Inflation/Deflation

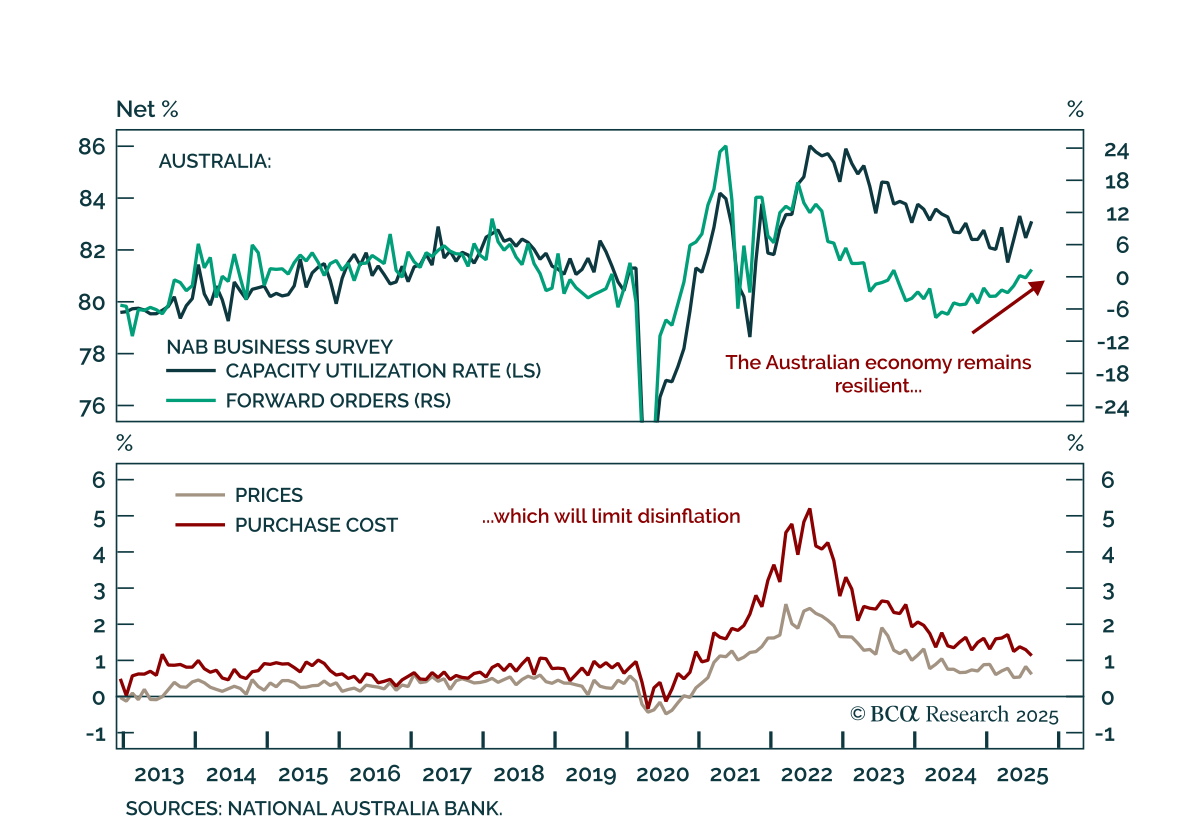

Australia’s NAB survey shows underlying resilience, reinforcing our underweight on ACGBs and the case for AUD flatteners vs. CAD steepeners. The August survey was mixed, with current conditions improving to 7 from 5, while business confidence softened to 4…

The August NFIB survey shows a fragile US economy with disinflationary signals and weak employment, supporting our defensive stance. The Small Business Optimism Index rose to 100.8 from 100.3, a six-month high, though still below December 2024 levels. Much of…

Japan’s Eco Watchers Survey points to stabilization; JGBs remain unattractive and the yen’s near-term setup is less favorable versus USD. The August survey modestly beat expectations, with the current component rising to 46.7 from 45.2 and expectations…

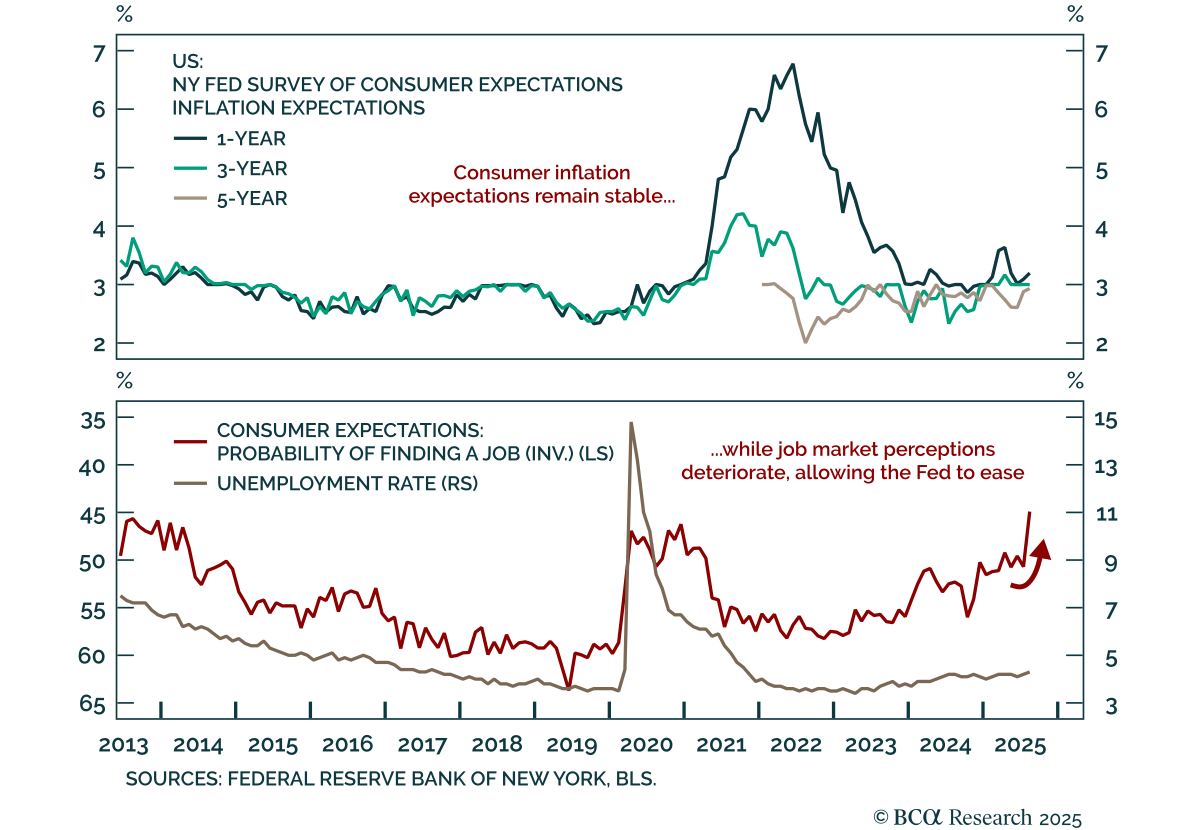

Stable long-term inflation expectations and weak labor perceptions support a defensive stance. The NY Fed Survey of Consumer Expectations showed 1-year inflation expectations ticking up to 3.2% in August, while the 3-year (3.0%) and 5-year (2.9%)…

Inflation expectations in the US remain reasonably well anchored and there are few signs of a brewing wage-price spiral. Thus, the near-term risks to growth outweigh the risks of higher inflation. Looking beyond the next year or two, however, we are worried about stagflation.

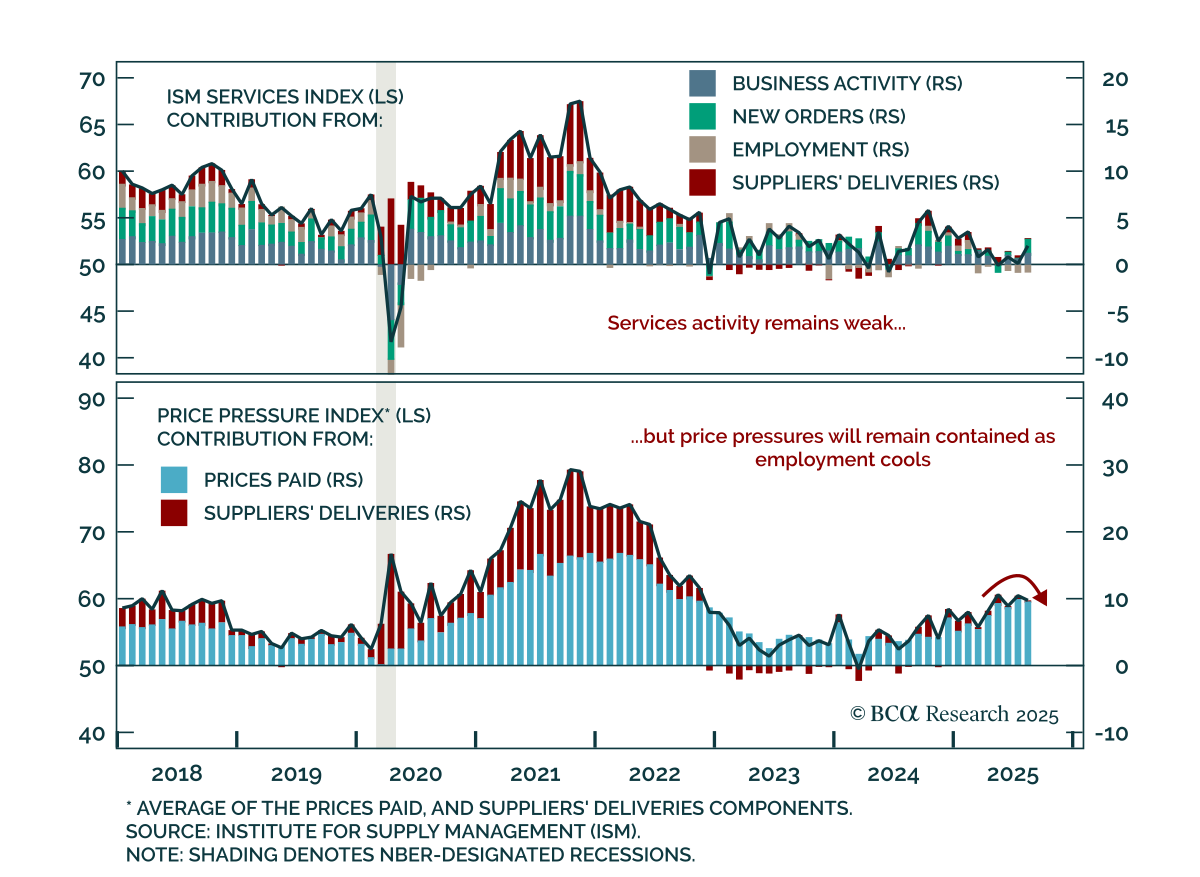

August ISM Services beat expectations, but employment weakness highlights fragile momentum. The index rose to 52.0 from 50.1, driven by business activity and new orders. However, the employment component stayed in contraction at 46.5. Inflation signals…

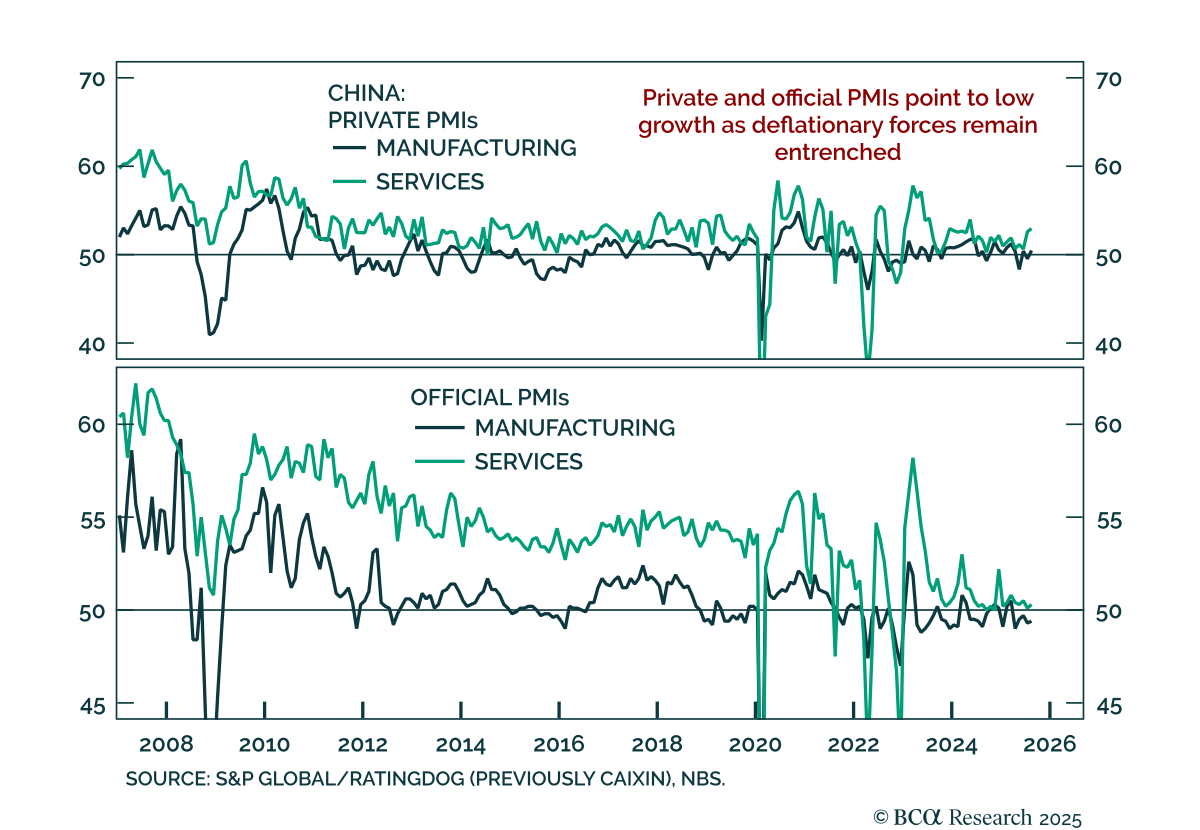

China’s August PMIs improved, but underlying data point to persistent weakness and limited momentum. The official NBS composite rose to 50.5 from 50.2, with manufacturing still in contraction at 49.4 and services edging higher to 50.3. Private PMIs showed…

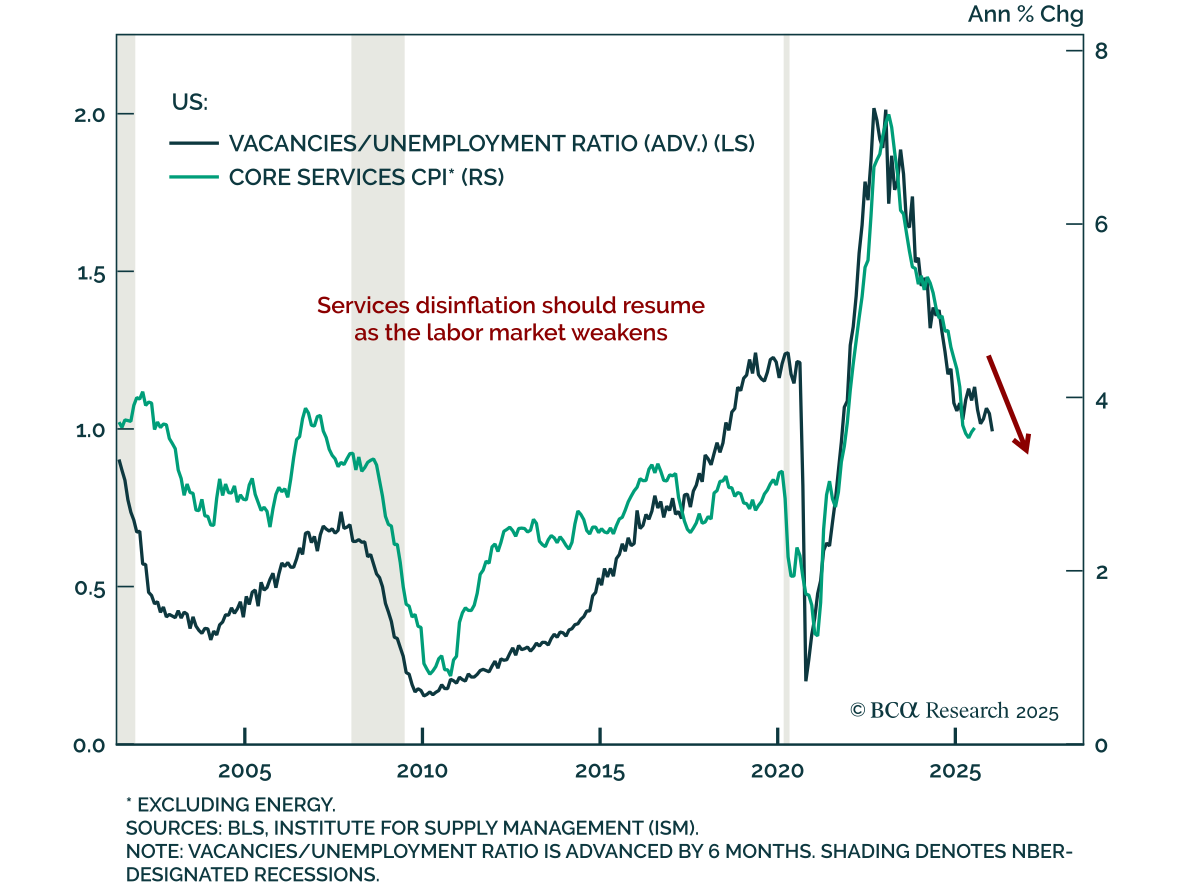

US job openings fell to a 10-month low in July, underscoring continued labor market weakening. Openings declined to 7.18m from 7.36m. The decline was led by non-cyclical sectors such as education and health services, which had recently been drivers of…

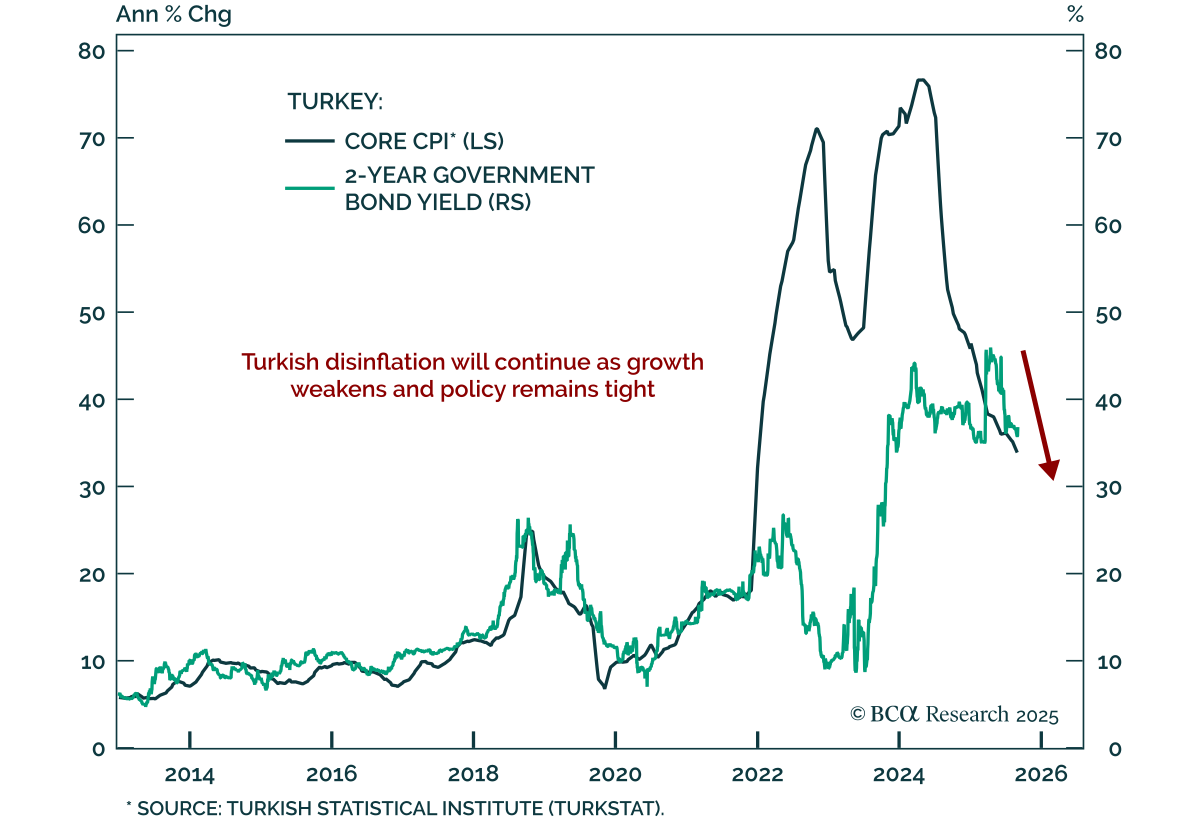

Turkey’s disinflation trend remains intact, supporting a bullish case for short-term bonds. Headline inflation eased to 33% y/y in August from 33.5% in July. Our Emerging Markets strategists expect further slowing as monetary and fiscal policy stay tight.…

Our Portfolio Allocation Summary for September 2025.