Economy

China’s economy is weakening across the board as global risk-off hits equities. With housing conditions worsening and exports contracting—a perfect storm—Beijing faces mounting pressure to deliver stronger, housing-focused stimulus.

Today, we are sending you the BCA annual outlook for 2026. The report is an edited transcript of our recent conversation with Mr. X and his daughter Ms. X, who are long-time BCA clients. Our discussion featured BCA’s economic and financial market outlook for the year ahead.

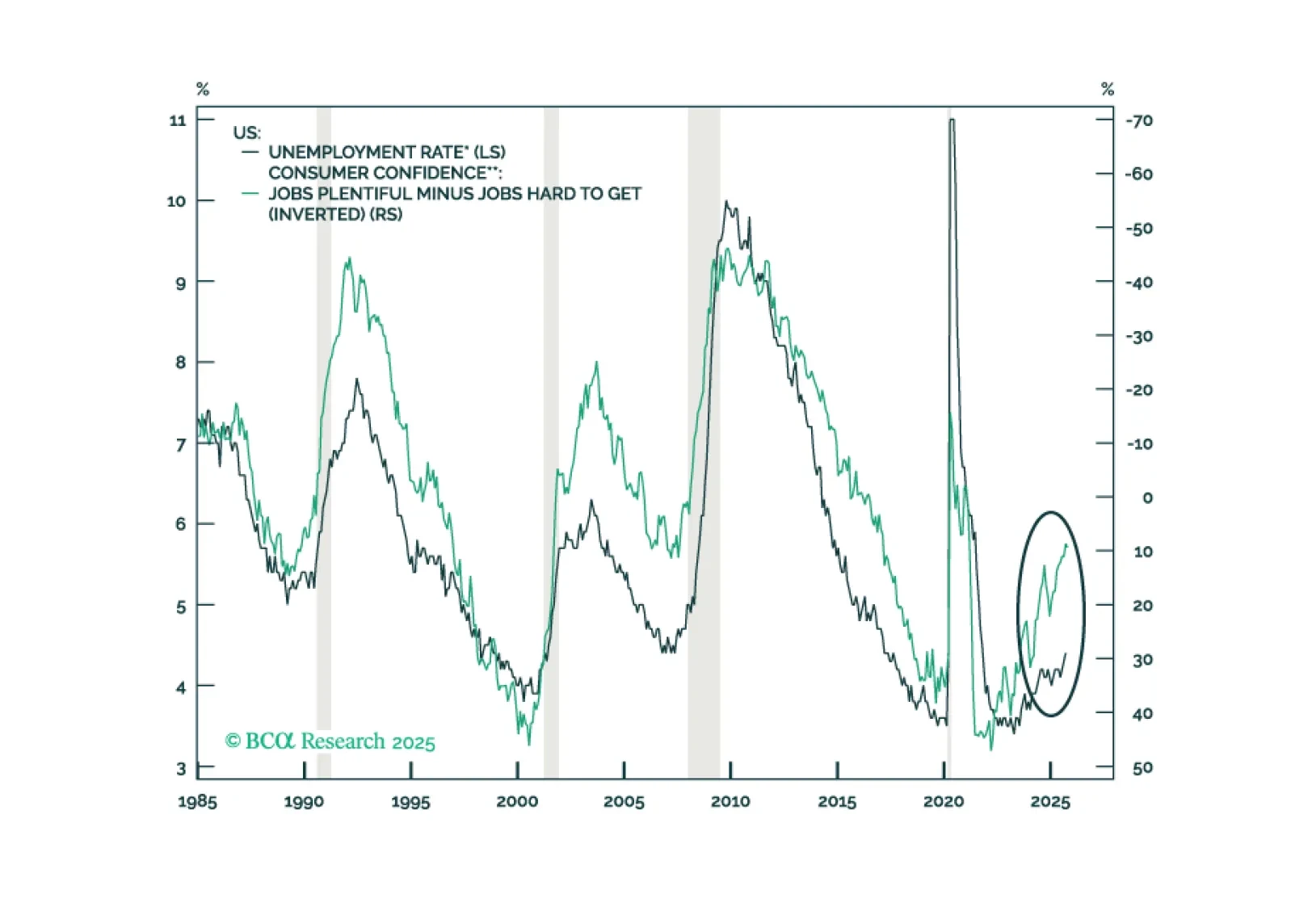

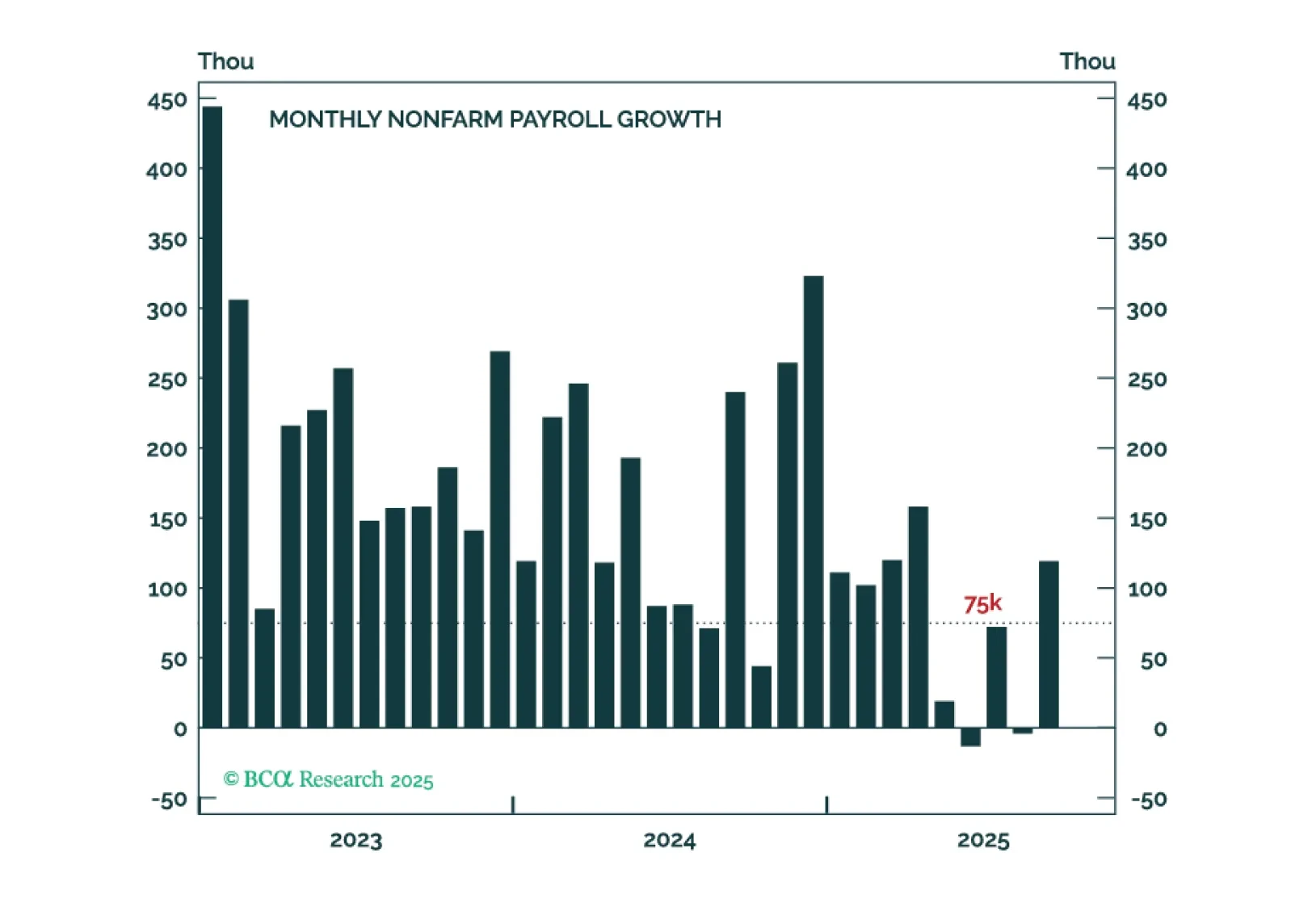

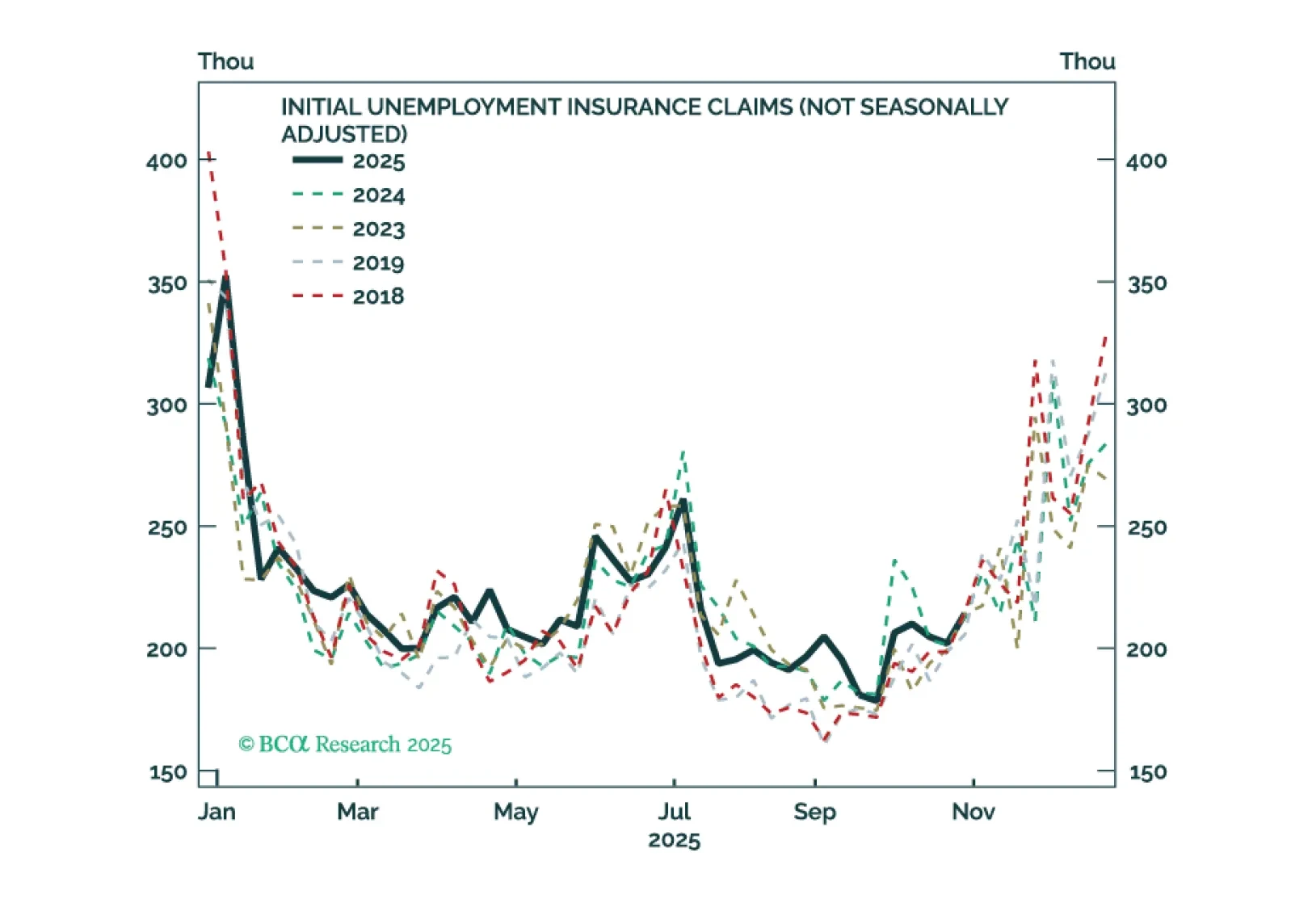

The September employment report probably won’t convince enough hawks to vote for a rate cut in December.

Germany’s economy is regaining momentum after nearly two years of recession. Despite the ongoing cyclical rebound and fiscal stimulus, political gridlock and deep-seated structural challenges threaten to limit the country’s long-term growth potential. Investors should be underweight German Bunds and favor Eurozone equities over German equities.

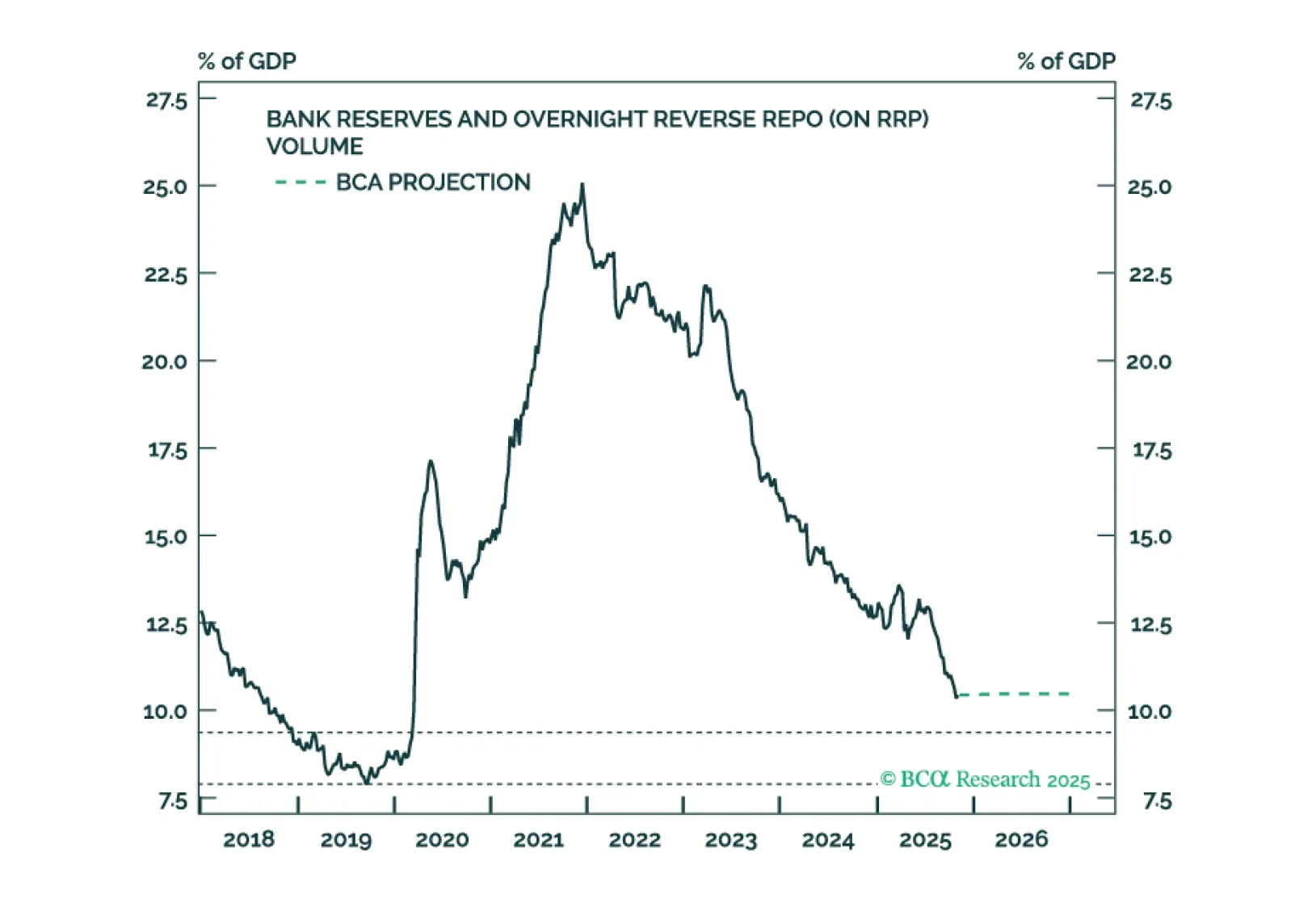

This Special Report outlines the Fed’s balance sheet strategy and the rationale behind it. We also provide updated projections for the major asset and liability line items on the Fed’s balance sheet.

Our Portfolio Allocation Summary for November 2025.

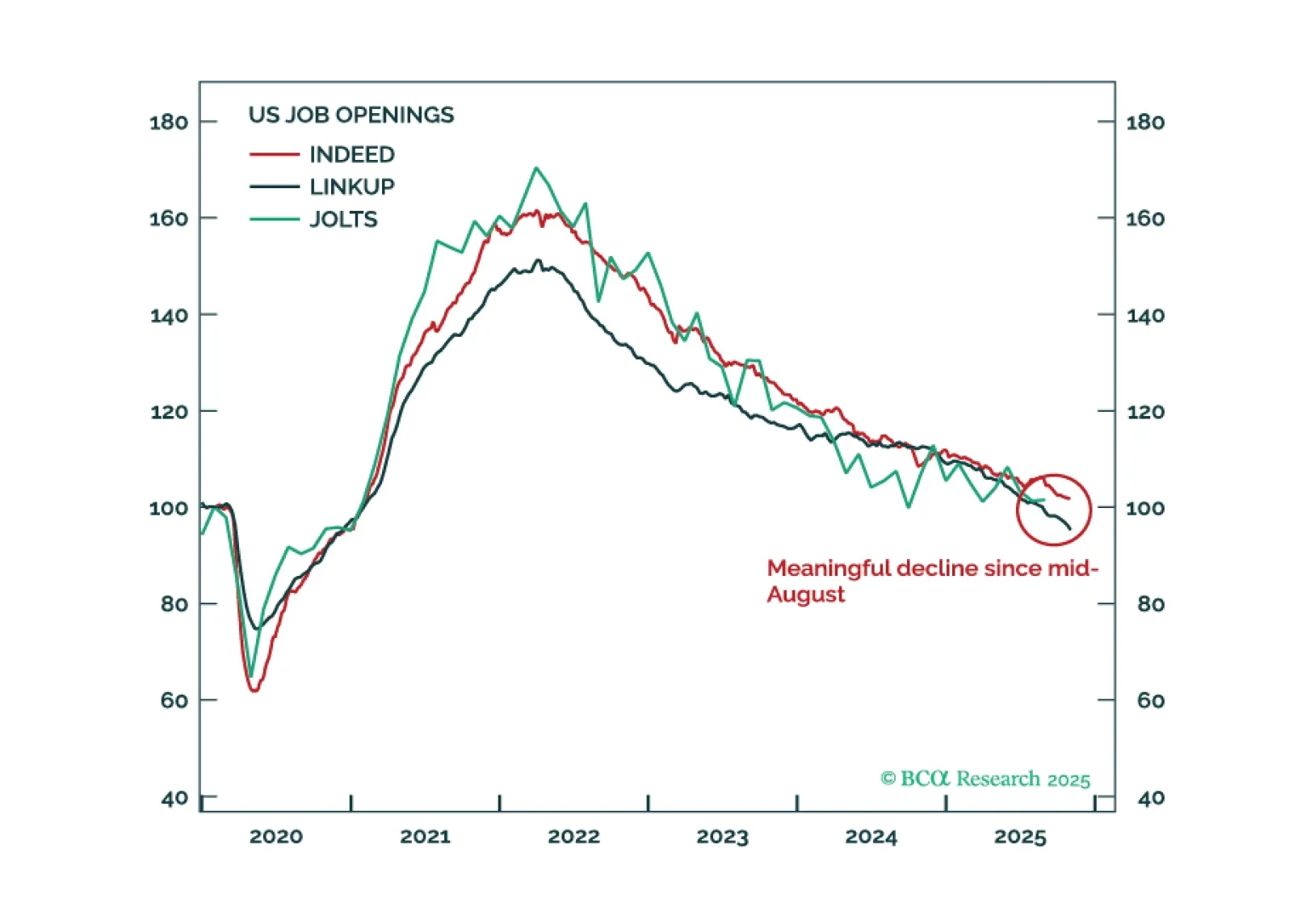

In the absence of official government data, investors are turning to alternative sources to gauge the direction of the US economy. Our analysis of this data suggests that the economy has continued to expand at a moderate pace over the past two months. If the Supreme Court were to strike down the tariffs, this would reduce the near-term odds of a recession while raising the odds of overheating.

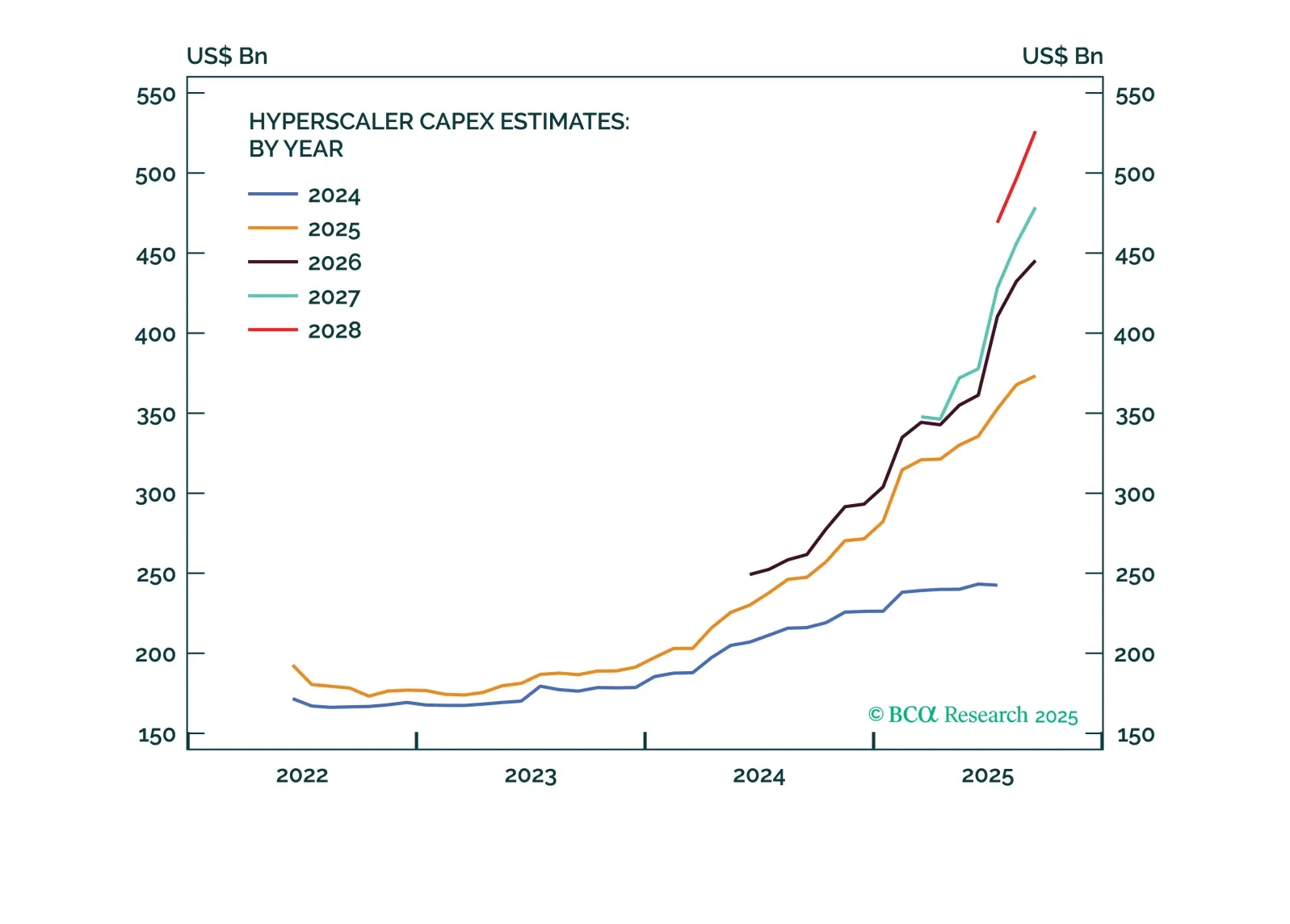

Fresh off a month of boning up on all things AI, we walk through a high-level Q&A discussing AI capex and how much the AI investing boom is really contributing to US growth.

MacroQuant is tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold and copper.

In Section II, Doug and Global Investment Strategy’s Miroslav Aradski consider the implications of the AI investment boom.