Brazil

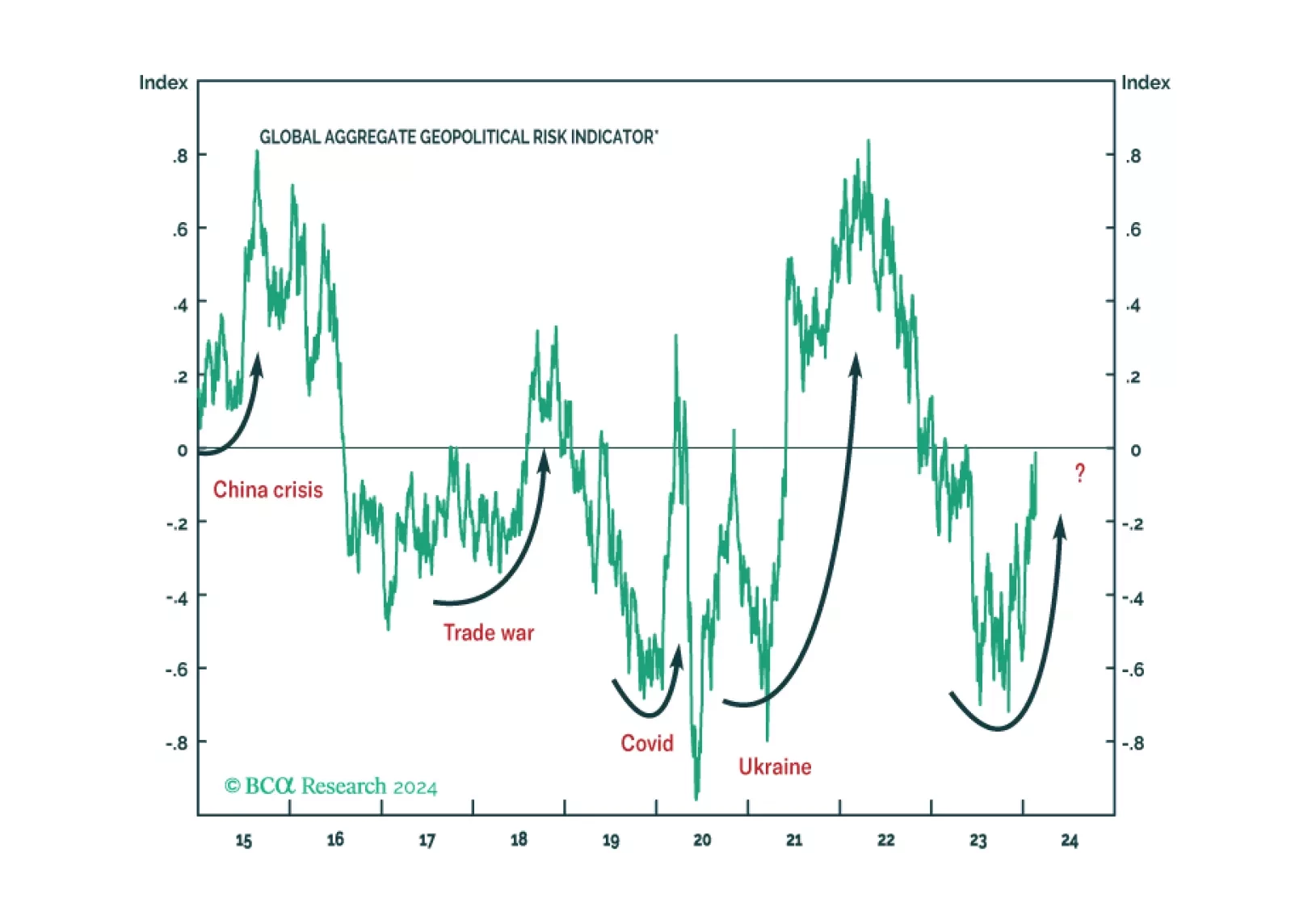

While 2024 will see various election risks, global geopolitical uncertainty is driven by the US election and its struggle with Russia, China, and Iran. The stock market can manage local domestic political risk. But it will correct upon a major outbreak of geopolitical uncertainty.

The Brazilian government and the central bank will be prioritizing growth over curbing the fiscal deficit and inflation. The outcome of an easy policy mix is that growth and inflation will be higher relative to market expectations, and real interest rates will drop considerably. We recommend that investors go long mid- and small-cap stocks on a pullback and inflation-linked bonds. However, foreign investors should hedge the currency risk.

In this report, we explore Brazil’s inflation and monetary policy outlook, the Lula administration’s back-and-forth between pragmatism and populism, and how these factors will affect Brazilian financial markets going forward. All in all, we believe Brazilian risk assets will be in a trading range relative to their EM peers in the next 12 months.

The new fiscal framework will fail to prevent the rise of the public debt-to-GDP ratio as it relies on overly optimistic revenue growth. A rising public debt-to-GDP ratio will lead to a widening fiscal risk premium in Brazilian financial markets. We are making two new recommendations: downgrade Brazilian sovereign credit from neutral to underweight, and go long Brazilian CDS / short Mexican CDS.

Remain cautious and defensive overall. Stay long DM Europe over EM Europe. Look for EM opportunities in Southeast Asia and Latin America over Greater China.

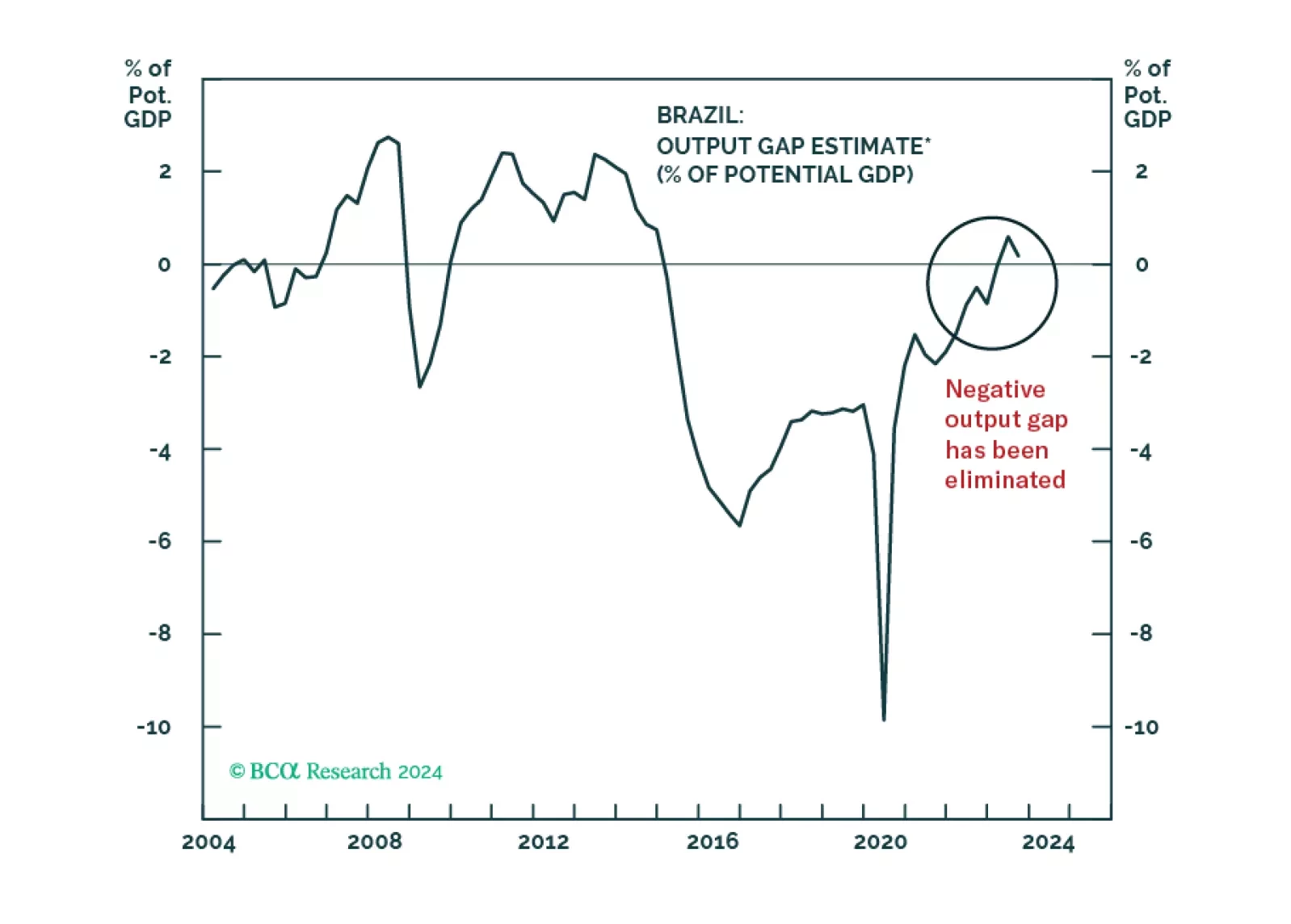

The only feasible way for Brazil to stabilize its public debt-to-GDP ratio is by having nominal GDP growth meaningfully above government borrowing costs. This requires large fiscal stimulus to boost nominal GDP and much lower interest rates. These factors will constitute the economic policy anchor of Lula’s 3.0 presidency. When markets begin to price this in, the outcome will be chronic downward pressure on the currency.