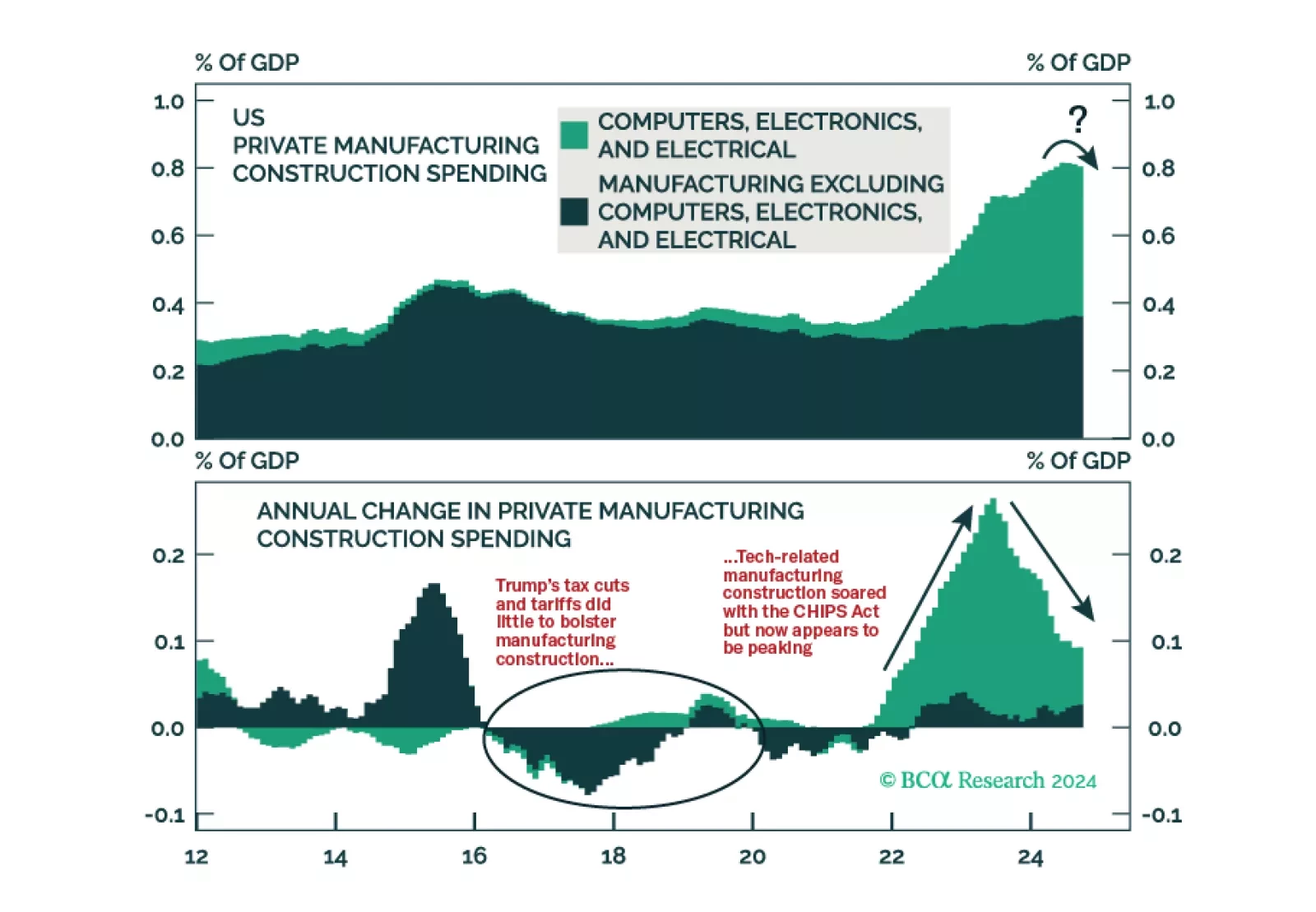

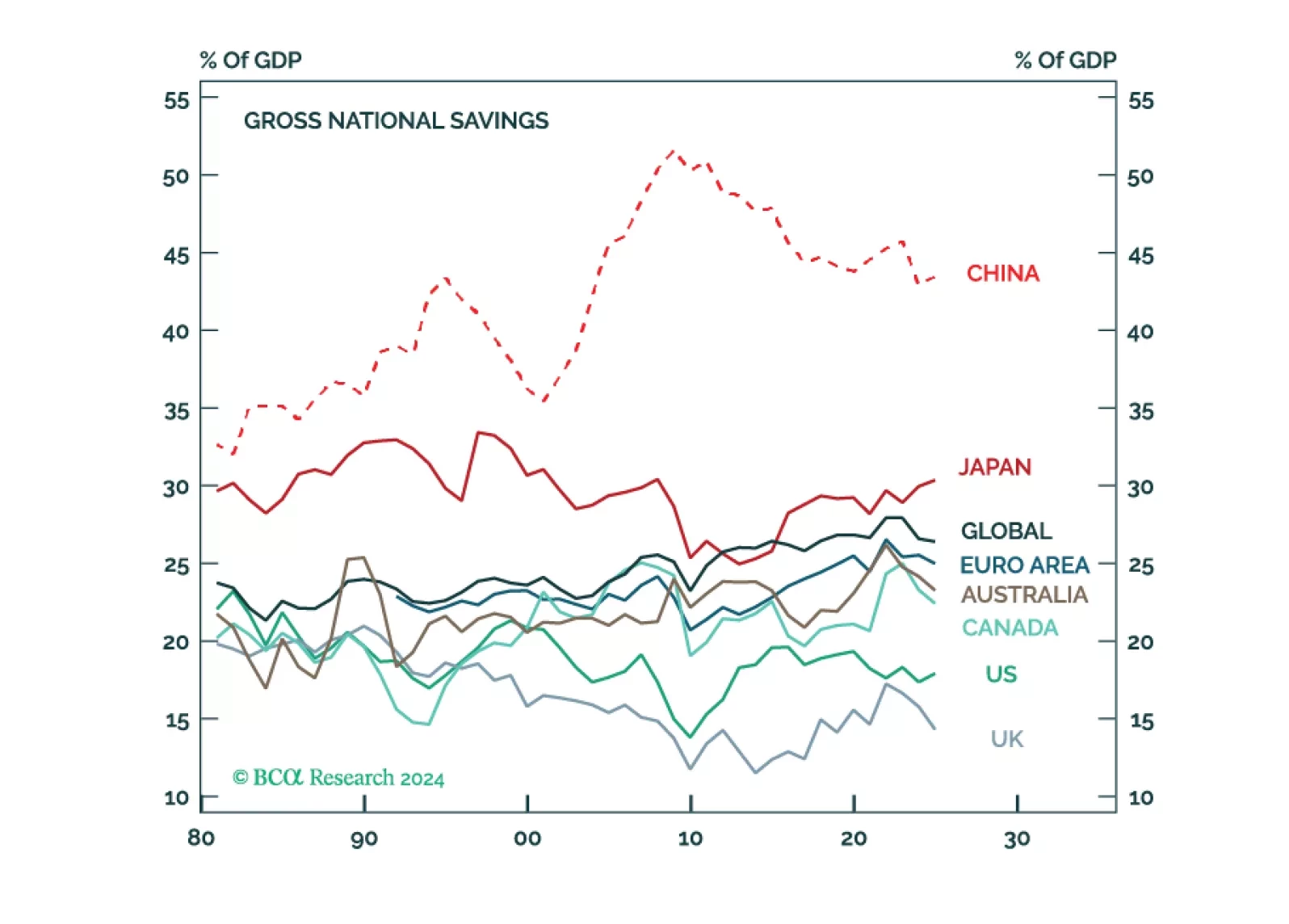

Executive Summary The US Needs To Reduce Its Primary Budget Deficit By Nearly 4% Of GDP To Stabilize Debt Rising government debt in the US has heightened the risk of a fiscal crisis. If interest rates stay where they are, the US primary budget balance would need to improve by nearly 4% of GDP to stabilize the debt-to-GDP ratio.The good news is that bond yields would probably fall if the US government were to bring down the budget deficit, thus allowing for a somewhat smaller fiscal adjustment. The bad news is that many of Trump’s stated policies would lead to larger, not smaller, deficits.That said, interest rates are much higher now than during Trump’s first term. This means that Trump may need to rely more on tariff revenue than investors are currently expecting.He may also allow Republicans in Congress to repeal large parts of the Inflation Reduction Act (IRA), while permitting sharp cuts to social spending.Social spending has a bigger fiscal multiplier than corporate tax cuts. Consequently, even if the federal budget deficit were to rise over the next few years, aggregate demand could still weaken in response to shifts in fiscal policy. With state spending already set to decline, bond yields would probably fall.While government debt is very high in Japan, interest rates remain below nominal GDP growth, which reduces the odds of a crisis. In China, the challenge is to shift the debt burden from local governments to the central government. In peripheral Europe, debt-to-GDP ratios have declined over the past few years but remain dangerously elevated.Bottom Line: Higher interest rates will increase the pressure on governments to trim deficits. In the US, the Trump administration will rely on tariffs to partially pay for tax cuts, while also delivering deeper-than-expected social spending cuts. This will result in lower bond yields over time.The Fundamental Equation of Debt SustainabilityOver the past few decades, most major economies have responded to macroeconomic shocks by easing fiscal policy. In the US, the shift towards bigger budget deficits was exacerbated by a series of tax cuts – such as those in 2001, 2003, and 2017 – which were not offset by lower spending. As a result, government debt stands near historic highs in most economies (Chart 1). Chart 1AGovernment Debt Is Near Historically High Levels In Many Developed Economies (I) Chart 1BGovernment Debt Is Near Historically High Levels In Many Developed Economies (II) How significant are the risks of a major fiscal crisis in the US and elsewhere?To address this question, it is useful to start with the fundamental equation of debt sustainability, which specifies the value of the primary balance (the budget balance excluding interest payments) that is consistent with a stable debt-to-GDP ratio (see Appendix A for a derivation): Where p is the primary budget balance, expressed as a share of GDP; r is the real interest rate; and g is the growth rate of the economy.The US: An Unsustainable Fiscal Outlook Chart 2The US Needs To Reduce Its Primary Budget Deficit By Nearly 4% Of GDP To Stabilize Debt Given that US real bond yields are approximately equal to trend growth, the US would need a primary budget balance of close to zero to stabilize the debt-to-GDP ratio (Chart 2). The Congressional Budget Office (CBO) estimates that the primary budget deficit will be 3.9% of GDP in 2024. This implies that fiscal consolidation of nearly 4% of GDP is required to put government debt on a sustainable trajectory.The good news is that bond yields would probably fall if the government sought to bring down the deficit. If the 10-year TIPS yield were to drop to 1% from its current level of around 2%, 2.9% of GDP in fiscal tightening would be necessary to stabilize the debt-to-GDP ratio.The bad news is that most of Trump’s stated policies would lead to larger, not smaller, deficits. According to the non-partisan Committee for a Responsible Federal Budget, Trump’s proposed spending and revenue measures would raise federal debt by an additional $7.75 trillion over the next 10 years in a central scenario (Table 1). This would cause the debt-to-GDP ratio to rise to 143% of GDP by 2035 – a 44 percentage-point increase from current levels (Chart 3).Why Fiscal Consolidation May Happen, Even Under TrumpGiven what transpired under Trump’s first term, it is understandable that most investors expect the federal budget deficit to only widen further over the coming years. However, there is an important limiting factor to higher budget deficits that was not present during Trump’s first term in office: The 10-year TIPS yield was close to zero when he assumed the presidency in early 2017, and then fell into negative territory once the pandemic began. Back then, the market simply did not care about large budget deficits.This is not the case anymore. Net interest payments on federal government debt have risen from 1.3% of GDP in 2016 to 3.1% of GDP as of 2024. Even under current policy – which unrealistically assumes the personal tax cuts in the Tax Cuts & Jobs Act (TCJA) will sunset at the end of 2025 – interest costs are projected to swell to 4.1% of GDP in 2034, equal to 23% of all government revenue (Chart 4).Table 1Trump's Proposed Fiscal Policies Would Increase The Budget Deficit Chart 3Federal Debt Would Continue To Surge Under Trump's Proposed Policies Chart 4Rising Interest Payments Will Force Fiscal Austerity Chart 5Little Evidence So Far That Productivity Growth Has Shifted Into Higher Gear Faster Productivity Growth? Hopefully, But Don’t Bet on It Chart 6Capital Spending Remains Downbeat The US could get lucky and experience much faster productivity growth. As the fundamental equation of debt sustainability highlights, this would allow for a larger budget deficit.Unfortunately, there is little evidence so far that productivity growth has shifted into higher gear. While the productivity numbers have improved somewhat over the past few quarters, this follows a period where output-per-hour shrank outright. Averaging the productivity numbers since the start of the decade, we are still close to the pre-pandemic trend (Chart 5).Meanwhile, key drivers of productivity growth, such as capital spending, remain downbeat (Chart 6).In any case, economic theory suggests that faster productivity growth should raise the rate of return on capital. Increased competition for private-sector savings should, in turn, push up the interest rate at which the government borrows. As per the debt sustainability equation, this would necessitate a higher primary budget balance. Yield Curve Control Is Not As Easy As It SeemsOne possible strategy to keep interest costs down, while still running large budget deficits, is for the Fed to purchase bonds which trade above a certain prespecified yield. This is exactly what the Bank of Japan did with its Yield Curve Control (YCC) policy.Let us put aside the issue of the Fed’s independence. In the unlikely case that the Fed could be cajoled into pursuing such a scheme, it would still run into a major problem: inflation.The Bank of Japan was able to cap yields because the economy was suffering from deflation. Even in the absence of the rate cap, yields would probably not have risen very much.If the Fed were to try to cap yields – effectively monetizing government debt – inflation expectations would rise. Higher inflation expectations would push down real yields, increasing the incentive for firms to borrow and for households to spend more in advance of higher prices. Such a dynamic would cause the economy to overheat, leading to even higher inflation expectations.As the last few years have demonstrated, inflation is very unpopular. Whereas higher unemployment mainly hurts those who lose their jobs, inflation hurts everyone. Thus, pursuing any strategy that produced higher inflation would be political suicide.The Multiplier-Weighted Fiscal Thrust Will Probably Be Negative Next YearIt is highly likely that the Trump administration will push through a full extension of the TJCA. However, this will just maintain the status quo. It will not represent new stimulus. Chart 7Manufacturing Construction May Be Peaking Additional stimulus could come in the form of eliminating taxes on tips, which was one of Trump’s signature campaign promises. Such a move would reduce revenue by a relatively modest $300 billion over 10 years. Exempting overtime income and social security benefits from taxation would be much more costly – worth a combined $3.3 trillion over 10 years. However, Trump did not emphasize these measures very heavily on the campaign trail and so they will probably be dropped.Trump did mention cutting the corporate tax rate further from 21% to 15%. However, such a step may run afoul with populists in the Republican Party and their derision for “woke capital.” Trump himself mused earlier in the campaign that he would be content to just cut the corporate tax rate to 20% (a “nice round figure” as he called it).On the flipside, Trump could increase tariffs significantly, raising $2-to-$4.3 trillion over 10 years. Contrary to Trump’s claims, tariffs would be a regressive tax on households. Moreover, to the extent that half of global trade is in intermediate goods, higher tariffs would effectively boost taxes on businesses.In order to keep bond yields from rising further, Trump may let the Republicans in Congress take an ax to government spending. This could mean repealing large parts of the Inflation Reduction Act (IRA) (Chart 7). It could also mean sharp cuts to social spending. Trump’s promise this week to eliminate the Department of Education – whose $238 billion annual budget largely consists of doling out assistance to low-income students – is a good example of what may lie ahead.Social spending has a large fiscal multiplier because the poor generally spend whatever income they receive. Corporate tax cuts, in contrast, have a smaller multiplier since they disproportionately benefit highly profitable companies that are not liquidity constrained. Consequently, even if the federal fiscal deficit were to rise over the next few years, aggregate demand could still weaken in response to shifts in fiscal policy.In such a scenario, bond yields would likely decline. Lower aggregate demand would prompt the Fed to cut rates more than is currently discounted. While a larger deficit would entail more Treasury issuance, higher after-tax private-sector savings would be able to absorb most of that debt.A Word on State and Local Government SpendingMost people focus on fiscal policy at the federal level. However, it is worth remembering that state and local government spending is half as large as overall federal spending and double that of discretionary federal spending.State and local government spending jumped during the pandemic on account of the transfers that those lower levels of government received from Washington. Having spent most of the money, expenditures will decline. The Association for State Budget Officers reckons that state spending will fall by about 6% in 2025, the first annual decline since the GFC (Chart 8).Debt Sustainability Outside the USGovernment debt in Japan remains the highest in the G7. Although this debt is a source of vulnerability, it needs to be seen in the context of the debt sustainability equation discussed at the outset of this report.The 10-year Japanese government bond yield currently stands at 1.07%. This is less than nominal GDP growth, which clocked in at 2.9% year-over-year in Q3 2024. The IMF expects nominal GDP growth to average 2.8% over the next five years, which should bring net debt down from 156% of GDP to 151% of GDP (Chart 9). Chart 8State Spending Is Expected To Shrink Chart 9If Sustained, The Recent Acceleration In Japanese Nominal GDP Growth Should Mitigate The Risks Of A Fiscal Crisis Government revenue in Japan, as a share of GDP, is the second lowest in the G7 after the US (Chart 10). The Japanese government would sooner raise taxes than allow a debt crisis.In China, debt levels are high in the corporate sector and among local governments. Household debt rose sharply in the pre-pandemic period but has been broadly flat over the past few years (Chart 11). Chart 10Japan's Government Has Room To Raise Revenue Chart 11Breakdown Of Chinese Debt One distinguishing feature of China’s economy is that it generates large amounts of savings. The national savings rate is close to double that of most other major economies (Chart 12). The flipside of this excess savings is inadequate spending. Insufficient demand is fueling deflation, leading to anemic nominal GDP growth (Chart 13).What China ultimately needs is more spending. Unfortunately, the fiscal impulse is currently close to zero against a budgeted target of 2.2% of GDP (Chart 14). Local governments account for nearly 90% of overall government spending but have been hamstrung by falling land sales. Chart 12China Saves Too Much Chart 13Deflation Risks Have Risen In China Efforts by the central government to replace debt issued by local government financing vehicles (LGFVs) with central government-backed liabilities are welcome. However, this may only bring spending back towards where it should have been all along. Chart 14Chinese Government Spending Is Well Below Target Chart 15Debt-To-GDP Ratios Have Declined In Europe's Periphery Over The Past Few Years But Remain Dangerously Elevated Turning to Europe, the peripheral economies have made some progress in bringing down debt-to-GDP ratios in the aftermath of the pandemic (Chart 15). However, government debt is still very high, and in the case of Italy, the IMF expects the debt-to-GDP ratio to start rising again over the next few years. Although the ECB will take the necessary steps to preclude another crisis, peripheral Europe will need to pursue fiscal austerity for years to come.Trade UpdatesWe were stopped out of our long US health care/short S&P 500 trade, with the appointment of RFK Jr. being the coup de grâce. There is a reasonably high probability that he will not be confirmed by the Senate, so we are reinstating the trade, but this time against consumer discretionary stocks. Consumer discretionary companies are particularly vulnerable to a trade war and a potential US recession next year.Meanwhile, we are maintaining our bearish bias on stocks by being long the June 30, 2025 SPY ETF put with a strike price of $550, which has risen 25% since we initiated the position last week. Peter BerezinChief Global Strategistpeterb@bcaresearch.comPlease follow me onLinkedIn & Twitter APPENDIX AThe Arithmetic Of Debt SustainabilityGlobal Investment Strategy View MatrixThe Global Investment Strategy team (GIS) summarizes its views via a matrix featuring recommendations over a tactical 1-to-3 month horizon and a cyclical 6-to-12 month horizon. While GIS uses the MacroQuant model as one of several inputs into its decision-making process, the GIS views shown in this matrix may differ from the MacroQuant model's recommendations shown in the dedicated monthly MacroQuant reports.Special Trade Recommendations