Diplomacy/Foreign Relations

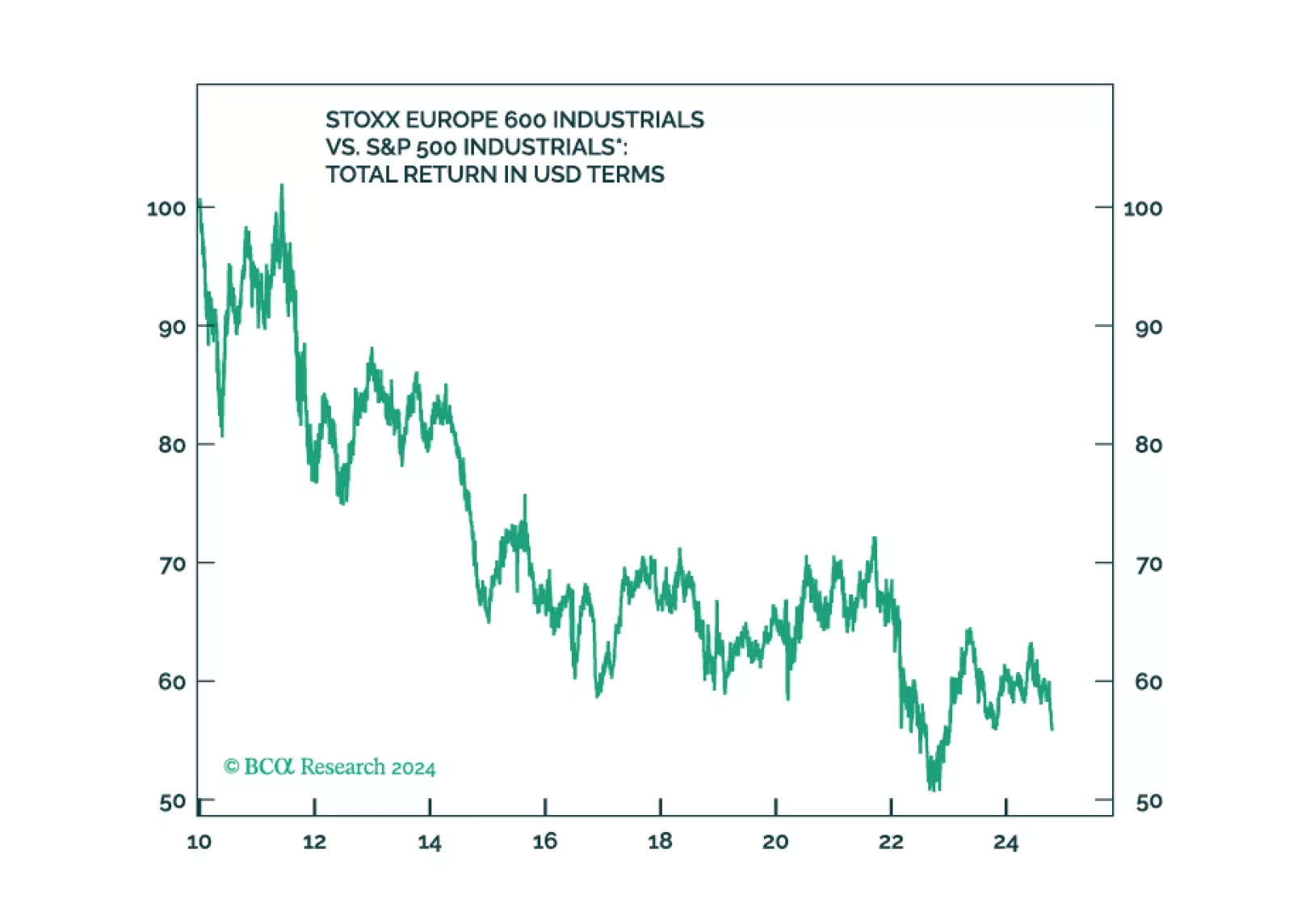

In this Special Report, Marko Papic, Chief Strategist of BCA Research’s GeoMacro Strategy, and Mathieu Savary, Chief Strategist of BCA Research’s European Investment Strategy, together argue that the conflict in Ukraine is already frozen, already losing support in the West, and is likely to taper off over the course of 2025. However, there is no easy alpha left to harvest from that conclusion, the market has already moved on. Some long-term investment opportunities remain in broad European assets.

We maintain 37% odds of a major recessionary oil shock, 51% odds of minor shocks, and 12% odds of no shocks.

Markets are rallying on Fed rate cuts and China stimulus but there will also be October surprises ahead of the US election, which Trump could still win. Russia’s conflict with the West is escalating and the Middle East is destabilizing further. Investors should favor US bonds but they should add some risk in emerging markets in response to China’s policy turn.

As we head into a more turbulent macroeconomic and geopolitical period, investors should favor countries with newly elected government, small government size, and ample room to cut policy rate. Ideally, they should also be in a stable region, and not so dependent on the US or China. Hence, we are introducing the Global Political Capital Index as a way to integrate these factors into a score that can help narrow down the countries with the best and worst abilities to deal with the incoming challenges.

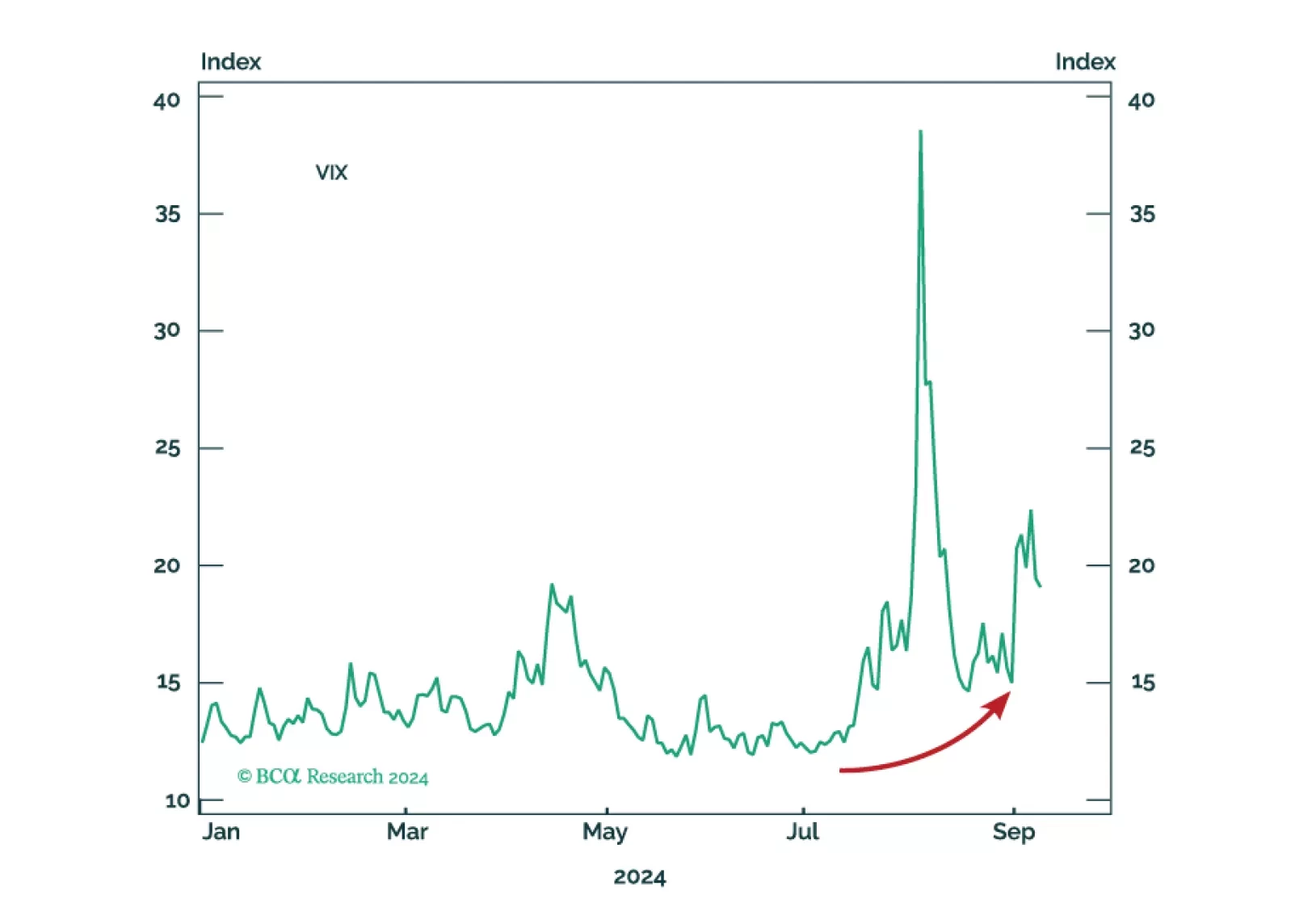

Investors should de-risk tactically in expectation of shocks and surprises ahead of the US election and an uncertain aftermath. Democratic victory with a gridlocked Congress is our base case but would bring minor tax hikes and nuclear brinksmanship with Russia. A Republican single-party sweep offers huge tax cuts but also a global trade war. Recession looms regardless.

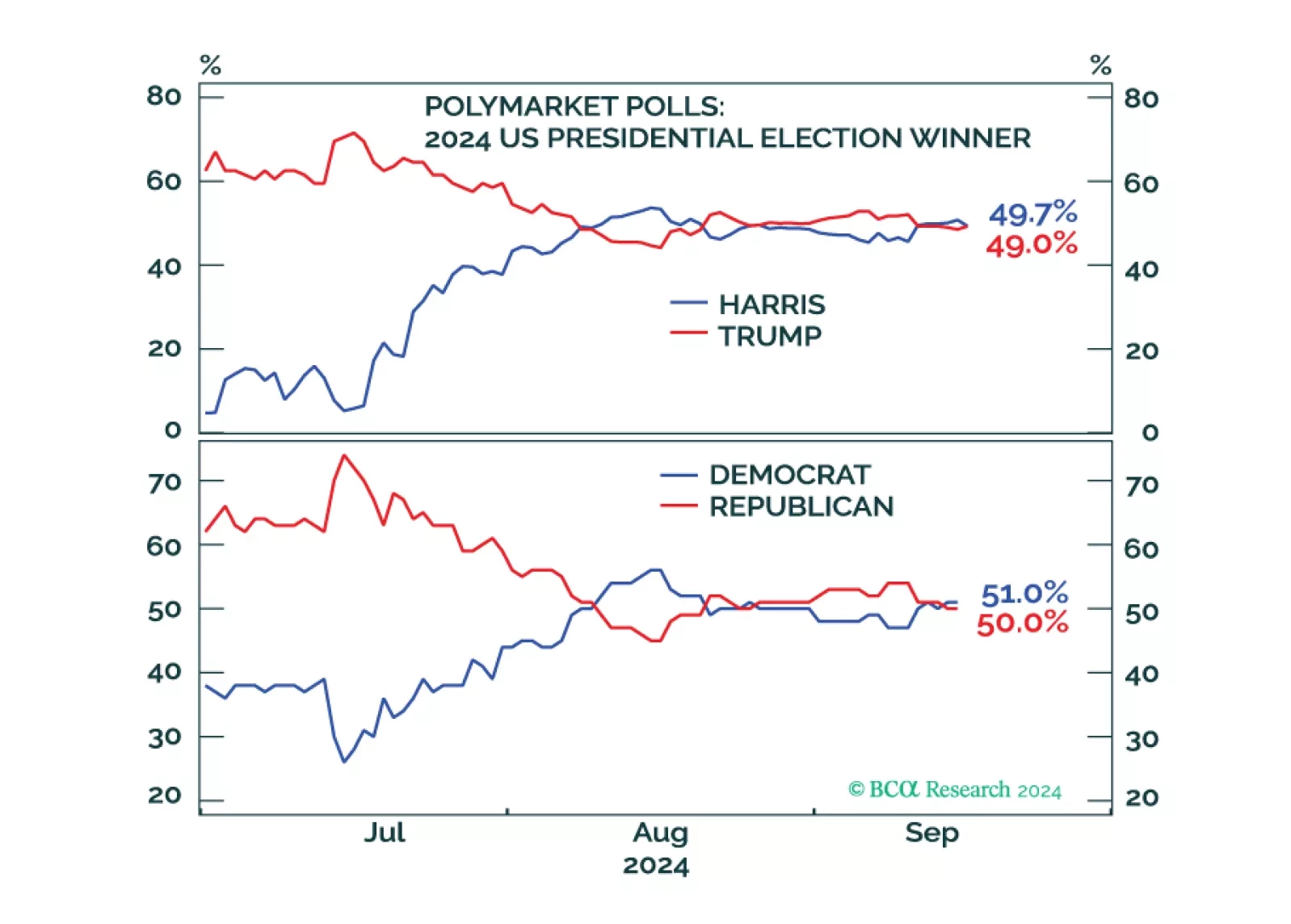

Despite the disastrous performance by former President Trump in the debate with Vice President Kamala Harris, there are still paths for him to come back to power. The economy and global instability could flare up anytime between now and election day, while quirks in the Electoral College ensure that the election will be close. The race is still competitive and policy uncertainty and volatility will be elevated.