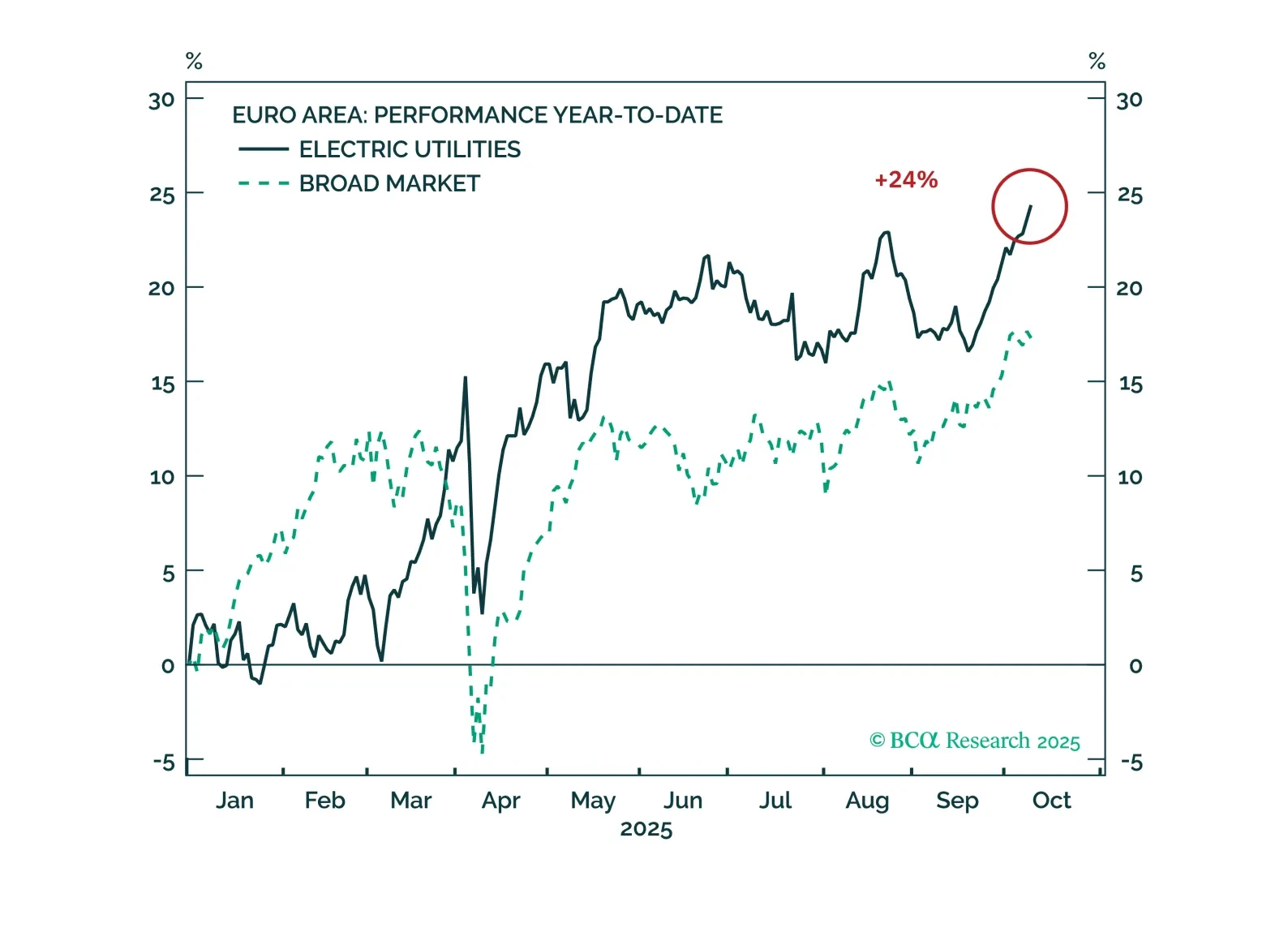

Utilities

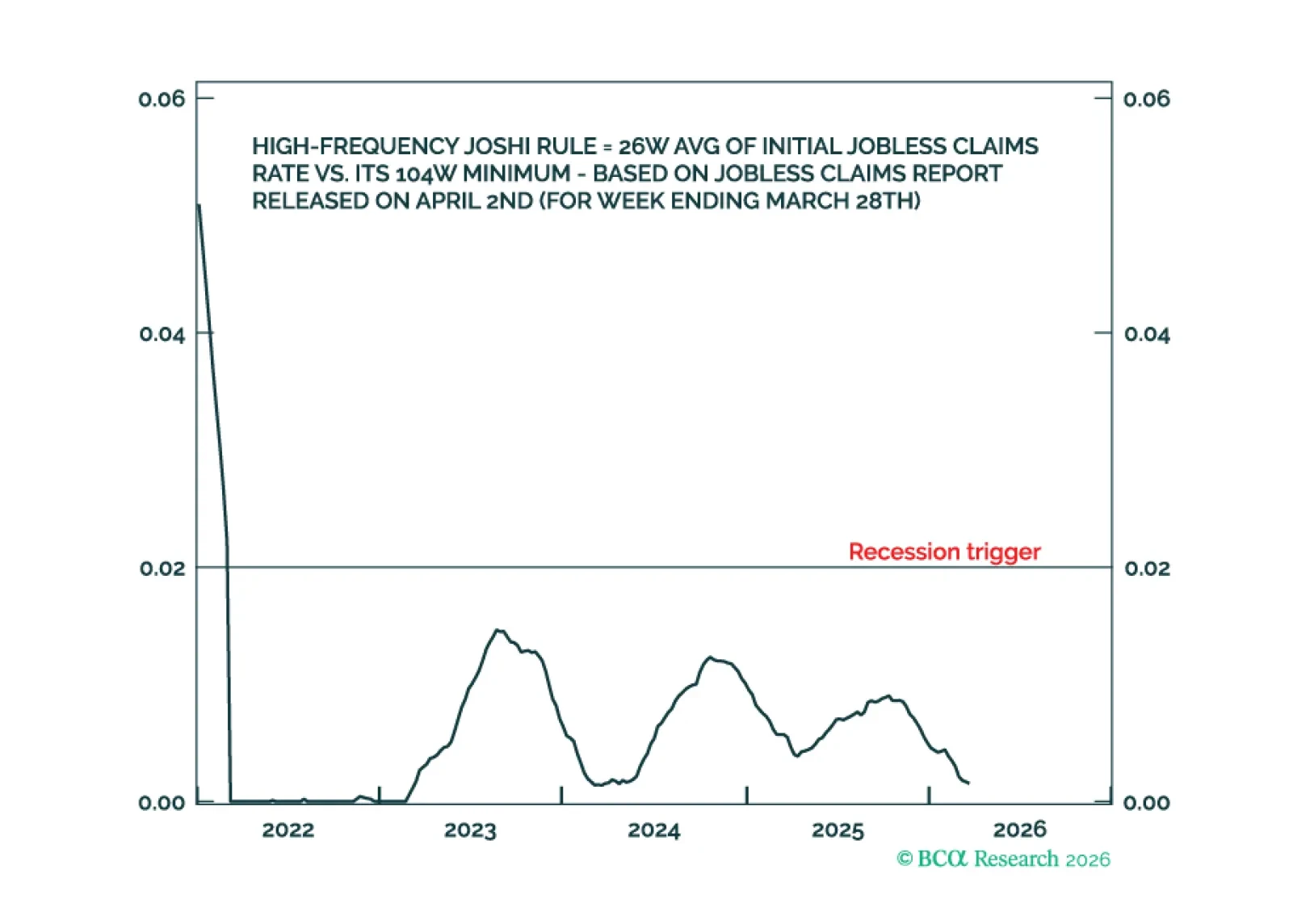

While the Middle East conflict’s inflationary impact is likely to persist, US recession risk is contained whereas non-US recession risk is more elevated. We discuss what this means for investment strategy. Plus, a new tactical trade is to underweight Utilities.

The structural demand base for electricity is expanding, requiring massive investment in grid capacity, storage solutions, and renewable generation. For investors, this trend highlights long-duration opportunities in utilities as electricity responds to the ever-growing needs of data centers and becomes the backbone of Europe’s decarbonized growth model.

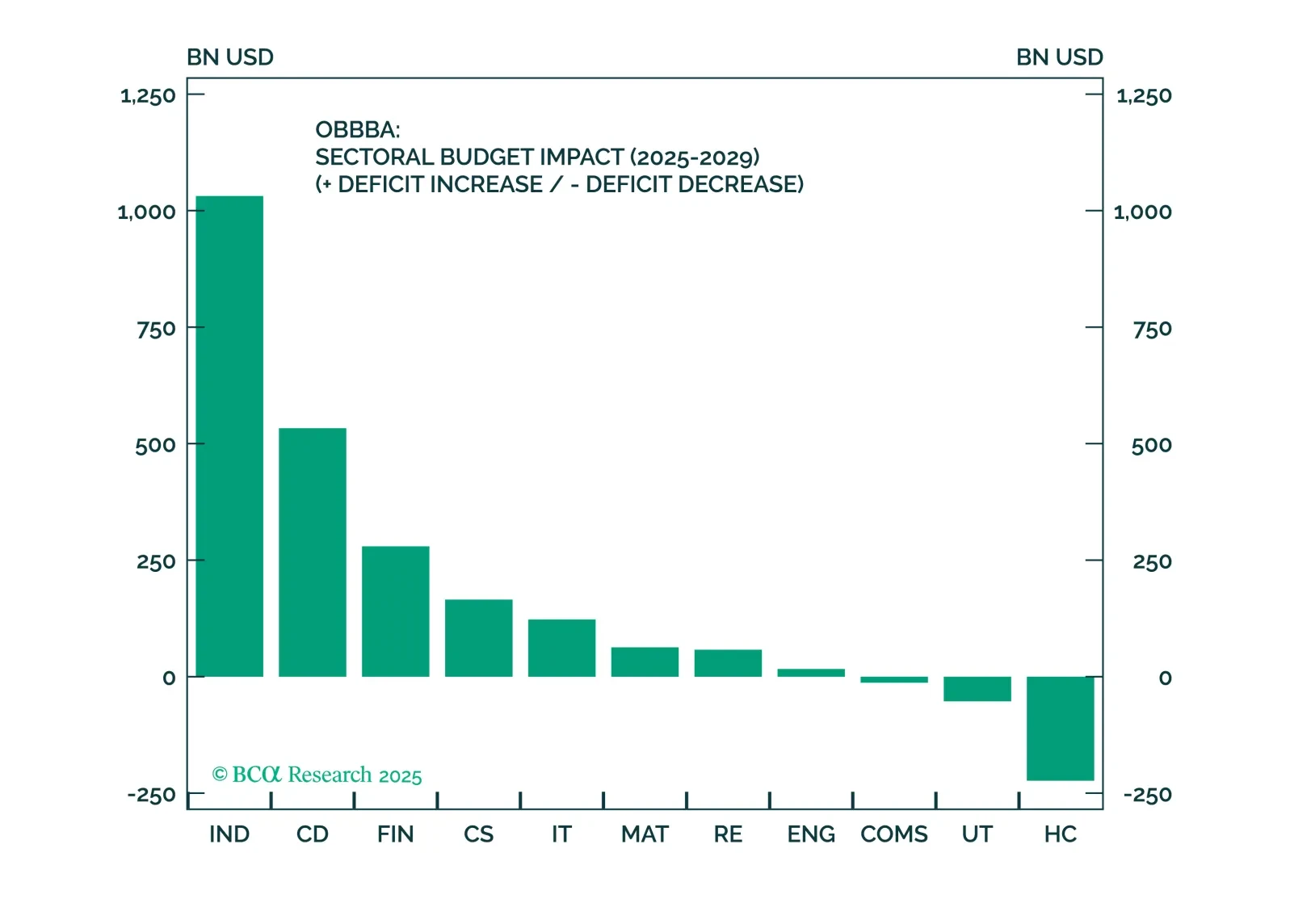

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.

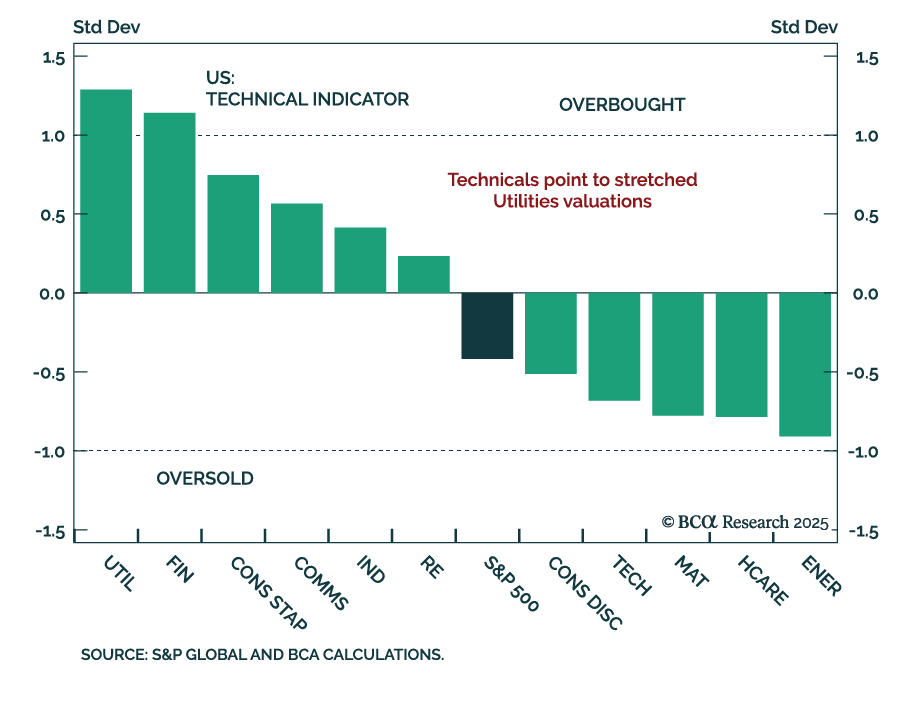

Utilities remain a long-term structural investment theme thanks to the tailwinds from GenAI, EV, and onshoring. However, there is little upside left over the tactical investment horizon as all the positives are priced in. We close our overweight and book profits.

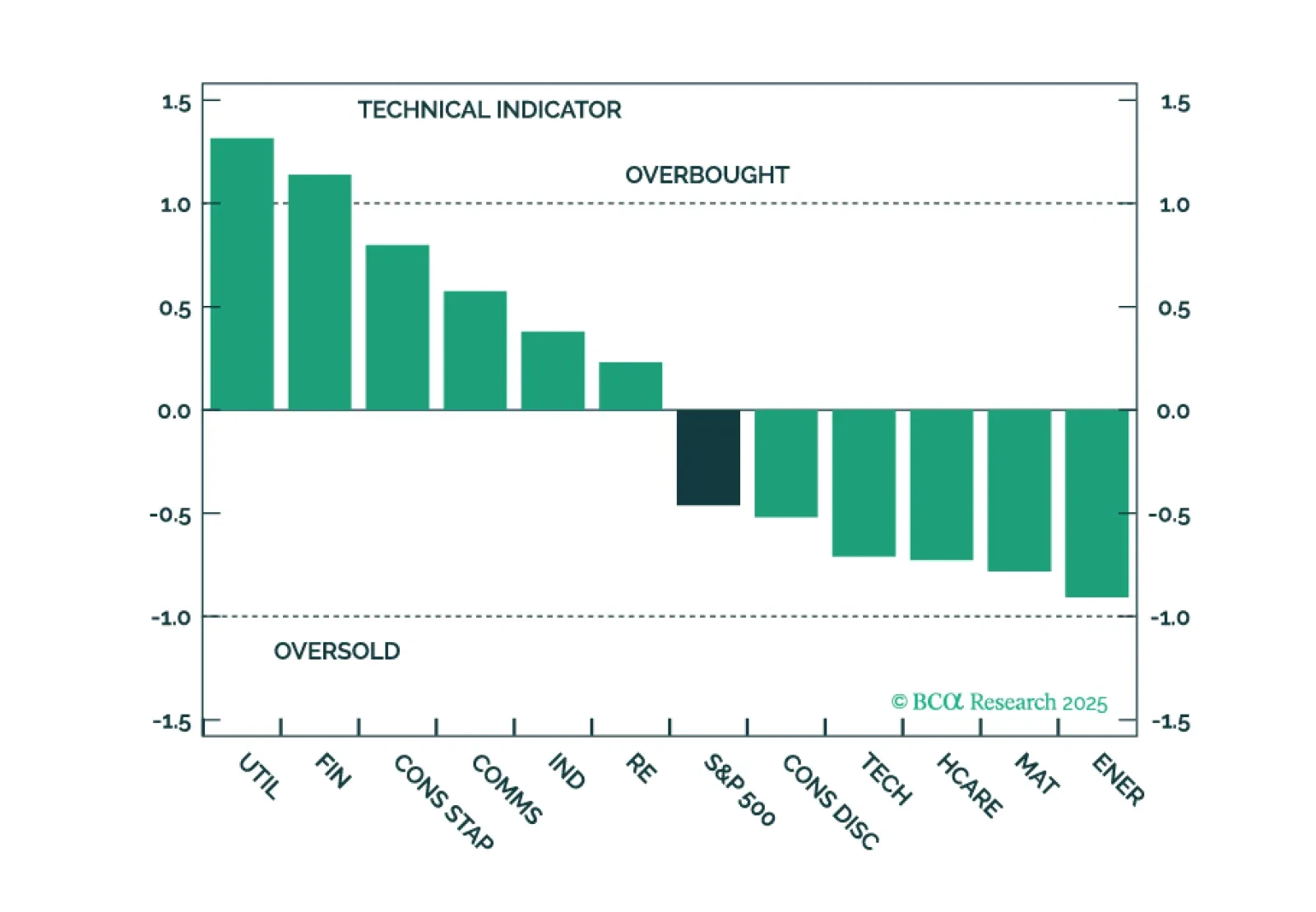

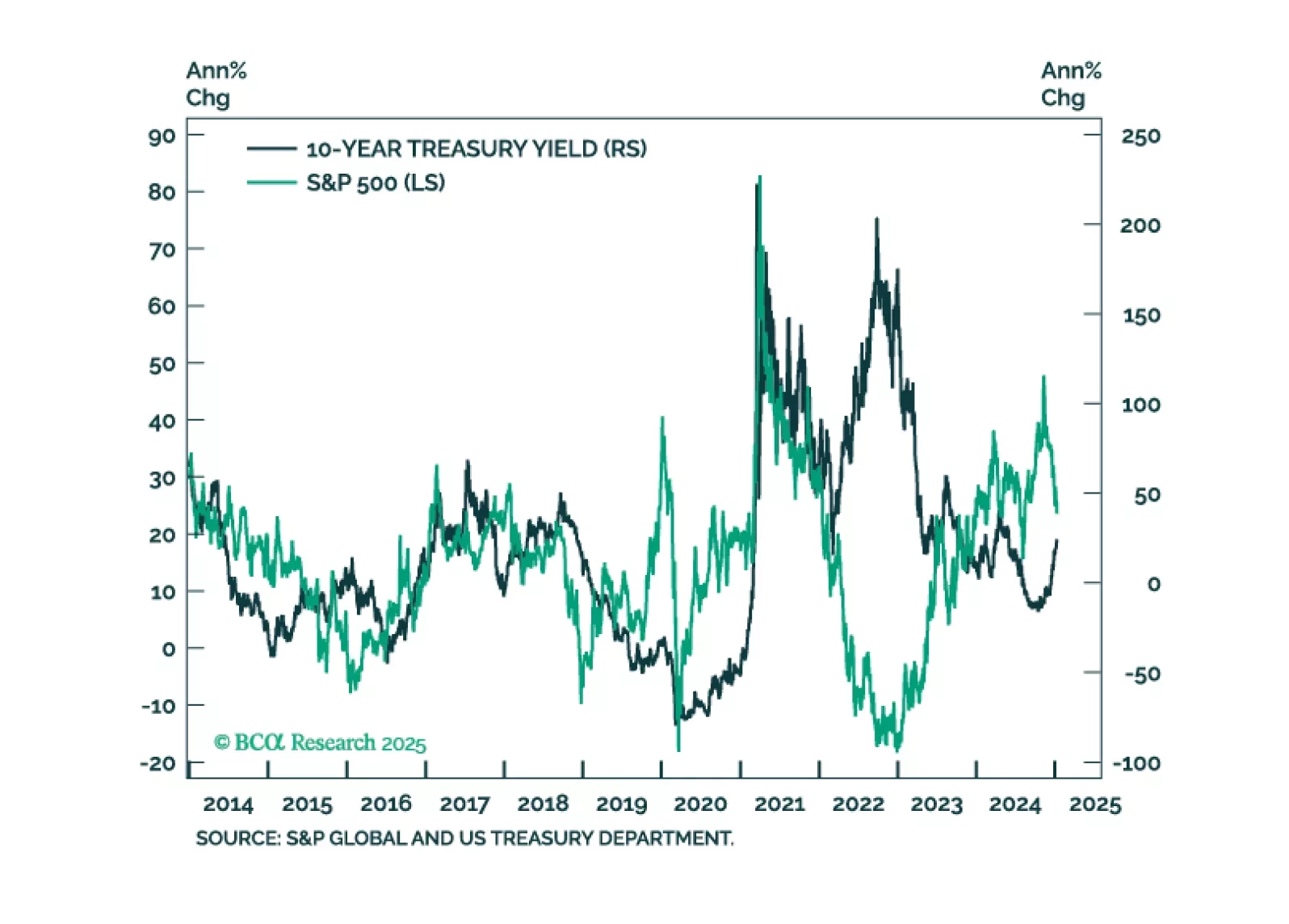

In this first presentation of 2025, we start with an overview of the 2025 outlook webcast polls, and a brief post-mortem of the 2024 market performance. Then, we shift gears and examine what is behind the recent surge in bond yields and its implications for equities. We also review market technicals and positioning and conclude with a list of trades to prepare our portfolio for continued moves in yields.

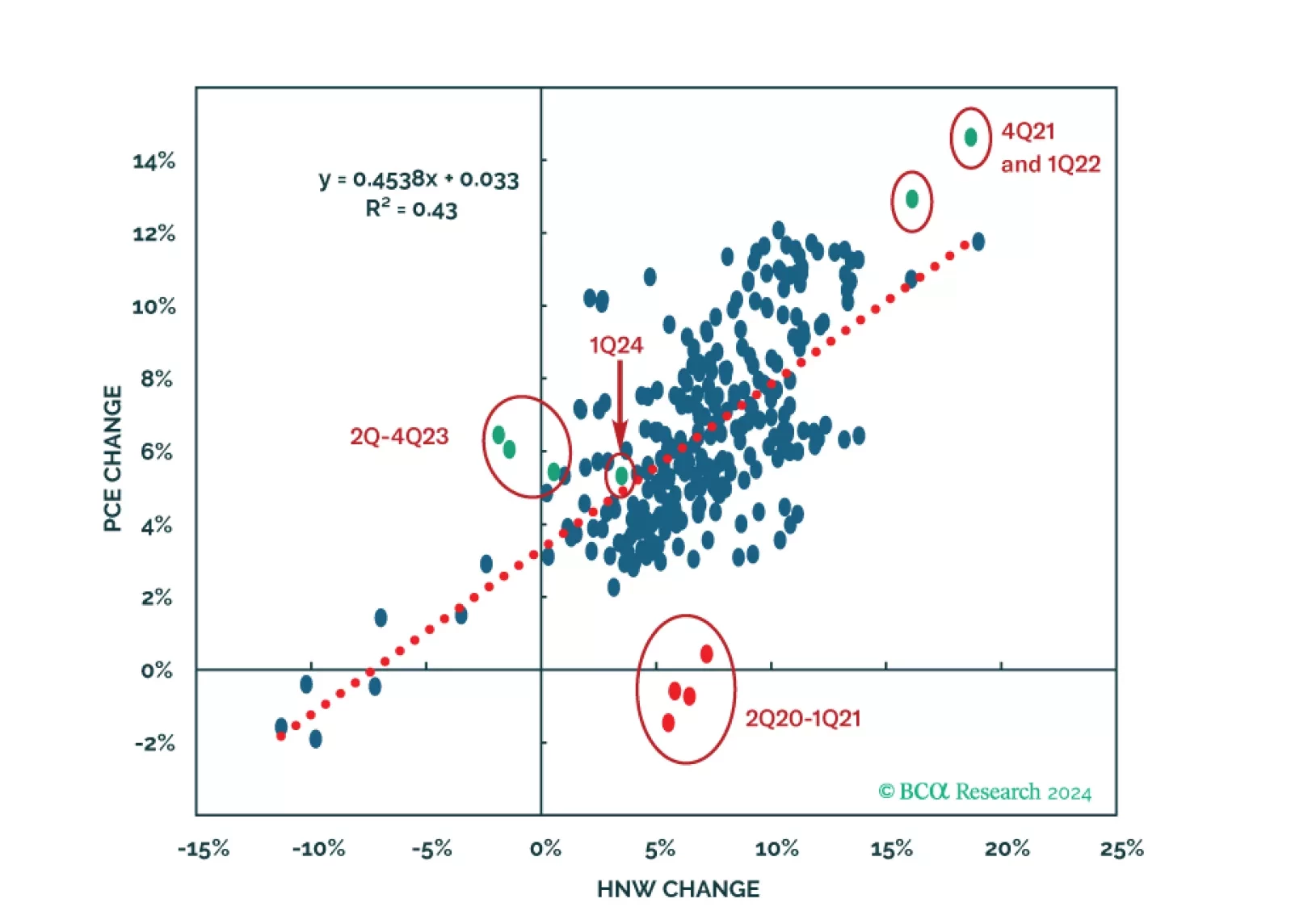

This Special Report examines the post-pandemic evolution of consumption growth, relative equity sector and subindustry performance and recent commentary from consumer-facing companies to assess the likelihood that softer spending among lower-income households will spread to middle- and upper-income households.