China

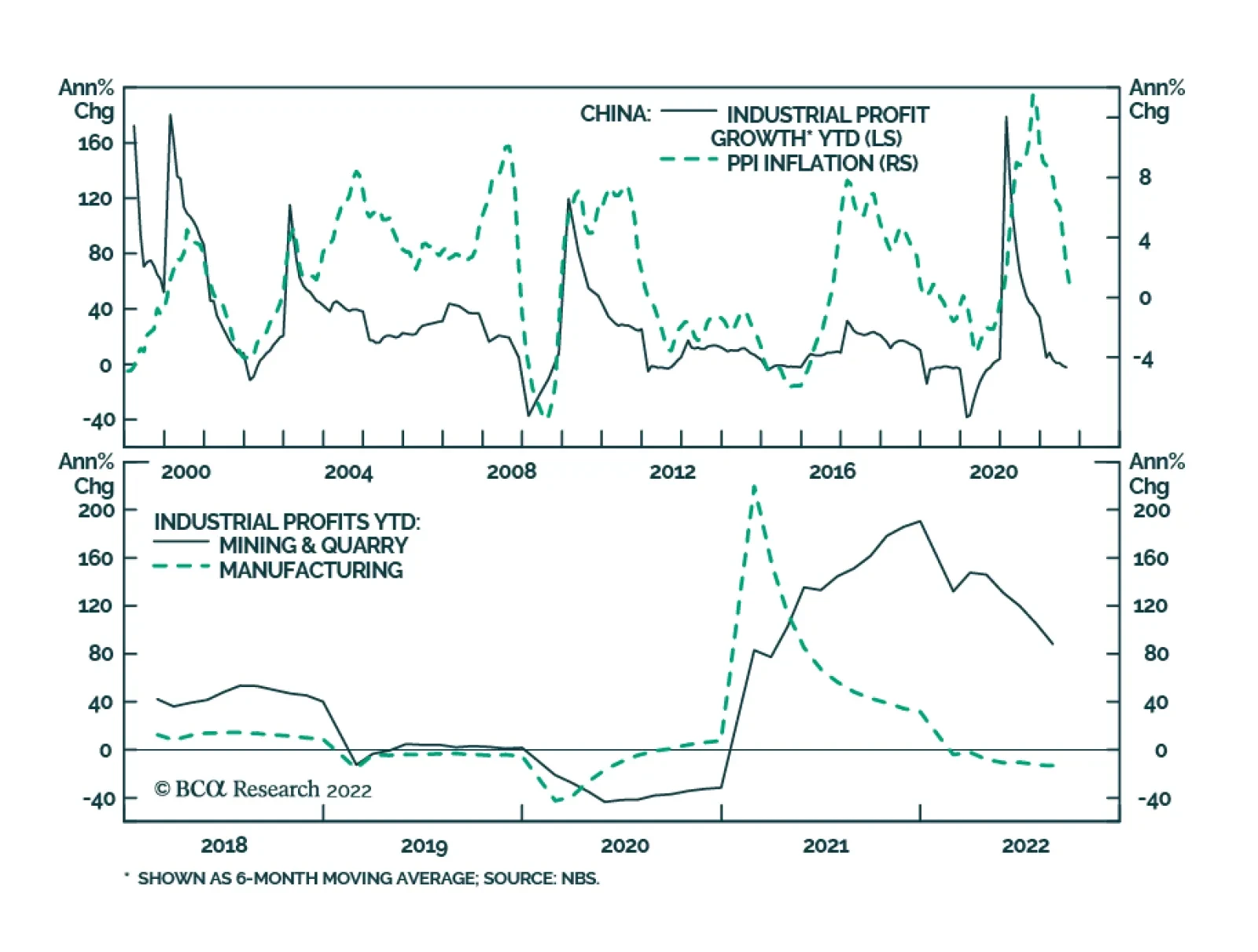

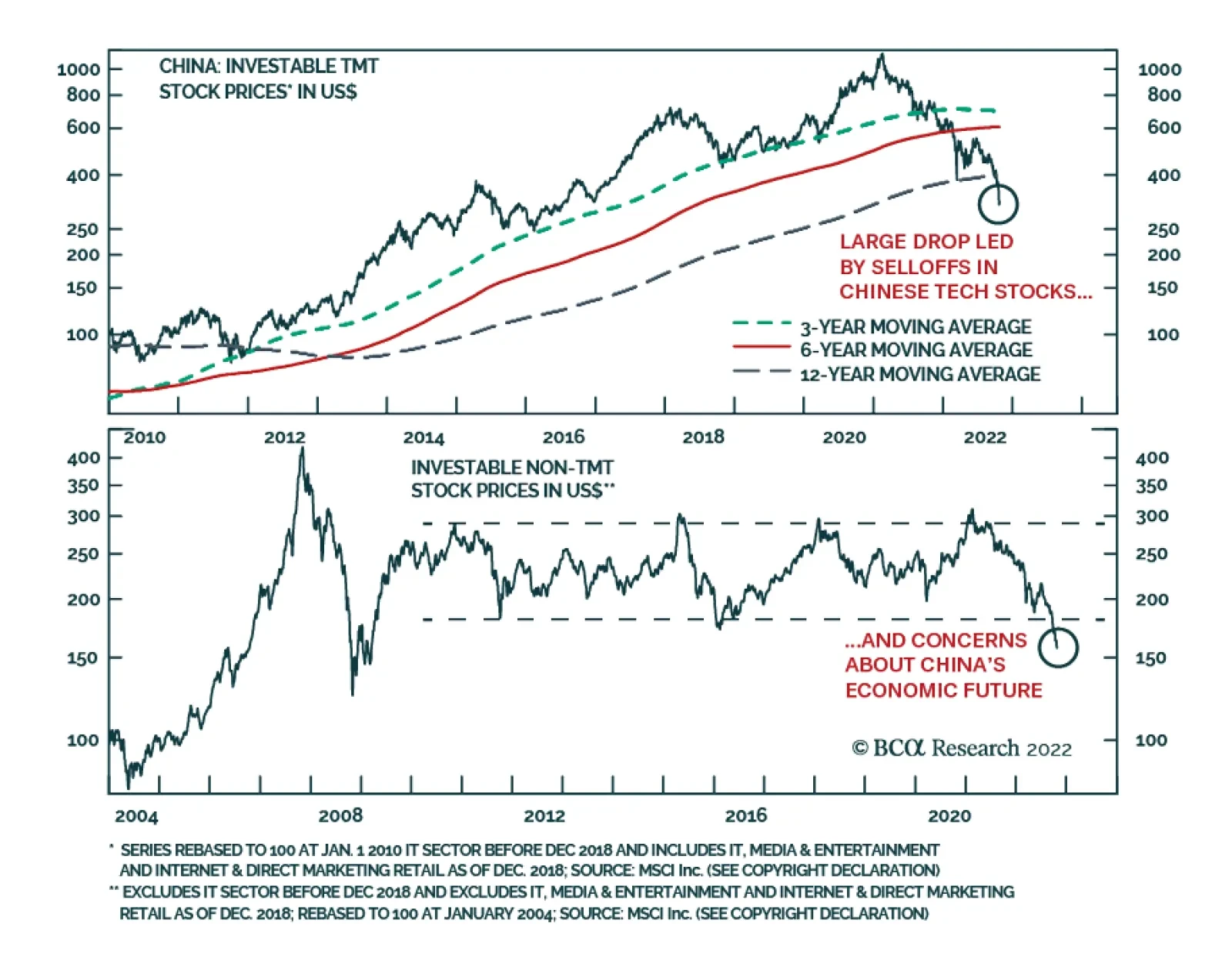

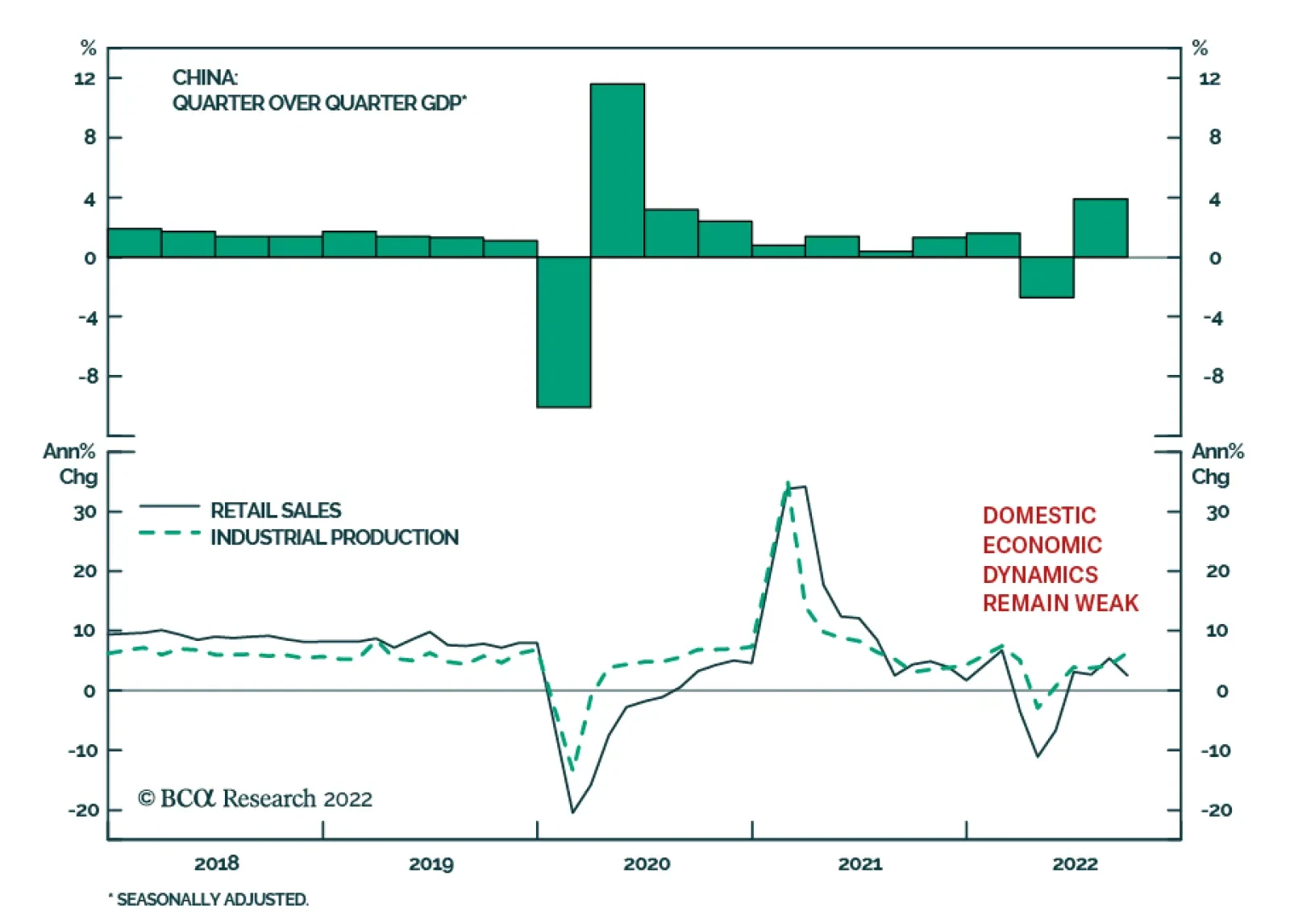

China's economy is about to experience demand-driven deflation. The lack of an economic recovery and falling producer prices will depress corporate profits and, hence, share prices. Beijing will allow the yuan to depreciate more to prop up its economy.

Stay short Greater China assets. Stay long Japanese yen. Hold back on Brazil for now but look forward to opportunities in future.

Falling inflation will allow bond yields to decline in the major economies over the next few quarters. As such, we recommend that investors shift their duration stance from underweight to neutral over a 12 month-and-longer horizon and to overweight over a 6-month horizon. Structurally, however, a depletion of the global savings glut could put upward pressure on yields.

In Section I, we note that while recent inflation developments point to some supply-side and pandemic-related disinflation, they also point to potentially stickier inflation over the coming several months. The inflation, monetary policy, and geopolitical outlook remains sufficiently risky that an overweight stance towards equities within a global multi-asset portfolio is not justified, and we continue to recommend a neutral stance for now. This month’s Section II is a guest piece written by Martin Barnes. Martin, who retired from BCA Research as Chief Economist last year after a long and illustrious career, discusses the outlook for government debt and the possibility of an eventual crisis.

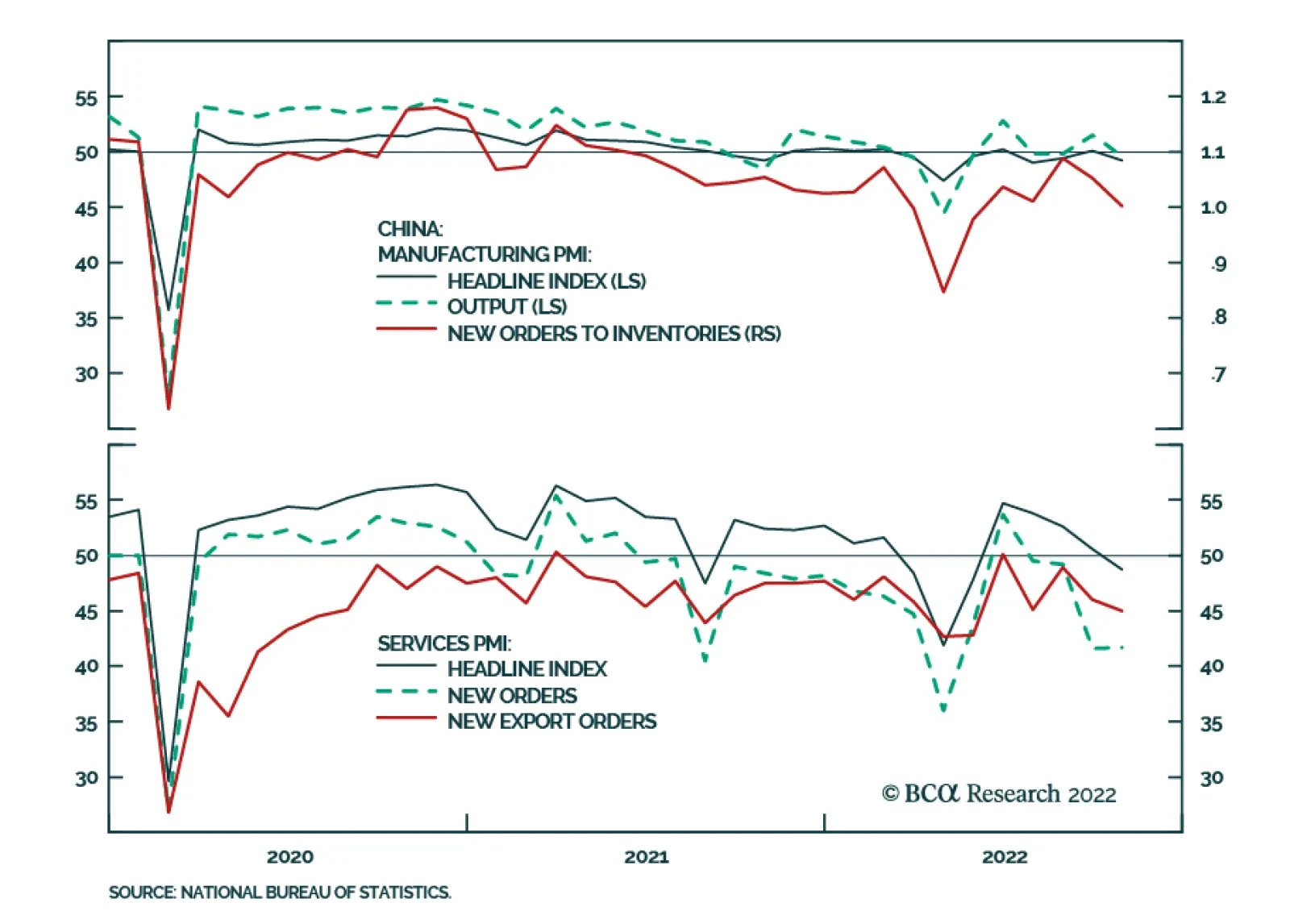

The 20<sup>th</sup> Communist Party Congress concluded on Sunday with President Xi Jinping cementing his third term in office. We are maintaining our cautious stance on Chinese stocks and the exchange rate. The lack of a significant shift away from current macro and regulatory policies means that China’s economic recovery and stock performance remain at risk.

There has been an unprecedented divergence between global and Chinese thermal coal ("coal") prices since the Russia-Ukraine war commenced in February 2022. Such a wide price gap is unsustainable. This price convergence will continue, with international prices falling faster than Chinese ones.