Developed Countries

Stay defensive at least until the US midterm election is over. Gridlock is disinflationary in 2023 and hence marginally positive for US equities. But any relief rally will be short-lived as recession risks are very high.

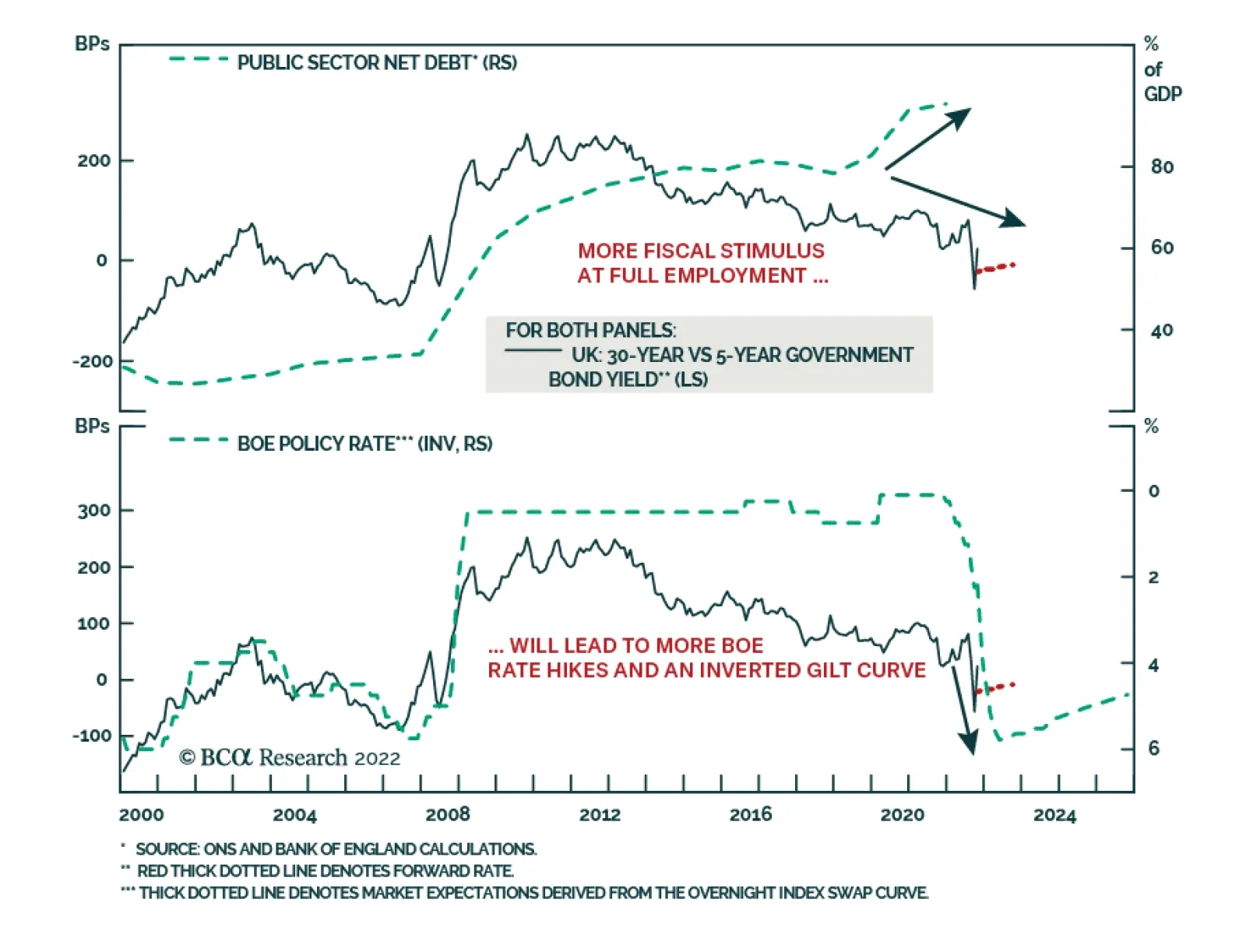

Our preferred tactical global fixed income trades for the rest of 2022 into early 2023 are all expressions of our views on relative monetary policy shifts within the main developed market economies. These involve bets on a relatively more hawkish Fed and Bank of England versus a relatively more dovish ECB and Bank of Canada, while also betting on additional selling pressure on Italian government bonds.

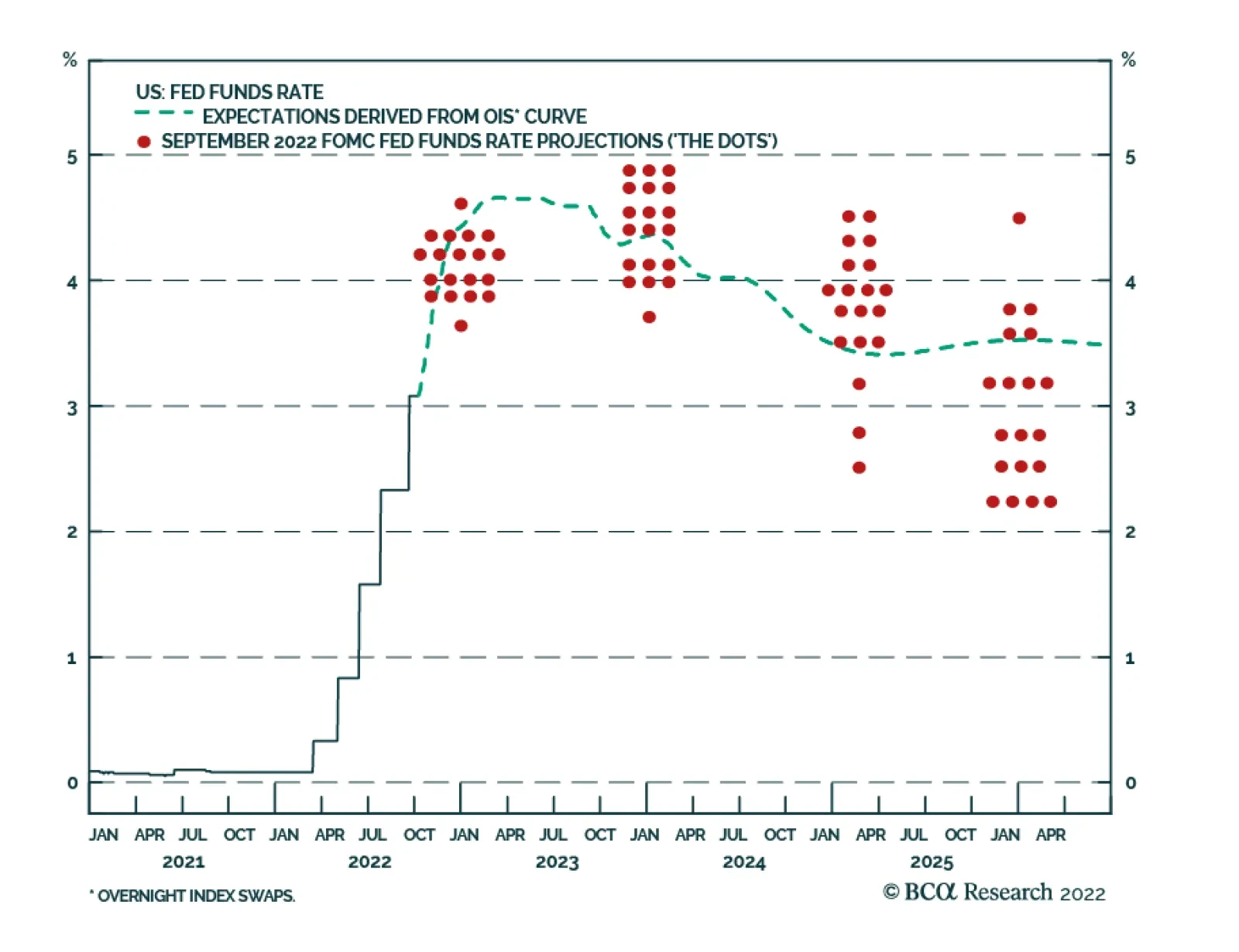

We continue to anticipate that the Fed won’t pause its tightening cycle until Q1 or Q2 of 2023, and current labor market trends certainly give no indication that a Fed pause (or “pivot”) is imminent.

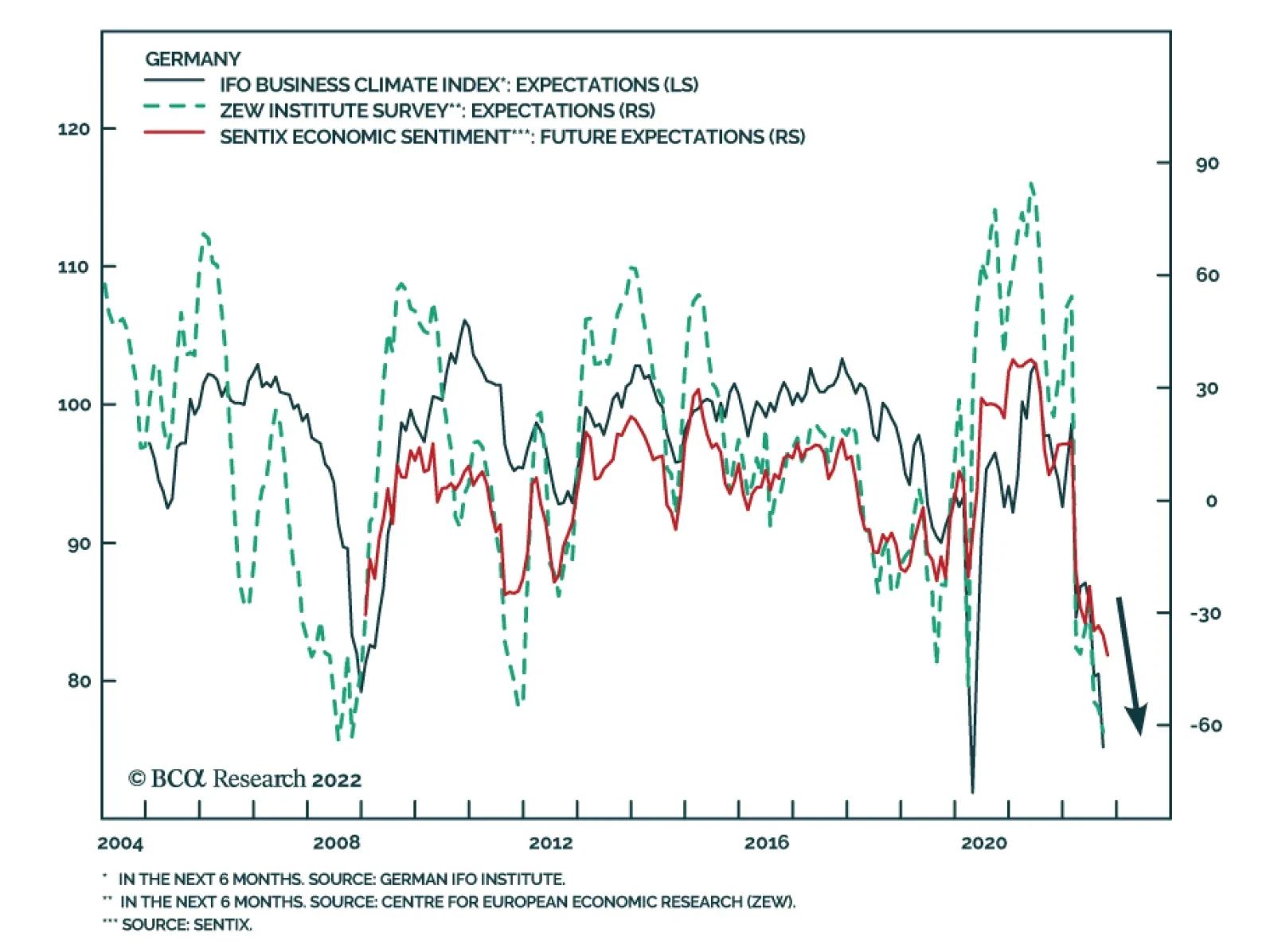

Sentiment toward stocks is depressed and European valuations have declined substantially. However, the earnings outlook remains poor. Which side will win?