Financial Markets

Dear client, We are launching a new type of Daily Insight titled “Cross-Asset Focus”, where we delve into the dynamics between multiple asset classes, tying them to the current macro and market regimes. The inaugural entry looks at the dynamics between…

According to the latest estimate of the output gap, the US economy still operates above potential. Continued overheating – a no-landing scenario – would cause a drastic re-pricing across markets which expect a near-perfect soft-landing. The output gap is…

US Treasury yields rose nearly 60 bps since their September lows, with the 10-year maturity recently reaching 4.2%. This move was a bear steepening, the front of the curve did not rise as much. Positive economic surprises mainly drove this spike, but the…

Our Emerging Markets Strategy team sees evidence of a “Trump trade” across markets, as the dollar strengthens, Treasury yields jump, and US small caps try to break out. However, the tactical and cyclical outcomes differ. While Trump 2.0 points to tariffs…

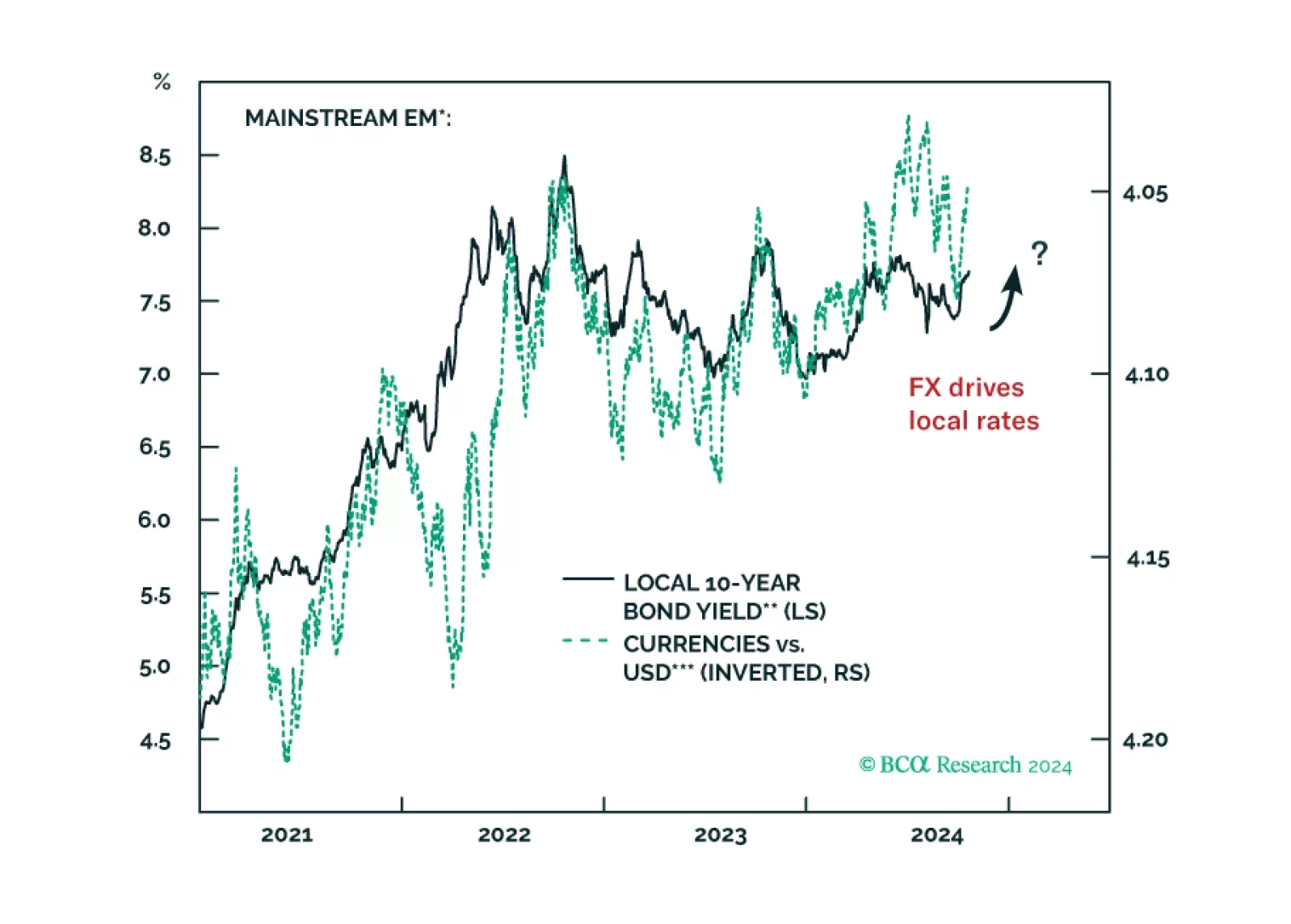

As the odds of a Trump victory increase, there are indications that the “Trump trade” has commenced in global financial markets, with negative short-term implications for EM. In short, the US dollar will strengthen, and US bond yields will rise in the lead-up to and after the election if Trump wins. In response, EM countries’ currencies will depreciate, and their fixed-income and equity markets will suffer over the coming months.

The recent slump in globally- and tech-sensitive East Asian trade shows no respite, with advanced October Korean exports and September Taiwanese export orders data disappointing. Korean exports for the first 20 days of October dropped 2.9% year-over-year…

Since the August selloff in risk assets, the main cross-asset driver was the shift from inflation worries to growth worries. Some of that price action has reversed, as TIPS breakeven inflation rates swiftly rebounded since early September. The 2-year…

Our US Equity Strategy colleagues expect Q3 earnings to be strong enough to fuel the soft-landing narrative. Analysts expect S&P 500 earnings growth to be 4.0% year-over-year, with sales growth of 4.0% too. Yet, with average surprises of 5.6% for…

The war in Ukraine has ended in late 2022… for markets at least. This is the conclusion from our GeoMacro team’s latest report, which aims to dispel five crucial myths surrounding the conflict. The myths are the following: The Ukraine-Russia War Will…

The ECB cut interest rates by 25 bps for the third time this year, lowering the deposit facility rate from 3.5% to 3.25%. While the ECB is avoiding explicitly committing to a path for policy, President Lagarde’s repeated statement that the disinflationary…