Yield Curve

Our Portfolio Allocation Summary for August 2025.

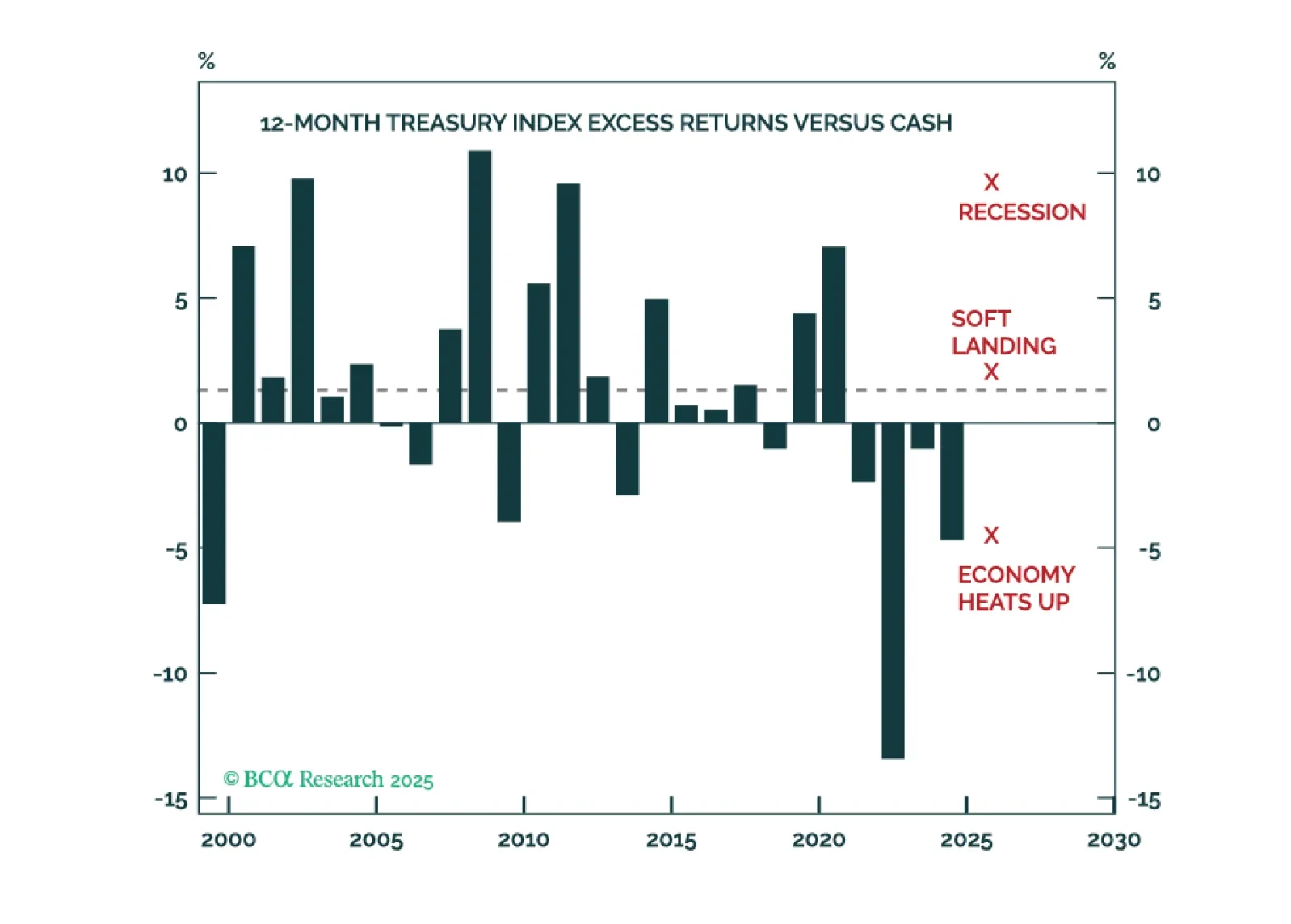

Investors should anticipate above average Treasury returns during the next 12 months, and curve steepeners will continue to profit.

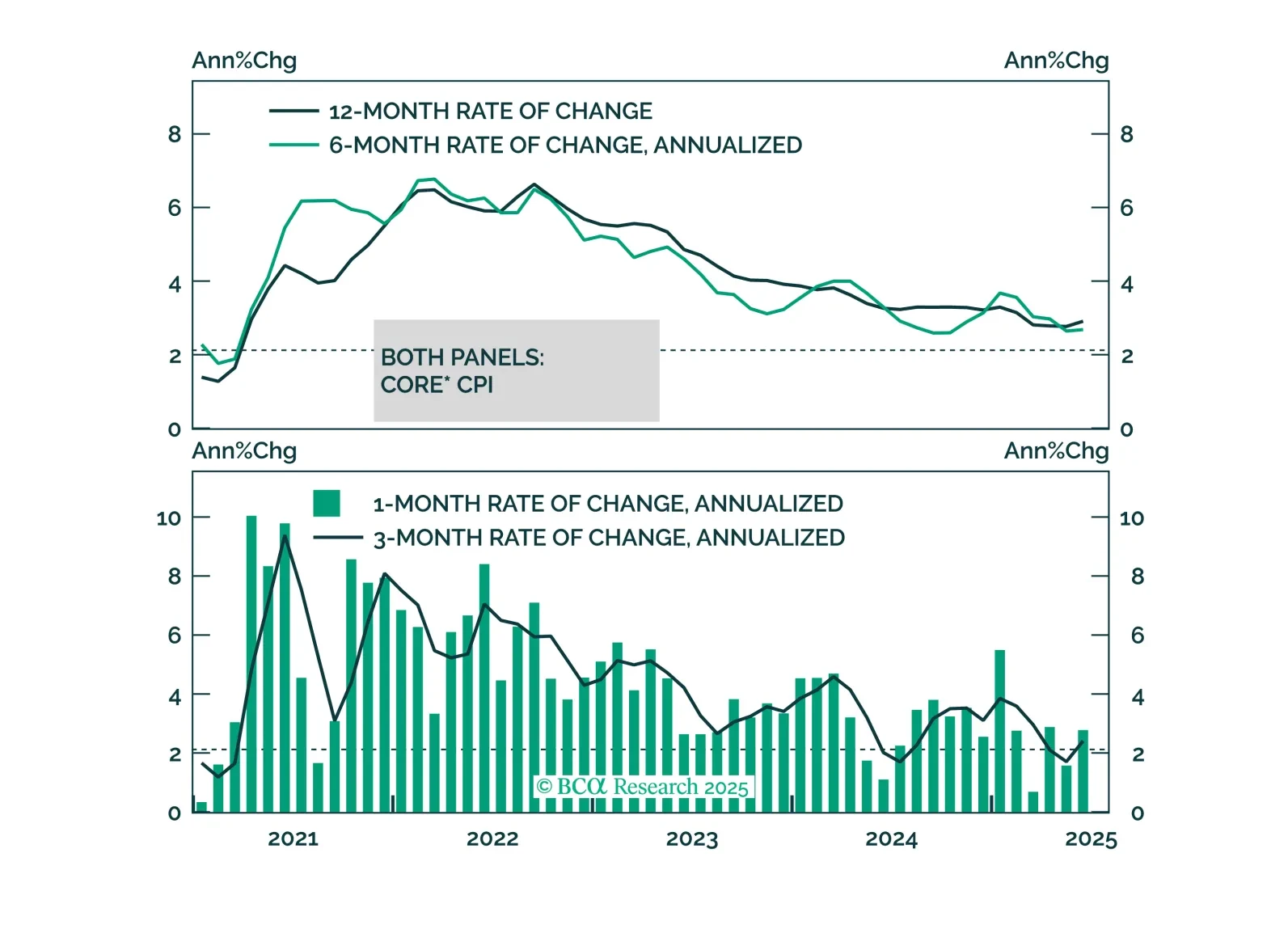

We discuss the implications of this morning’s CPI report and the relative attractiveness of 2/5 Treasury curve steepeners.

Our Portfolio Allocation Summary for July 2025.

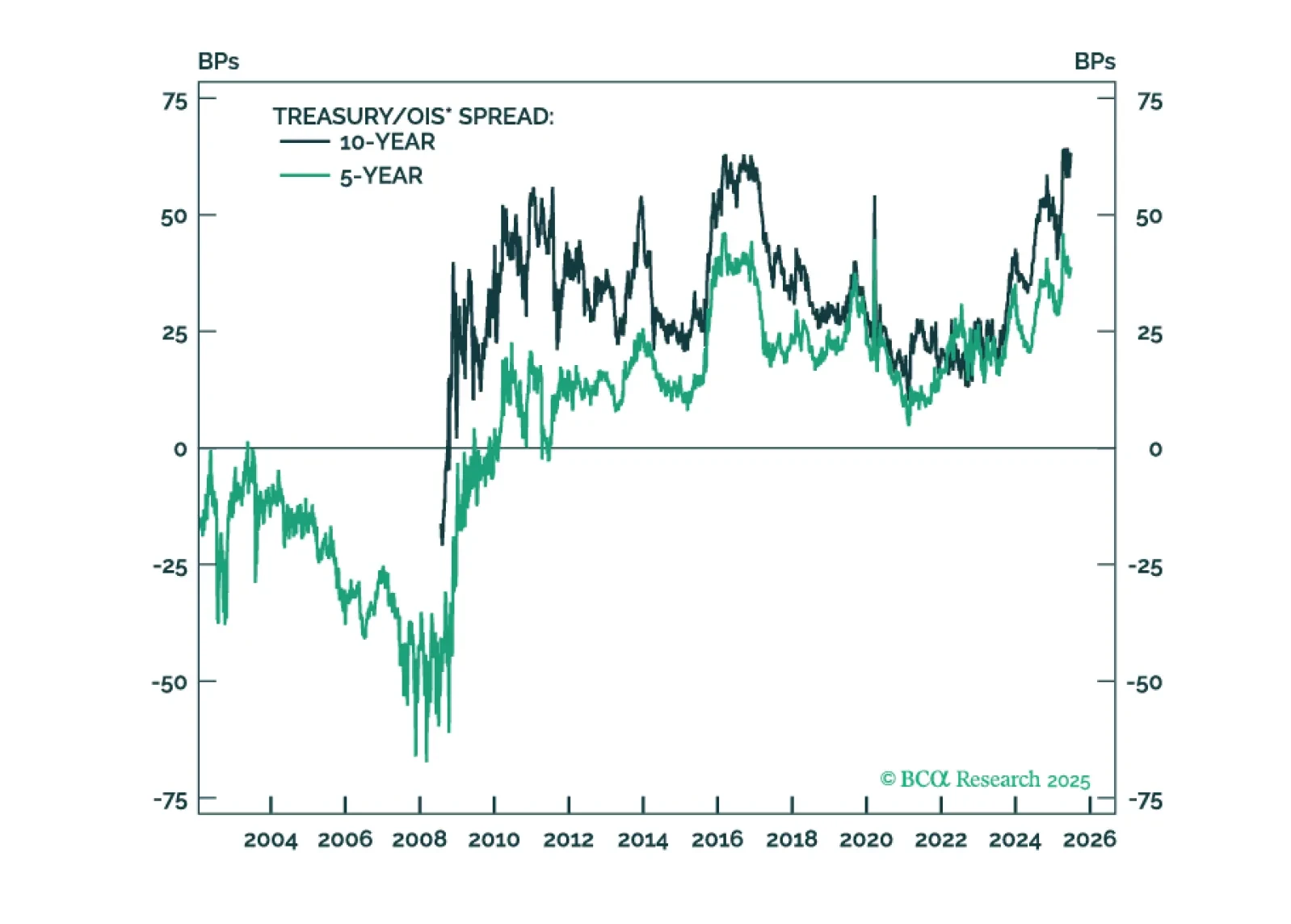

The Treasury/OIS spread has exerted notable upward pressure on Treasury yields during the past year, but the factors driving the spread are now turning more favorable.

Our Portfolio Allocation Summary for June 2025.

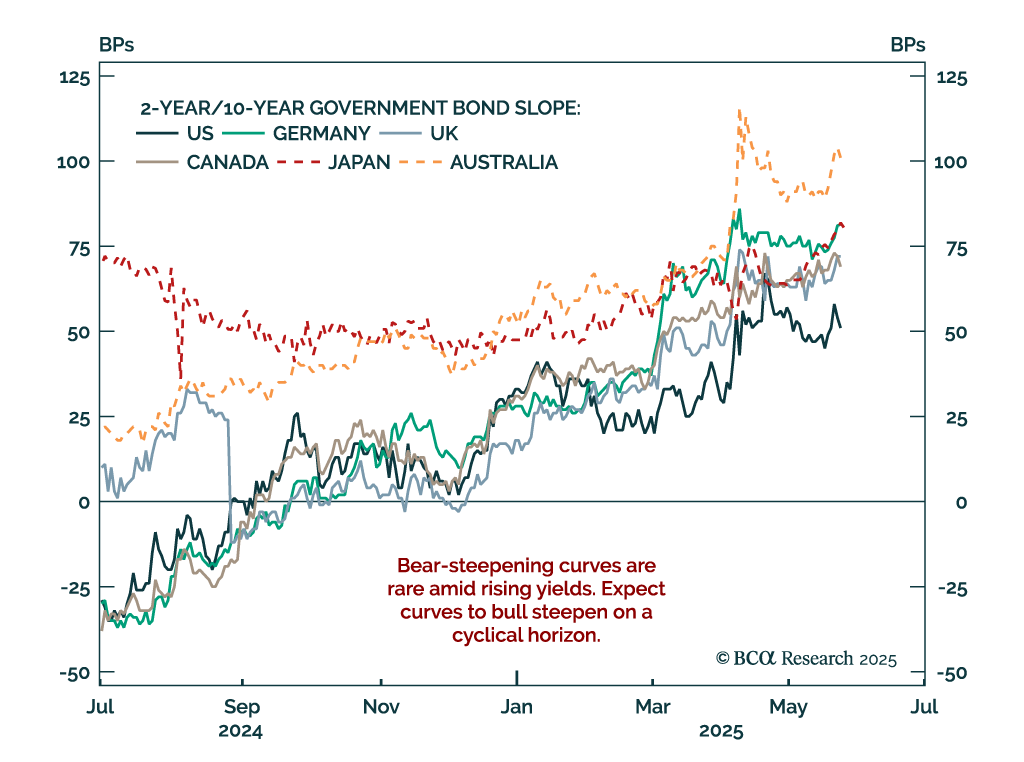

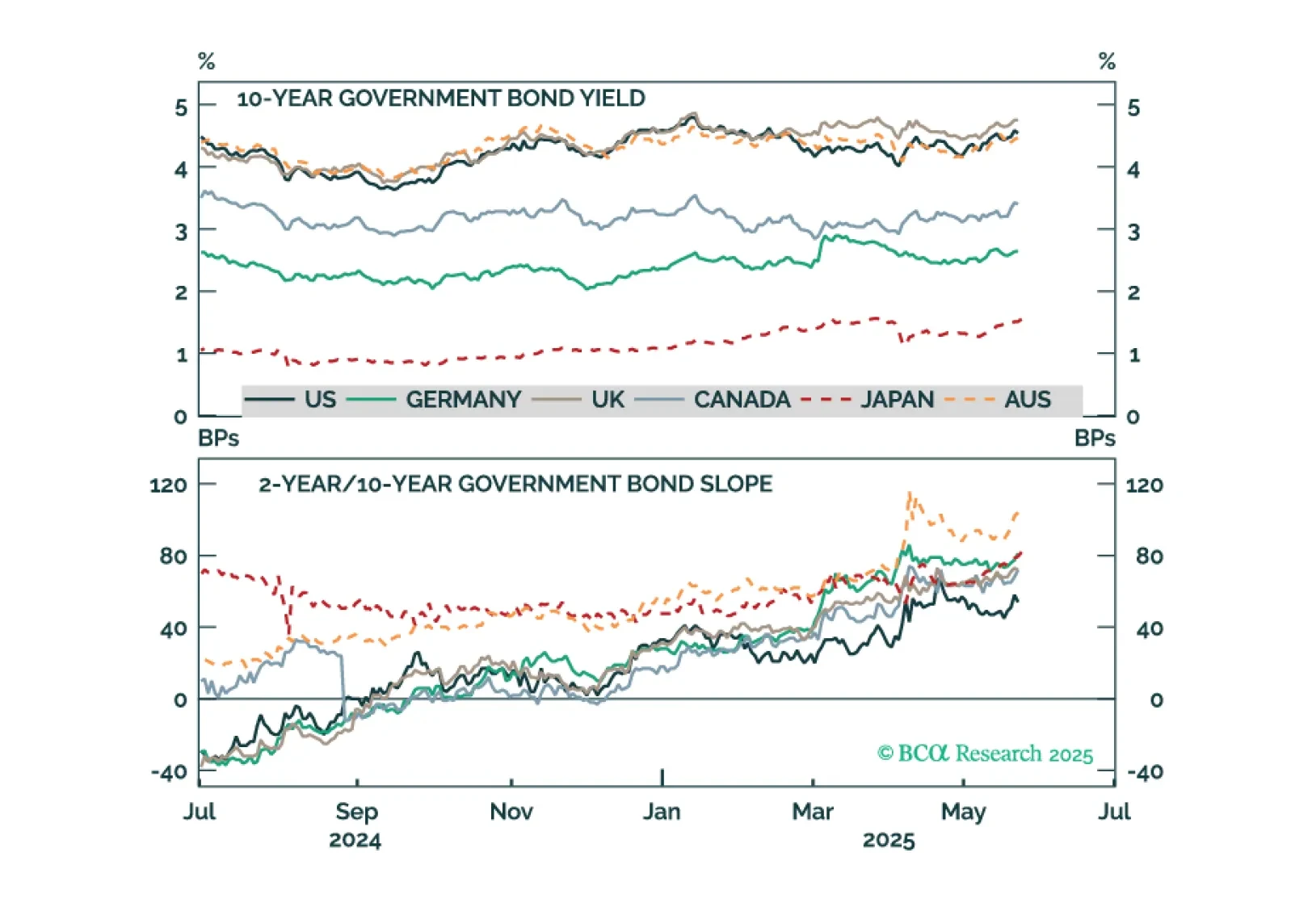

We perform a decomposition of yields moves across six major developed government bond markets to get to the bottom of what’s been driving the global bond selloff of the past eight months.

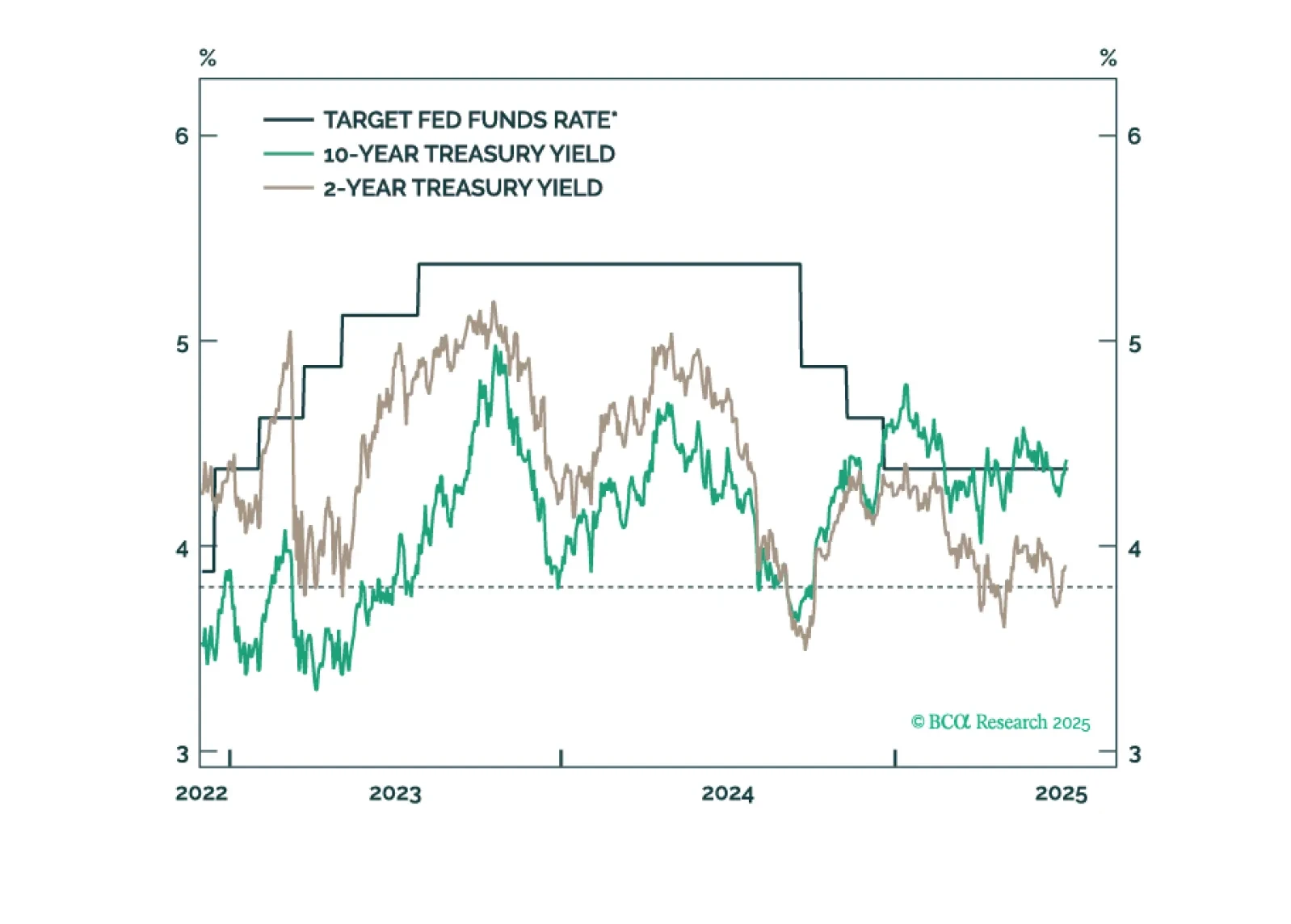

A weakening economy will apply downward pressure to Treasury yields, but the Trump term premium will keep long-dated yields higher than they would otherwise be. This makes Treasury curve steepeners the most attractive trade in US fixed income.