United States

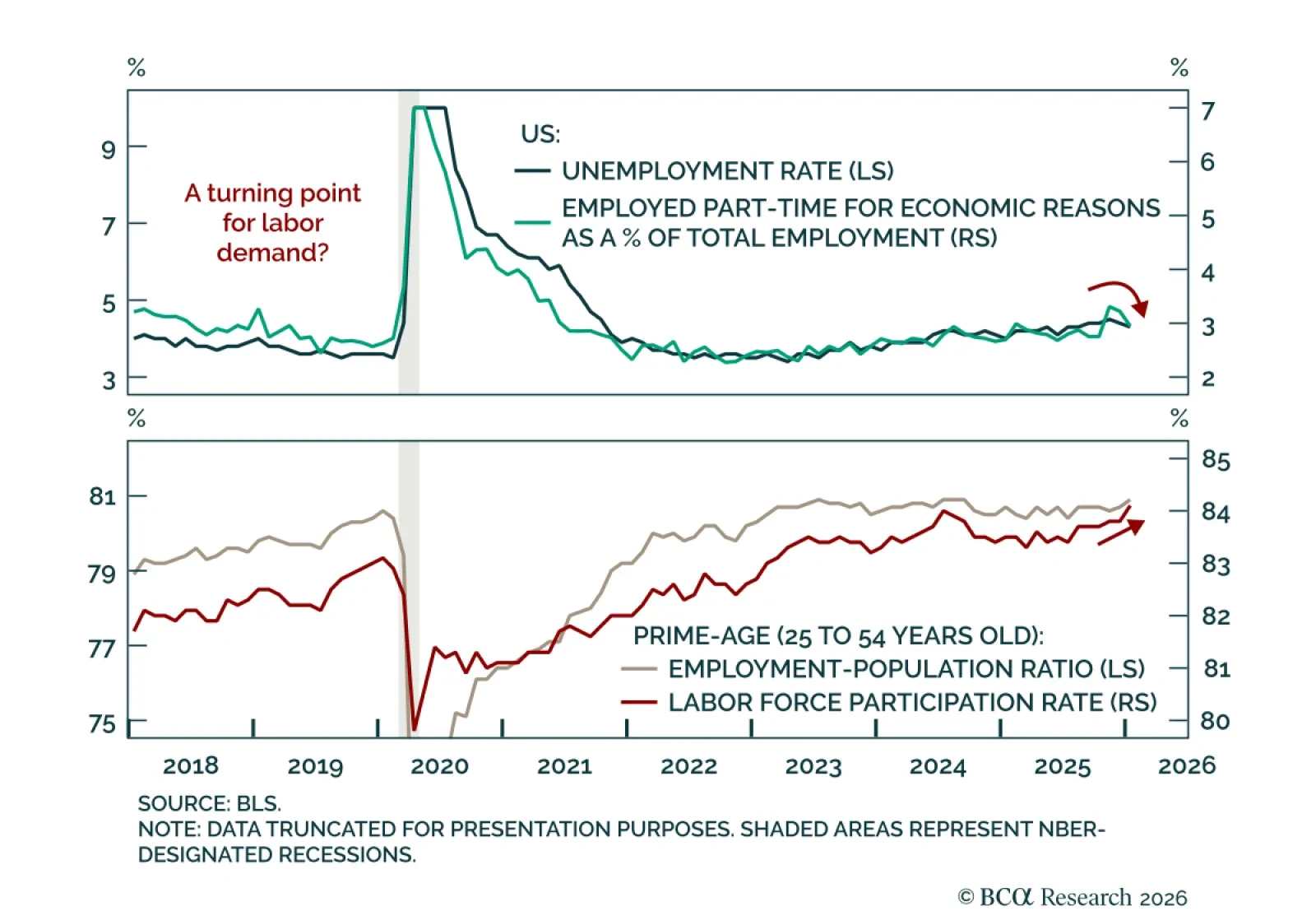

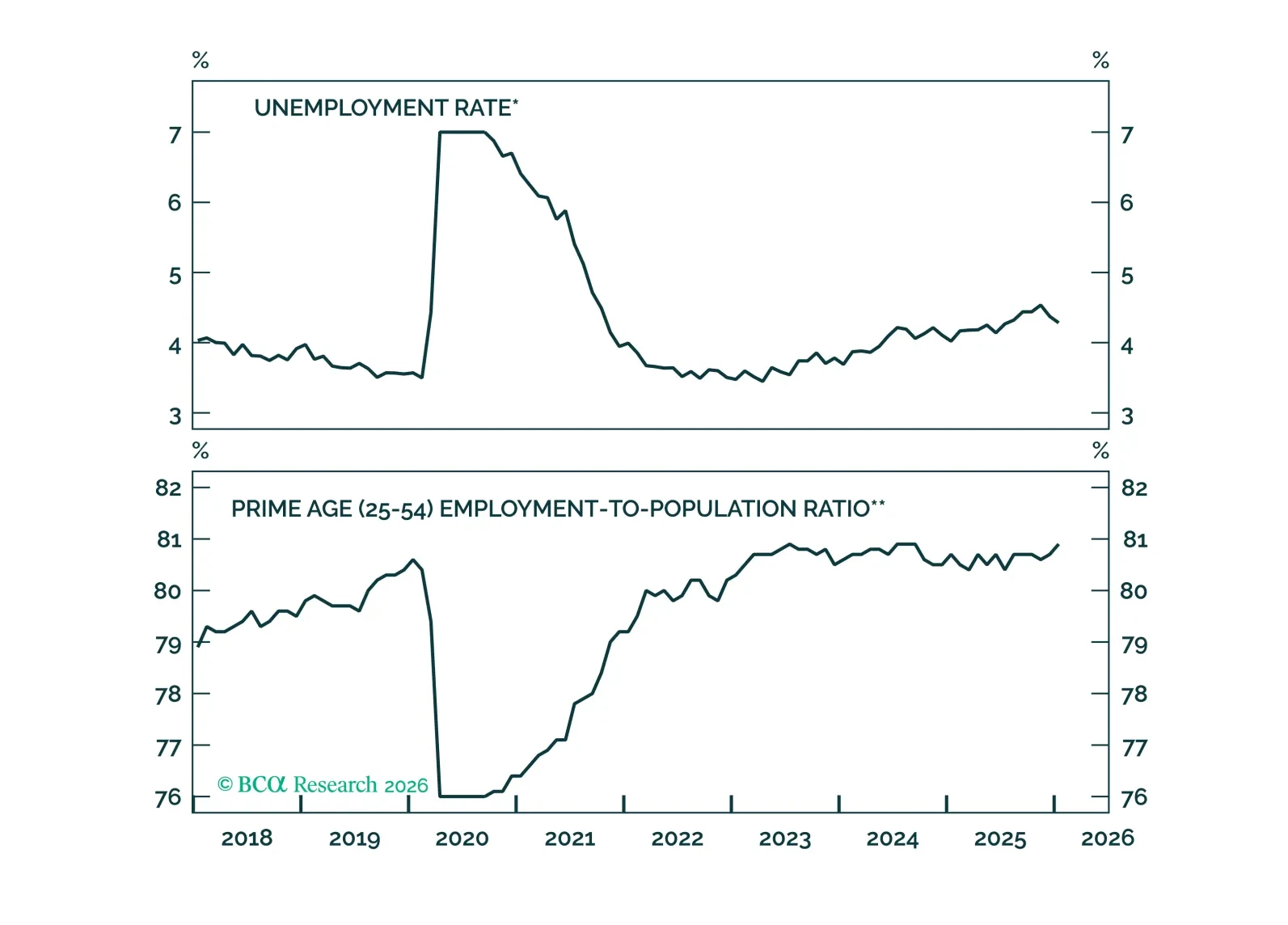

The January employment report exceeded expectations, pointing to a genuine pickup in labor demand and reducing the urgency for near-term Fed easing. Nonfarm payrolls rose 130k, up from 48k in December. Net revisions to November and December lowered payrolls…

The labor market tightened in January, significantly lowering the odds of a H1 2026 rate cut. Rate cuts driven by lower inflation are still likely in H2 2026.

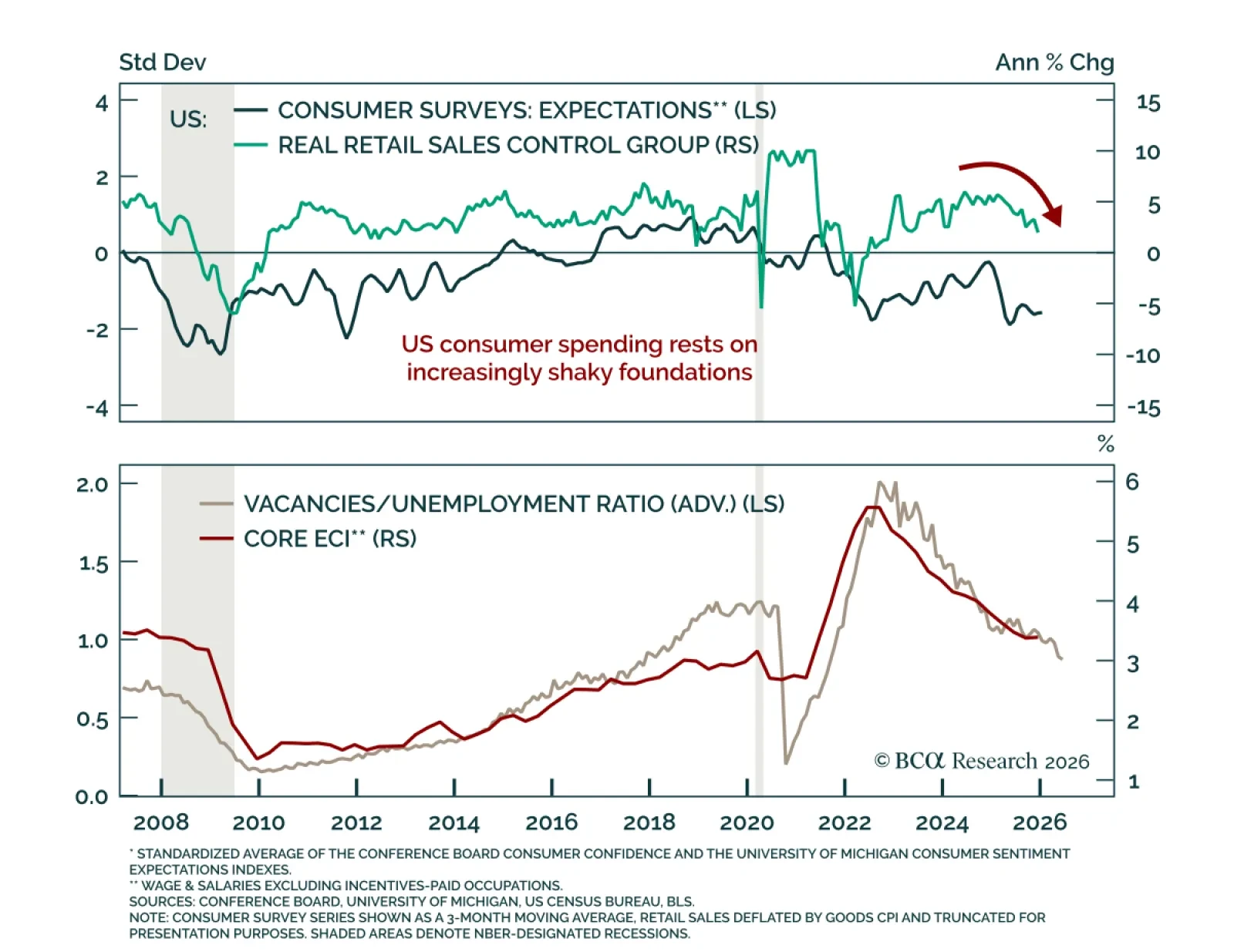

US retail sales point to growing consumer weakness. December US retail sales missed expectations across the board and slowed from November. The headline and core measures excluding gas and/or autos were flat, while the control group used to calculate GDP fell…

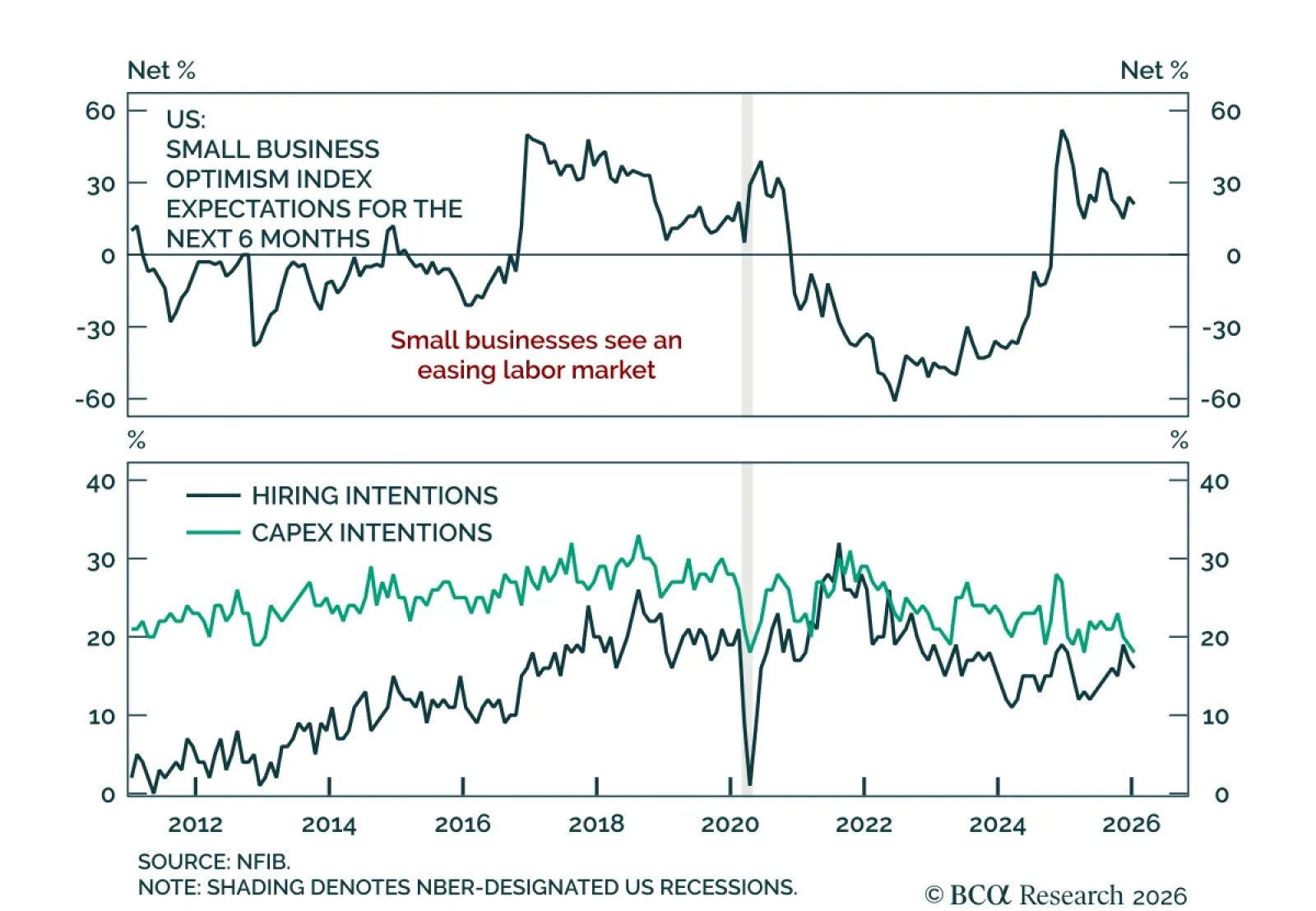

The January NFIB survey points to broad-based weakness among small businesses, reinforcing signs of easing labor market conditions amid mixed growth signals. The January NFIB Small Business Optimism Index missed estimates, easing to 99.3 from 99.5 in…

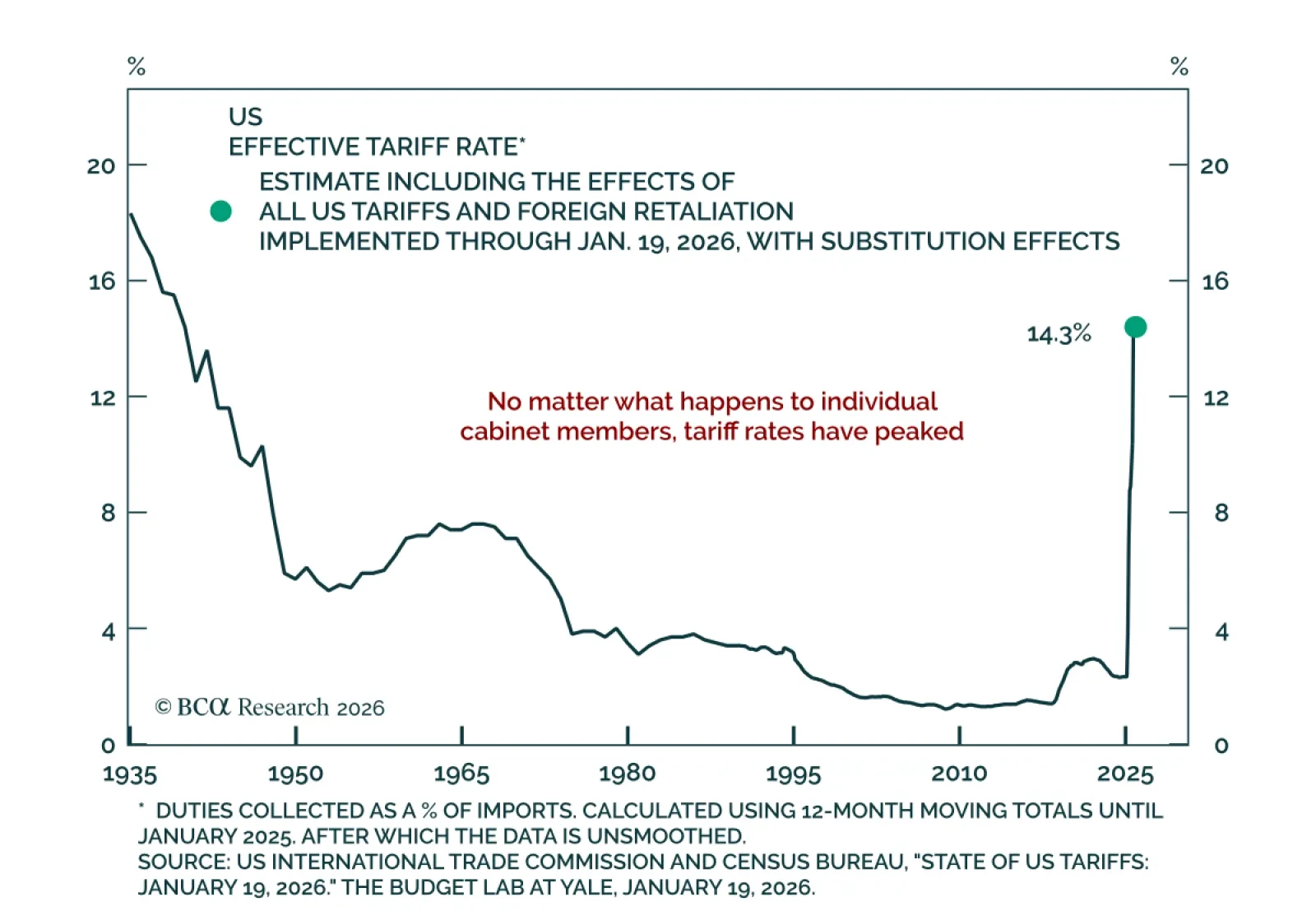

Rumors around the possible exit of Commerce Secretary Howard Lutnick are unlikely to materially alter the trajectory of US trade policy. While the Epstein scandal is widening across US and UK politics, our US Political strategists caution against…

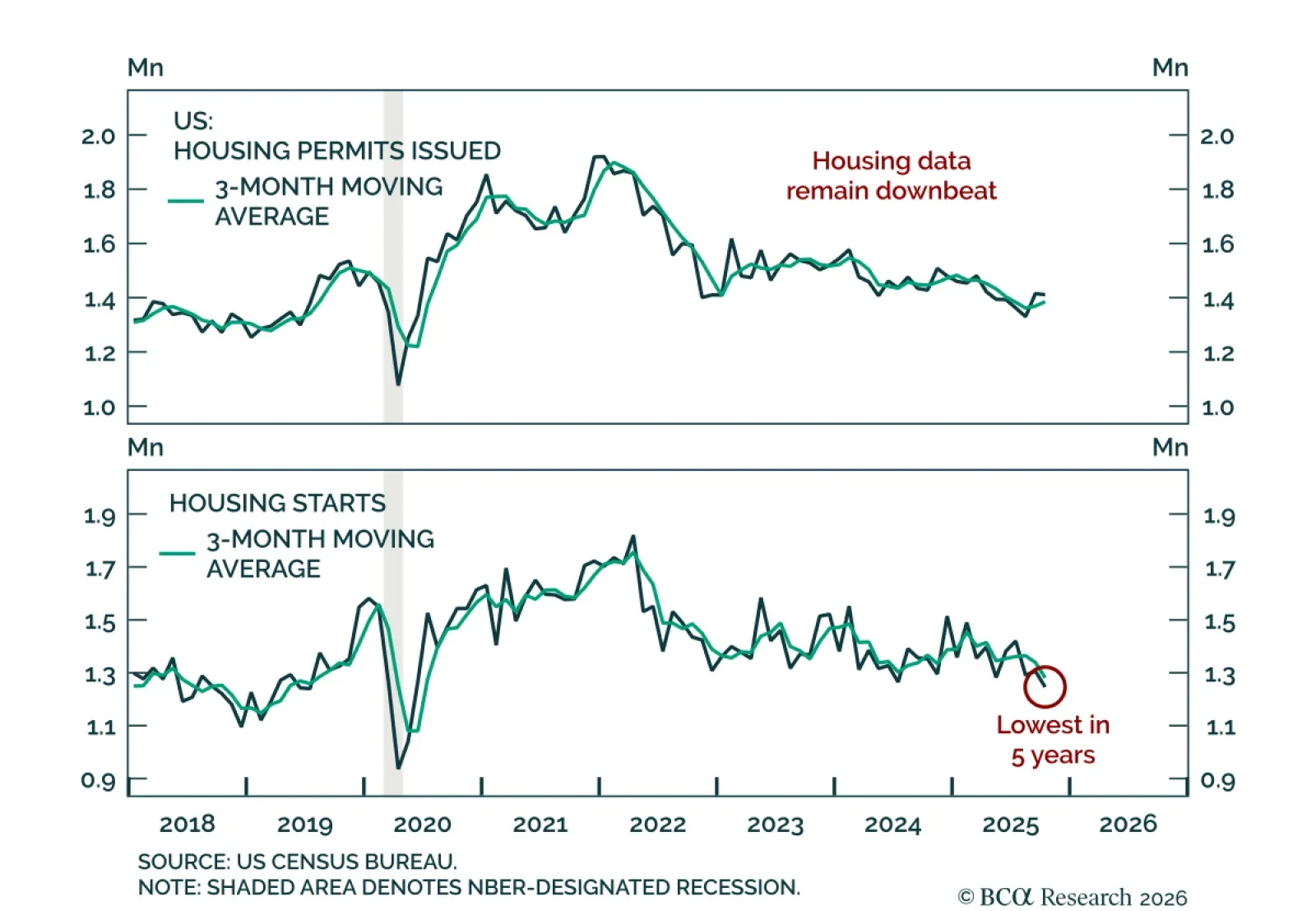

Our Global Investment strategists argue it remains too early to bet on housing becoming a key driver of US economic growth this year. The residential real estate market remains soft, and unlike the AI boom, residential investment was a drag on growth in…

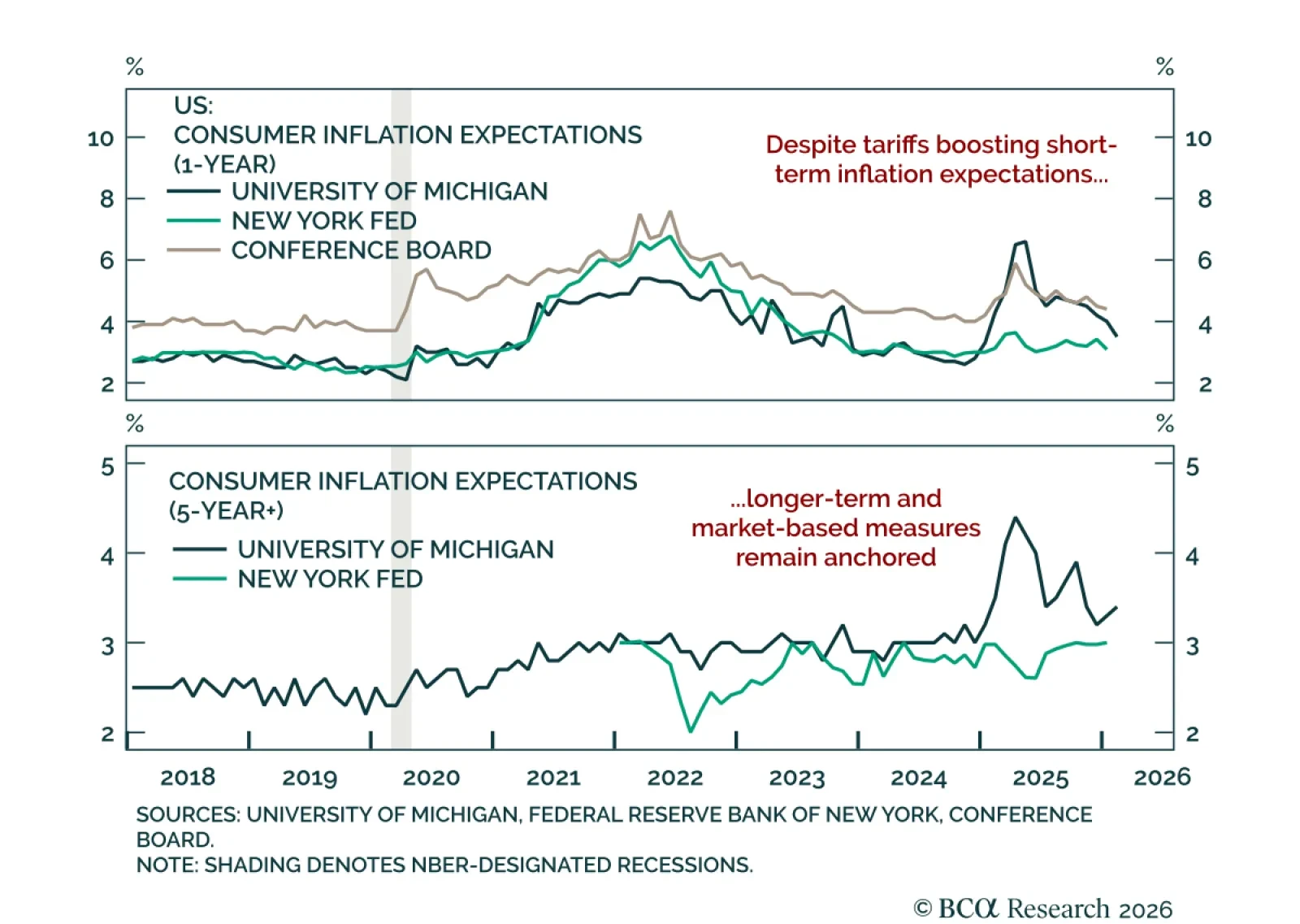

US inflation expectations remain well anchored, preserving policy flexibility as labor market risks stay elevated. The NY Fed’s January Survey of Consumer Expectations showed a decline in 1-year inflation expectations, while 3-year and 5-year expectations…

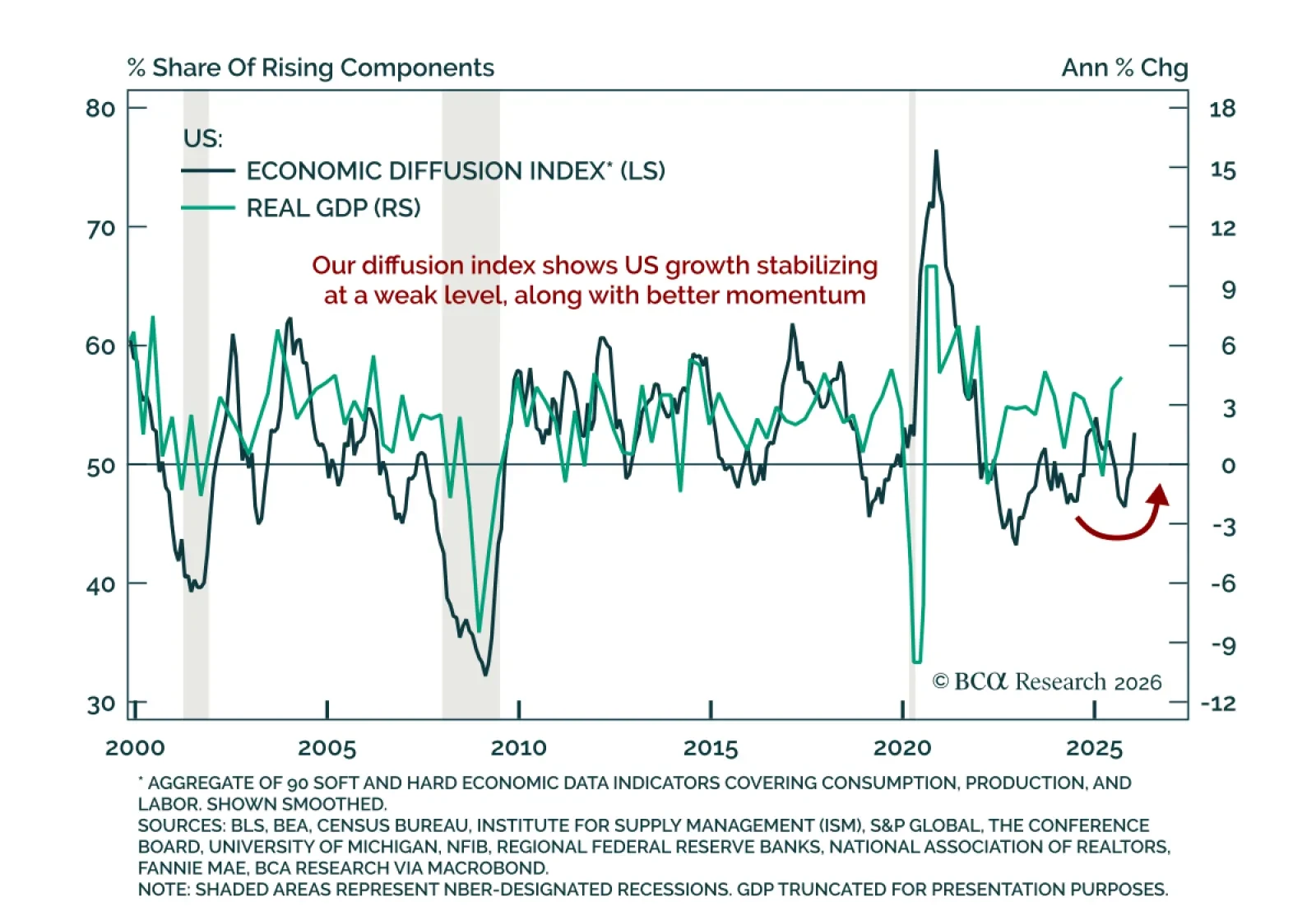

After weakening through 2025, US growth indicators now point to stabilization at a weak level. Our US growth diffusion index, which combines 90 hard and soft indicators and has historically led GDP turning points, shows growth stabilizing. Importantly, this…

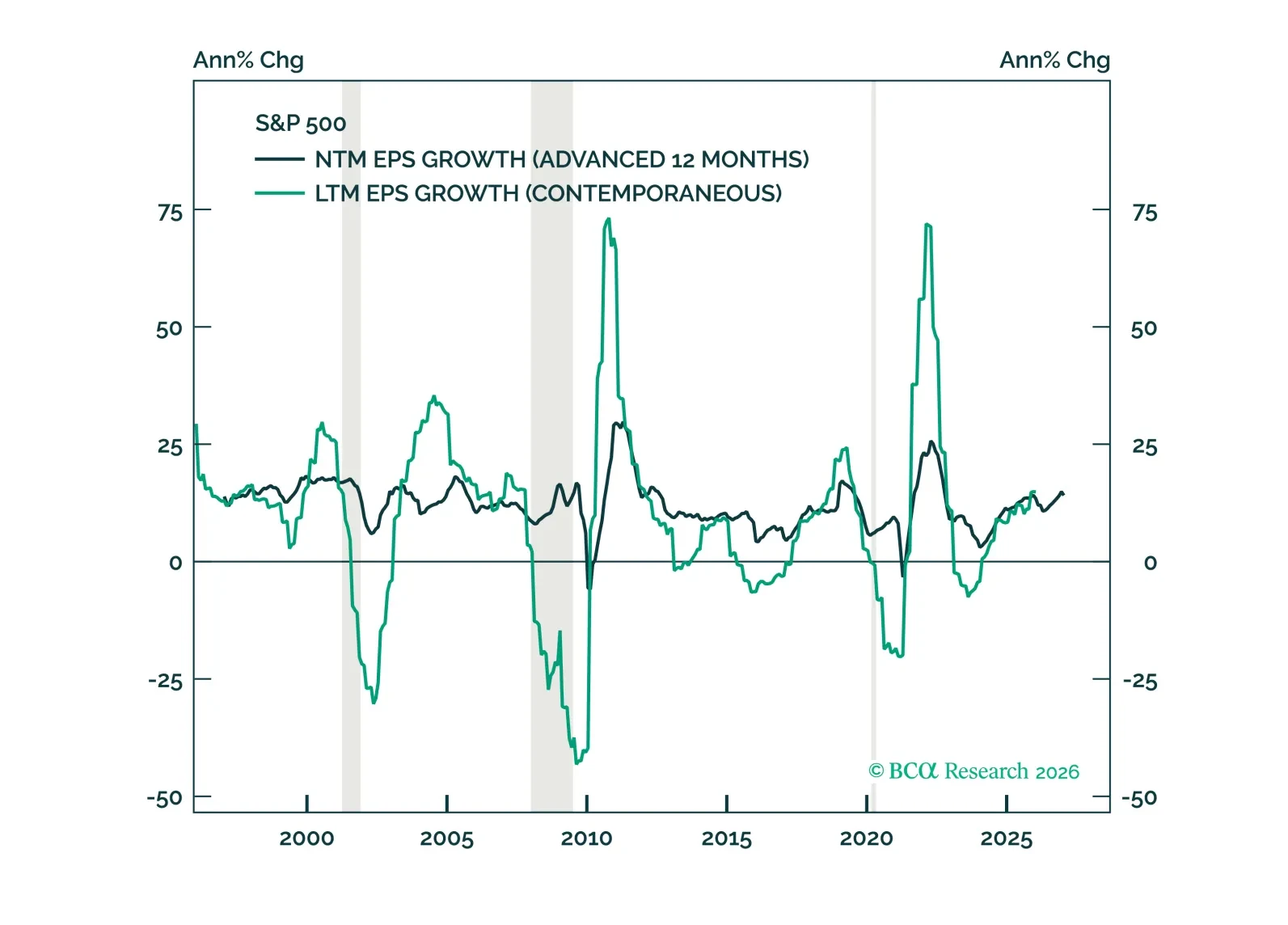

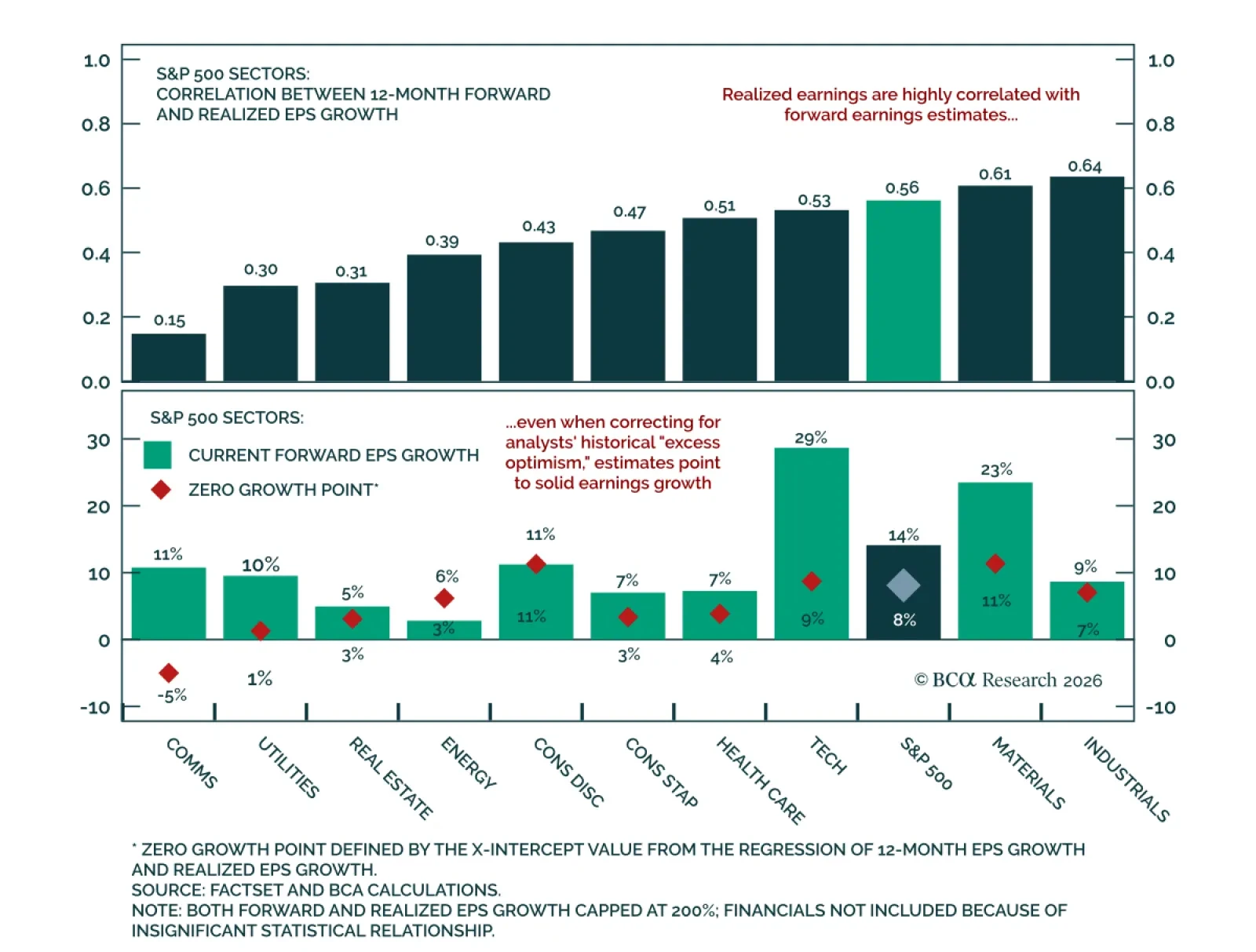

Earnings strength, durability, and breadth are all improving. As the market transitions from multiple-driven to earnings-driven returns, this backdrop supports continued gains in 2026—but with less concentration and greater scope for laggards to catch up rather than leaders to roll over.

Robust forward EPS growth signals a strong earnings backdrop heading into 2026. Our Chart Of The Week comes from Noah Weisberger, our new Chief US Equity Strategist. Noah expects equity performance in 2026 to be increasingly driven by topline growth…