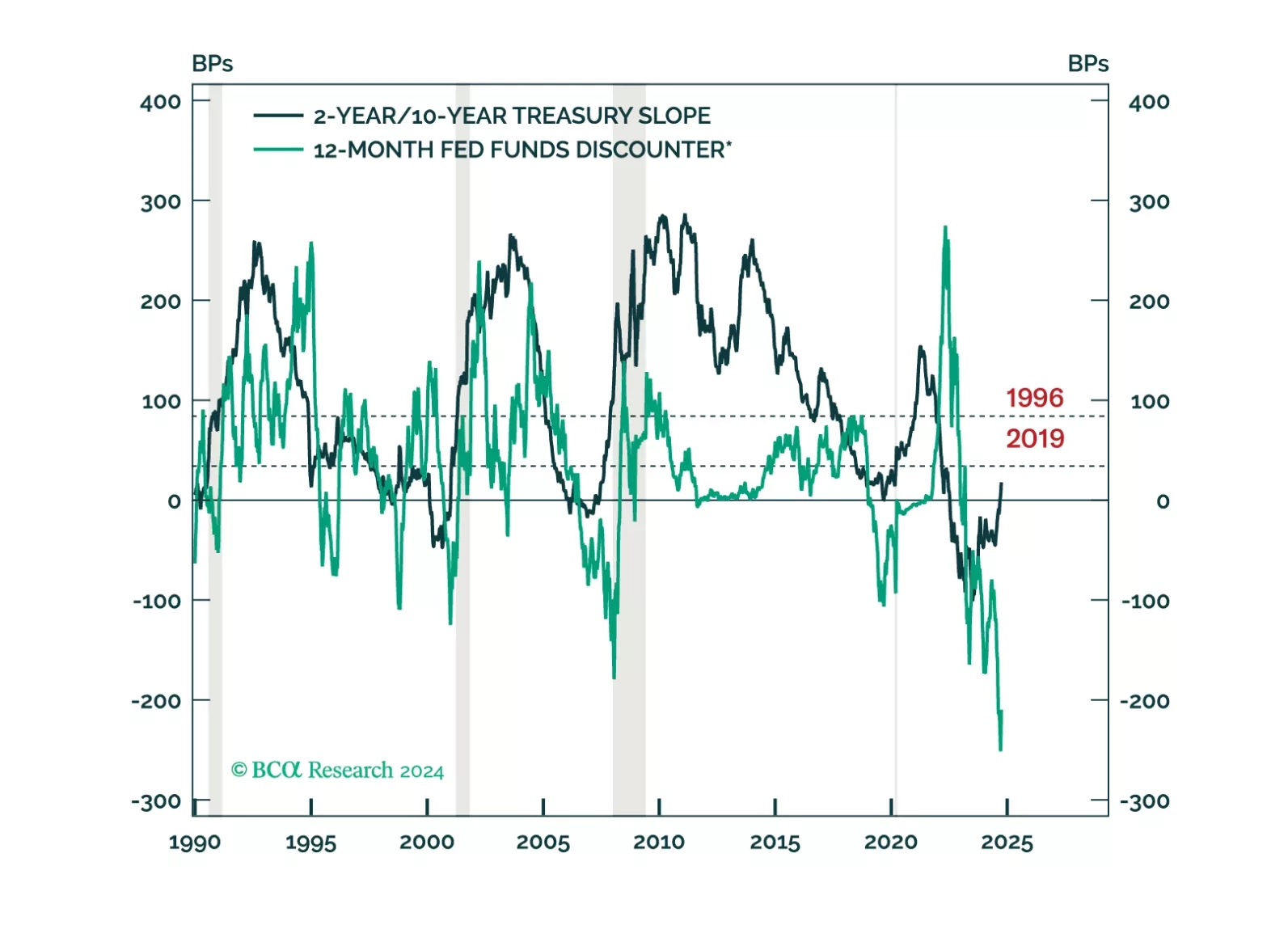

Yield Curve

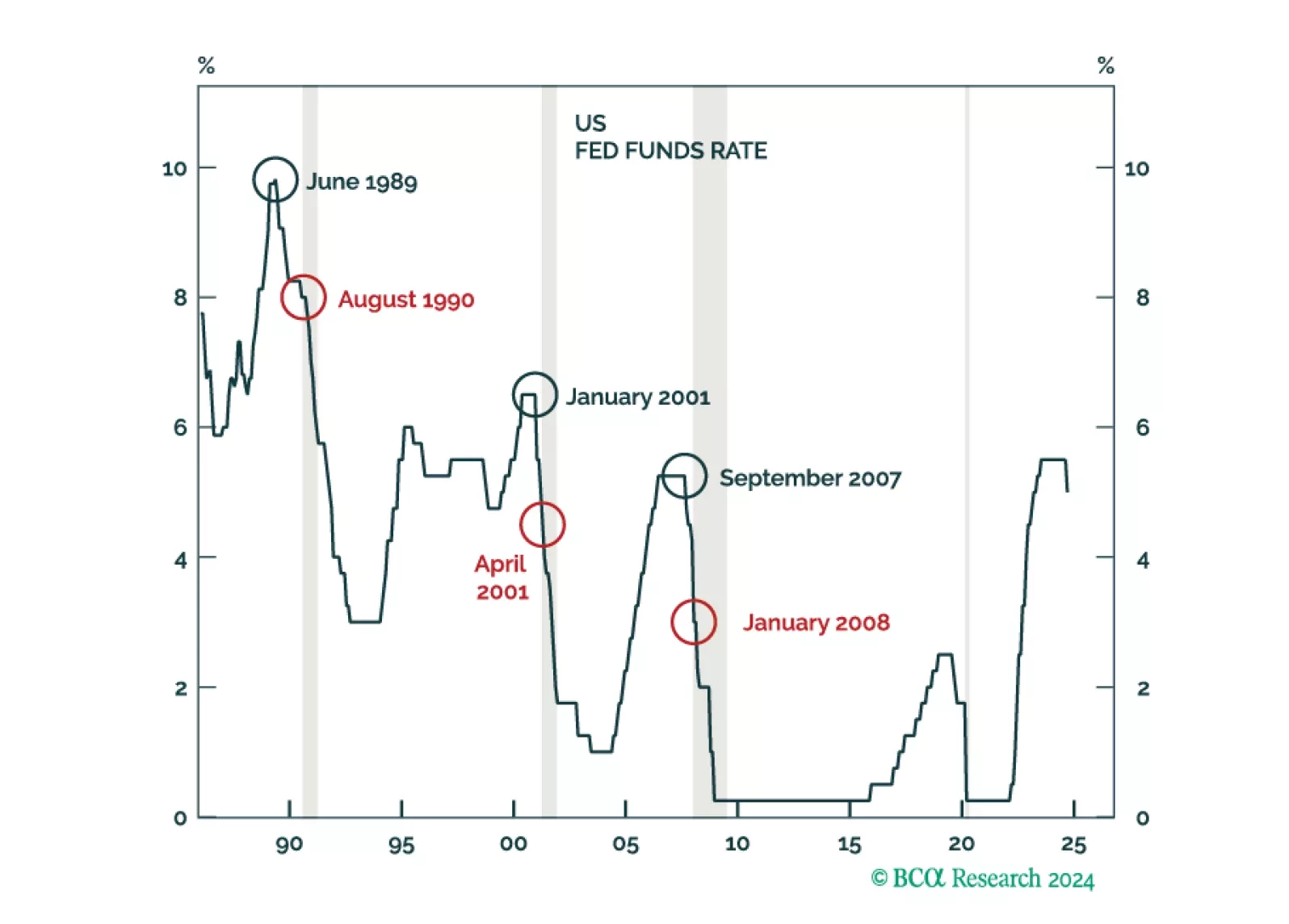

The prospect of a new trade war more than offsets the other pro-business parts of Trump’s agenda. With the labor market already weakening going into the election, we are raising our 12-month US recession probability from 65% to 75%.

Our thoughts on the bond market’s reaction to the election and this afternoon’s FOMC meeting.

A Donald Trump victory would send bond yields higher during the next few weeks, but yields will fall in 2025 no matter the election outcome.

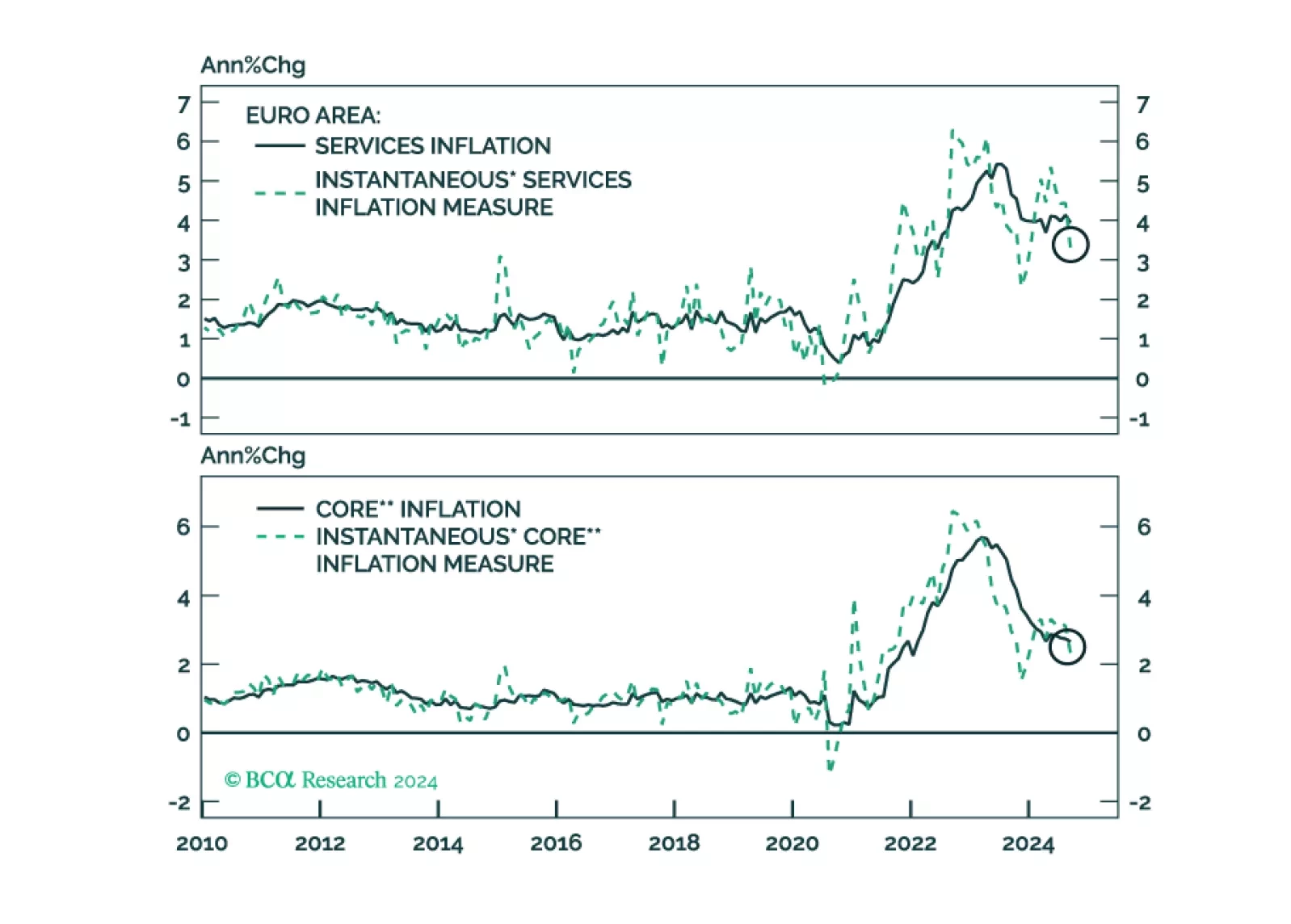

Yesterday, the ECB solidified its recent dovish tilt in response to weaker growth and decreasing inflationary pressures. It is now set to cut rates 25bps each meeting. How low will the ECB deposit rate ultimately go and what does this imply for yields and the euro?

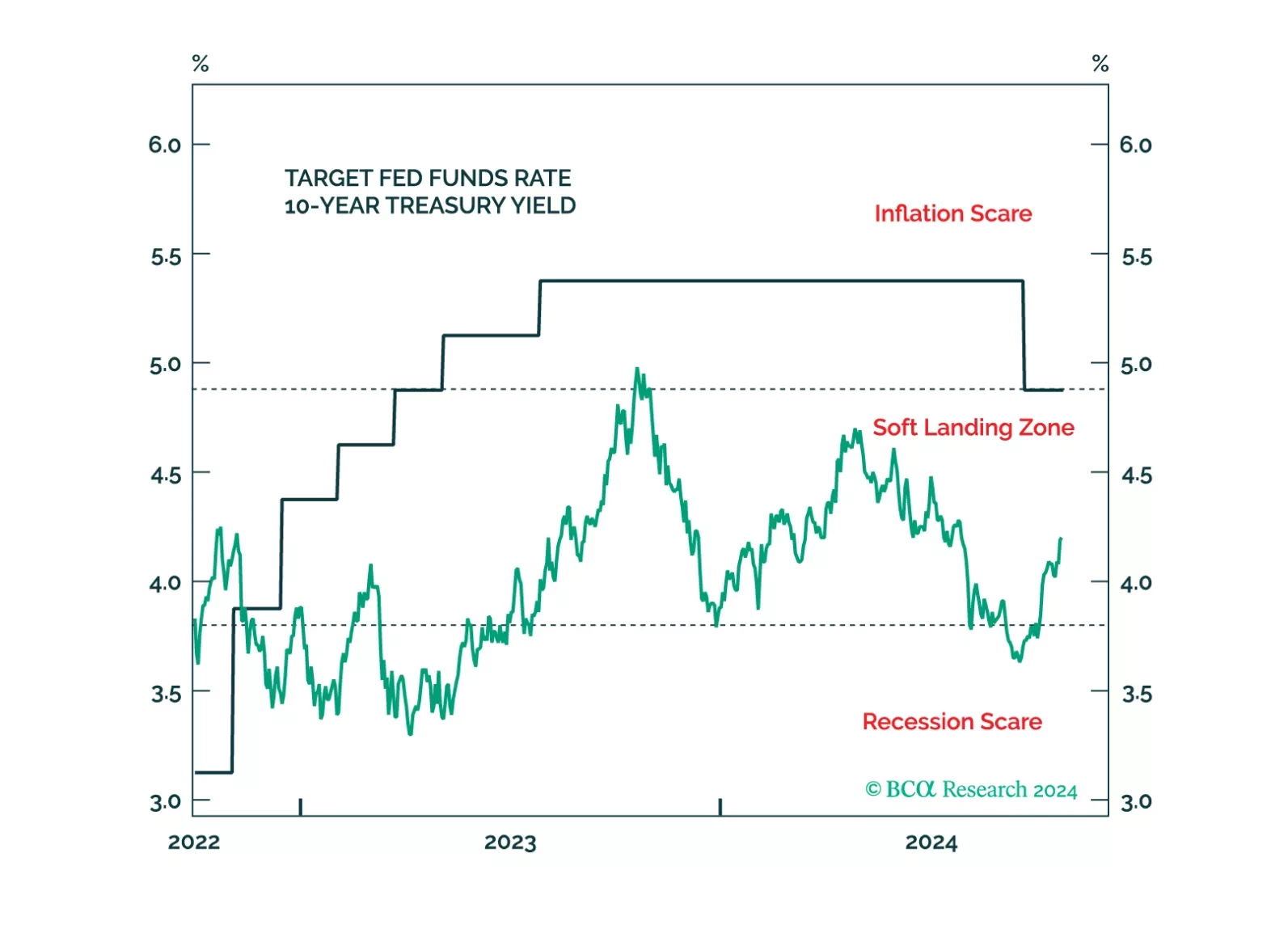

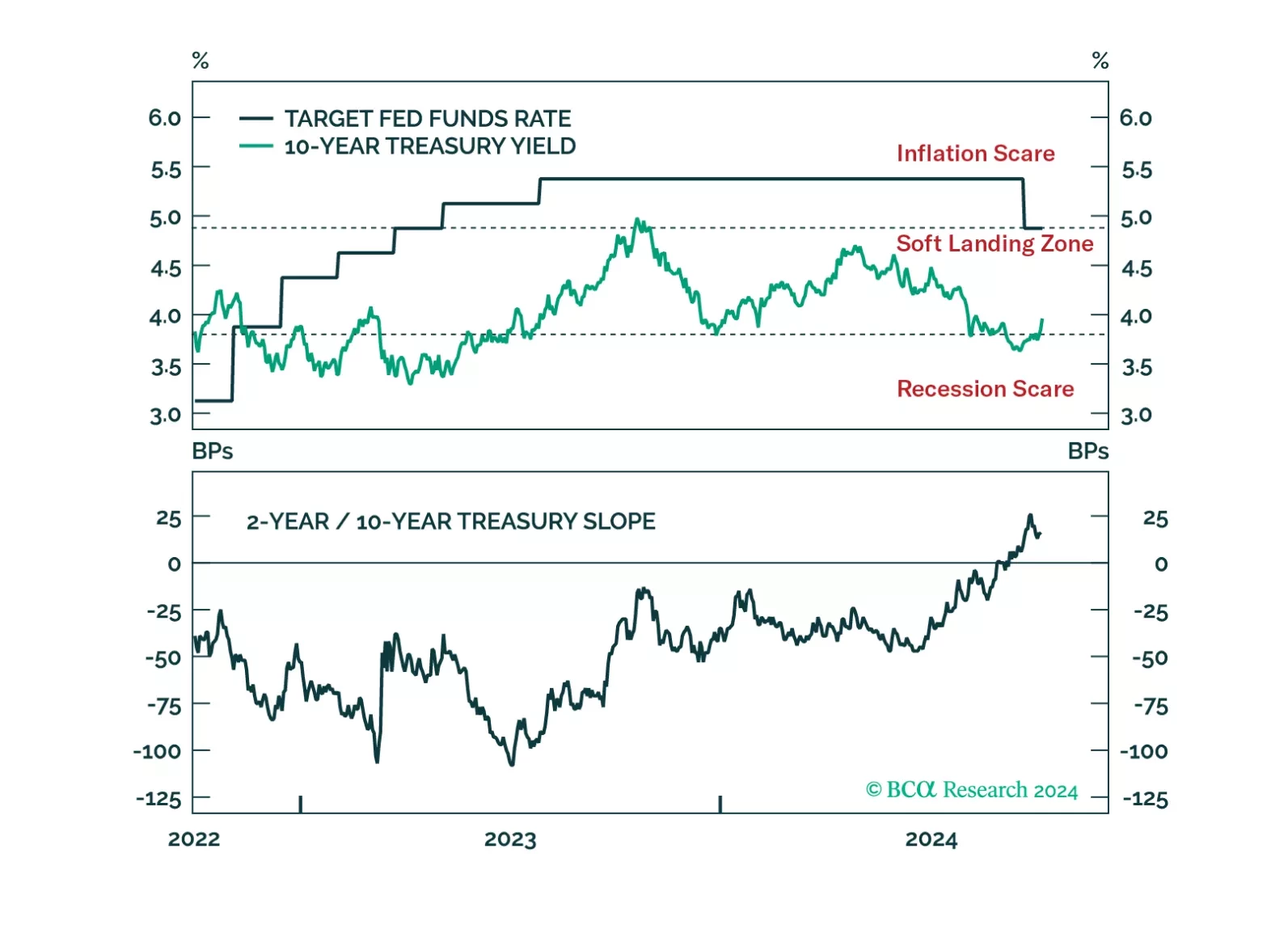

The bond market priced out a lot of recession risk after this morning’s employment report, and the 10-year Treasury yield has moved back into the Soft Landing Zone. We assess the data and consider whether we need to change our cyclical positioning.

Our Portfolio Allocation Summary for October 2024.

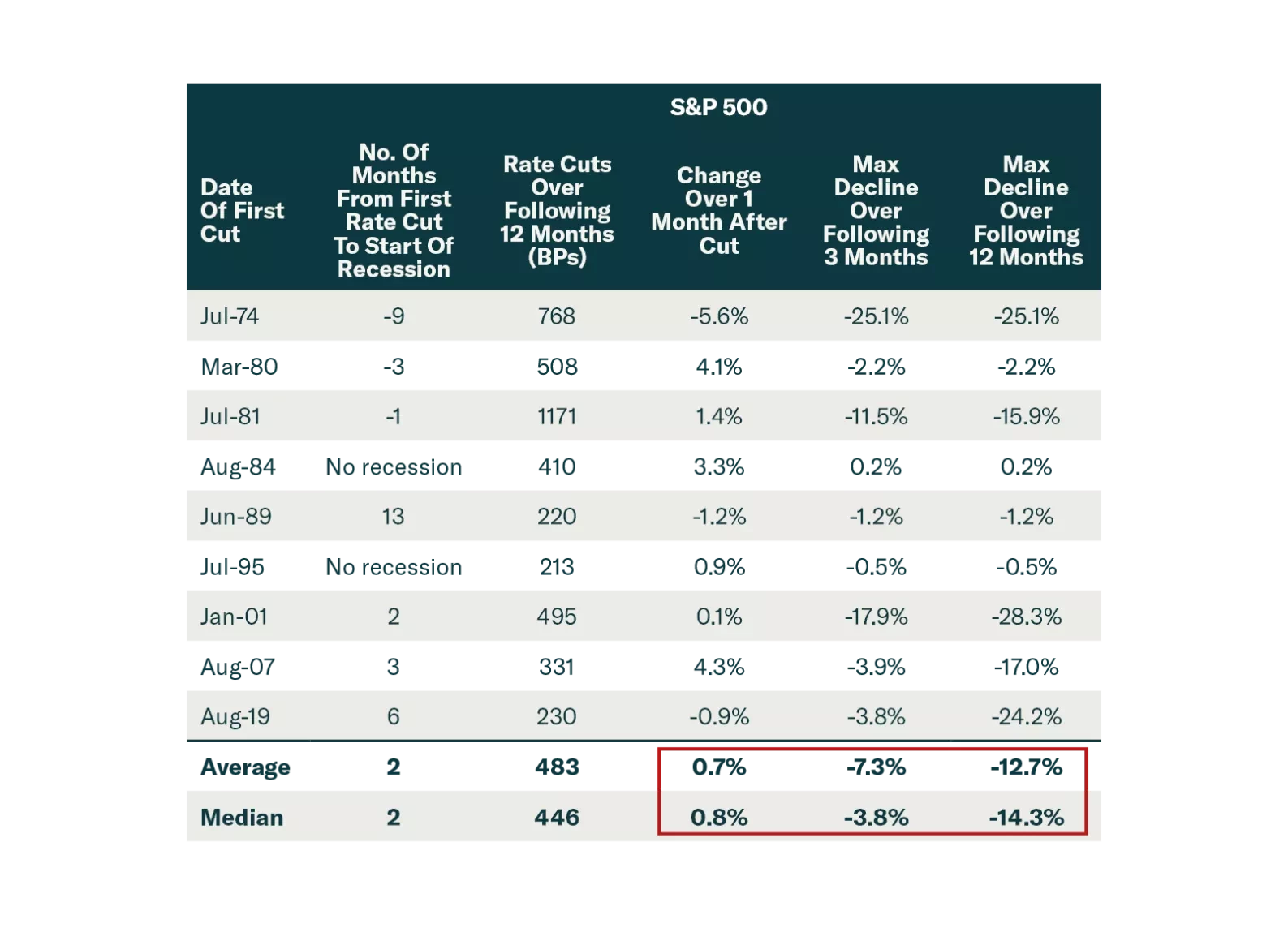

The market got excited by the 50 bps Fed cut and China stimulus. But these are a recognition that economies are slowing significantly. Stocks often rally after the first Fed cut, before falling sharply. Investors should stay defensive.

After resisting the consensus narrative in 2022 that a US recession was imminent, and then predicting an immaculate disinflation for 2023, the Global Investment Strategy team has joined the dark side and is now expecting a recession to start in the US within the next six months. Accordingly, we recommend that investors underweight stocks and overweight government bonds.