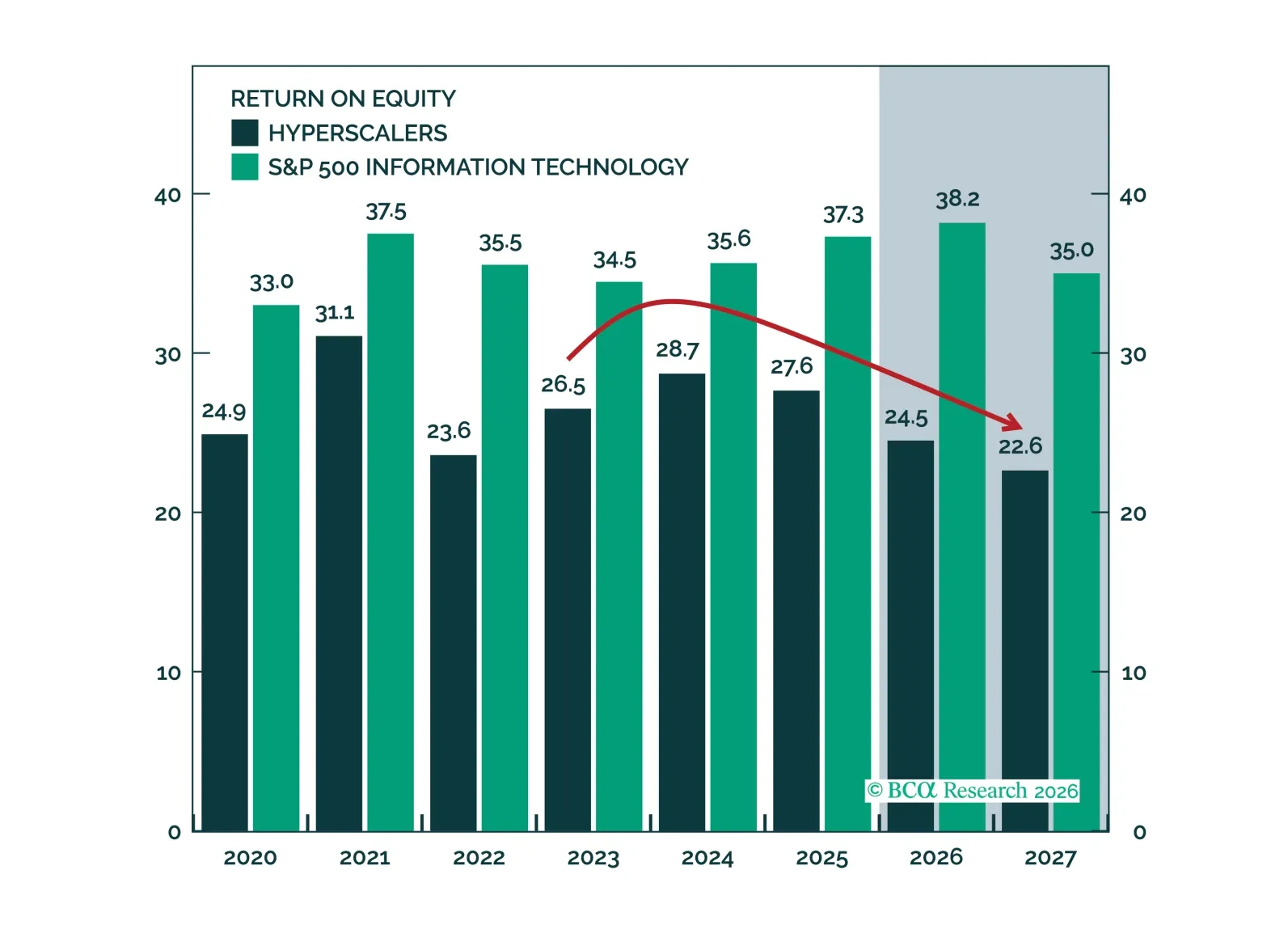

The capex debate is better framed not as boom versus bubble, but as around capacity, leverage, and cash conversion. ROEs have compressed, but revenue growth and margin expansion offer a credible path back. Spenders likely have time to make good on their investments, though the market’s leash may be shorter than anticipated.

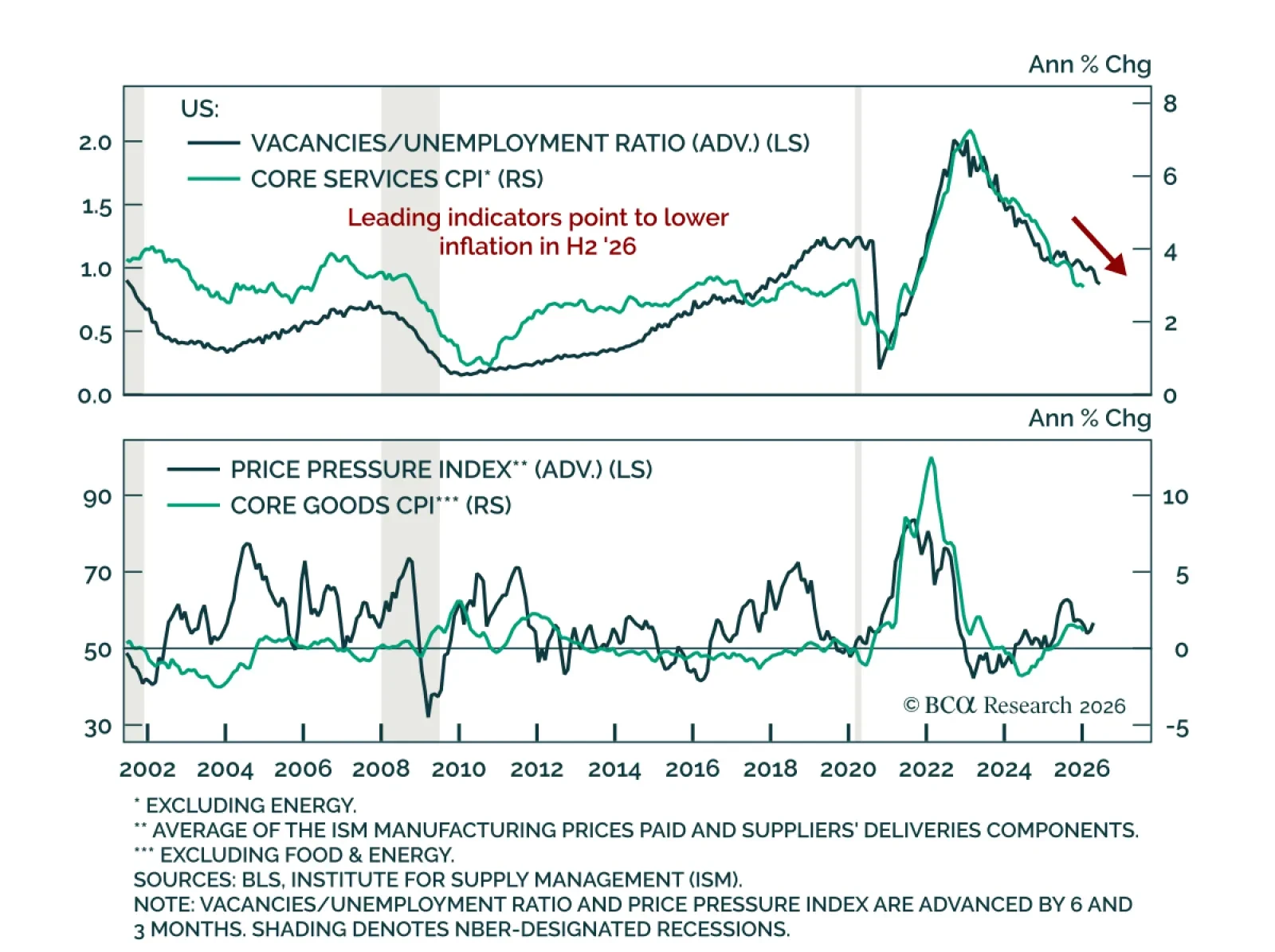

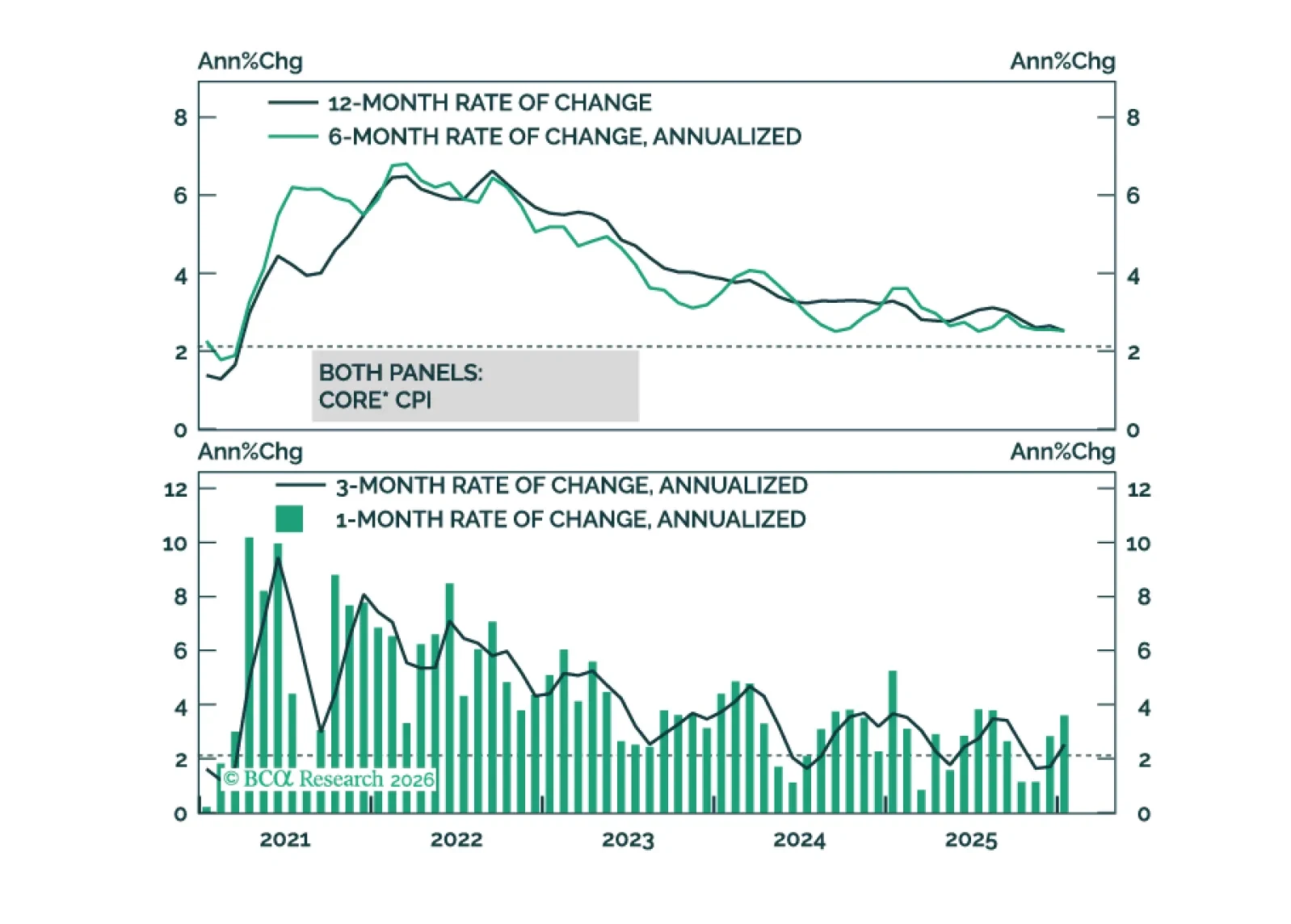

January US CPI cooled slightly, with leading indicators pointing to further disinflation later this year. Headline inflation fell to 2.4% y/y in January from 2.7%. Similarly, core also cooled to 2.5% from 2.6%, in line with estimates. Core goods inflation…

Core inflation will get close to the Fed’s 2% target by the end of this year.

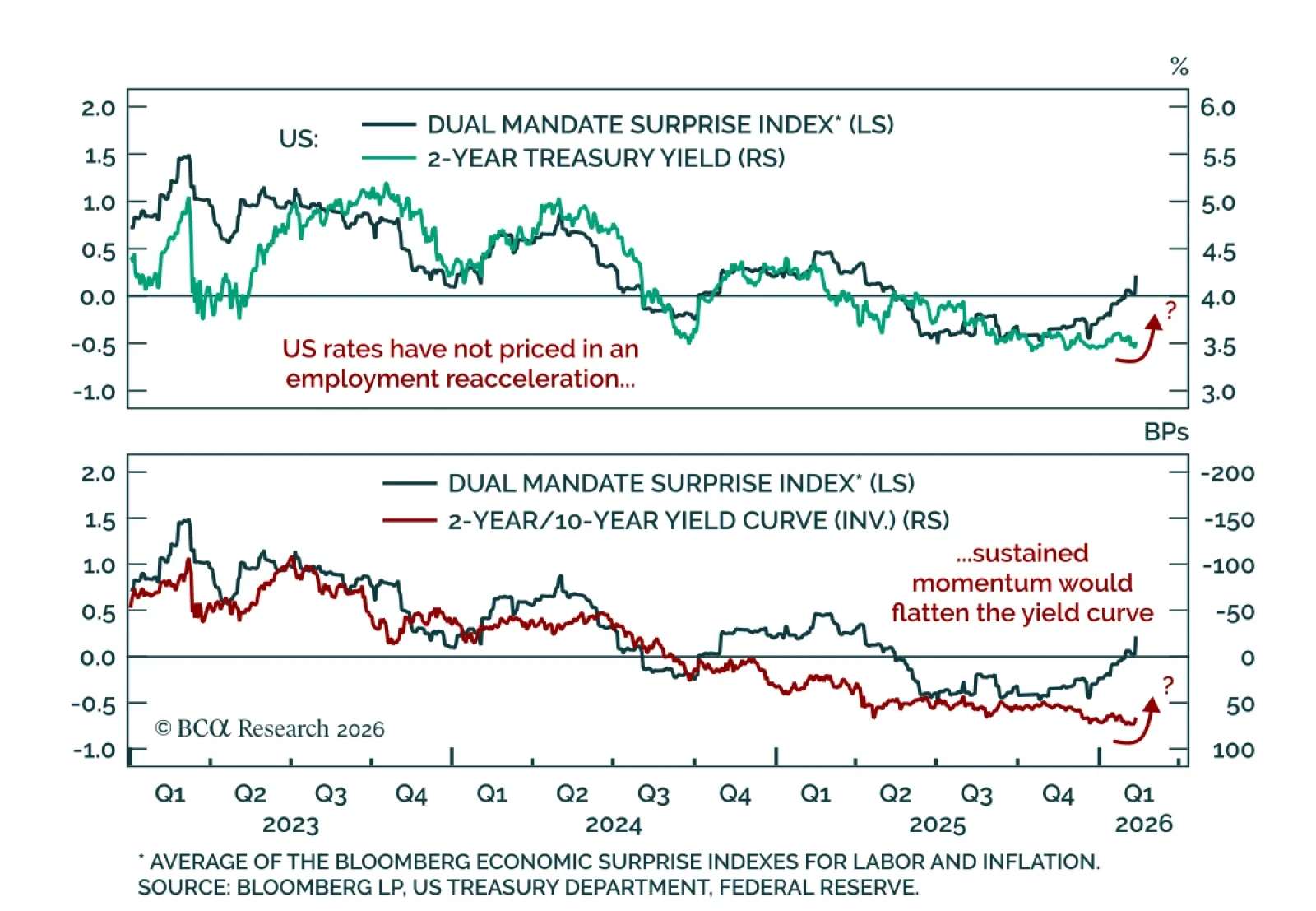

January’s upside jobs surprise creates a risk for our long duration and steepeners recommendations for US bond portfolios. The employment report exceeded expectations, hinting at rebounding job growth and stabilizing labor market utilization. This was…