Developed Countries

A country’s external balance remains one of the key pillars of the longer-term trend for the exchange rate. In this week’s report, we look at the developments in global basic balances, and their implications for currency strategy.

The G7’s attempt to insert itself in the oil-price-formation process performed by global trading markets will distort markets and the signals driving production, consumption and investment. The G7 will need a face-saving off-ramp to ditch this planner-based proposal. We expect Brent prices to move toward our expectations of $105/bbl in 4Q22 and $118/bbl in 2023, and remain long the XOP ETF.

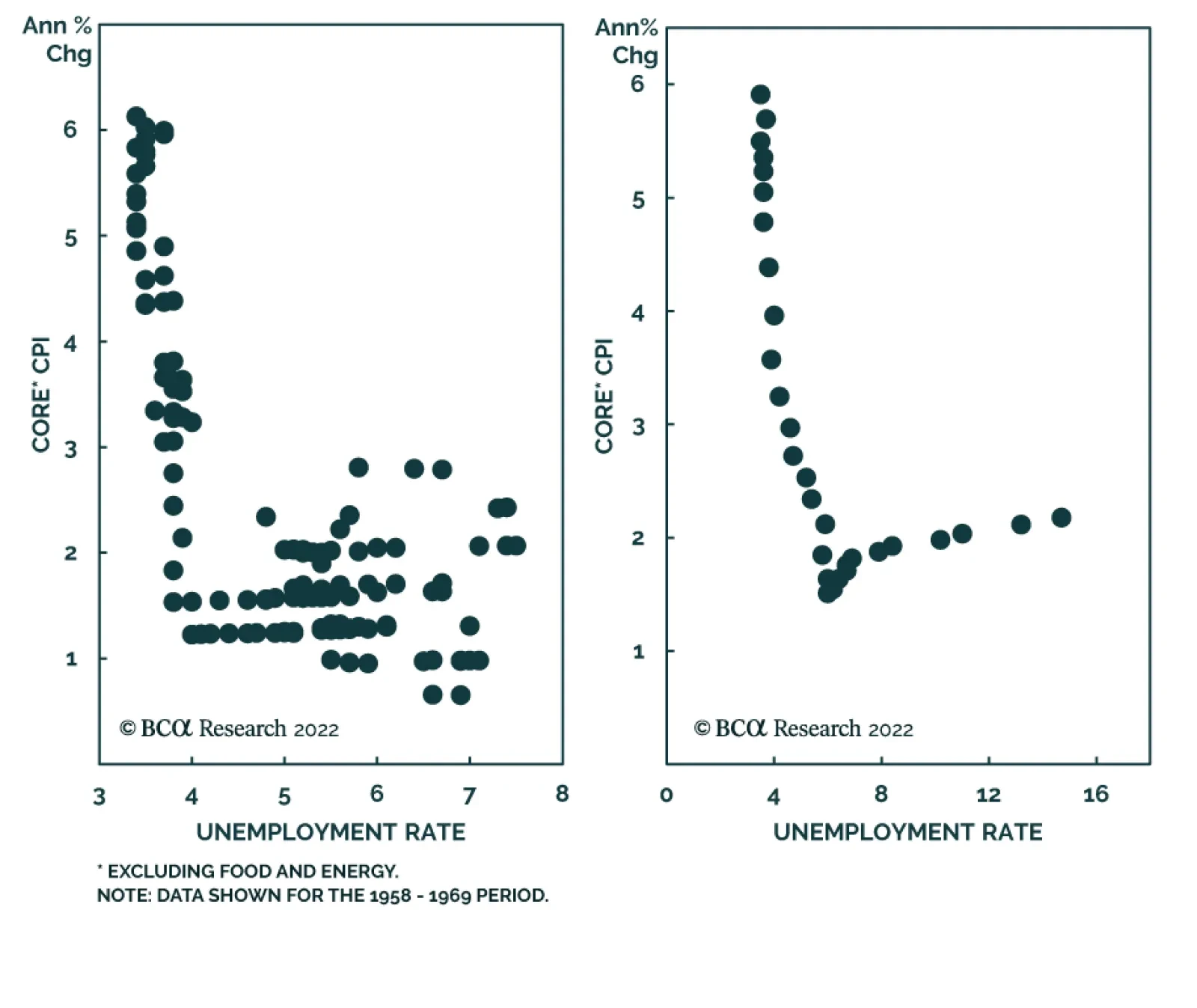

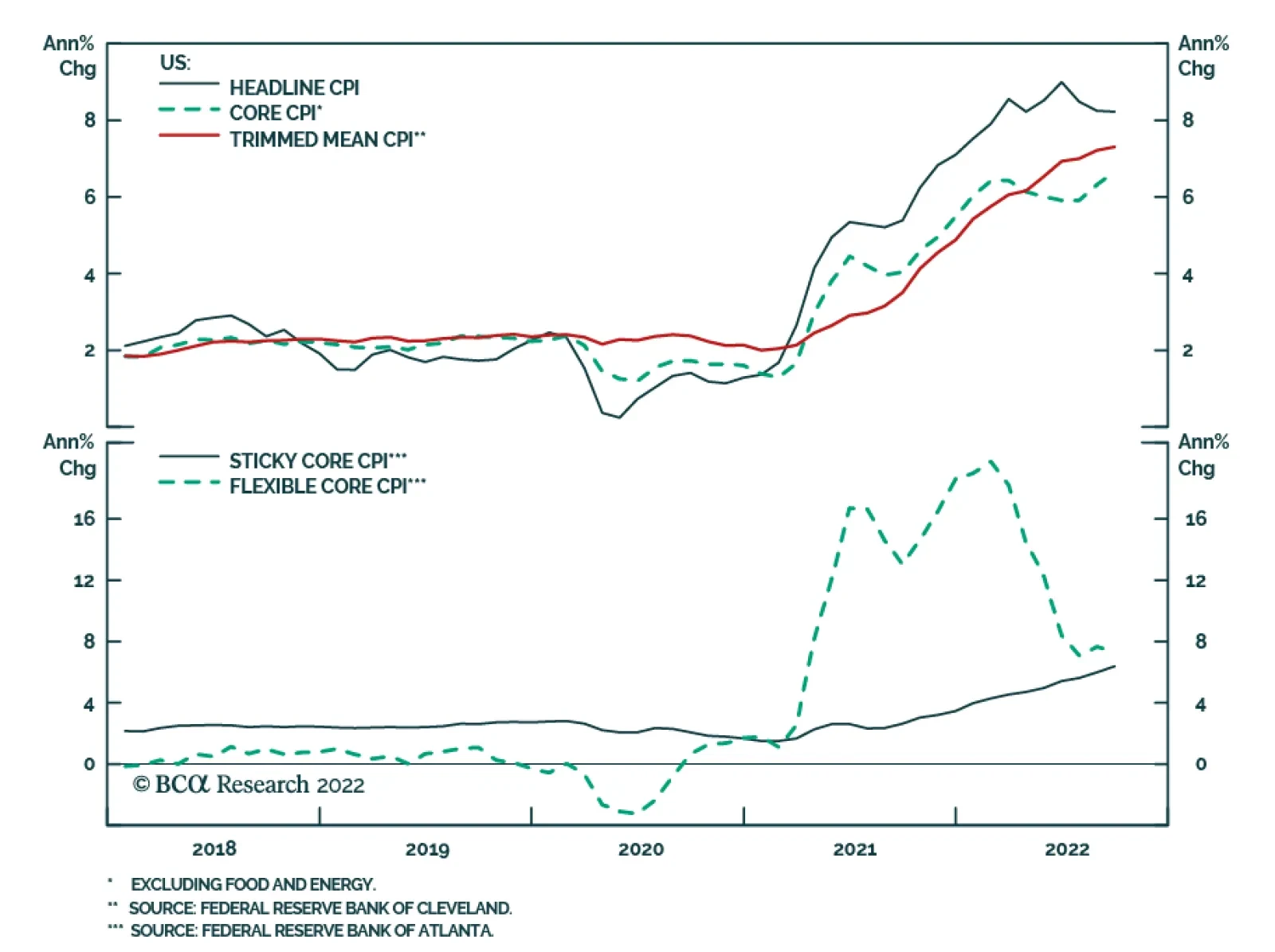

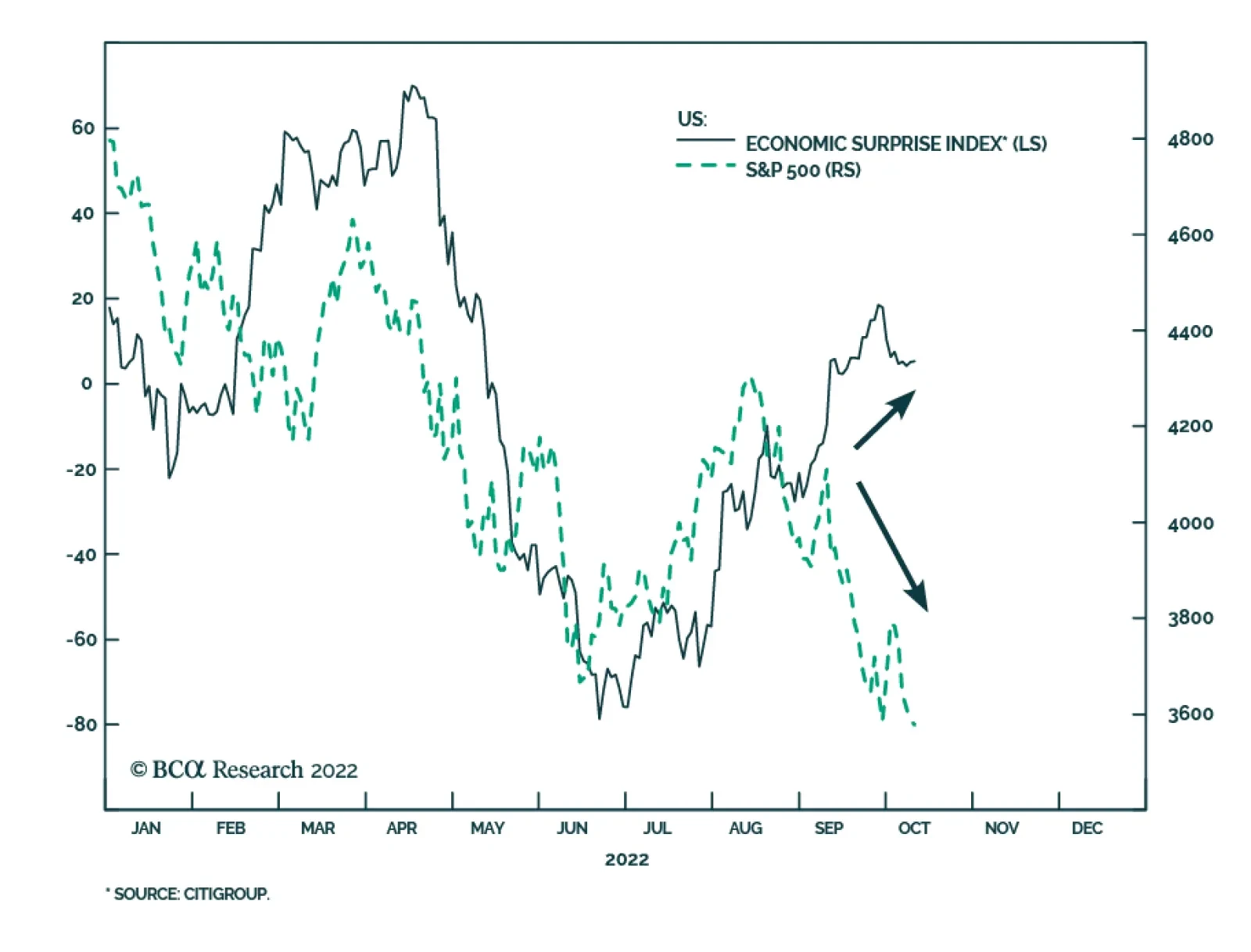

BCA’s Emerging Markets Strategy team’s view remains that US inflation will prove to be sticky. That said, in this report, we examine under what conditions a considerable drop in US core inflation, whenever it transpires, would be bullish for stocks. Potentially significant US disinflation would be bullish for stocks if it is due to an improvement in supply-side dynamics, but bearish if it is demand driven.

Is the BoE’s emergency intervention in its bond market a British idiosyncrasy that global investors can ignore? No, the UK’s near death experience sends three salutary warnings, with implications for all investors.