Yemen

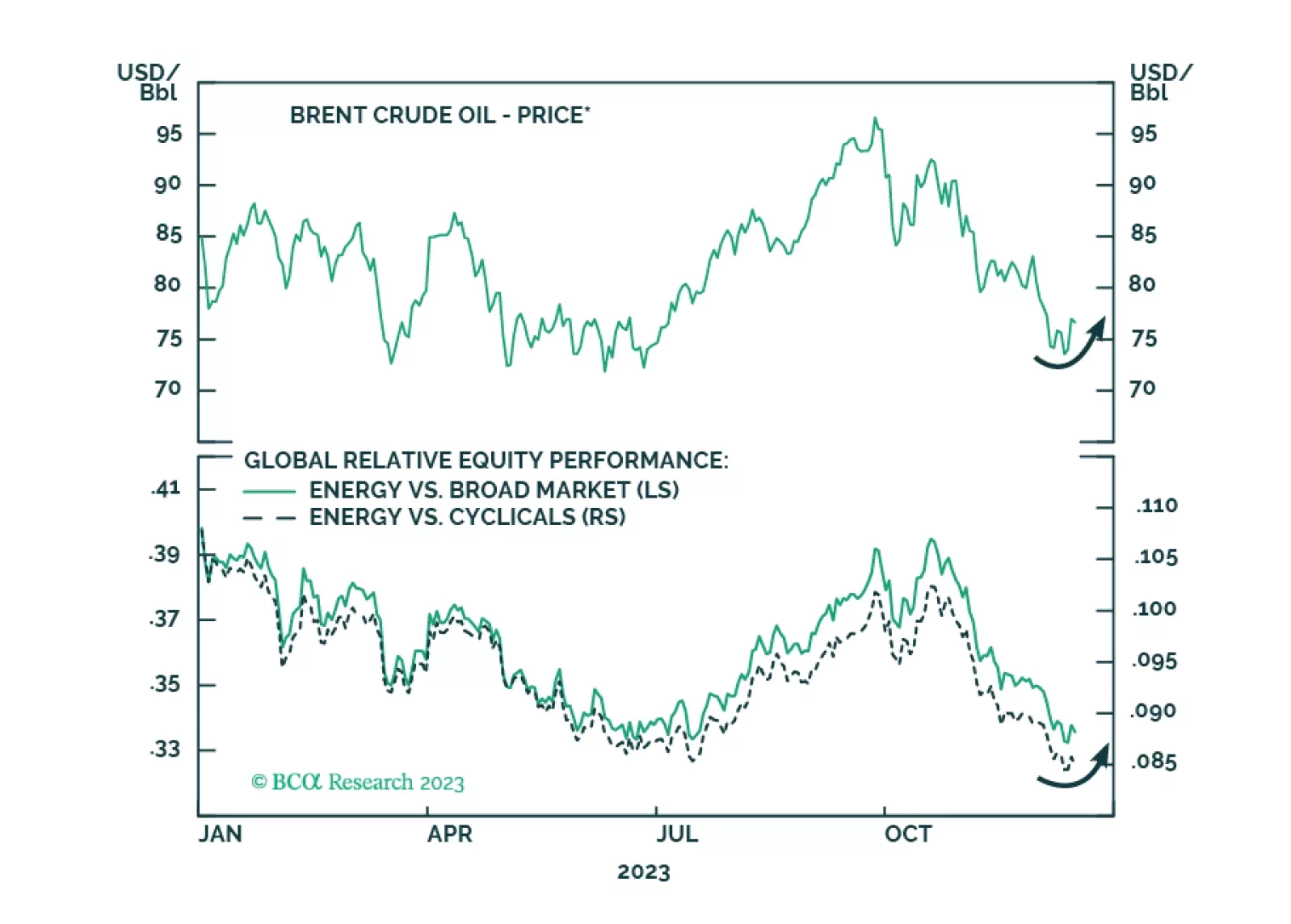

Oil prices will rise tactically due to supply risks. Recent developments indicate escalation of the conflict with Iran in the Middle East and confirm our expectation of energy supply disruptions and oil price spikes in the short run.

Highlights There is a tentative decline in geopolitical risk: An orderly Brexit or no Brexit is the likely final outcome and the U.S.-China talks are coming together. The outstanding geopolitical risks still warrant caution on global equities in the near term. Internal and external instability in Saudi Arabia, any American persistence with maximum pressure sanctions on Iran, and domestic instability in Iraq pose a risk to global oil supply. Go long spot crude oil and GBP/JPY. Feature Chart 1A Tentative Decline In Geopolitical Risk Our views on Brexit and the U.S.-China trade talks are coming together, resulting in a tentative decline in geopolitical risk (Chart 1). The British parliament still needs to ratify Boris Johnson’s exit agreement, painstakingly negotiated with the EU in a surprise summit this week. He may not have the votes. If he fails then he will have a basis to seek an extension to the Brexit deadline on October 31. But it is clear that the EU is willing to allow compromises to prevent a no-deal exit shock from exacerbating the slowdown in the European economy. An orderly Brexit is the final outcome (or no Brexit at all if an election and new referendum should say so). We are removing the $1.30 target on our long GBP/USD call in light of these developments and going long GBP/JPY. Similarly, while uncertainty lingers over U.S.-China relations, it is clear that President Trump is sensitive to the impact of the manufacturing recession and the risk of an overall recession on his reelection prospects. He is therefore pursuing a ceasefire and delaying tariffs. China is minimally reciprocating to forestall a collapse in relations. The December 15 tariff hike will be delayed and, if a ceasefire fails to improve the economic outlook, we expect Trump to engage in some tariff rollback on the pretext that talks are “making progress.” However, we do not expect a bilateral trade agreement or total tariff rollback. And other factors (like political risks in Greater China) could still derail the process. The outstanding geopolitical risks still warrant caution on global equities in the near term. These risks include a collapse in the U.S.-China talks (e.g. due to Hong Kong, Taiwan, or the tech race), and the ascent of Elizabeth Warren as the front runner in the Democratic Party’s early primary election. There is also the risk of another oil price shock emanating from the Middle East, which we discuss in this report. The Aftermath Of Abqaiq It has been a geopolitically eventful summer in the Middle East (Diagram 1). While there were plenty of warning shots, the September 14 drone and missile strikes on Saudi Aramco infrastructure was the big bang – wiping out 5.7 mm b/d of crude oil supplies overnight (Chart 2). The attacks were significant not only in terms of their impact on global oil markets, but also because they exposed the U.S.’s and Saudi Arabia’s reluctance to engage in a full-scale military confrontation with Iran. It is too early to call peak tensions in the Persian Gulf. Diagram 1Timeline: Summer Fireworks In The Persian Gulf Chart 2Closing Hormuz Would Be The Biggest Oil Shock Ever It is too early to call peak tensions in the Persian Gulf. The October 11 strike on an Iranian-owned oil tanker in the Red Sea and the reported U.S. cyber-attacks against Iranian news outlets may well mark the “limited retaliation” that we expected. Nevertheless, last month’s events uncovered vulnerabilities that suggest that even if the U.S. and its Gulf allies back off, geopolitical risk will remain elevated. Chart 3Saudis Are Profligate Defense Spenders The most obvious outcome of the September 14 attack is the realization of just how vulnerable Saudi Arabia is to attacks by its regional enemies. Despite being the third most profligate defense spender in the world – and the first relative to GDP (Chart 3) – Saudi Arabia was unable to protect its critical infrastructure. For that, Crown Prince Mohamed bin Salman (MBS) will surely face domestic pressure. After five years, Saudi Arabia has little to show from its war in Yemen, other than a humanitarian crisis that has hurt its international standing. Instead, the operation has been a burden on the kingdom’s finances and a nuisance to security in the southwestern provinces of Najran, Jizan and Asir, where the Iran-allied Houthis have conducted regular attacks on oil infrastructure and airports. Some domestic disquiet will be defused if the Yemen war is downgraded or resolved. Saudi Arabia recently accepted the olive branch extended by the Houthis and is reportedly in talks to deescalate. But this will not fully eliminate domestic uncertainty. After all, MBS’s other initiatives – in Syria, in Iraq, in lobbying the U.S. – are also in jeopardy. The conspiracy theory surrounding the September 29 murder of General Abdulaziz al-Faghem, King Salman’s longstanding personal bodyguard, is case in point. Rumor has it that the king was enraged upon hearing of the Houthi movement’s September 28 capture of three Saudi military brigades, and decided to revoke the Crown Prince’s title, instead appointing the youngest Sudairi brother, Prince Ahmed bin Abdulaziz, in his place.1 The ploy was allegedly uncovered, resulting in General al-Faghem’s murder.2 This is entirely speculation and we find the idea of MBS’s removal to be highly doubtful. The King’s and Crown Prince’s joint appearance during President Vladimir Putin’s visit to the kingdom earlier this week should dispel speculation about a brewing palace coup. Nevertheless, the murder itself is extremely concerning and reinforces independent reasons for concerns about internal stability. Chart 4Impatient Diversification Threatens Domestic Stability The pursuit of the Saudi reform agenda, “Vision 2030,” is premised first and foremost on the consolidation of power in the hands of MBS and his faction. The appointment of King Salman’s son, Prince Abdulaziz, as energy minister was motivated by a desire to expedite the initial public offering of state oil giant Saudi Aramco, which could begin as early as November. This was preceded by the appointment of Yasir Al-Rumayyan, head of the sovereign wealth fund and a close ally of MBS, as chairman of Aramco. Moreover, wealthy Saudis – some of whom were detained at the Ritz Carlton in November 2017 – are reportedly being strong-armed into buying stakes in the pending IPO. While weaning Saudi Arabia’s economy off of crude oil is the best course of action for long-term stability (Chart 4), the transition will threaten domestic stability. Meanwhile the conflict with Iran is far from settled. Bottom Line: The September 14 drone strikes on key Saudi oil infrastructure revealed both Saudi Arabia’s and the U.S.’s unwillingness to engage in military action against and a full confrontation with Iran. This will raise concerns regarding the kingdom’s ability to defend itself. Moreover, Saudi Arabia remains vulnerable to domestic pressure as MBS strives to maintain his consolidation of power in recent years and pursues Vision 2030. Internal or external instability in Saudi Arabia poses a risk to global oil supply. Iran’s Resistance Economy Can Handle Trump’s Maximum Pressure Chart 5Iran's Economy Is Feeling The Bite On the other side of the Persian Gulf, the Iranians are displaying a higher pain threshold than their enemies. The economy is suffering under the U.S.’s crippling sanctions, with exports at the lowest level since 2003 (Chart 5). The IMF expects Iran’s economy to contract by 9.5% this year, with annual inflation forecast at 35.7%. Oil exports, the lifeblood of its economy, are down 89% YoY. Nevertheless, Iran is well-versed in the game of chicken, it is methodically displaying its ability to create havoc across the region, and it has not waivered in its stance that President Trump must ease sanctions and rejoin the 2015 nuclear deal if it is to engage in bilateral talks. All the while, Iran continues to reduce its nuclear commitments. On September 5, Rouhani indicated plans to completely abandon research and development commitments under the Joint Comprehensive Plan of Action (JCPOA) and to begin working on more advanced uranium enrichment centrifuges which was capped at 3.7% under the JCPOA (Table 1). We also expect Iran to follow-through on its threat of withdrawing from the Nuclear Non-Proliferation Treaty (NPT) if Trump maintains sanctions. Table 1Iran Is Walking Away From 2015 Nuclear Deal The same resolve cannot be shown on the part of the United States or Saudi Arabia. Chart 6Americans Do Not Support War With Iran President Trump is constrained by the risk of an Iran-induced oil price shock ahead of the 2020 election. He is therefore eager to deescalate tensions with Iran. He is abandoning the field in Syria (on which more below), opting to add a symbolic 1,800 troops into Saudi Arabia for deterrent effect instead. This defensive posture is being undertaken within the context of American public opinion, which opposes war with Iran or additional military adventures in the Middle East (Chart 6). This signifies the U.S.’s strategic deleveraging from the Middle East in order to shift its focus to Asia Pacific, where America has a greater priority in managing the rise of China. At the same time, negotiations between the Saudis and Yemeni Houthis suggest a lack of Saudi appetite for all-out conflict with Iran, clearing the way for a diplomatic solution. As Rouhani stated “ending the war in Yemen will pave the ground for de-escalation in the region,” specifically between Saudi Arabia and Iran. The Saudis have amply signaled in the wake of the Abqaiq attack that they wish to avoid a direct confrontation, particularly given the Trump administration’s apparent unwillingness (under electoral constraint) to continue providing a “blank check” for MBS to conduct an aggressive foreign policy. Already the United Arab Emirates – a key player in the Saudi-led coalition against Yemen – has distanced itself from Riyadh and sought to ease tensions with Iran. It recently reduced its commitment to the Yemen war and engaged in high-level meetings with Iran. The UAE’s national security adviser, Tahnoun bin Zayed, visited Tehran on a secret mission, the latest in a series of backchannel efforts to mediate between Saudi Arabia and Iran. Other reported efforts at diplomacy include visits by Iraqi and Pakistani officials. The remaining uncertainty is whether Trump will quietly ease sanctions on Iran, and whether Iran will quit while it is ahead. If Trump maintains maximum pressure, Iran may need to stage further attacks and oil disruptions to threaten Trump’s economy and encourage sanction relief. Otherwise, Iran, smelling American and Saudi fear, could overstep its bounds and commit a provocation that requires a larger American response, thus re-escalating tensions. While Trump’s economic and electoral constraint suggests that he will ease sanctions underhandedly, Iran’s risk appetite is apparently very high: Abqaiq could have gone terribly wrong. It also has an opportunity to flex its muscles and demonstrate American inconstancy to the region. This could lead to miscalculation and a more significant oil price shock than already seen. Bottom Line: Iran has remained steadfast in its position while the United States, Saudi Arabia, and their allies appear to be capitulating. They have more to lose than gain from all-out conflict. But Iran’s decision-making is opaque and any American persistence with maximum pressure sanctions will motivate additional provocations, escalation, and oil supply disruption. Making Russia Great Again? Recent events in Turkey and Syria do not come as a surprise. We have long highlighted a deeper Turkish intervention into Syria as a regional “black swan” event. In August we warned clients that the Trump-Erdogan personal relationship would not save Turkey from impending U.S. sanctions. In September we warned that Turkish geopolitical risk premia had collapsed, as measured by our market-based GeoRisk indicator, and that this collapse was certain to reverse in a major way, sending the lira falling. As we go to press the Turks have declared a ceasefire to avoid sanctions but nothing is certain. Putin has pounced on the opportunity to capitalize on the U.S. retreat. If Turkey is the loser, who is the winner? First, Trump, who benefits from fulfilling a campaign pledge to reduce U.S. involvement in foreign wars – a stance that will ultimately be rewarded (or at least not punished) by a war-weary public. Second, Iran and Russia, Syria’s major allies, who have invested greatly in maintaining the regime of Bashar al-Assad throughout the civil war and now face American withdrawal and heightened U.S. tensions with its allies and partners in the region as a result. Iran benefits through the ability to increase its strategic arc, the so-called “Shia Crescent,” to the Mediterranean Sea. Russia benefits through solidifying its reclaimed status as a major player in the Middle East – an indication of global multipolarity. President Vladimir Putin has pounced on the opportunity to capitalize on the U.S. retreat with official visits to both Saudi Arabia and the UAE this week. He made promises of both stronger economic ties and the ability to broker regional power. On the economic front, the Russian Direct Investment Fund (RDIF) selected Saudi Arabia as the venue for its first foreign office, signaling its interest in the region. It has already approved 25 joint projects with investment valued at more than $2.5 billion. There are also talks of RDIF-Aramco projects in the oil services sector worth over $1 billion and oil and gas conversion projects worth more than $2 billion. Moreover, RDIF signed multiple deals worth $1.4 billion with UAE partners. Chart 7Russia Has Been Complying With OPEC 2.0 Cuts Most importantly, the Saudis and Russians share the same objective of supporting global oil prices and have been jointly managing OPEC 2.0 supply since 2017 (Chart 7). Russia’s approach to the region focuses on enhancing its all-around strategic influence. Chart 8Erdogan Is Playing Into Turkish Concerns About Syrian Refugees Although Russia’s allies include Iran and Syria – Saudi Arabia’s rivals – it has presented itself as a pragmatic partner to other powers, including Turkey and even the Saudis and Gulf states. As such, the Kremlin has leverage on both sides of the regional divide, giving it the potential to serve as a power broker. However, any Saudi purchase of the Russian S-400 defense system, long under negotiation, would unsettle the United States. Turkey is threatened with American sanctions for its purchase of the same system.3 The U.S. may be willing to tolerate some increased Russian influence in the Middle East, but a defense agreement may be its red line. The Trump administration still wields the stick of economic sanctions. Growing Russian influence extends beyond the Gulf states. The U.S.’s withdrawal from northeast Syria last week and the Turkish invasion is a gift to the Russians. They are now the only major power from outside the Middle East engaged in Syria. They have embraced this position, positioning themselves as peace brokers between the Syrian regime, with whom they are allied, and Turkey, as well as the Turkish arch-enemy, the Kurds, who now lack American support and must turn to Syria and Russia for some kind of arrangement to protect themselves. Russia has therefore cemented its return as a strategic player in the region, after its initial intervention in Syria in 2015. Turkey’s incursion into Syria is an attempt by President Erdogan to confront the battle-hardened Syrian Kurds and prevent a Kurdish-controlled continuous border with Syria, and to distract from his weakened domestic position. He is striving to garner support by playing to broad Turkish concerns about Syrian refugees in Turkey (Chart 8). The intervention will seek to create a space for refugees to be placed on the Syrian side of the border. However given that there is little domestic popular support for a military intervention, he runs the risk of further alienating voters, who are already losing patience with his ruling Justice and Development Party (AKP). So far, the incursion has the official support of all Turkey’s political parties except the Kurdish Peoples’ Democratic Party (HDP). However this will change as the intervention entails western economic sanctions, a drawn-out military conflict, and limited concrete benefits other than the removal of refugees. Chart 9Turkey's Already Vulnerable Economy Will Take A Hit The already vulnerable economy is likely to take a hit (Chart 9). Markets have reacted to the penalties imposed by the U.S. so far with a sigh of relief as they are not as damaging as they could have been – i.e. Turkish banks were spared.4 However, this is just the opening salvo and more sanctions are on the way – Congress is moving to impose sanctions of its own, which Trump is unlikely to veto. Moreover, the European Union is following suit and imposing sanctions of its own, including on military equipment. Volkswagen already announced it is postponing a final decision on whether to build a $1.1 billion plant in Turkey. This comes at a time of already existing sensitivities with the EU over Turkish oil and gas drilling activities in waters off Cyprus. EU foreign ministers are responding by drawing up a list of economic sanctions. These economic risks will likely hold back the central bank’s rate cutting cycle as the lira and financial assets will take a hit. Bottom Line: The U.S. pivot away from the Middle East is a boon for Moscow, which is pursuing increased cooperation in the Gulf and gaining influence in Syria. Russia is marketing itself as a strategic player and effective power broker. Erdogan’s incursion in Syria, while motivated by domestic weakness, will backfire on the Turkish economy. Maintain a cautious stance on Turkish currency and risk assets. Iraq Is The Fulcrum Iraq’s geographic position, wedged between Saudi Arabia and Iran, renders it the epicenter of the regional power struggle. In the wake of the Trump administration’s maximum pressure campaign on Iran we have frequently highlighted that a dramatic means of Iranian pushback, short of closing shipping in the Strait of Hormuz, is fomenting unrest in an already unstable Iraq. This would be a threat to U.S. strategy as well as to global oil supplies. Iraq is the epicenter of the regional power struggle. In this context, Iraq’s revered Shia cleric Muqtada al-Sadr’s visit to Iran on September 10, just four days ahead of the September Saudi Aramco attack, raises eyebrows. Sadr is the key player in Iraq today and over the past two years he had staked out a position of national independence for Iraq, eschewing overreliance on Iran. A rapprochement between Sadr and Iran is a negative domestic development for Iraq, which has recently been making strides to reduce Iran’s political and military grip. It would undermine Iraqi stability by increasing divisions over ideology, sect, economic patronage, and national security. There is speculation that Sadr’s trip was intended to discuss Prime Minister Adel Abdul Mahdi, who is perceived as weak and incapable of managing the various powers on Iraq’s political scene. The violent protests rocking Iraq since early September support this assessment. Protestors are motivated by discontent over unemployment, poor services, and government corruption, which are perceived to have mostly deteriorated since the start of Abdul Mahdi’s term (Chart 10). While Abdul Mahdi has announced some reforms in response to the popular discontent, including a cabinet reshuffle and promises of handouts for the poor, they have done little to quell the protests. The popular demands are only one of the existential threats facing the government. The second and potentially more serious risk is the security threat. Iraq has been failing at its attempts to formally integrate the Popular Mobilization Units (PMU) – Iran-backed paramilitary groups that were instrumental in ISIS’s defeat – into the national security forces. This is essential in order to prevent Iran from maintaining direct control of security forces within Iraq. A majority of the public agrees that the PMU should not play a role in politics (Chart 11), reflecting the underlying trend demanding Iraqi autonomy from Iran. Chart 10Rising Discontent In Iraq Chart 11Little Support For A Political Role For The PMU Given that the PMU is in effect an umbrella term for ~50 predominantly Shia paramilitary groups, internal divisions exist within the forces which compete for power, legitimacy, and resources. Recently, it has been purging group leaders perceived as a threat to the overall forces and the senior leadership which maintain strong links to Iran. Chart 12Iraq Is Divided Across Political Affiliation This internal struggle also reflects the intra-Shia struggle for power among Iraq’s main political parties. On the one side there is the conservative, pro-Khamenei bloc led by former Prime Minister Nouri al-Maliki and PMU commander Hadi al-Ameri, and on the other is the reformist, nationalist leader Muqtada al-Sadr’s joined by Ammar al-Hakim. Given that most Iraqis view their country as a divided nation across political affiliation, this is a risk to domestic stability (Chart 12). Thus even if the wider risk of regional tensions abates and reduces the threat of sabotage to oil infrastructure and transportation, the current domestic situation in Iraq remains uneasy. But given that we do not see the regional tensions abating yet – due to either American maximum pressure or Iranian hubris – this dynamic translates into an active threat to oil supplies, with 3.4 mm b/d of exports concentrated in the southern city of Basra. Bottom Line: Heightened domestic instability in Iraq poses a non-negligible threat to oil supplies. This risk is compounded by Iraq’s location as a geographic buffer between regional rivals Iran and Saudi Arabia, and Iran’s interest in fomenting unrest to pressure the U.S. into relaxing sanctions. Investment Conclusions The common thread across the Middle East is a persistent threat to global oil supply in the wake of the extraordinary Abqaiq attack. First, it cannot be stated with confidence that Iran will refrain from causing additional oil disruptions, as it is convinced that President Trump’s appetite for conflict is small (and Trump is indeed constrained by fear of an oil shock). President Rouhani has an interest in removing Trump from power, which an oil shock might achieve, and the Supreme Leader may even be willing to risk a conflict with the United States as a means of increasing support for the regime and infusing a new generation with revolutionary spirit. Iran loses in a total war, but Tehran is convinced that the U.S. does not have the will to engage in total war. Second, Russia’s interest in the region is not in generating a durable peace but in filling the vacuum left by the United States and making itself a power broker. Any instability simply increases oil prices which is positive for Russia. Third, Iraq’s instability is both domestically and internationally driven. It is nearly impossible to differentiate between the two. Iranian hubris could manifest in sabotage in Iraq. Or Iraq could destabilize under the regional pressures with minimal Iranian encouragement. Either way the world’s current below-average spare oil production capacity could be hit sooner than expected if shortages result. Go long spot crude oil. On equities, with a U.S.-China ceasefire in the works, and little chance of a no-deal Brexit, we see our cyclically positive outlook reinforced, though we maintain near-term caution due to U.S. domestic politics. In terms of equity focus, we are overweight European equities in developed markets and Southeast Asian equities in emerging markets. Roukaya Ibrahim, Editor/Strategist Geopolitical Strategy RoukayaI@bcaresearch.com Footnotes 1 The Sudairi branch of the al-Saud family is made up of the seven sons of the late King Abdulaziz and Hussa al-Sudairi of the powerful Najd tribe. 2 Please see TRT World “Killing of Saudi King’s Personal Bodyguard Triggers Speculation,” October 2, 2019, available at https://www.trtworld.com. 3 In the wake of the attack on Saudi Aramco oil facilities, President Putin trolled the U.S. by recommending that Saudi Arabia follow the footsteps of Iran and Turkey in purchasing Russia’s S-300 or S-400 air defense systems. 4 The U.S. penalties include sanctions against current and former officials of the Turkish government, a hike in tariffs on imports of Turkish steel back up to 50 percent, and the halt in negotiations on a $100 billion trade deal.