United States

Since the August selloff in risk assets, the main cross-asset driver was the shift from inflation worries to growth worries. Some of that price action has reversed, as TIPS breakeven inflation rates swiftly rebounded since early September. The 2-year…

Our US Equity Strategy colleagues expect Q3 earnings to be strong enough to fuel the soft-landing narrative. Analysts expect S&P 500 earnings growth to be 4.0% year-over-year, with sales growth of 4.0% too. Yet, with average surprises of 5.6% for…

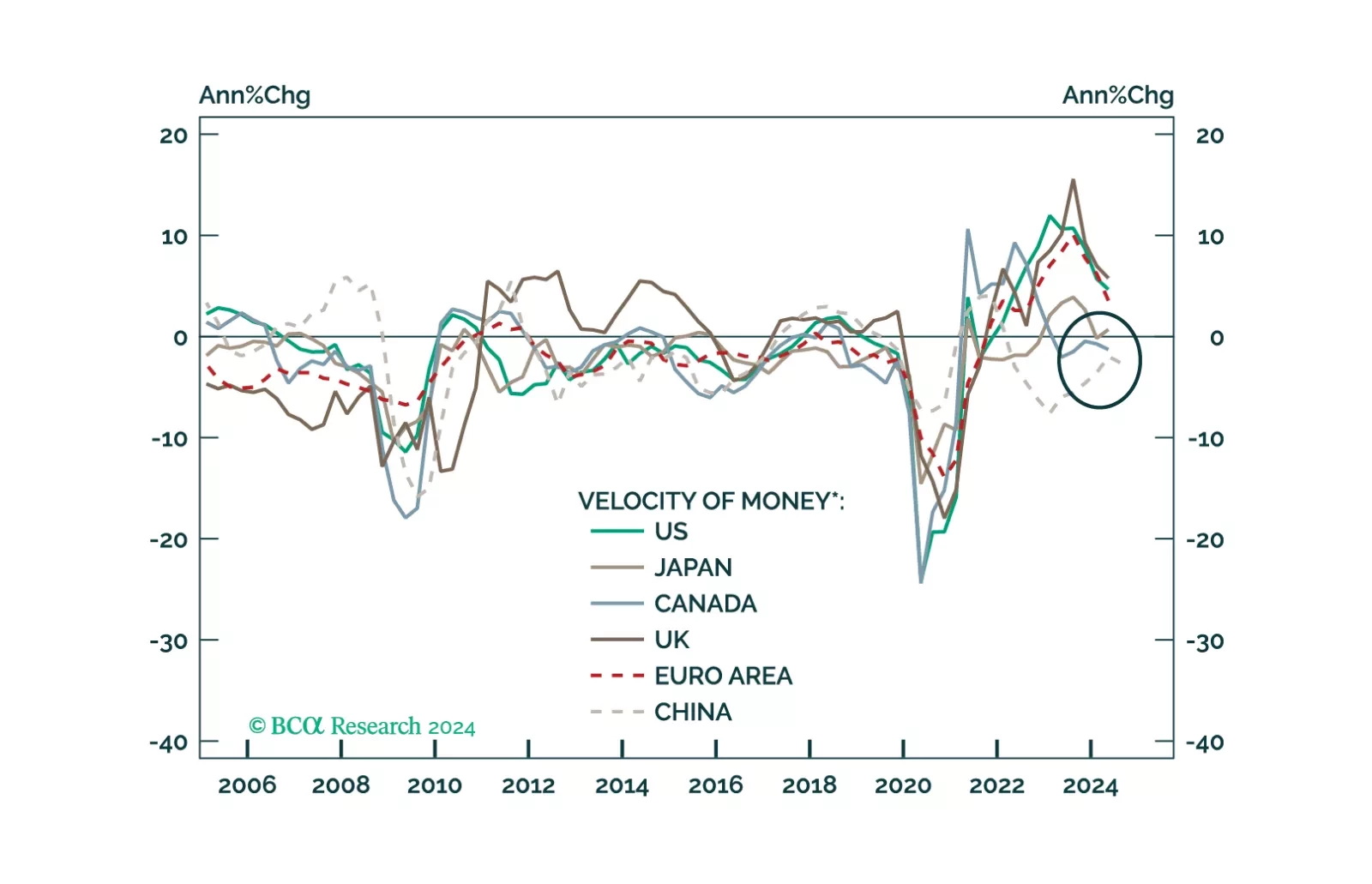

This Insight looks at the likely direction of bond yields and the dollar, from the lens of money velocity.

US housing starts and building permits eased below expectations in September. Permits, a proxy for future construction, dropped 2.9% after rising 4.6% in August. New construction fell 0.5% after rising 7.8% a month prior. These disappointing numbers extend…

Crude prices have been trendless but volatile in 2024. Oil’s choppy price action illustrates the demand and supply tug-o-war in the market. Our bias is for crude prices to weaken on a six-to-nine months horizon. Good economic news such as the resilience of…

The war in Ukraine has ended in late 2022… for markets at least. This is the conclusion from our GeoMacro team’s latest report, which aims to dispel five crucial myths surrounding the conflict. The myths are the following: The Ukraine-Russia War Will…

US retail sales beat expectations in September, rising 0.4% from August when growth was essentially flat. The control group also beat expectations at 0.7% month-on-month, accelerating from 0.3%. Growth was however somehow weak on an annual basis, suggesting a…

Recent economic data surprises drove equities and bond yields higher, putting our US Investment Strategy team’s bearish views to the test. They recently published a piece assessing their views considering these bullish developments. First, there is more to…

Japanese core machinery orders decreased by 1.9% in August and dropped 3.4% year-over-year, missing expectations for modest growth. This decline reversed July’s improvement, when machinery orders grew at an 8.7% annual pace. Japanese core machinery orders…

Third-quarter earnings season has started last week for banks, with most major banks reporting earnings above expectations so far. Our US Investment strategists routinely analyze the big banks' earnings calls to gauge their views on the strength of…