War/Conflict

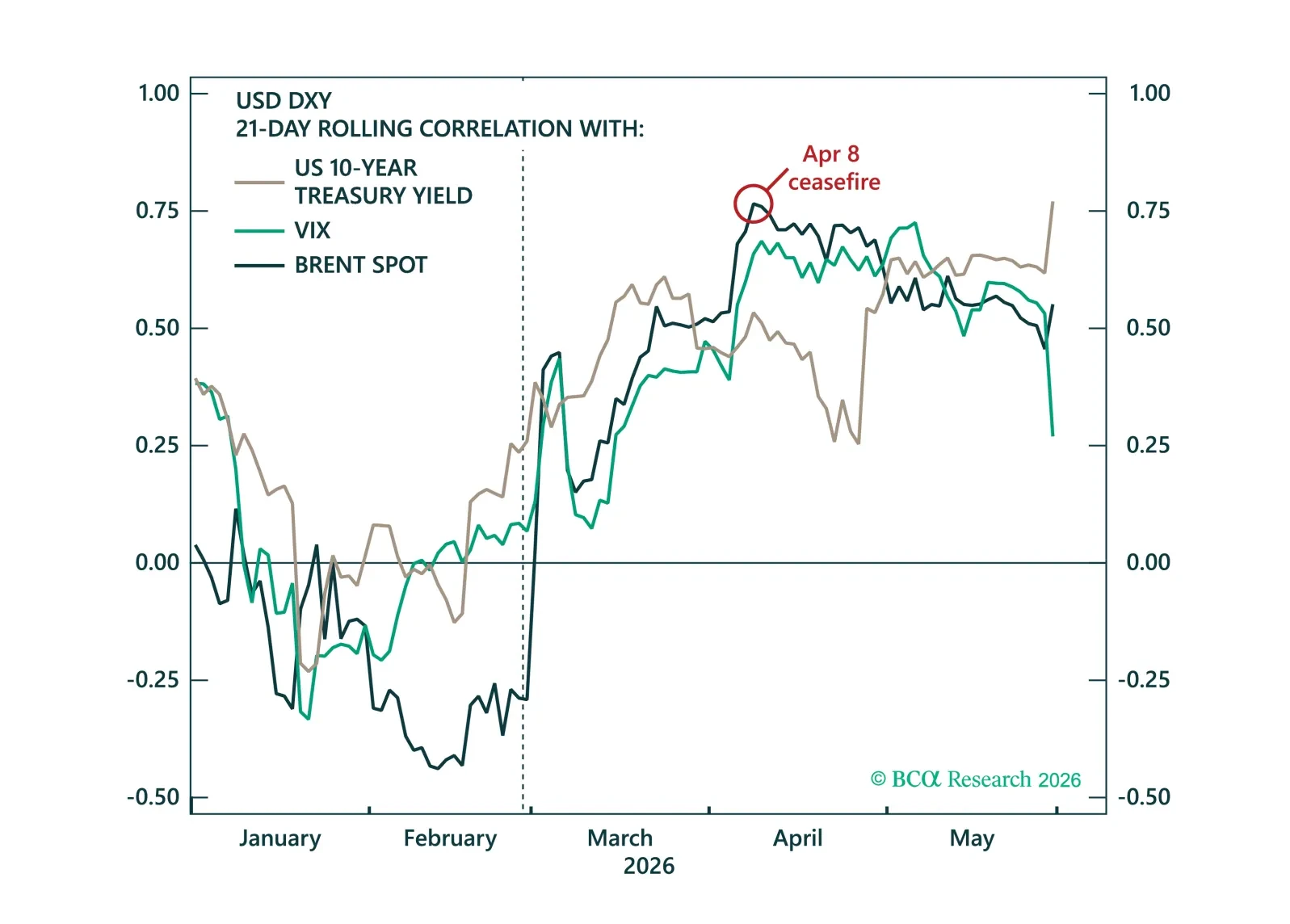

The dollar's muted response to the Iran conflict has led many to question its safe-haven appeal. We argue the opposite – the dollar's defensive properties have returned, while improving growth and rate dynamics should underpin further USD strength in the months ahead.

The odds of a near-term US-Iran deal have gone up slightly, but the odds of a Russian provocation that divides NATO have also gone up.

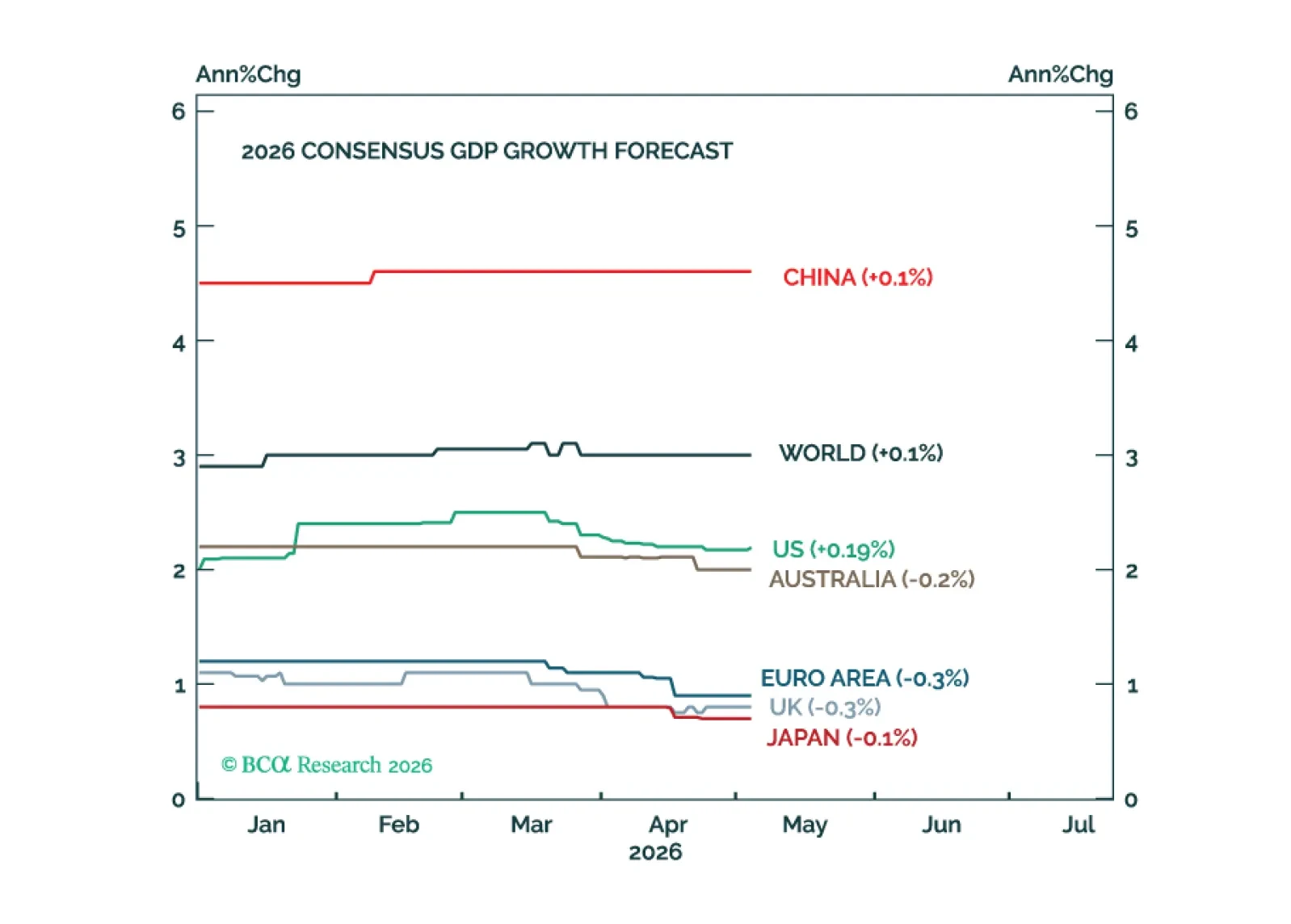

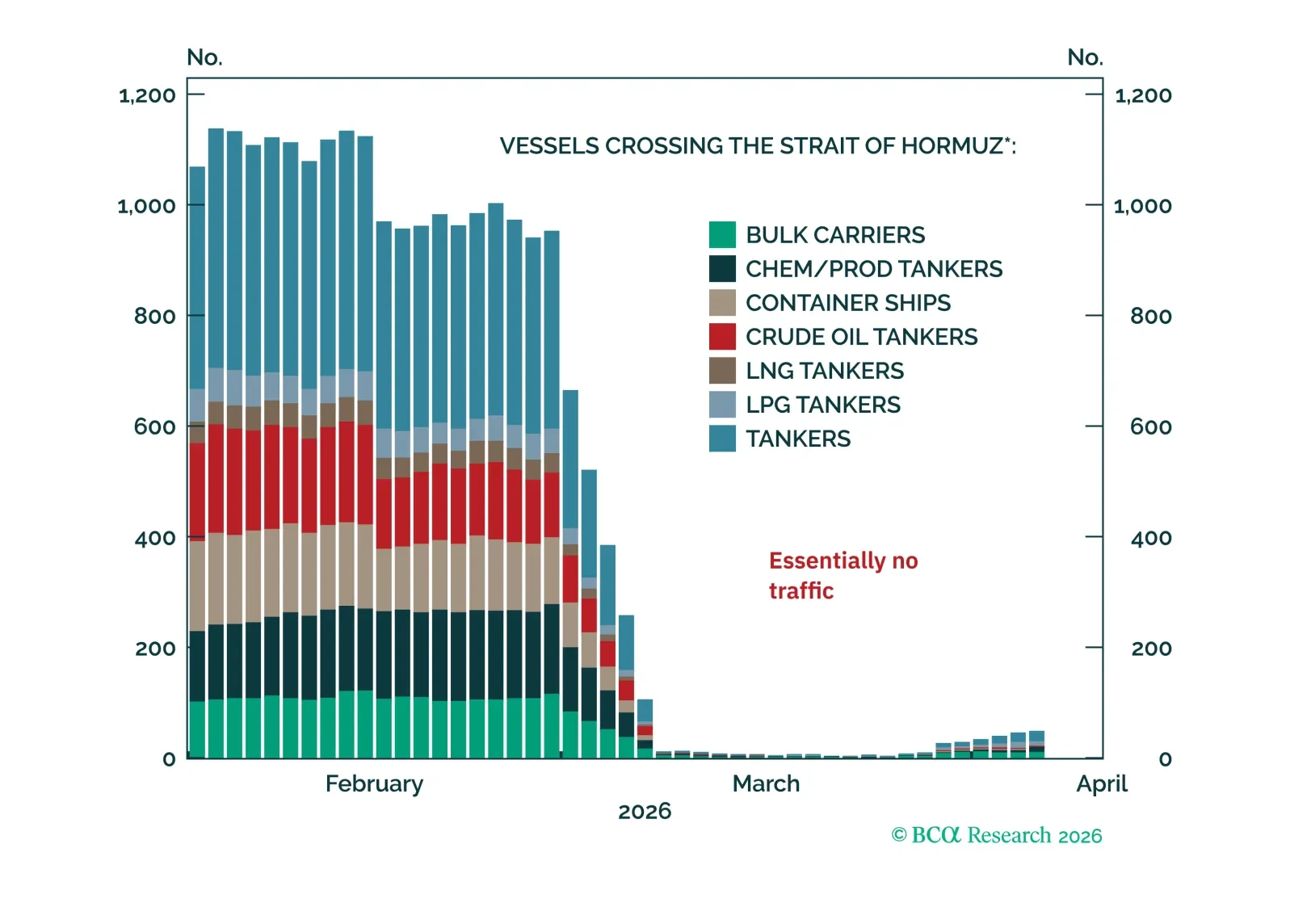

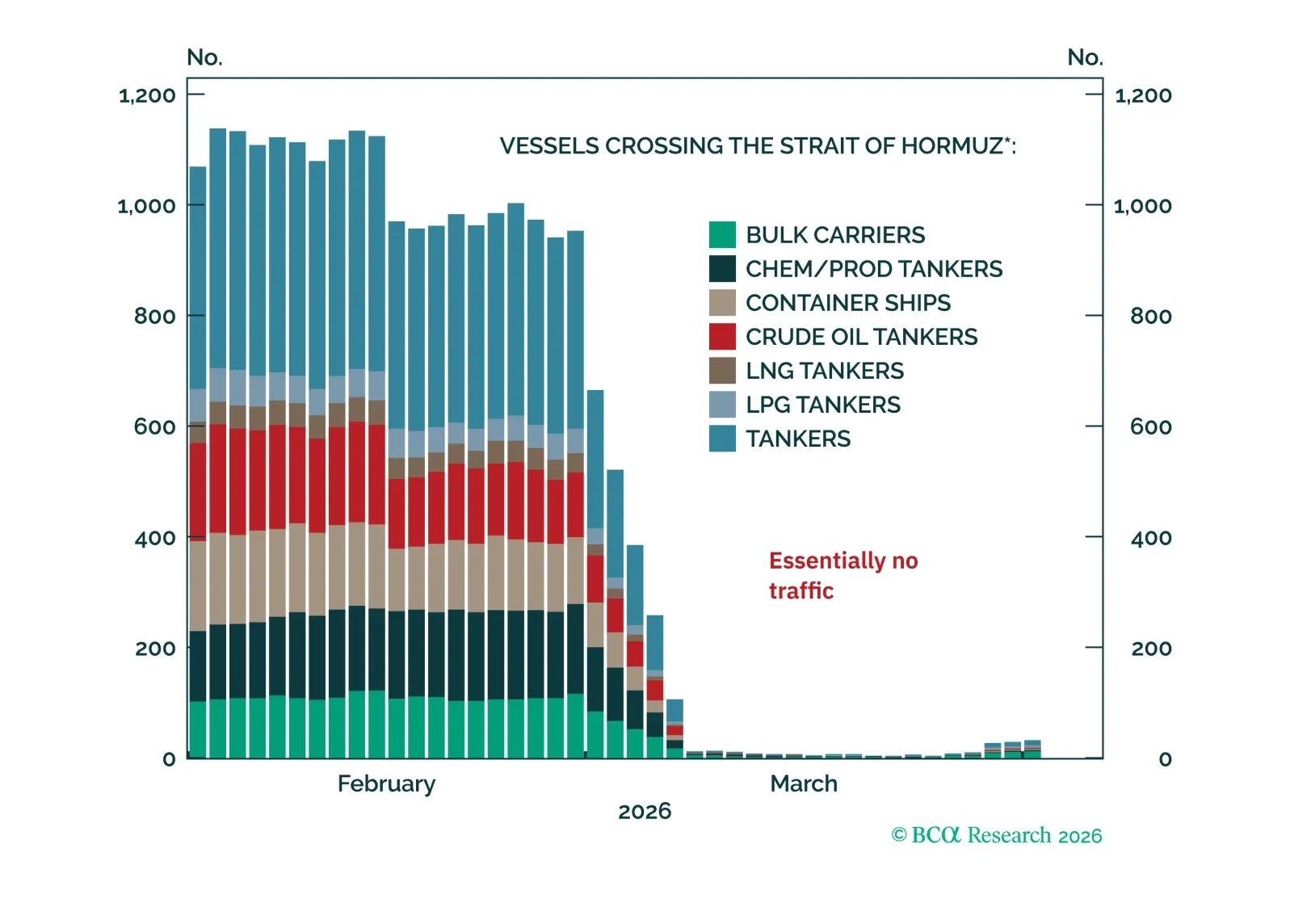

The global economy has weathered the oil shock reasonably well so far. However, the risk of a recession will increase meaningfully if the Strait of Hormuz remains closed into June.

The Iran war is likely to re-escalate later this year even if shipping somehow resumes in the very near term — and yet an early reopening is looking less likely.

The Iran war is deescalating further — against our expectations — setting up an aggressive return to the risk-on rally.

The relief rally in stocks can continue a while longer. However, much can still go wrong. As such, we are retaining a 12-month underweight to stocks but are moving to neutral on a short-term tactical horizon.

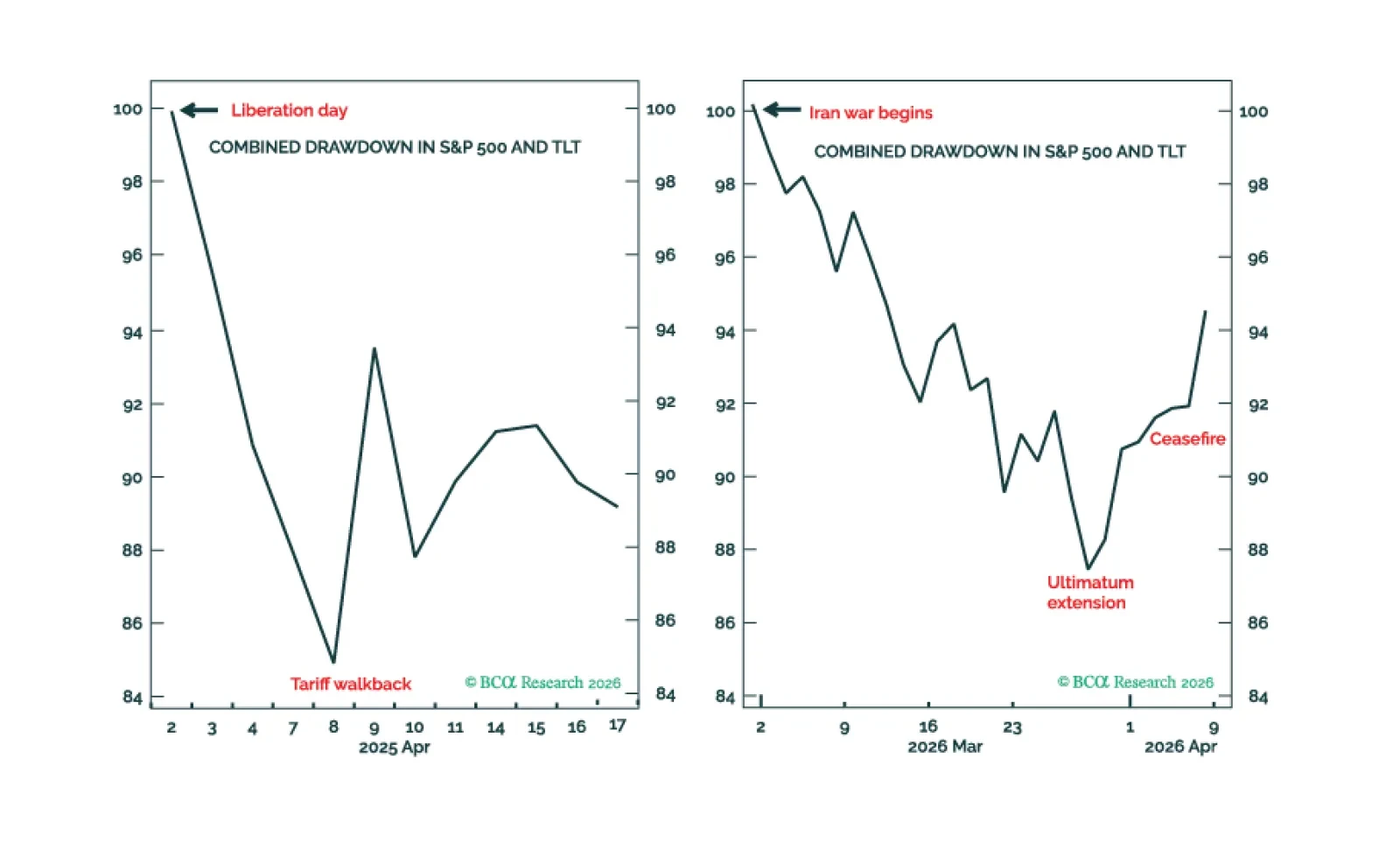

Trump’s breaking point is encapsulated by the combined drawdown in stocks plus bonds reaching 12-15 percent. On this basis, we describe how to ‘trade Trump’. Plus, we highlight three positions that should do well independent of Trump’s actions, including a new trade.

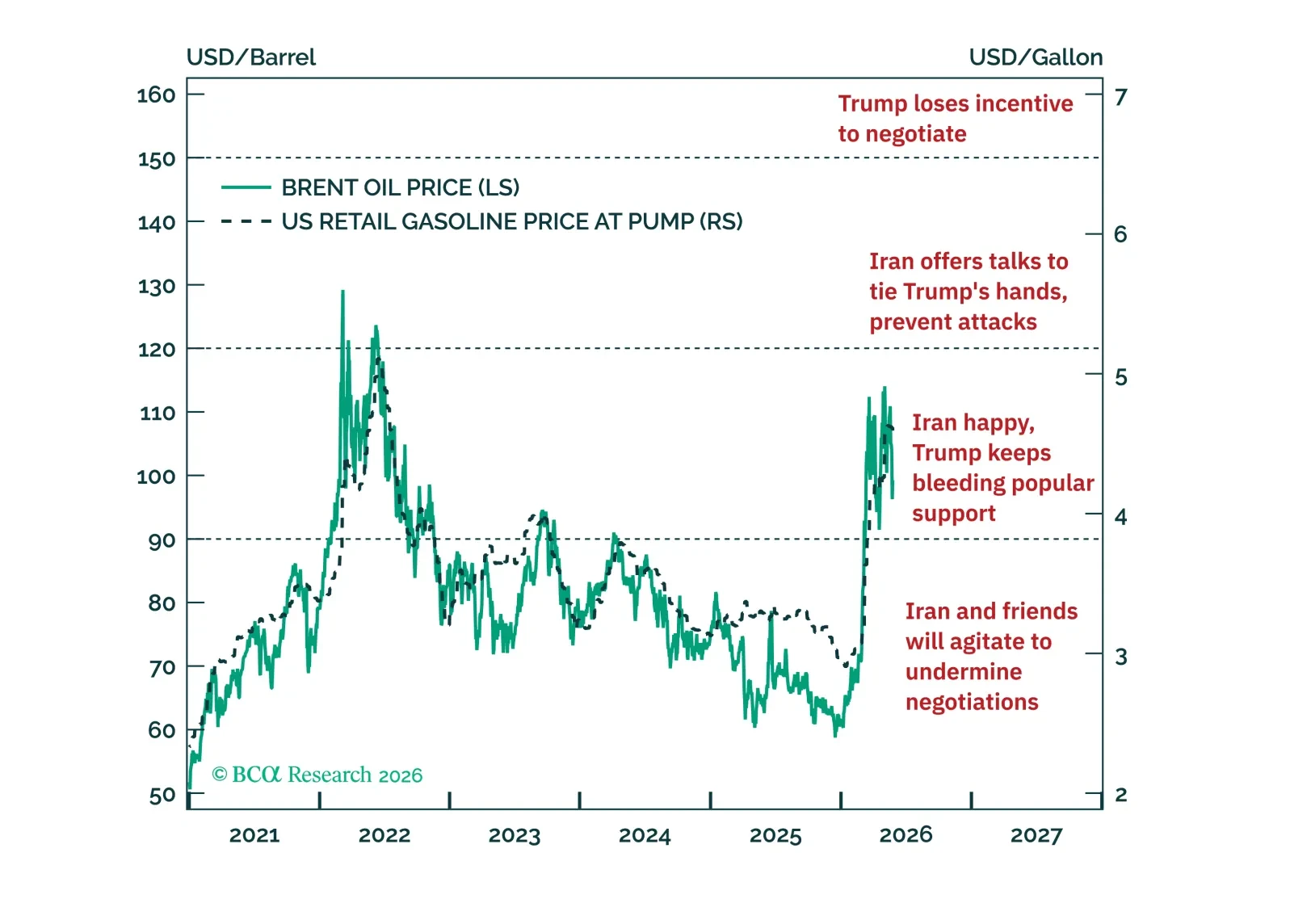

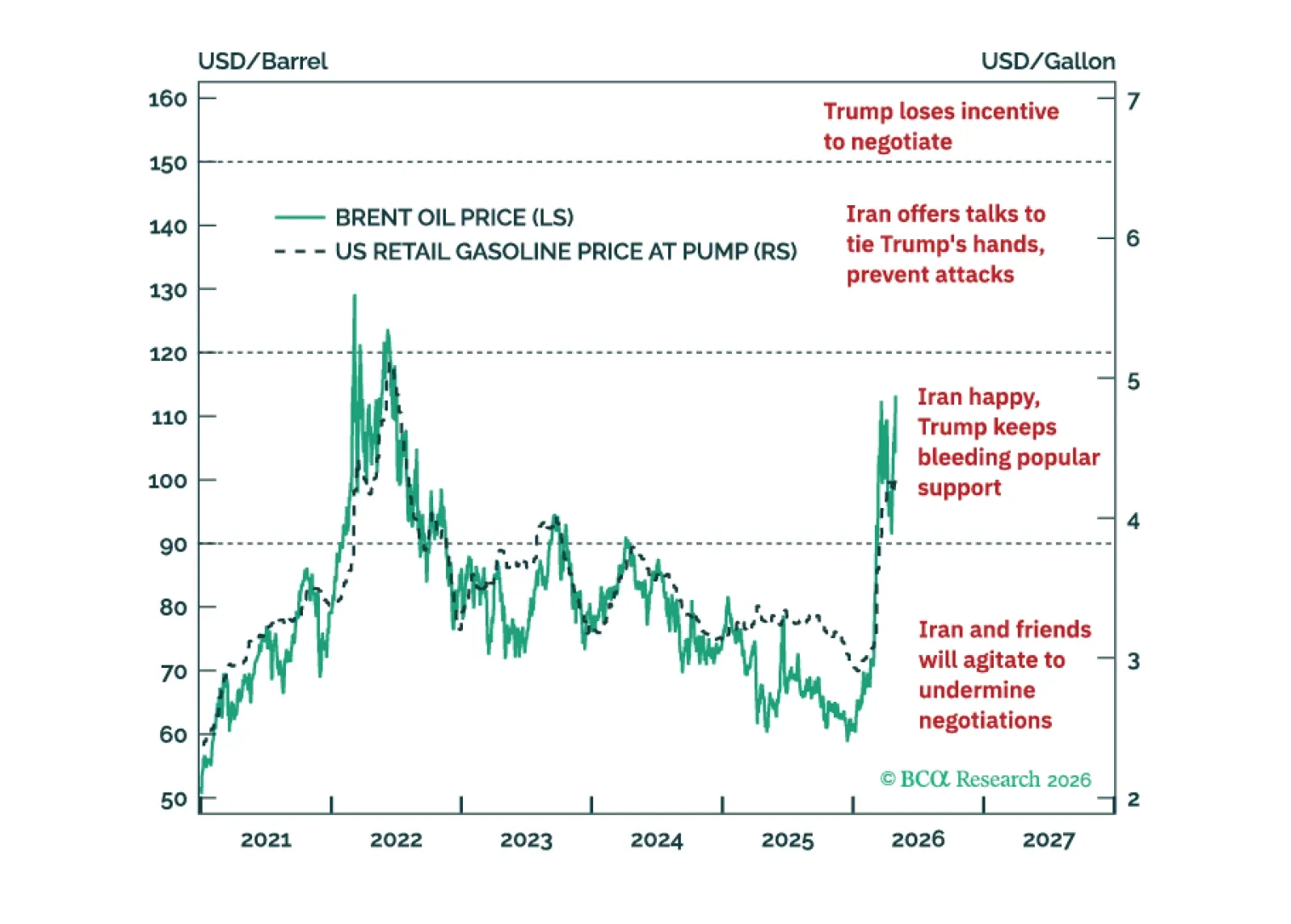

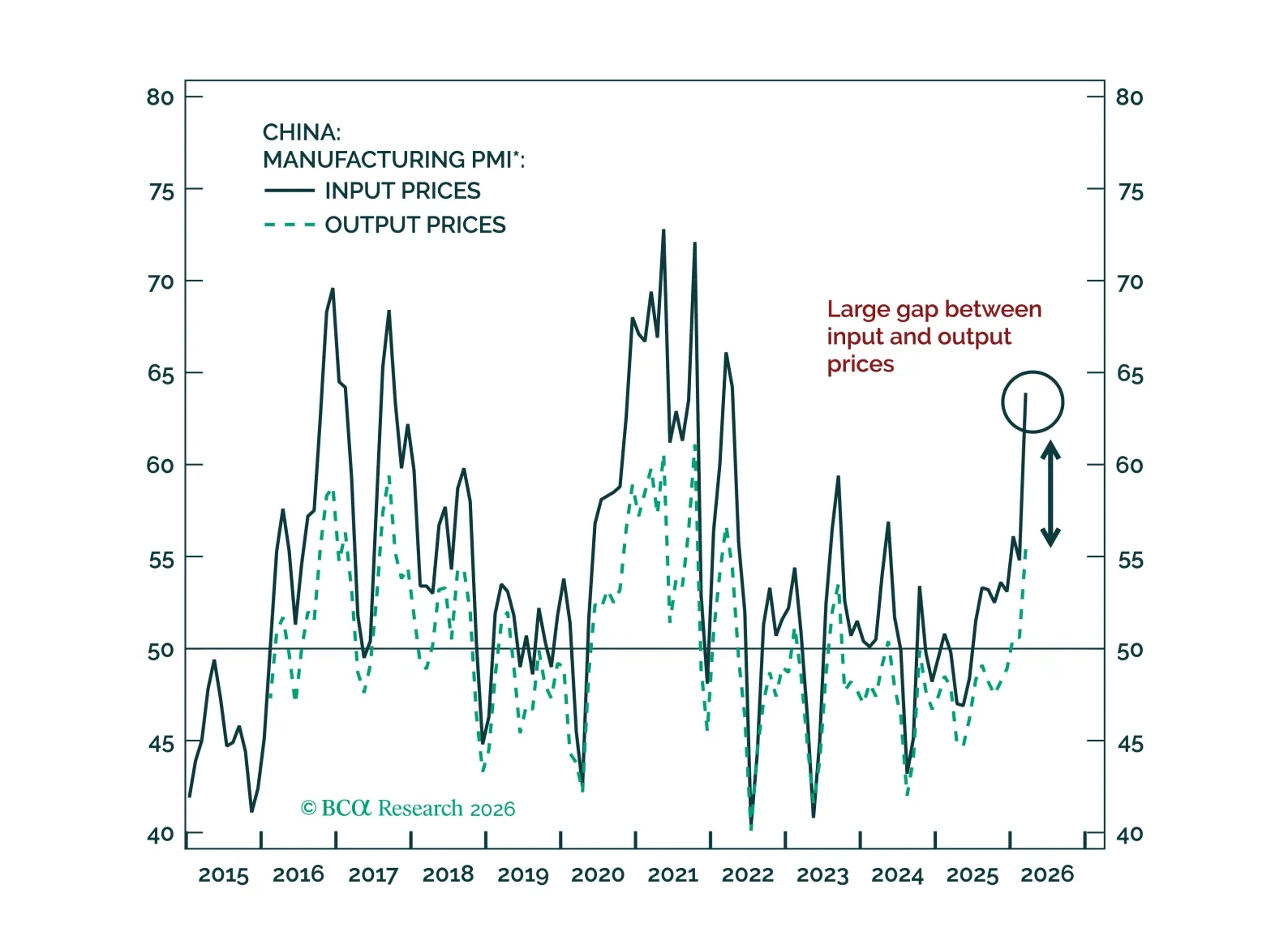

The ceasefire announced on Tuesday may signal peak intensity in the Middle East crisis, but sustained energy price pressures will continue to challenge Chinese corporate profitability.

Domestic politics suggest that President Trump needs to retreat from the war in Iran, but strategic factors suggest not. Stay defensive for now.

Our "miniature stagflation" episode is coming together on the back of the Iran shock, China slowdown, and American political division.