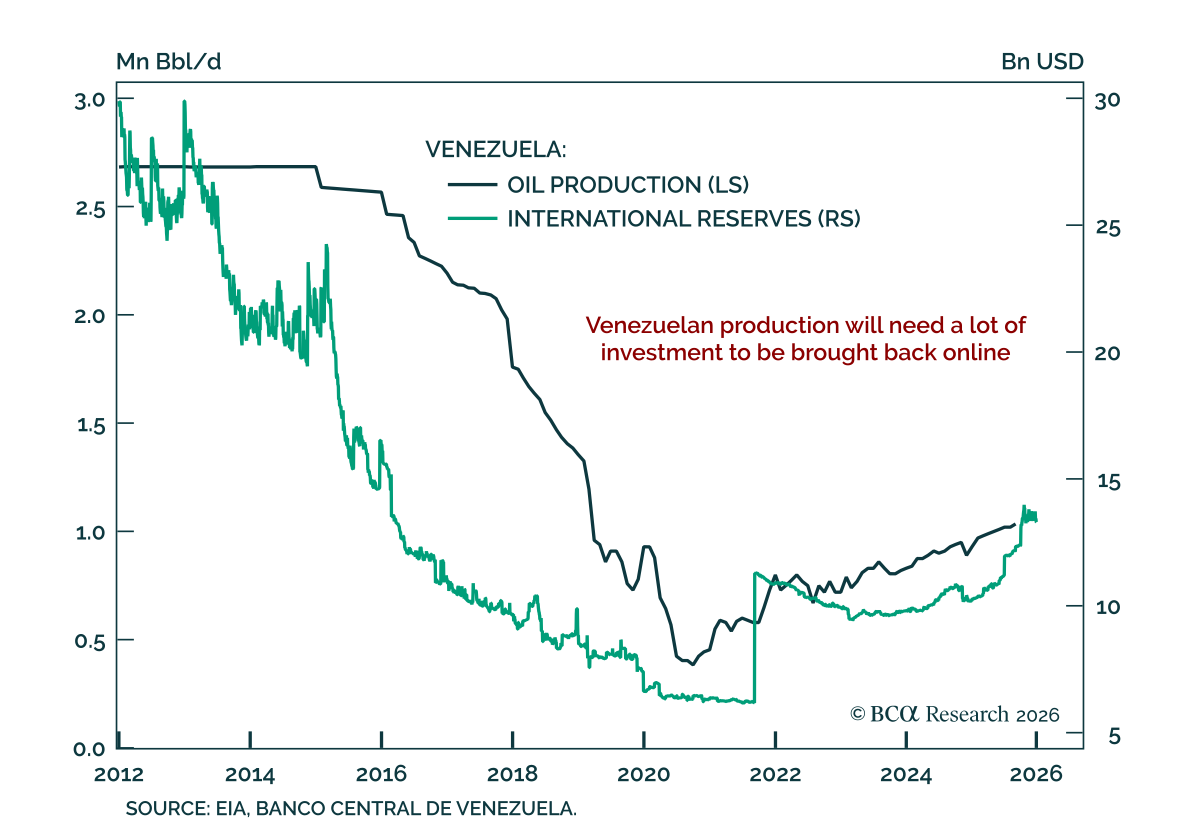

Highlights The collapse in oil prices supercharges the geopolitical risks stemming from the global pandemic and recession. Low oil prices should discourage petro-states from waging war, but Iran may be an important exception. Russian instability is one of the most important secular geopolitical consequences of this year’s crisis. President Trump’s precarious status this election year raises the possibility of provocations or reactions on his part. Europe faces instability on its eastern and southern borders in coming years, but integration rather than breakup is the response. Over a strategic time frame, go long AAA-rated municipal bonds, cyber security stocks, infrastructure stocks, and China reflation plays. Feature Chart 1Someone Took Physical Delivery! Oil markets melted this week. Oil volatility measured by the Crude Oil ETF Volatility Index surpassed 300% as WTI futures for May 2020 delivery fell into a black hole, bottoming at -$40.40 per barrel (Chart 1). Our own long Brent trade, initiated on 27 March 2020 at $24.92 per barrel, is down 17.9% as we go to press. Strategically we are putting cash to work acquiring risk assets and we remain long Brent. The forward curve implies that prices will rise to $35 and $31 per barrel for Brent and WTI by April 2021. We initiated this trade because we assessed that: The US and EU would gradually reopen their economies (they are doing so). Oil production would be destroyed (more on this below). Russia and Saudi Arabia would agree to production cuts (they did). Monetary and fiscal stimulus would take effect (the tsunami of stimulus is still growing). Global demand would start the long process of recovery (no turn yet, unknown timing). On a shorter time horizon, we are defensively positioned but things are starting to look up on COVID-19 – New York Governor Andrew Cuomo has released results of a study showing that 15% of New Yorkers have antibodies, implying a death rate of only 0.5%. The US dollar and global policy uncertainty may be peaking as we go to press (Chart 2). However, second-order effects still pose risks that keep us wary. Chart 2Dollar And Policy Uncertainty Roaring Geopolitics is the “next shoe to drop” – and it is already dropping. A host of risks are flying under the radar as the world focuses on the virus. Taken alone, not every risk warrants a risk-off positioning. But combined, these risks reveal extreme global uncertainty which does warrant a risk-off position in the near term. This week’s threats between the US and Iran, in particular, show that the political and geopolitical fallout from COVID-19 begins now, it will not “wait” until the pandemic crisis subsides. In this report we focus on the risks from oil-producing economies, but we first we update our fiscal stimulus tally. Stimulus Tsunami Chart 3Stimulus Tsunami Still Building Policymakers responded to COVID-19 by doing “whatever it takes” to prop up demand (Chart 3). Please see the Appendix for our latest update of our global fiscal stimulus table. The latest fiscal and monetary measures show that countries are still adding stimulus – i.e. there is not yet a substantial shift away from providing stimulus: China has increased its measures to a total of 10% of GDP for the year so far, according to BCA Research China Investment Strategy. This includes a general increase in credit growth, a big increase in government spending (2% of GDP), a bank re-lending scheme (1.5% of GDP), an increase in general purpose local government bonds (2% of GDP), plus special purpose bonds (4% of GDP) and other measures. On the political front, the government has rolled out a new slogan, “the Six Stabilities and the Six Guarantees,” and President Xi Jinping said on an inspection tour to Shaanxi that the state will increase investments to ensure that employment is stabilized. This is the maximum reflationary signal from China that we have long expected. The US agreed to a $484 billion “fourth phase” stimulus package, bringing its total to 13% of GDP. President Trump is already pushing for a fifth phase involving bailouts of state and local governments and infrastructure, which we fully expect to take place even if it takes a bit longer than packages that have been passed so far this year. German Chancellor Angela Merkel has opened the way for the EU to issue Eurobonds, in keeping with our expectations. Germany is spending 12% of GDP in total – which can go much higher depending on how many corporate loans are tapped – while Italy is increasing its stimulus to 3% of GDP. As deficits rise to astronomical sums, and economies gradually reopen, will legislatures balk at passing new stimulus? Yes, eventually. Financial markets will have to put more pressure on policymakers to get them to pass more stimulus. This can lead to volatility. In the US the pandemic is coinciding with “peak polarization” over the 2020 election. Lack of coordination between federal and state governments is increasing uncertainty. Currently disputes center on the timing of economic reopening and the provisioning bailout funds for state and local governments. Senate Majority Leader Mitch McConnell is threatening to deny bailouts for American states with large, unfunded public pension benefits (Chart 4A). He is insisting that the Senate “push the pause button” on coronavirus relief measures; specifically that nothing new be passed until the Senate convenes in Washington on May 4. He may then lead a charge in the Republican Senate to try to require structural reforms from states in exchange for bailouts. Estimates of the total state budget shortfall due to the crisis stand at $500 billion over the next three years, which is almost certainly an understatement (Chart 4B). Chart 4AUS States Have Unfunded Liabilities Chart 4BUS States Face Funding Shortfalls Could a local government or state declare bankruptcy? Not anytime soon. Technically there is no provision for states to declare bankruptcy. A constitutional challenge to such a declaration would go to the Supreme Court. One commonly cited precedent, Arkansas in 1933, ended up with a federal bailout.1 A unilateral declaration could conceivably become a kind of “Lehman moment” in the public sector, but state governors will ask their legislatures to provide more fiscal flexibility and will seek bailouts from the federal government first. The Federal Reserve is already committed to buying state and local bonds and can expand these purchases to keep interest rates low. Washington would be forced to provide at least short-term funding if state workers started getting fired in the midst of the crisis because of straightened state finances – another $500 billion for the states is entirely feasible in today’s climate. Constraints will prevail on the GOP Senate to provide state bailout funds. This conflict over state finances could have a negative impact on US equities in the near term, but it is largely a bluff – McConnell will lose this battle. The fundamental dynamic in Washington is that of populism combined with a pandemic that neutralizes arguments about moral hazard. Big-spending Democrats in the House of Representatives control the purse strings while big-spending President Trump faces an election. Senate Republicans are cornered on all sides – and their fate is tied to the President’s – so they will eventually capitulate. Bottom Line: The global fiscal and monetary policy tsunami is still building. But there are plenty of chances for near-term debacles. Over the long run the gargantuan stimulus is the signal while the rest is noise. Over the long run we expect the reflationary efforts to prevail and therefore we are long Treasury inflation-protected securities and US investment grade corporate bonds. We recommend going strategically long AAA-rated US municipal bonds relative to 10-year Treasuries. Petro-State Meltdown Since March we have highlighted that the collapse in oil prices will destabilize oil producers above and beyond the pandemic and recession. This leaves Iran in danger, but even threatens the stability of great powers like Russia. Normally there is something of a correlation between the global oil price and the willingness of petro-states to engage in war (Chart 5). Chart 5Petro-States Cease Fire When Oil Drops When prices fall, revenues dry up and governments have to prioritize domestic stability. This tends to defer inter-state conflict. We can loosely corroborate this evidence by showing that global defense stocks tend to be correlated with oil prices (Chart 6). Global growth is the obvious driver of both of these indicators. But states whose budgets are closely tied to the commodity cycle are the most likely to cut defense spending. Chart 6Global Growth Drives Oil And Guns Russia is case in point. Revenues from Rostec, one of Russia’s largest arms firms, rise and fall with the Urals crude oil price (Chart 7). The Russians launch into foreign adventures during oil bull markets, when state coffers are flush with cash. They have an uncanny way of calling the top of the cycle by invading countries (Chart 8). Chart 7Oil Correlates With Russian Arms Sales Chart 8Russian Invasions Call Peak In Oil Bull Markets Chart 9Turkish Political Risk On The Rise In the current oil rout, there is already some evidence of hostilities dying down in this way. For instance, after years of dogged fighting in Yemen, Saudi Arabia is finally declaring a ceasefire there. Turkey, which benefits from low oil prices, has temporarily gotten the upper hand in Libya vis-à-vis Khalifa Haftar and the Libyan National Army, which depends on oil revenues and backing from petro-states like Russia and the GCC. Of course, Turkey’s deepening involvement in foreign conflicts is evidence of populism at home so it does not bode well for the lira or Turkish assets (Chart 9). But it does highlight the impact of weak oil on petro-players such as Haftar. However, the tendency of petro-states to cease fire amid low prices is merely a rule of thumb, not a law of physics. Past performance is no guarantee of future results. Already we are seeing that Iran is defying this dynamic by engaging in provocative saber-rattling with the United States. Iran And Iraq The US and Iran are rattling sabers again. One would think that Iran, deep in the throes of recession and COVID-19, would eschew a conflict with the US at a time when a vulnerable and anti-Iranian US president is only seven months away from an election. Chart 10US Maximum Pressure On Iran Iran has survived nearly two years of “maximum pressure” from President Trump (Chart 10), and previous US sanction regimes, and has a fair chance of seeing the Democrats retake Washington. The Democrats would restart negotiations to restore the 2015 nuclear deal, which was favorable to Iran. Therefore risking air strikes from President Trump is counterproductive and potentially disastrous. Yet this logic only holds if the Iranian regime is capable of sustaining the pain of a pandemic and global recession on top of its already collapsing economy. Iran’s ability to circumvent sanctions to acquire funds depended on the economy outside of Iran doing fine. Now Iran’s illicit funds are drying up. This could lead to a pullback in funding for militant proxies across the region as Iran cuts costs. But it also removes the constraint on Iran taking bolder actions. If the economy is collapsing anyway then Iran can take bigger risks. Furthermore if Iran is teetering, there may be an incentive to initiate foreign conflicts to refocus domestic angst. This could be done without crossing Trump’s red lines by attacking Iraq or Saudi Arabia. With weak oil demand, Iran’s leverage declines. But a major attack would reduce oil production and accelerate the global supply-demand rebalance. Iran’s attack on the Saudi Abqaiq refinery last September took six million barrels per day offline briefly, but it was clearly not intended to shut down that production permanently. Threats against shipping in the Persian Gulf bring about 14 million barrels per day into jeopardy (Chart 11). Chart 11Closing Hormuz Would Be The Biggest Oil Shock Ever Iran-backed militias in Iraq have continued to attack American assets and have provoked American air strikes over the past month, despite the near-war scenario that erupted just before COVID. Iranian ships have harassed US naval ships in recent days. President Trump has ordered the navy to destroy ships that threaten it; Iranian commander has warned that Iran will sink US warships that threaten its ships in the Gulf. There is a 20% chance of armed hostilities between the US and Iran. Why would Iran be willing to confront the United States? First, Iran rightly believes that the US is war-weary and that Trump is committed to withdrawing from the Middle East. But this could prompt a fateful mistake. The equation changes if the US public is incensed and Trump’s election campaign could benefit from conflict. Chart 12Youth Pose Stability Risk To Iran Second, the US is never going to engage in a ground invasion of Iran. Airstrikes would not easily dislodge the regime. They could have the opposite effect and convert an entire generation of young, modernizing Iranians into battle-hardened supporters of the Islamic revolution (Chart 12). This is a dire calculation that the Iranian leaders would only make if they believed their regime was about to collapse. But they are quite possibly the closest to collapse that they have been since the 1980s and nobody knows where their pain threshold lies. They are especially vulnerable as the regime approaches the uncharted succession of Supreme Leader Ali Khamanei. Since early 2018 we have argued that there is a 20% chance of armed hostilities between the US and Iran. We upgraded this to 40% in June 2019 and downgraded it back to 20% after the Iranians shied from direct conflict this January. Our position remains the same 20%. This is still a major understated risk at a time when the global focus is entirely elsewhere. It will persist into 2021 if Trump is reelected. If the Democrats win the US election, this war risk will abate. The Iranians will play hard to get but they are politically prohibited from pursuing confrontation with the US when a 2015-type deal is available. This would open up the possibility for greater oil supply to be unlocked in the future, but sanctions are not likely to be lifted till 2022 at earliest. Russia Russia may not be on the verge of invading anyone, but it is internally vulnerable and fully capable of striking out against foreign opponents. Cyberattacks, election interference, or disinformation campaigns would sow confusion or heighten tensions among the great powers. The Russian state is suffering a triple whammy of pandemic, recession, and oil collapse. President Vladimir Putin’s approval rating has fallen this year so far, whereas other leaders in the western world have all seen polling bounces (even President Trump, slightly) (Chart 13). Putin postponed a referendum designed to keep him in office through 2036 due to the COVID crisis. In other words, the pandemic has already disrupted his carefully laid succession plans. While Putin can bypass a referendum, he would have been better off in the long run with the public mandate. Generally it is Putin’s administration, not his personal popularity, that is at risk, but the looming impact on Russian health and livelihoods puts both in jeopardy (Chart 14) and requires larger fiscal outlays to try to stabilize approval (Chart 15). Chart 13Putin Saw No COVID Popularity Bump Chart 14Russian Regime Faces Political Discontent Moreover, regardless of popular opinion, Putin is likely to settle scores with the oligarchs. The fateful decision to clash with the Saudis in March, which led to the oil collapse, will fall on Igor Sechin, Chief Executive of Rosneft, and his faction. An extensive political purge may well ensue that would jeopardize domestic stability (Chart 16). Chart 15Russia To Focus On Domestic Stability Chart 16Russian Political Risk Will Rise Russian tensions with the US will rise over the US election in November. The Democrats would seek to make Russia pay for interfering in US politics to help President Trump win in 2016. But even President Trump may no longer be a reliable “ally” of Putin given that Putin’s oil tactics have bankrupted the US shale industry during Trump’s reelection campaign. The American and Russian air forces are currently sparring in the air space over Syria and the Mediterranean. The US has also warned against a malign actor threatening to hack the health care system of the Czech Republic, which could be Russia or another actor like North Korea or Iran. These issues have taken place off the radar due to the coronavirus but they are no less real for that. Venezuela We have predicted Venezuela’s regime change for several years but the oil meltdown, pandemic, and insufficient Russian and Chinese support should put the final nail in the regime’s coffin. Hugo Chavez’s rise to power, the last “regime change,” occurred as oil prices bottomed in 1998. Historically the Venezuelan armed forces have frequently overthrown civilian authorities, but in several cases not until oil prices recovered (Chart 17). Chart 17Venezuelan Coups Follow Oil Rebounds The US decision to designate Nicolas Maduro as a “narco-terrorist,” to deploy greater naval and coast guard assets around Venezuela, to reassert the Monroe Doctrine and Roosevelt Corollary, and to pull Chevron from the country all suggest that Washington is preparing for regime change. Such a change may or may not involve any American orchestration. Venezuela is an easy punching-bag for President Trump if he seeks to “wag the dog” ahead of the election. Venezuela would be a strategic prize and yet it cannot hurt the US economy or financial markets substantially, giving limited downside to President Trump if he pursues such a strategy. Obviously any conflict with Venezuela this year is far less relevant to global investors than one with Iran, North Korea, China, or Russia. Regime change would be positive for oil supply and negative for prices over the long run. But that is a story for the next cycle of energy development, as it would take years for government and oil industry change in Venezuela to increase production. The US election cycle is a critical aggravating factor for all of these petro-state risks. Shale producers are going bankrupt, putting pressure on the economy and some swing states. The risk of a conflict arises not only from Trump playing “wag the dog” after the crisis abates, but also from other states provoking the president, causing him to react or overreact. The “Other Guys” Oil producers outside the US, Canada, gulf OPEC, and Russia – the “other guys” – are extremely vulnerable to this year’s global crisis and price collapse. Comprising half of global production, they were already seeing production declines and a falling global market share over the past decade when they should have benefited from a global economic expansion. They never recovered from the 2014-15 oil plunge and market share war (Chart 18). Angola (1.4 million barrels per day), Algeria (one million barrels per day), and Nigeria (1.8 million barrels per day) are relatively sizable producers whose domestic stability is in question in the coming years as they cut budgets and deplete limited forex reserves to adjust to the lower oil price. This means fewer fiscal resources to keep political and regional factions cooperating and provide basic services. Algeria is particularly vulnerable. President Abdelaziz Bouteflika, who ruled as a strongman from 1999, was forced out last year, leaving a power vacuum that persists under Prime Minister Abdelaziz Djerad, in the wake of the low-participation elections in December. An active popular protest movement, Hirak, already exists and is under police suppression. Unemployment is high, especially among the youth. Neighboring Libya is in the midst of a war and extremist militants within Libya and North Africa would like to expand their range of operations in a destabilized Algeria. Instability would send immigrants north to Europe. Oil production will be reduced involuntarily as well as voluntarily this year due to regime failures. Brazil is not facing the risk of state failure like Algeria, but it is facing a deteriorating domestic political outlook (Chart 19). President Jair Bolsonaro’s popularity was already low relative to most previous presidents before COVID. His narrow base in the Chamber of Deputies got narrower when he abandoned his political party. He has defied the pandemic, refused to endorse social distancing or lockdown orders by local governments, and fired his Health Minister Luiz Henrique Mandetta. Chart 18Petro-States: 'Other Guys' Face Instability Chart 19Brazilian Political Risk Rising Again Brazil has a high number of coronavirus deaths per million people relative to other emerging markets with similar health capacity and susceptibility to the disease. This, combined with sharply rising unemployment, could prove toxic for Bolsonaro, who has not received a bounce in popular opinion from the crisis like most other world leaders. Thus on balance we expect the October local elections to mark a comeback for the Worker’s Party. The limited fiscal gains of Bolsonaro’s pension reform are already wiped out by the global recession, which will set back the country’s frail recovery from its biggest recession in a century. The country is still on an unsustainable fiscal path. Bolsonaro does not have a strong personal commitment to neoliberal structural reform, which has been put aside anyway due to the need for government fiscal spending amid the crisis. Unless Bolsonaro’s popularity increases in the wake of the crisis – due to backlash against the state-level lockdowns – the economic shock is negative for Brazil’s political stability and economic policy orthodoxy. Bottom Line: Our rule of thumb about petro-states suggests that they will generally act less aggressive amid a historic oil price collapse, but Iran may prove a critical exception. Investors should not underestimate the risk of a US-Iran conflict this year. Beyond that, the US election will have a decisive impact as the Democrats will seek to resume the Iranian nuclear deal and Iran would eventually play ball. Venezuela is less globally relevant this year – although a “wag the dog” scenario is a distinct possibility – but it may well be a major oil supply surprise in the 2020s. More broadly the takeaway is that oil production will be reduced involuntarily as well as voluntarily this year due to regime failures. Investment Takeaways Obviously any conflict with Iran could affect the range of Middle Eastern OPEC supply, not just the portion already shuttered due to sanctions on Iran itself. Any Iran war risk is entirely separate from the risk of supply destruction from more routine state failures in Africa. These shortages have been far less consequential lately and have plenty of room to grow in significance (Chart 20). The extreme lows in oil prices today will create the conditions for higher oil prices later when demand recovers, via supply destruction. Chart 20More Unplanned Outages To Come Chart 21European Political Risk No Longer Underrated An important implication – to be explored in future reports – is that Europe’s neighborhood is about to get a lot more dangerous in the coming years, as the Middle East and Russia will become less stable. Middle East instability will result in new waves of immigration and terrorism after a lull since 2015-16. These waves would fuel right-wing political sentiment in parts of Europe that are the most vulnerable in today’ crisis: Italy, Spain, and France (Chart 21). This should not be equated with the EU breaking apart, however, as the populist parties in these countries are pursuing soft rather than hard Euroskepticism. Unless that changes the risk is to the Euro Area’s policy coherence rather than its existence. Finally Russian domestic instability is one of the major secular consequences of the pandemic and recession and its consequences could be far-reaching, particularly in its great power struggle with the United States. We are reinitiating a strategic long in cyber security stocks, the ISE Cyber Security Index, relative to the S&P500 Info Tech sector. Cyberattacks are a form of asymmetrical warfare that we expect to ramp up with the general increase in global geopolitical tensions. The US’s recent official warning against an unknown actor that apparently intended to attack the health system of the Czech Republic highlights the way in which malign actors could attempt to capitalize on the chaos of the pandemic. We also recommend strategic investors reinitiate our “China Play Index” – commodities and equities sensitive to China’s reflation – and our BCA Infrastructure Basket, which will benefit from Chinese reflation as well as US deficit spending. China’s reflation will help industrial metals more so than oil, but it is positive for the latter as well. Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 John Mauldin, "Don't Be So Sure That States Can't Go Bankrupt," Forbes, July 28, 2016, forbes.com. Section II: Appendix : GeoRisk Indicator China Russia UK Germany France Italy Canada Spain Taiwan Korea Turkey Brazil Appendix Table 1 The Global Fiscal Stimulus Response To COVID-19 Section III: Geopolitical Calendar