Yield Curve

Our Portfolio Allocation Summary for May 2024.

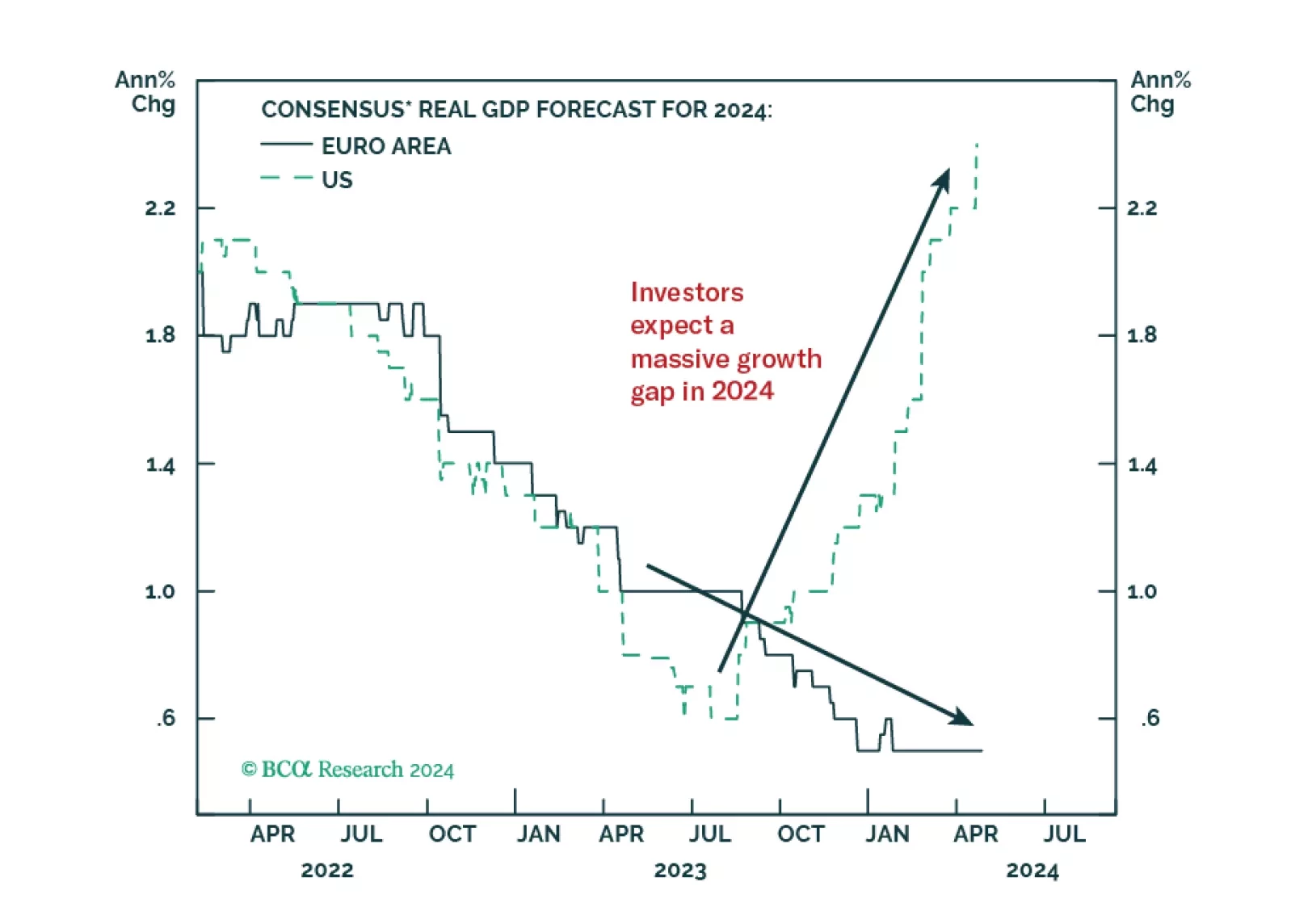

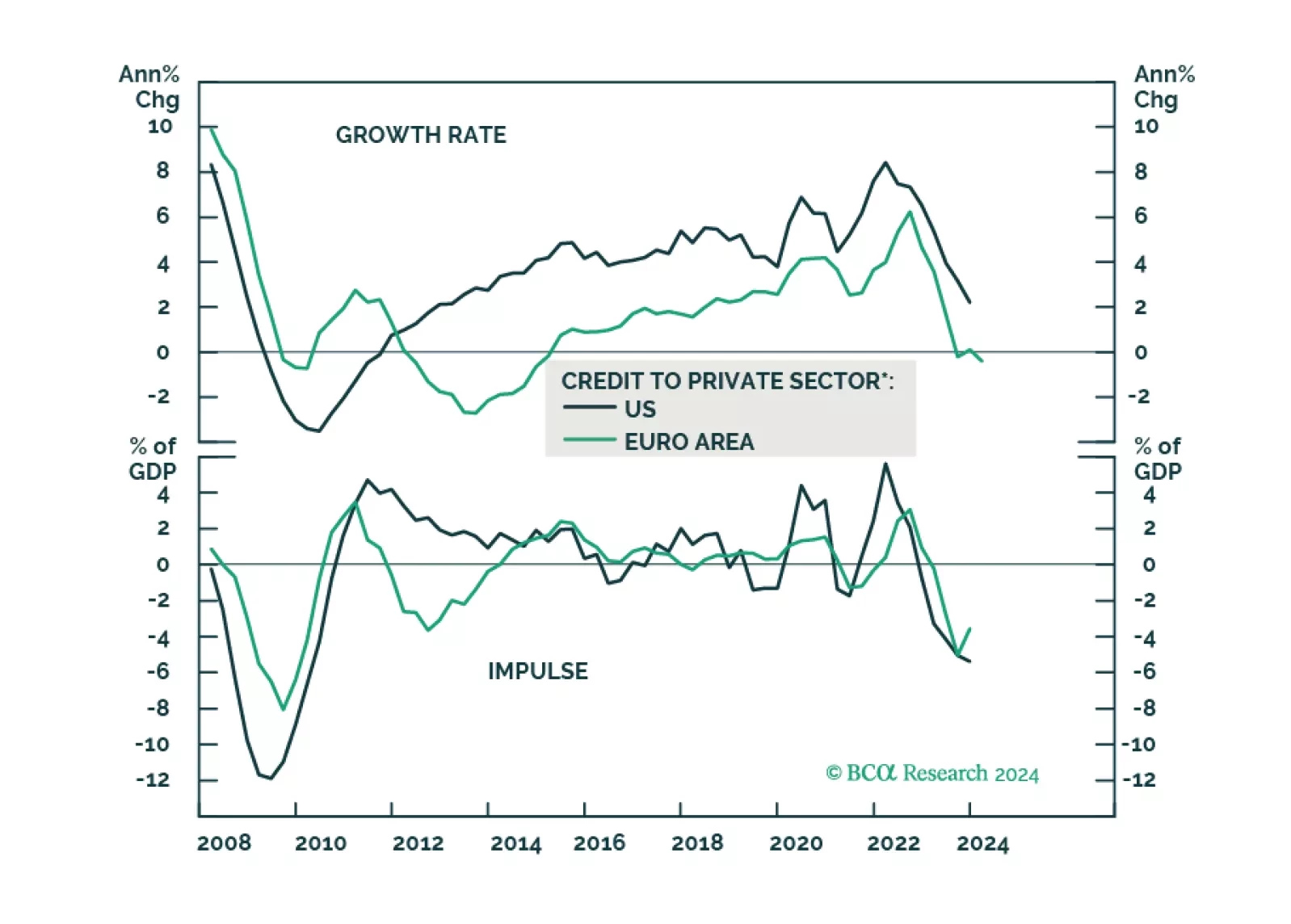

Investors anticipate a record growth gap between the US and the Eurozone in 2024. Does this skewed expectation create market opportunities?

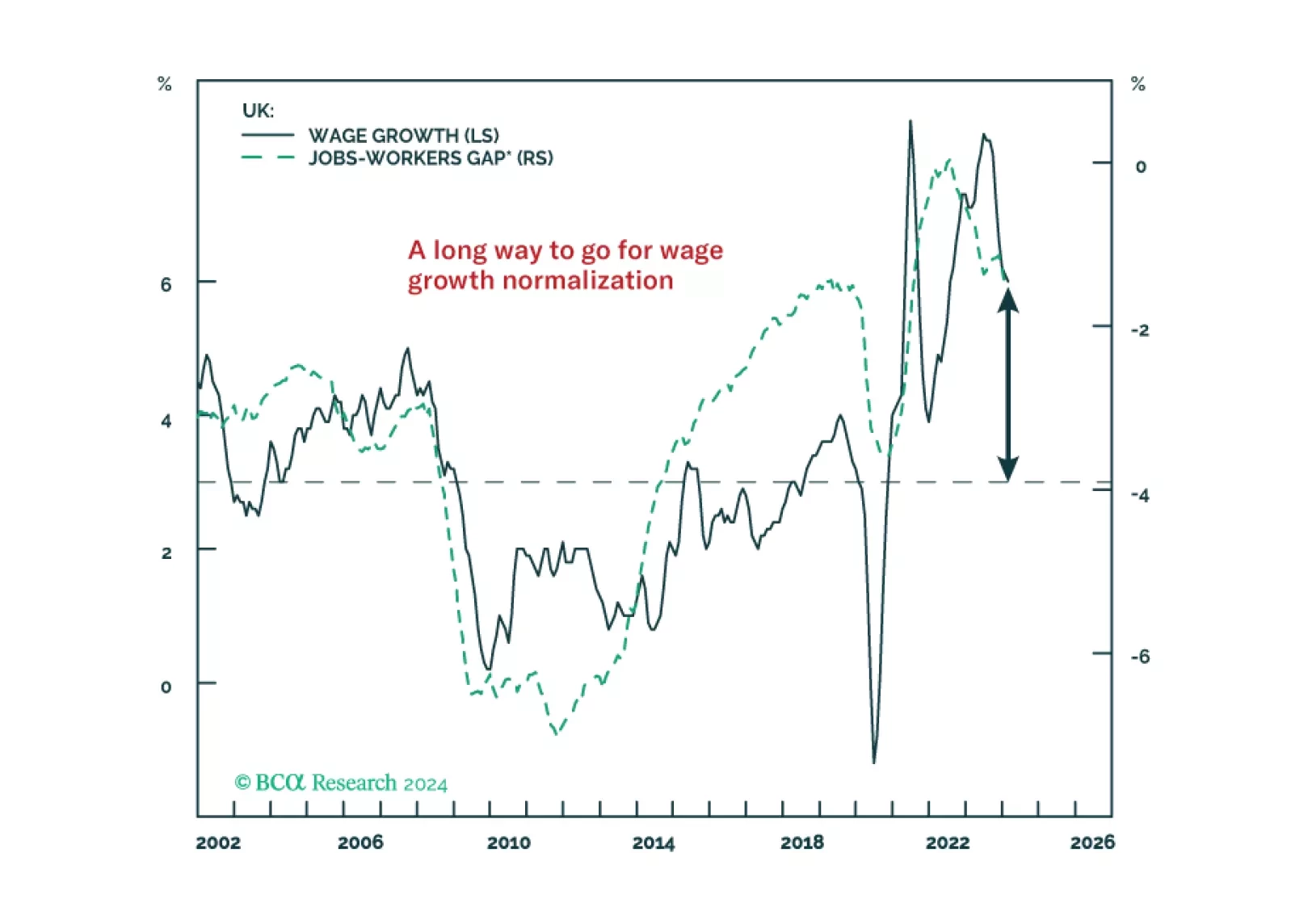

The UK labor market remains far too tight to expect wage growth to slow to levels consistent with the Bank of England inflation target. A true recession with rising unemployment is needed to finally slay the UK inflation beast. 2024 rate cuts are off the table, with the central bank having to keep monetary policy tighter for longer than markets expect and the UK economy now rebounding. We recommend downgrading UK gilts to underweight in global bond portfolios, while also looking for opportunities to buy the British pound on pullbacks versus the euro, Canadian dollar and Swedish krona.

This Special Report introduces a framework for assessing the relative importance of slope change and initial yield in curve trade performance. The yield penalty for curve steepeners has fallen significantly since the beginning of the year, and we recommend shifting out of Treasury curve flatteners and into Treasury curve steepeners in US bond portfolios.

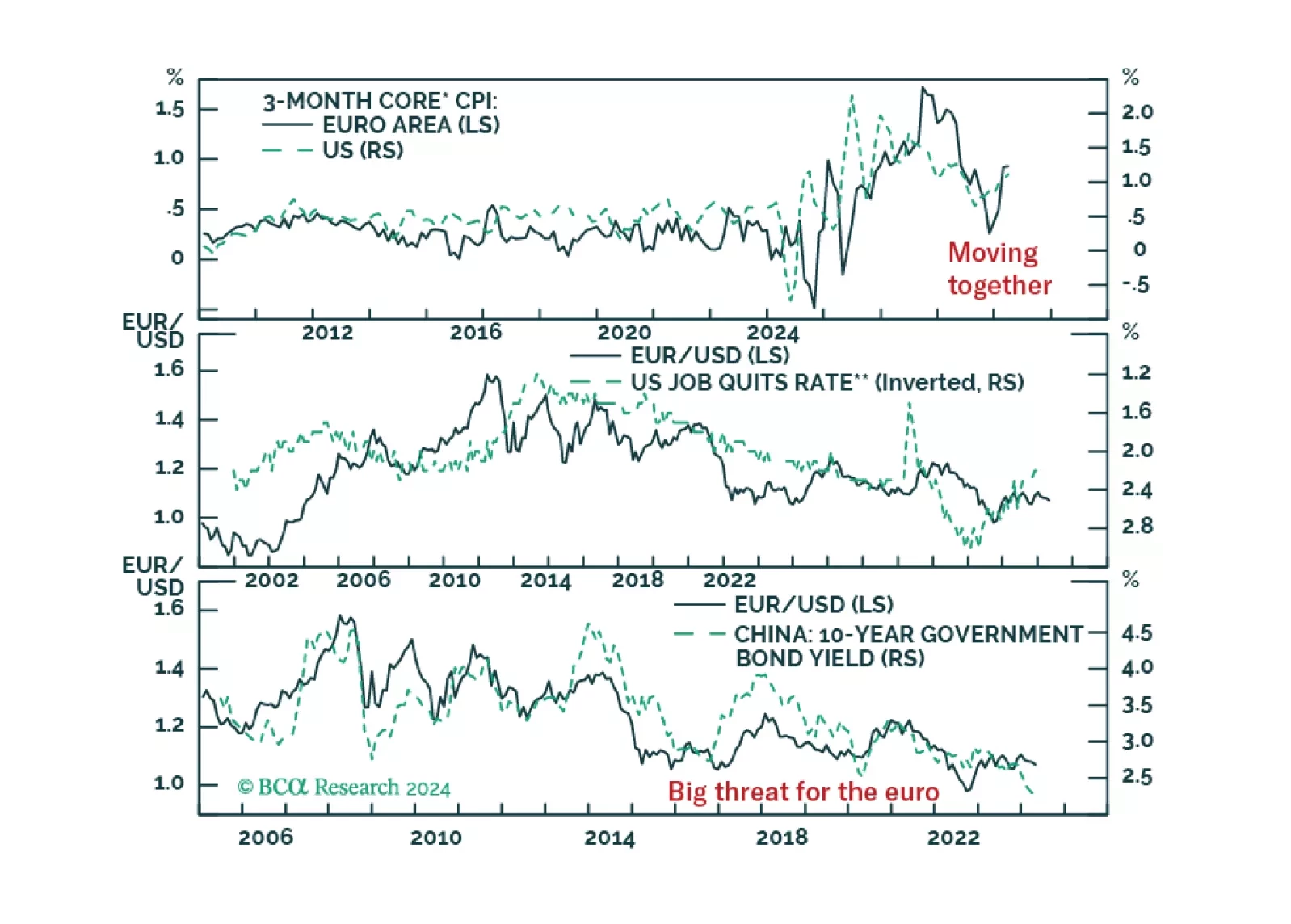

EUR/USD collapsed in the wake of last week’s hotter-than-expected US CPI report. Is this pessimism warranted and will the euro’s trading range that has prevailed since 2023 breakdown?

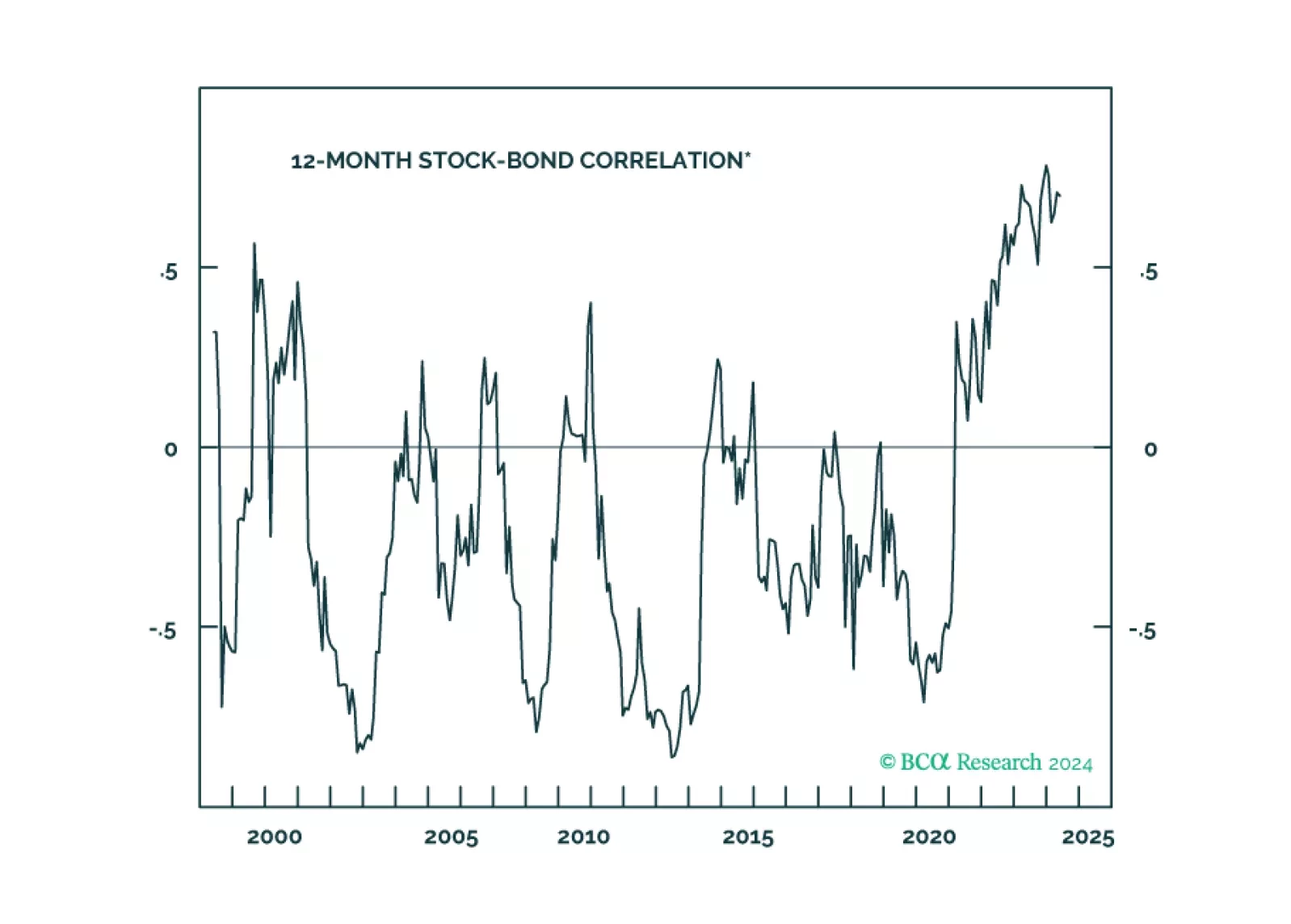

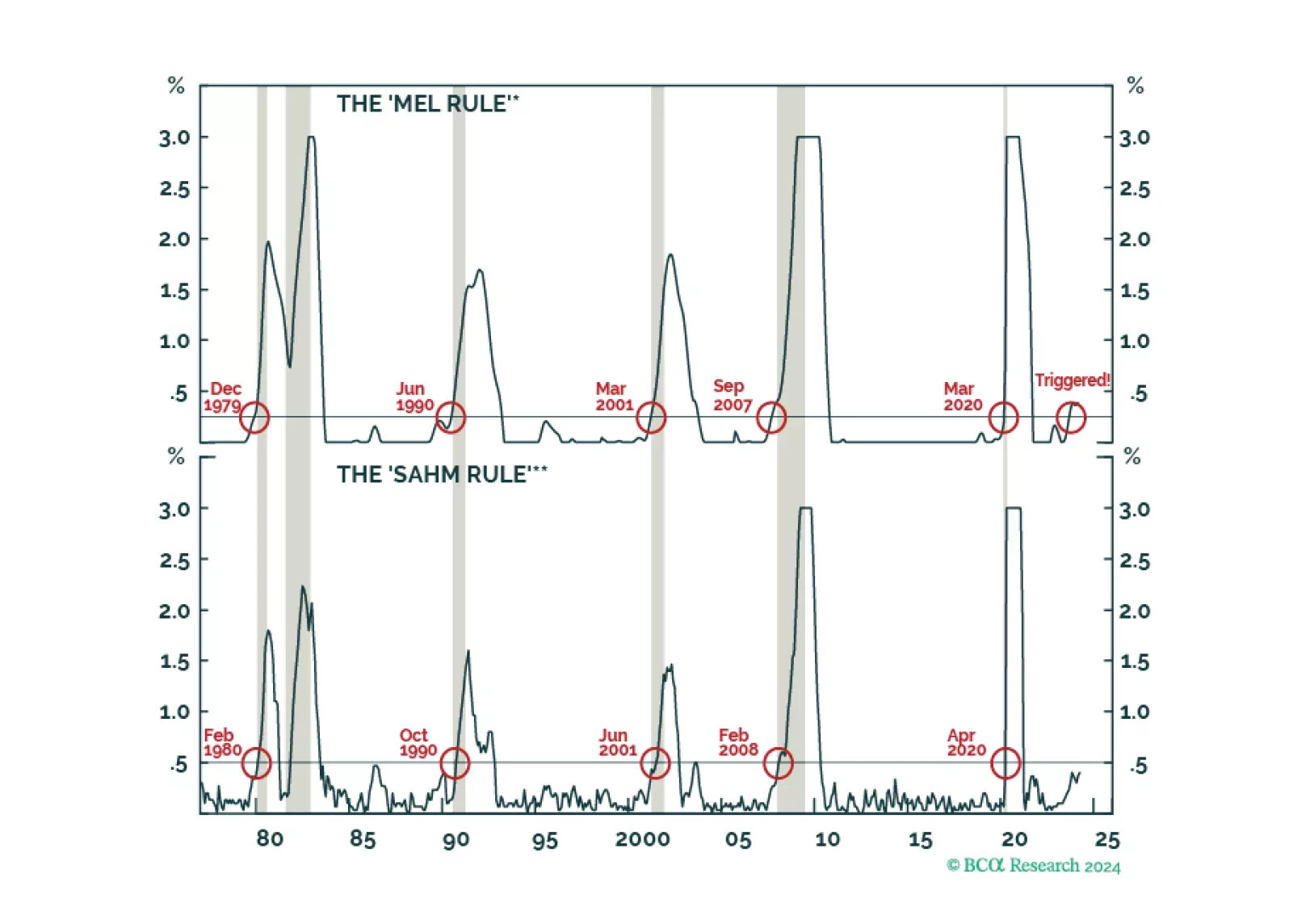

Contrary to conventional wisdom, most leading indicators suggest that the US labor market is weakening, including our very own “Mel rule.” After being overweight stocks last year, we moved to neutral at the start of 2024, and are now putting equities on downgrade watch with the expectation of shifting them to underweight later this year.

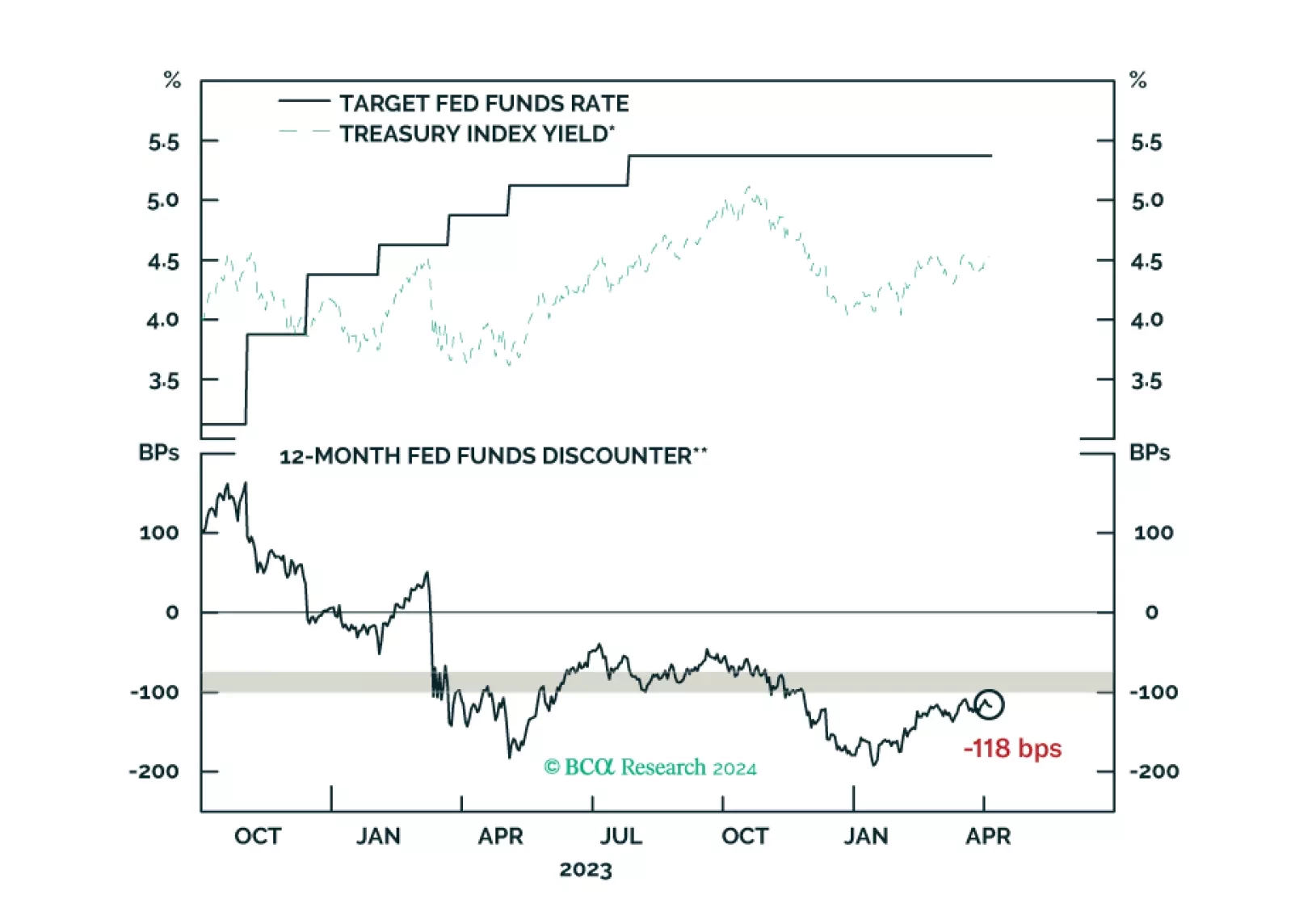

Our reaction to this morning’s employment report and bond market moves.

Our Portfolio Allocation Summary for April 2024.

The global economy is wobbling precariously between slowing growth and reaccelerating inflation. This is unlikely to end well. Stay cautious, and hedge against both recession and inflation.

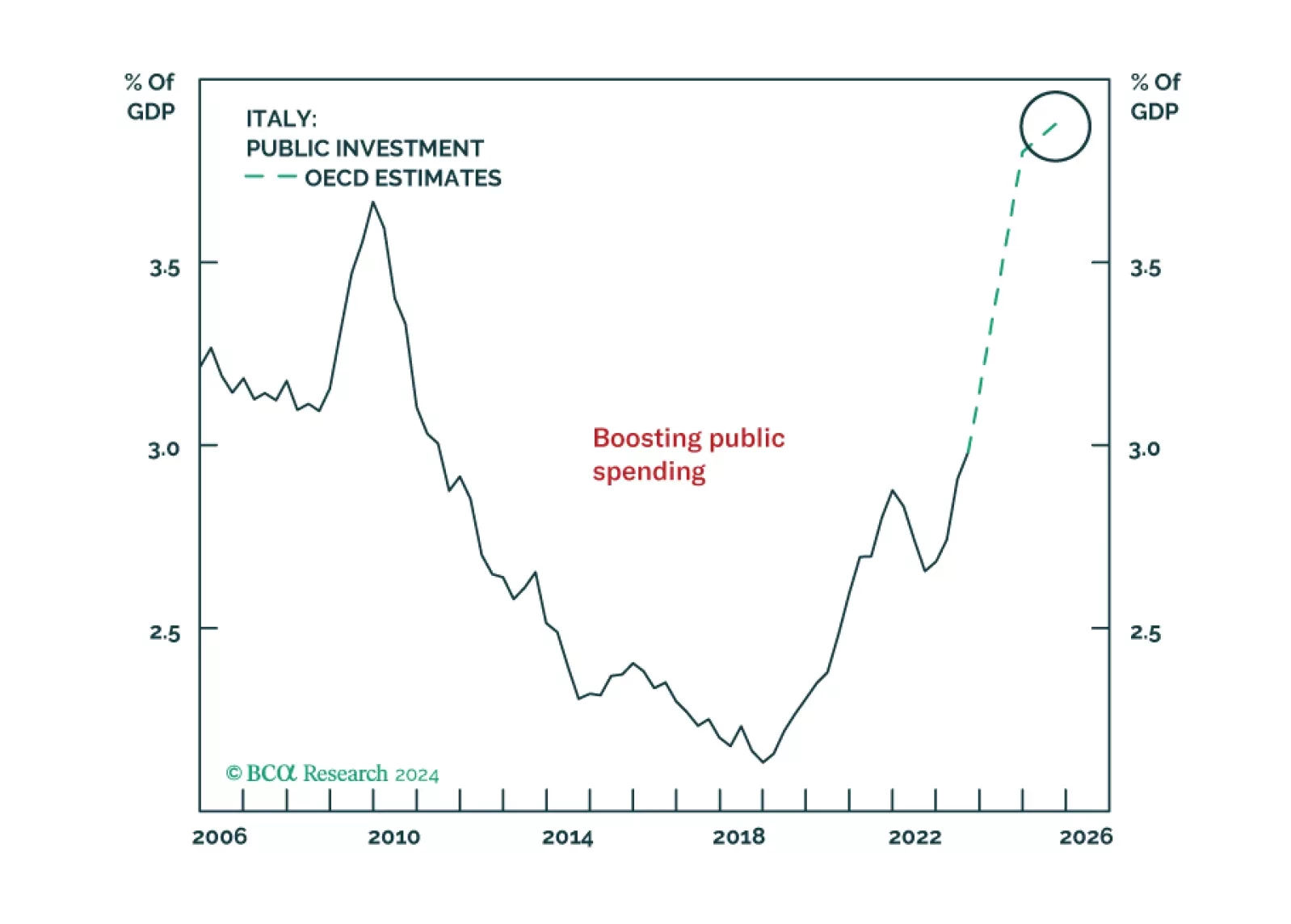

Italy is no longer Europe’s problem child. Investors will be better off reassessing their views of Italian assets, which represent a buying opportunity on a structural time horizon.