Domestic Politics

Do not play the bounce in US and global cyclical assets as Trump backpedals from the trade war. China will talk, but the pace will be slow and the outcome disappointing. Fiscal stimulus will surprise marginally in the EU, China, and even the US, but still may not rescue the business cycle.

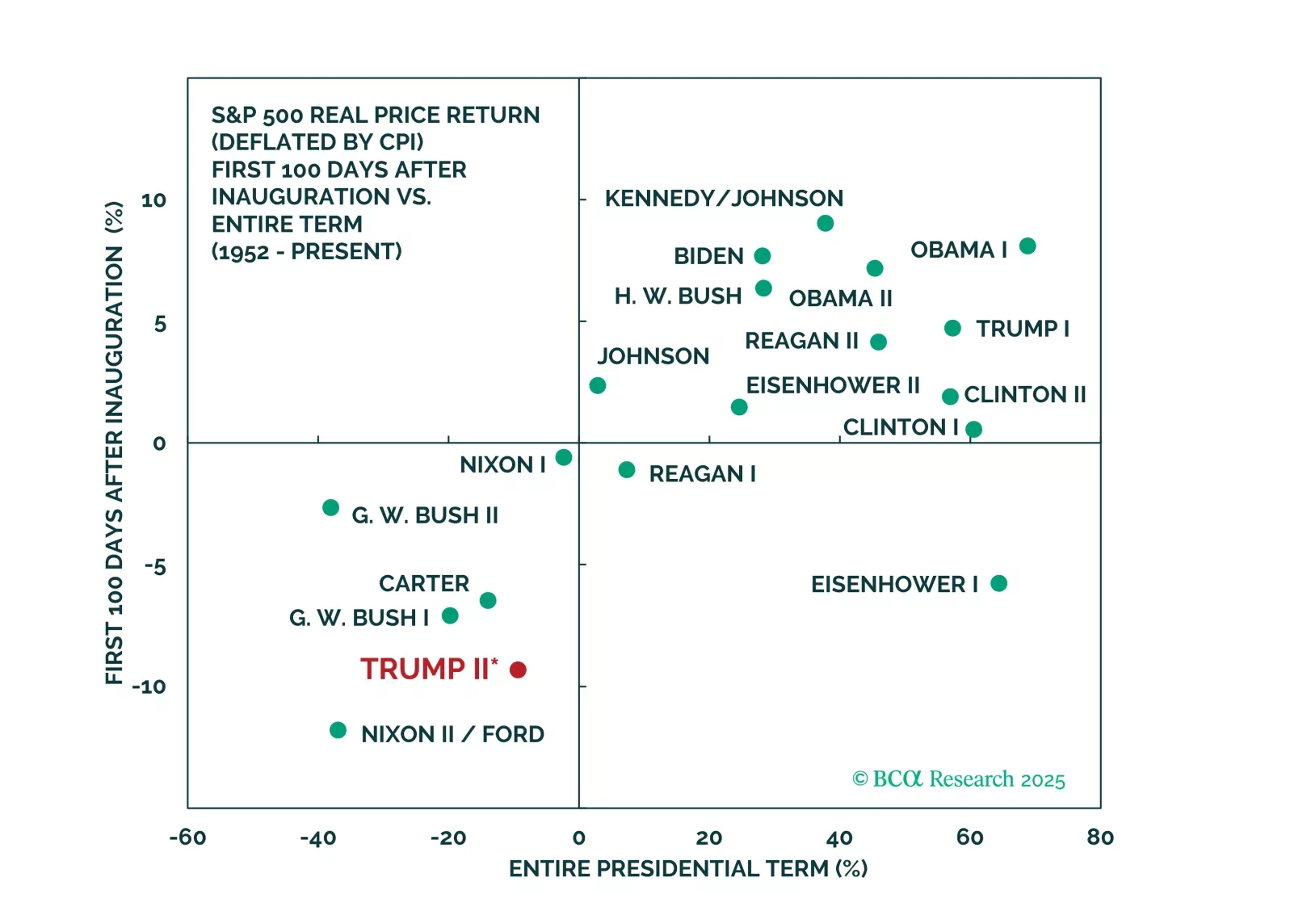

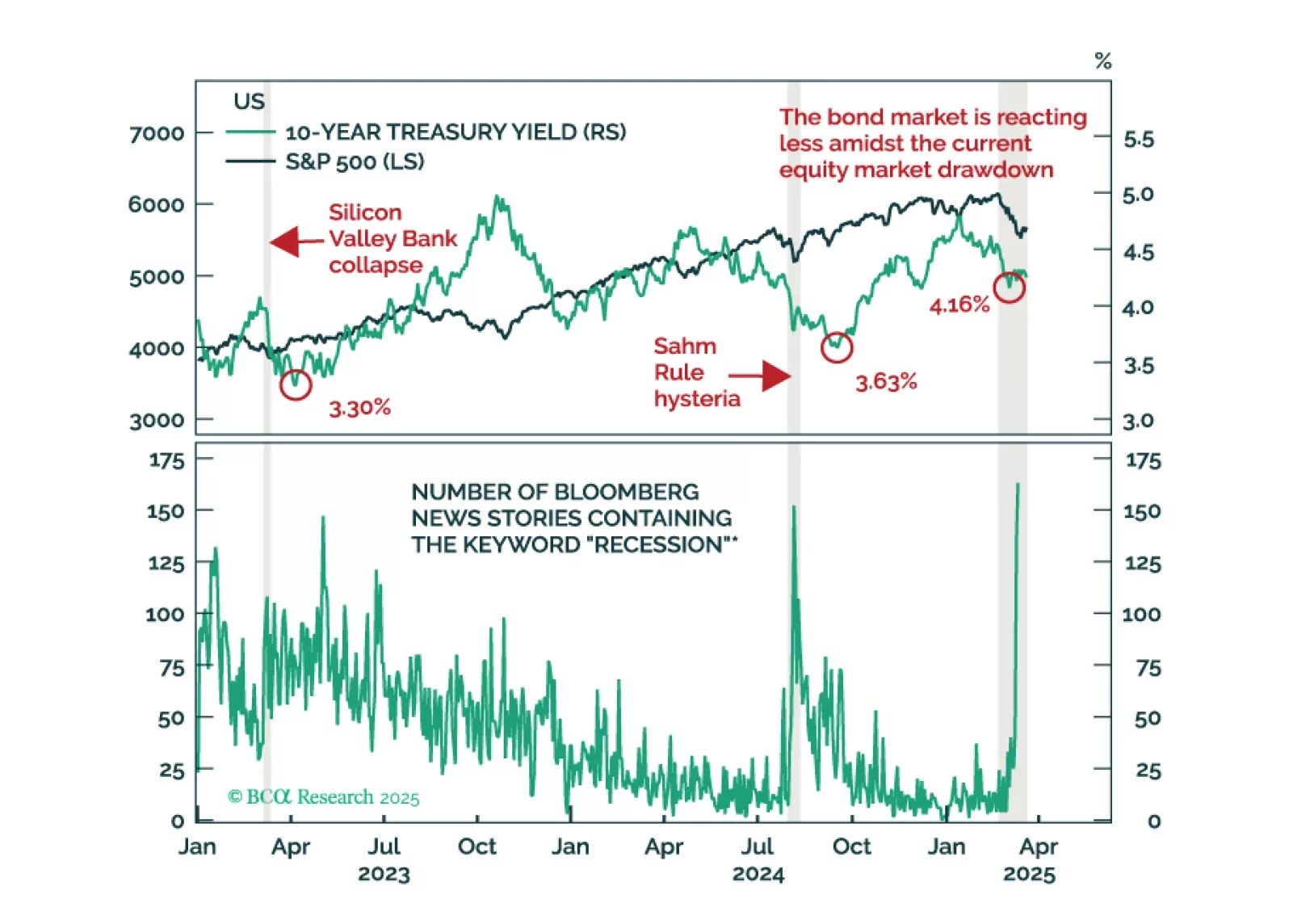

Trump's Tariff D-Day brings a negative surprise to financial markets already anxious over a declining US cyclical economy. Investors should sell risky assets, increase safe havens, and overweight US assets in the near term.

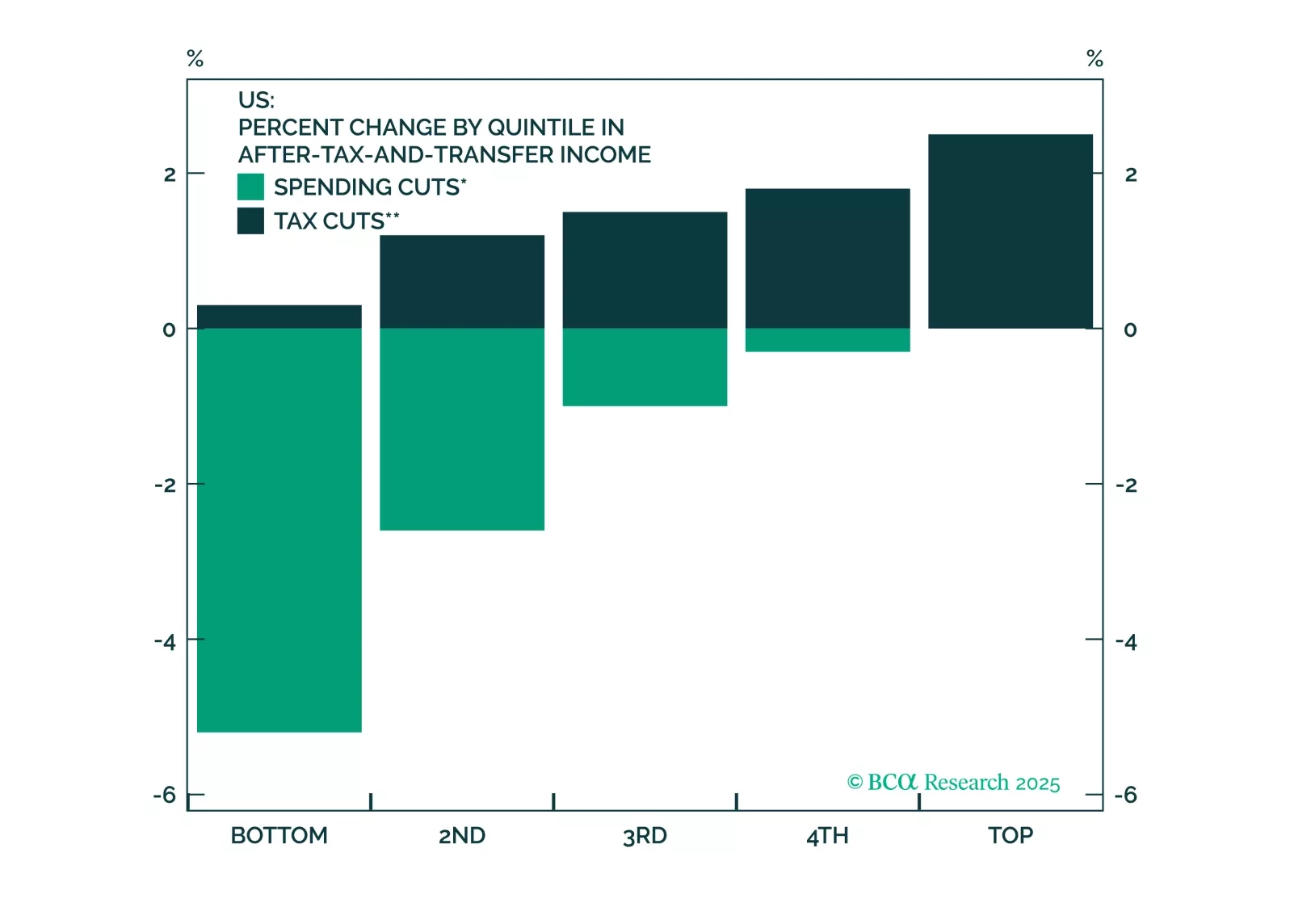

Stocks will continue to struggle in the second quarter as President Trump tries to implement tariffs. Tax cuts will only temporarily dispel growth fears, if at all. Middle Eastern instability will add oil price surprises to an environment that is looking fairly stagflationary.

In this Special Report, GeoMacro Strategist Marko Papic argues that the Trump administration is flirting with high risk / low reward. Triggering a recession may be the end goal of the White House, but borrowing costs are not declining as much as they ought to be while President Trump’s political capital is on thin ice. Most recessions are caused by a “murder weapon.” It is rare that this weapon can be holstered. This may be one of those times.

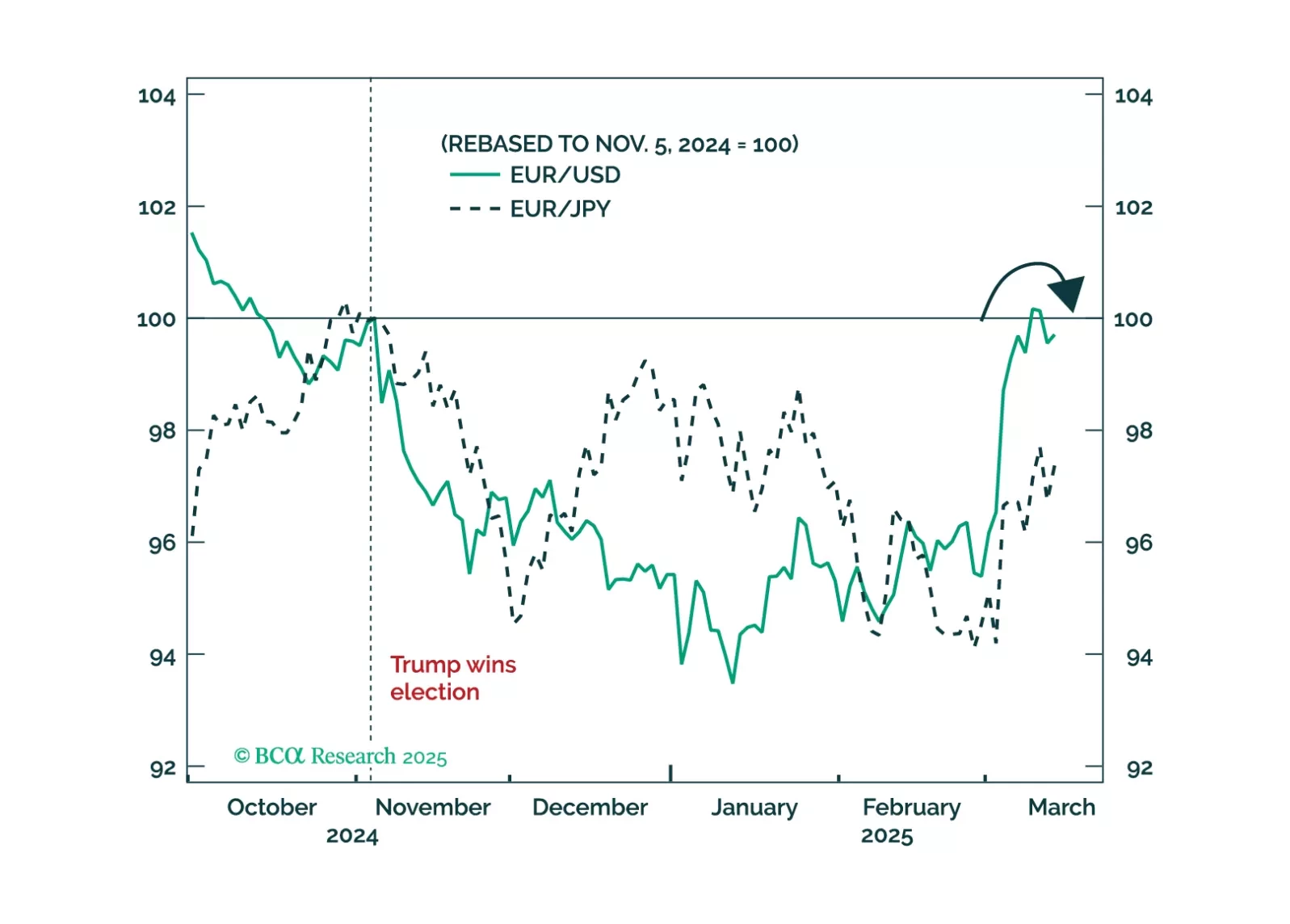

Trump’s foreign policy can be explained by rational US interests, but it requires settling the trade war with allies sooner rather than later. Book gains on EUR-USD for now.

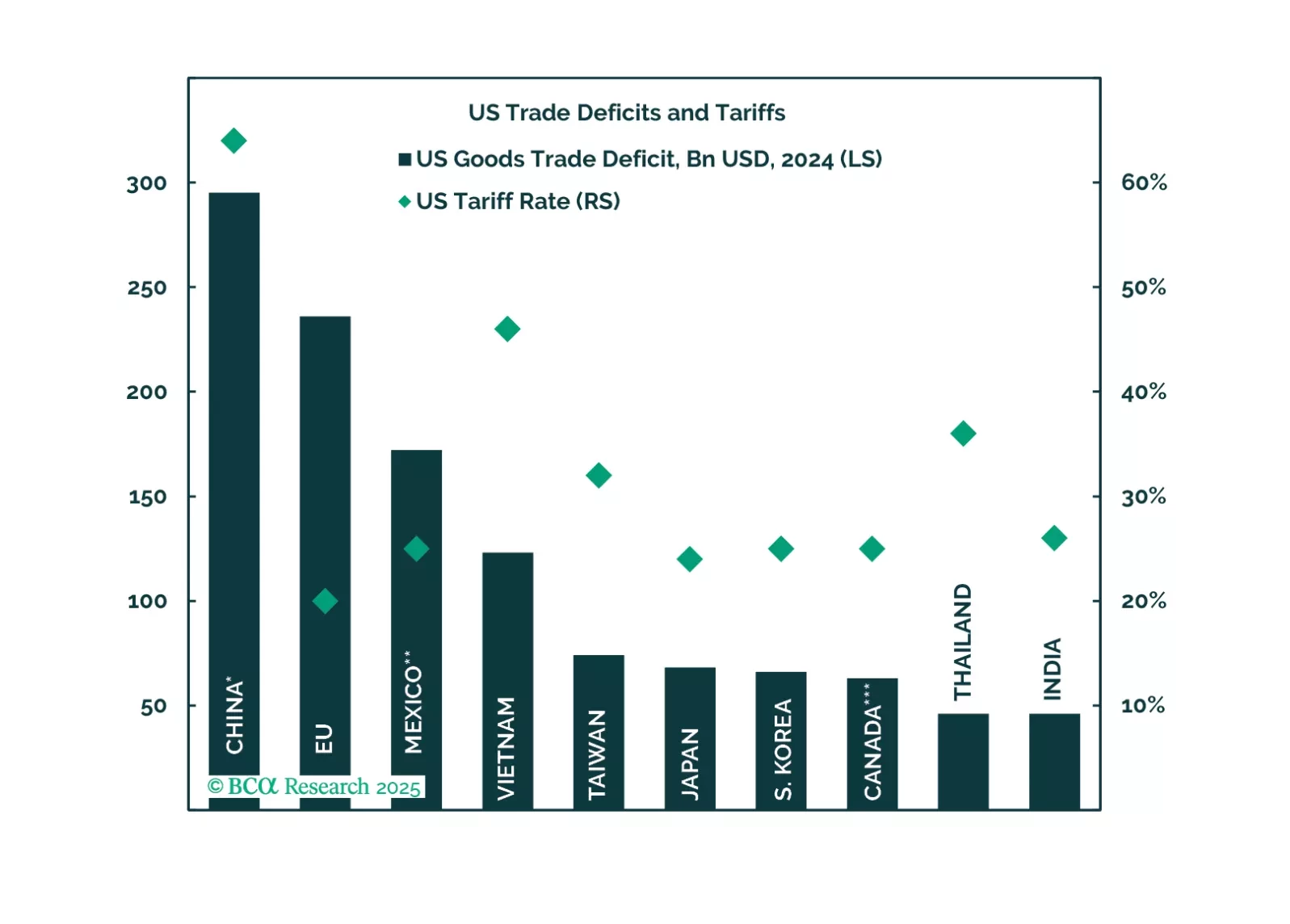

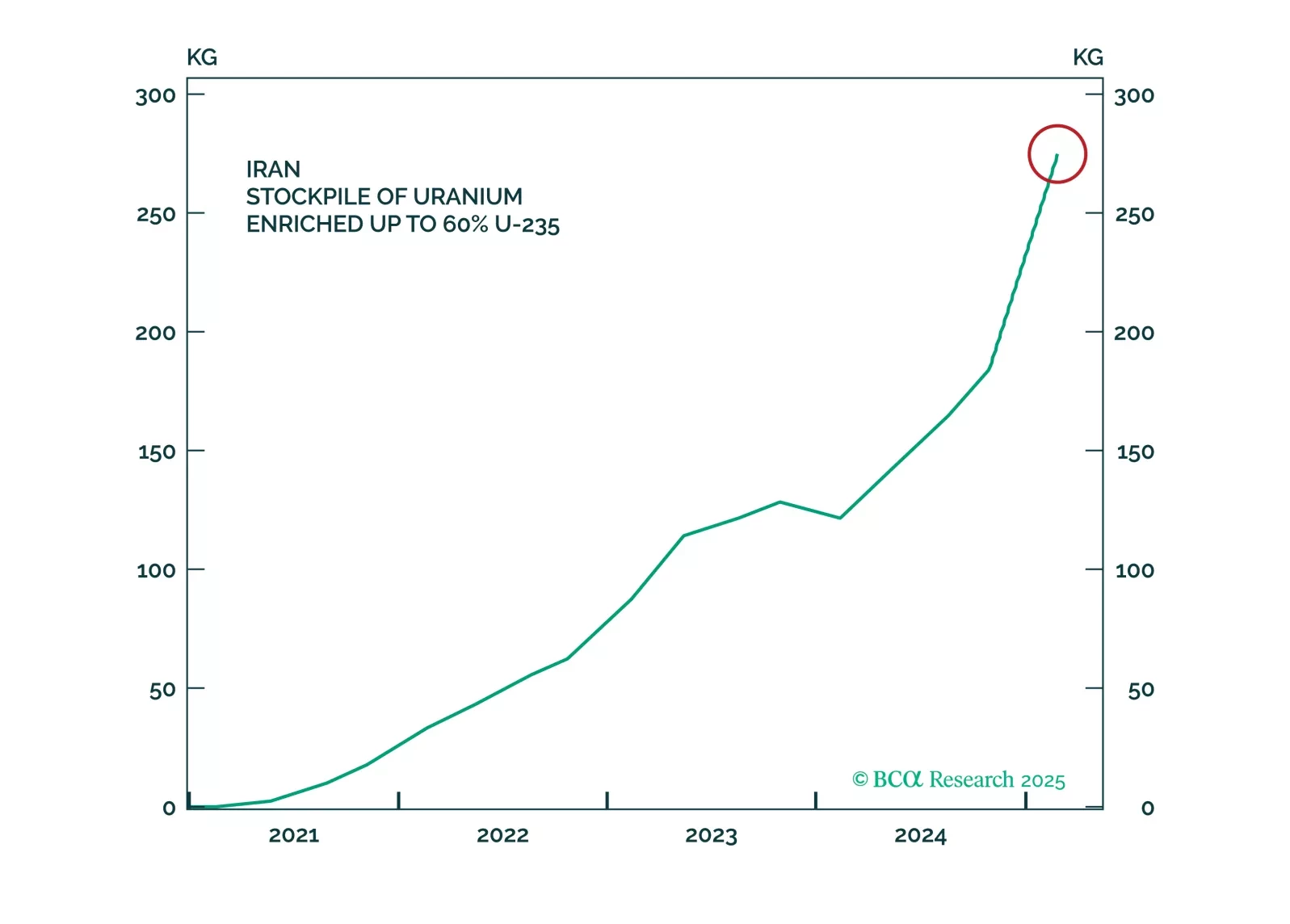

The tariffs on Canada and Mexico will come into effect as scheduled while the tariffs on China will be doubled. In the Middle East, Iranian response to any attack will threaten Middle Eastern oil supply. Meanwhile, Chinese fiscal support will surprise to the upside at the Two Sessions. But Trump's China policy will cause volatility. Now that the stock market is cracking, reinitiate defensive trades, such as long treasuries versus US stocks and long global defensives versus cyclicals.

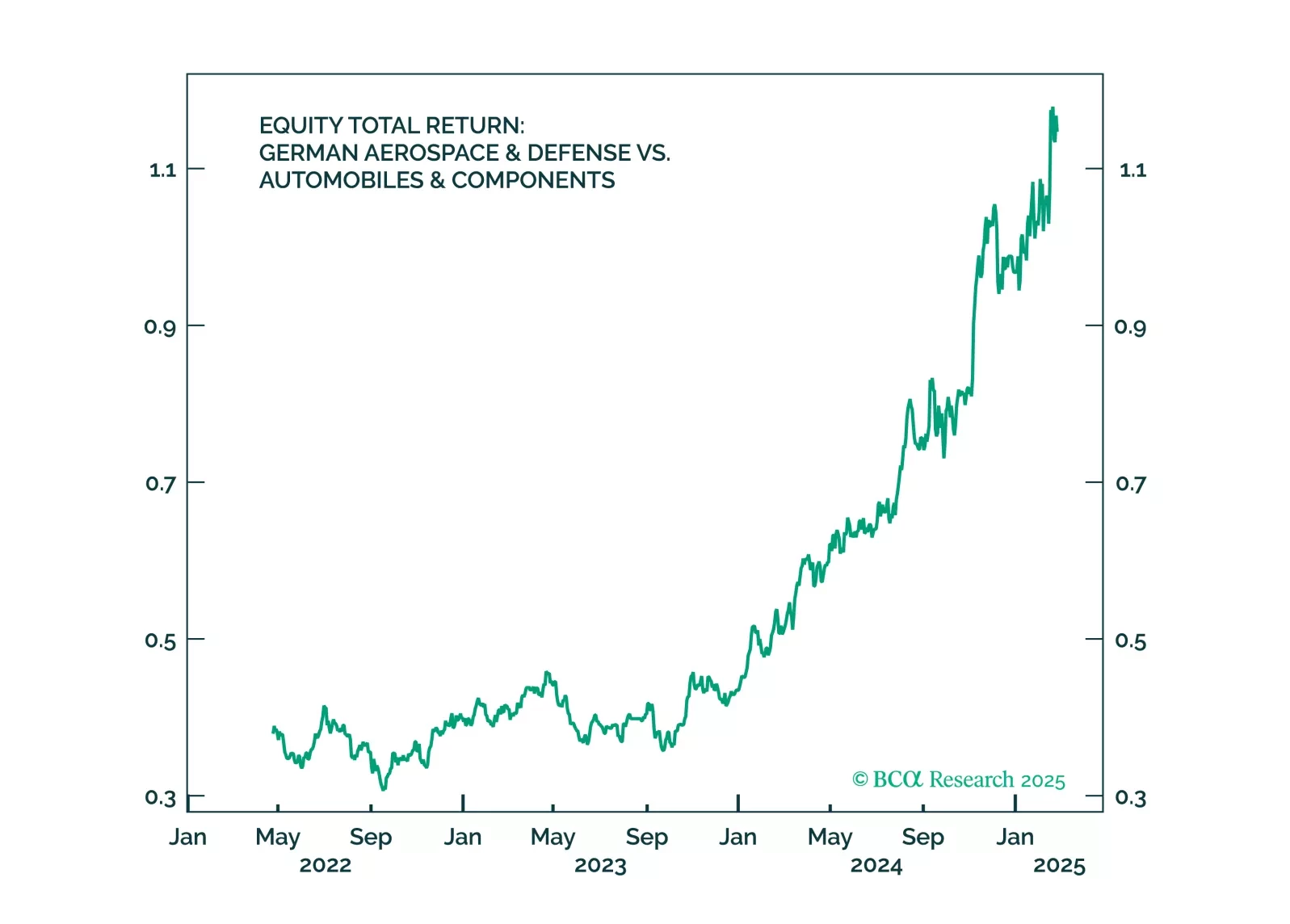

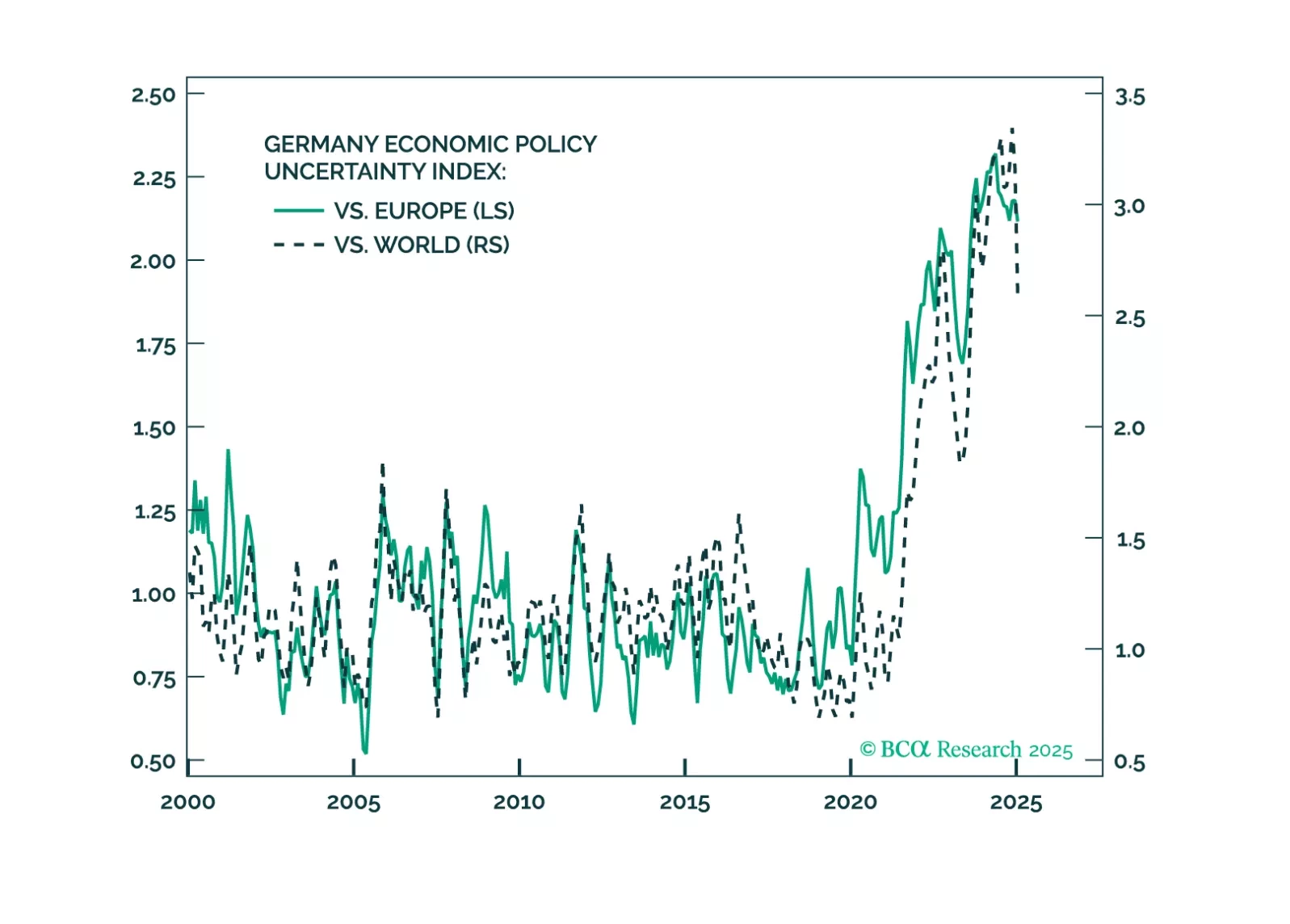

Trump’s ceasefire talks are positive for Germany – and so was the German election result. But Trump’s tariffs will hit Germany soon. Investors should use near-term volatility to increase exposure to Germany.

The rise of the far-right is challenging mainstream German politics. The CDU/CSU and SPD will govern Germany again after the election. A ceasefire in Ukraine will offer some relief, but Trump’s policies will keep tensions high.

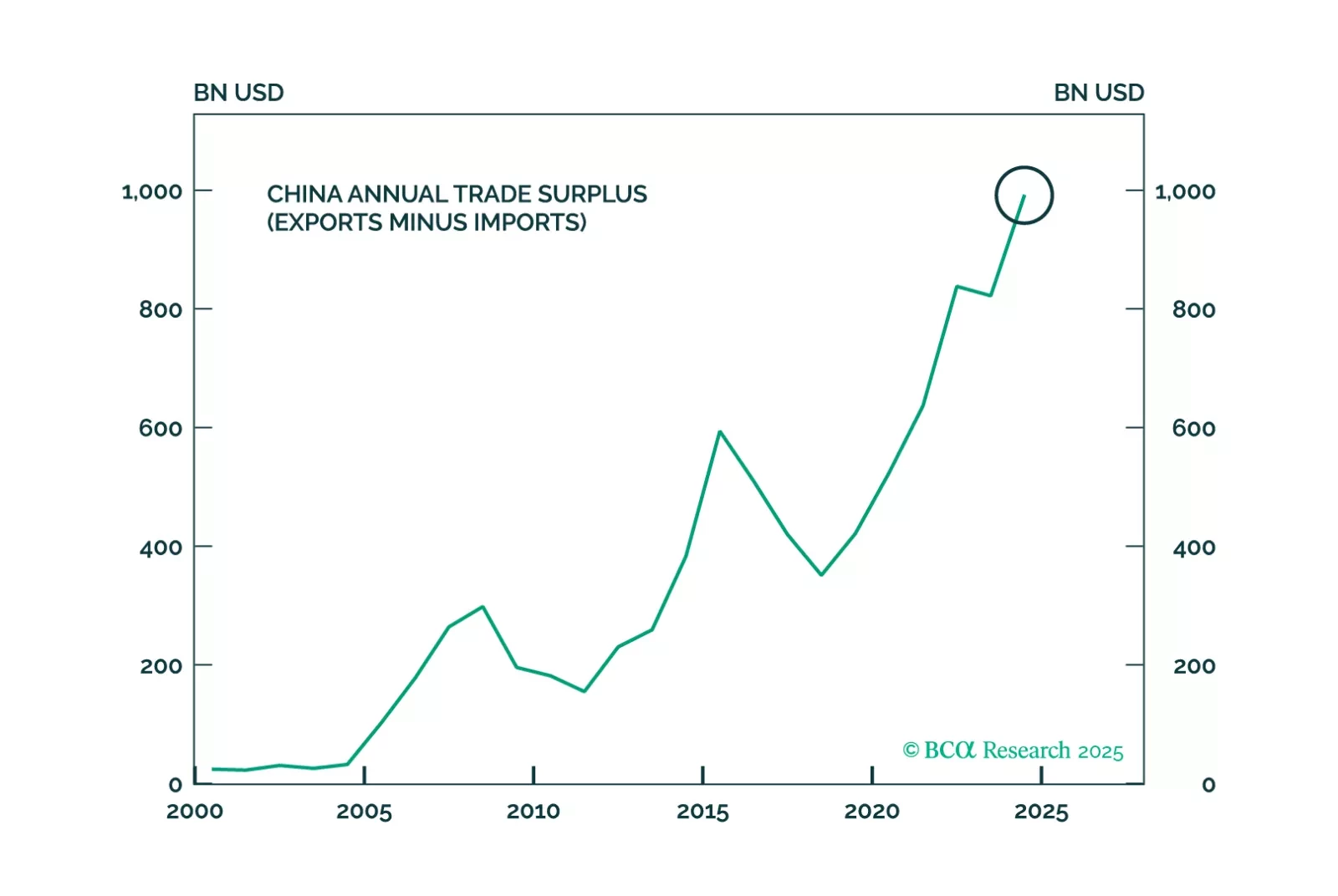

China barely hit its growth target in 2024 by shifting back to its old model of exports, racking up a record trade surplus with the world – right as Donald Trump walks back into the White House. Tariffs will elicit larger fiscal stimulus even as China rolls out innovations such as DeepSeek to meet its 2025 industrial goals, creating a volatile mix this year.

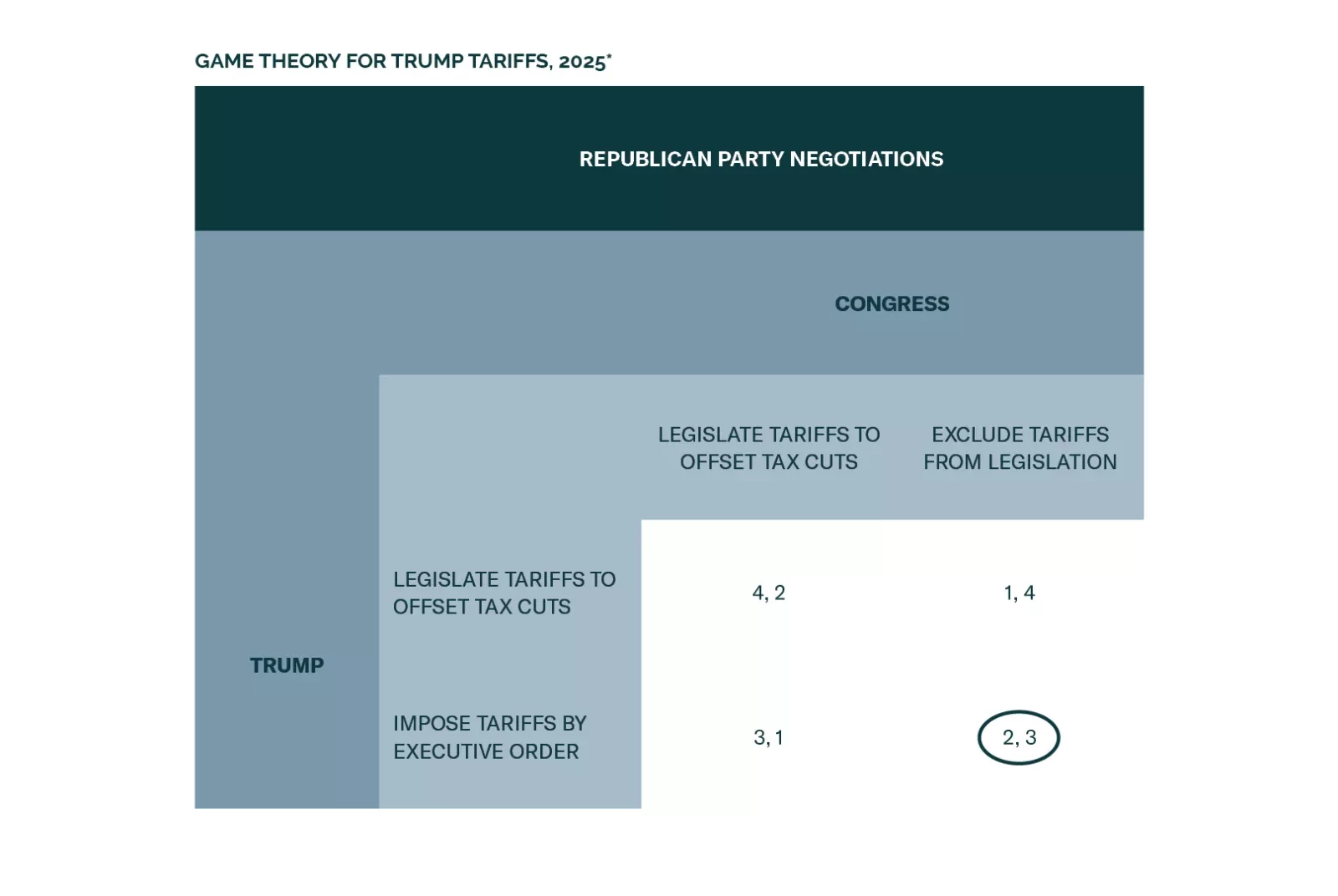

Simple games allow us to model several of the Trump administration’s most disruptive policies in 2025. We find that markets face an increase in volatility as Congress expands the budget, Trump implements tariffs on the world, China retaliates, and Taiwan tensions persist. A ceasefire in Ukraine is a marginally positive outcome for Europe, although it is not a long-term peace treaty.