Economy

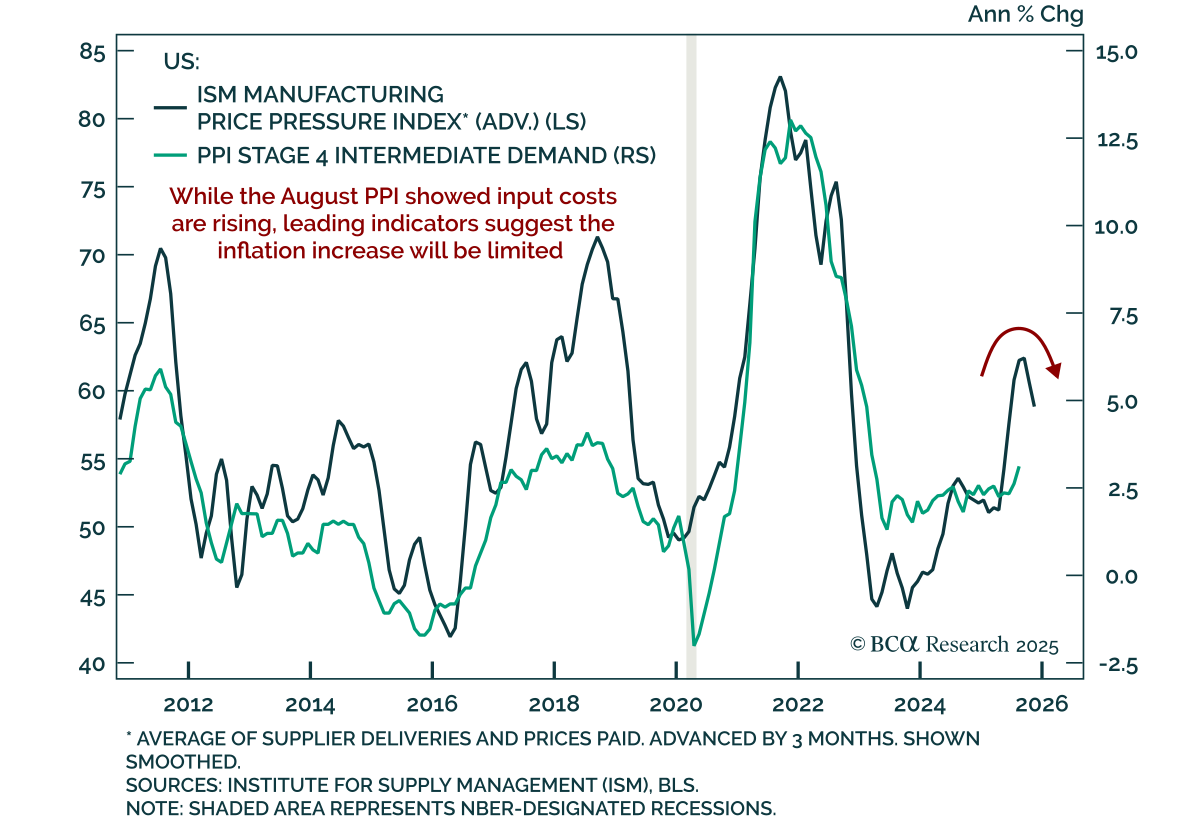

August PPI inflation cooled, reinforcing the case for Fed easing and long duration with steepeners. Headline PPI fell 0.1% m/m, bringing the annual rate down to 2.6% after July’s 0.7% gain. Core PPI (ex-food, energy, and trade) rose 0.3% m/m (2.8% y/y).…

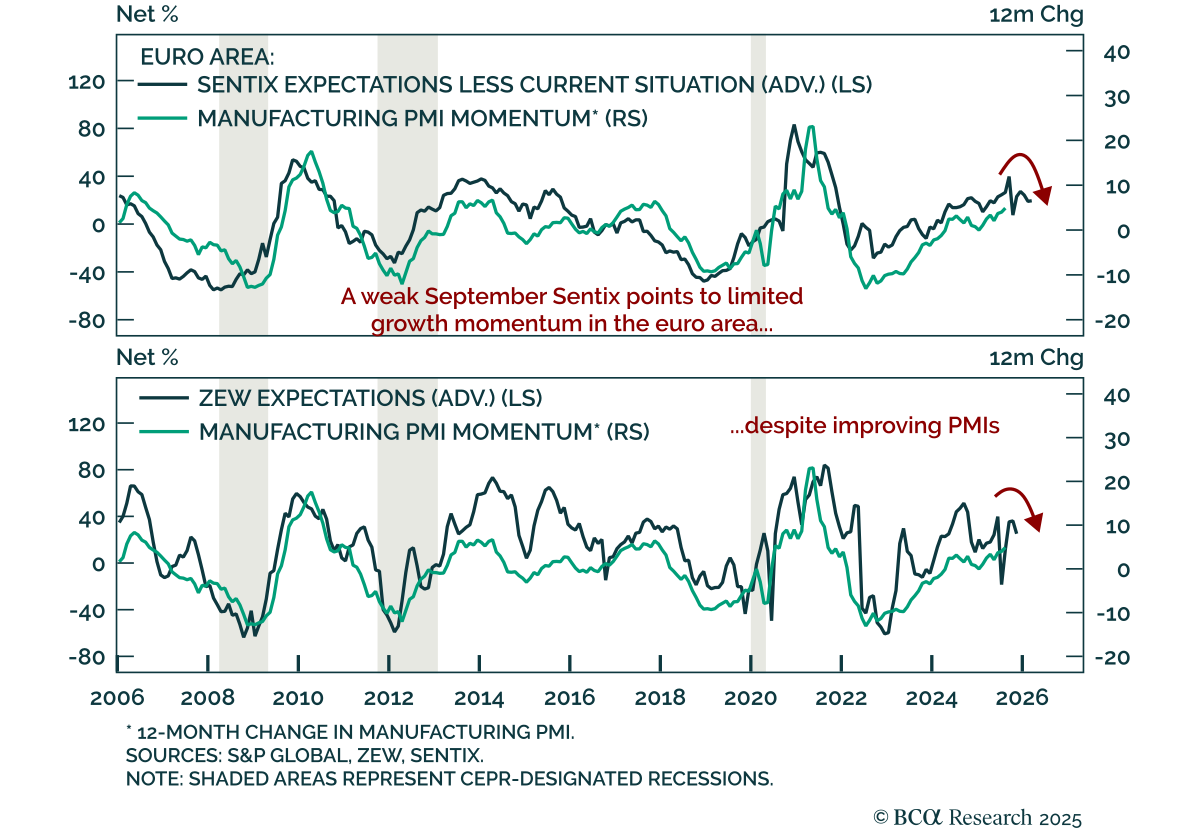

European sentiment continues to weaken, reinforcing the tactical case for US outperformance over Europe. The September Sentix Investor Confidence index fell to -9.2 from -3.7, defying expectations for an increase and signaling that August’s deterioration is…

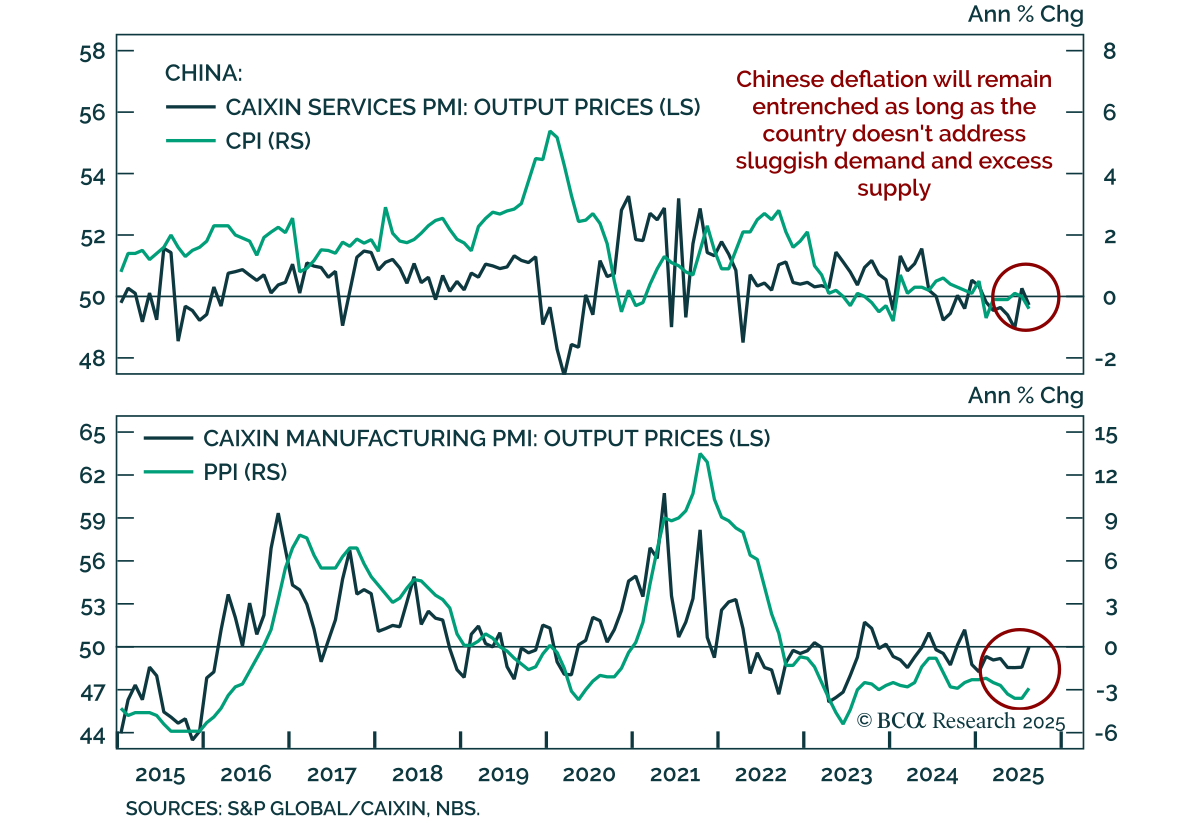

China’s August inflation data confirm entrenched deflation, reinforcing our overweight in onshore bonds and a tactical long in onshore small- and mid-caps versus large caps ahead of potential stimulus. Producer prices declined 2.9% y/y, easing from…

Core Europe’s industrial sector will relapse in the coming months due to US tariffs and a strong euro. Investors can play the imminent deflationary shock by being long Central European bonds. They should, however, hedge the currency risk vis-à-vis the euro.

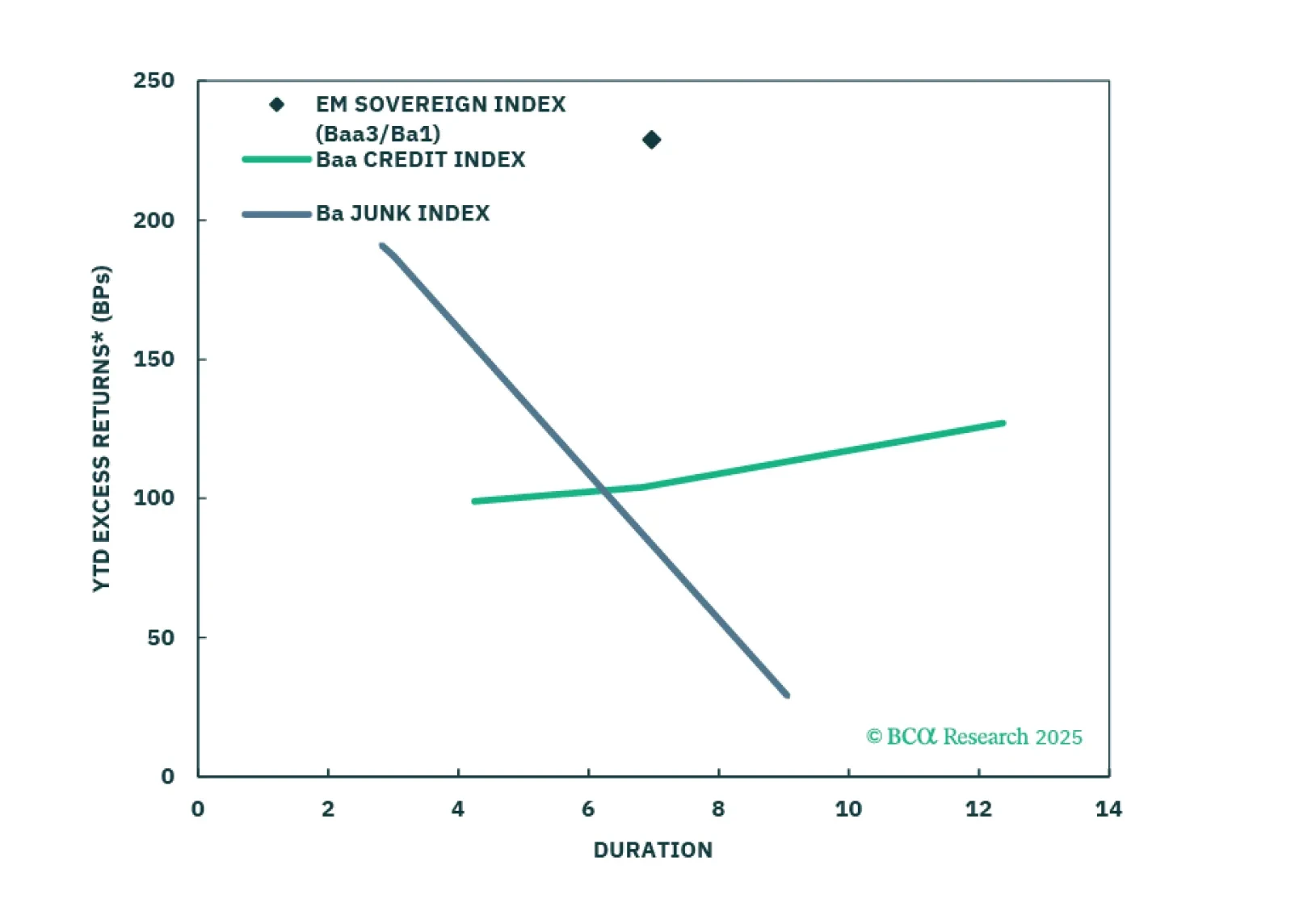

USD-denominated Emerging Market bonds have been outperforming US corporates for the past year. We don’t think the rally is exhausted yet.

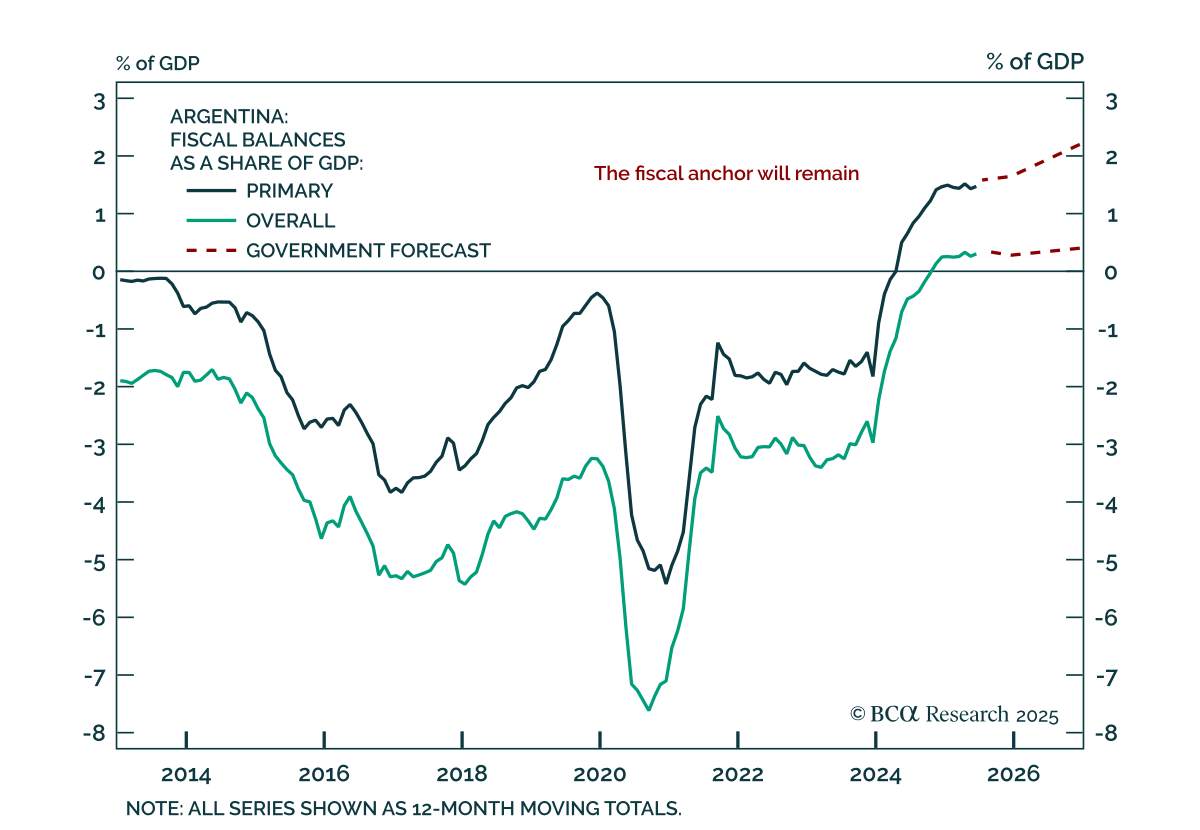

Despite the post-election selloff, investors should continue buying Argentine assets on weakness. Argentine markets sold off sharply after President Milei’s party suffered a crushing defeat in Sunday’s Buenos Aires election. Investors did not expect the…

The August NFIB survey shows a fragile US economy with disinflationary signals and weak employment, supporting our defensive stance. The Small Business Optimism Index rose to 100.8 from 100.3, a six-month high, though still below December 2024 levels. Much of…

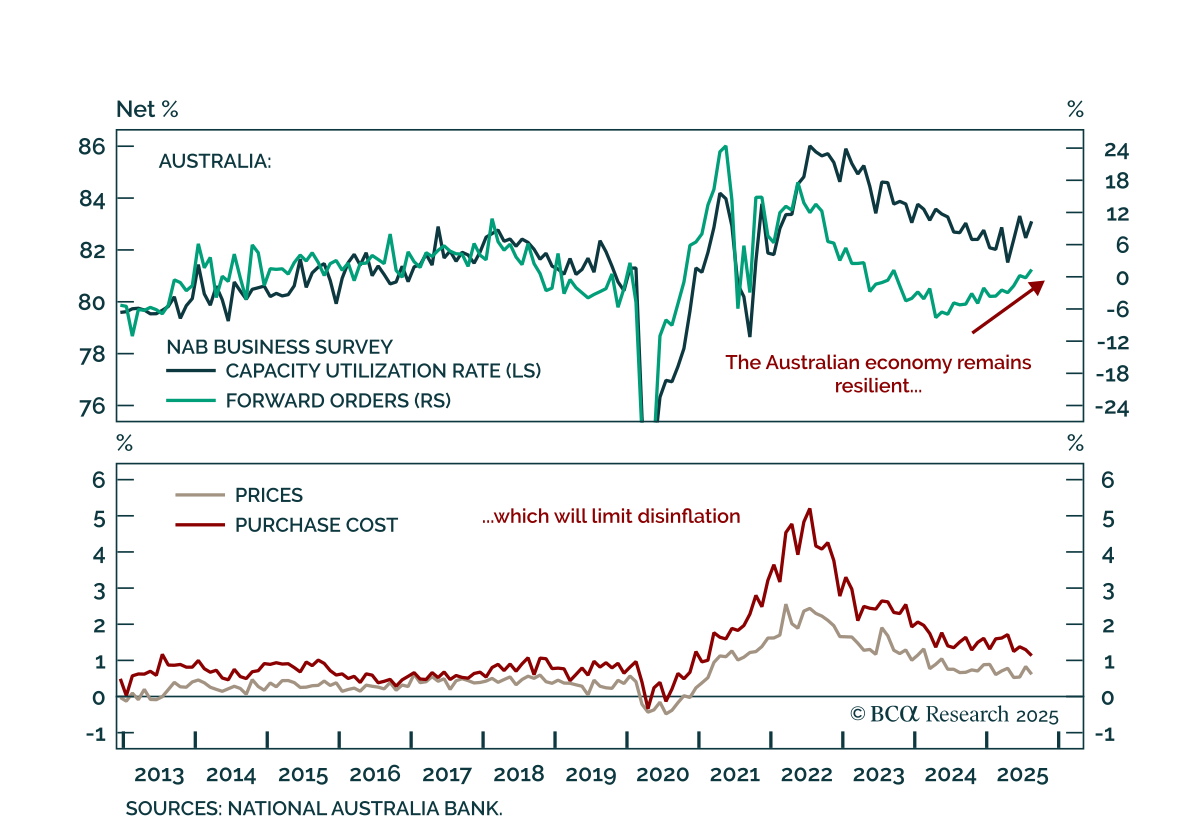

Australia’s NAB survey shows underlying resilience, reinforcing our underweight on ACGBs and the case for AUD flatteners vs. CAD steepeners. The August survey was mixed, with current conditions improving to 7 from 5, while business confidence softened to 4…

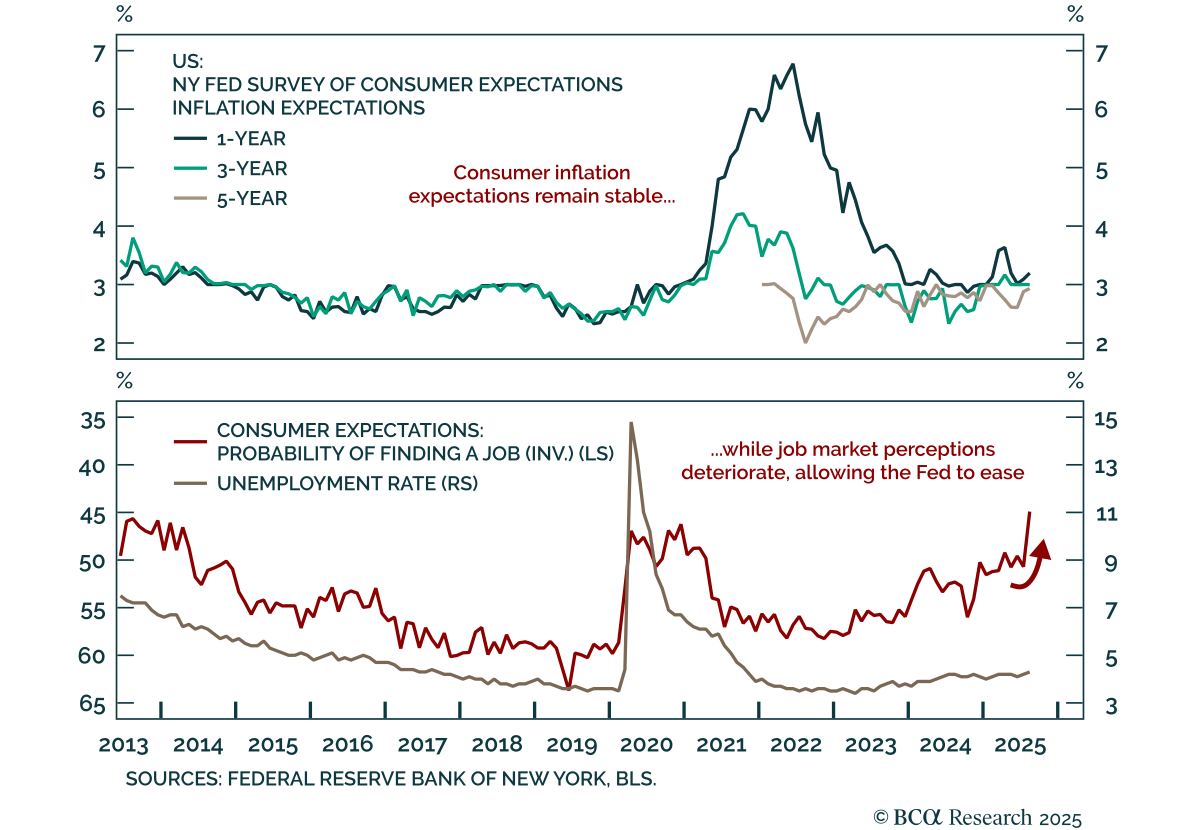

Stable long-term inflation expectations and weak labor perceptions support a defensive stance. The NY Fed Survey of Consumer Expectations showed 1-year inflation expectations ticking up to 3.2% in August, while the 3-year (3.0%) and 5-year (2.9%)…

Japan’s Eco Watchers Survey points to stabilization; JGBs remain unattractive and the yen’s near-term setup is less favorable versus USD. The August survey modestly beat expectations, with the current component rising to 46.7 from 45.2 and expectations…