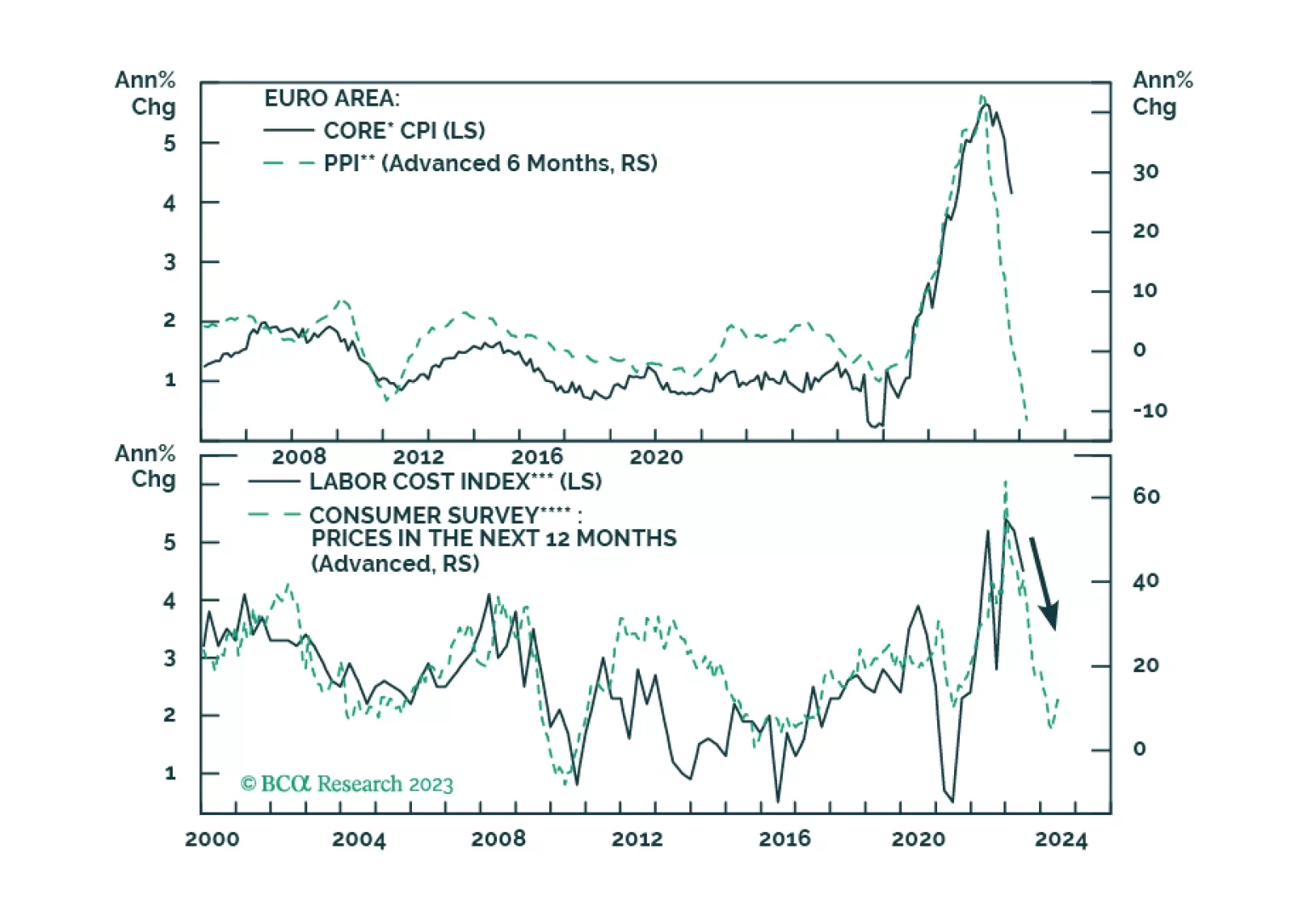

Inflation/Deflation

The Eurozone’s inflation will continue to slow over the coming months. While this trend will help Bund prices, will it boost the appeal of European equities?

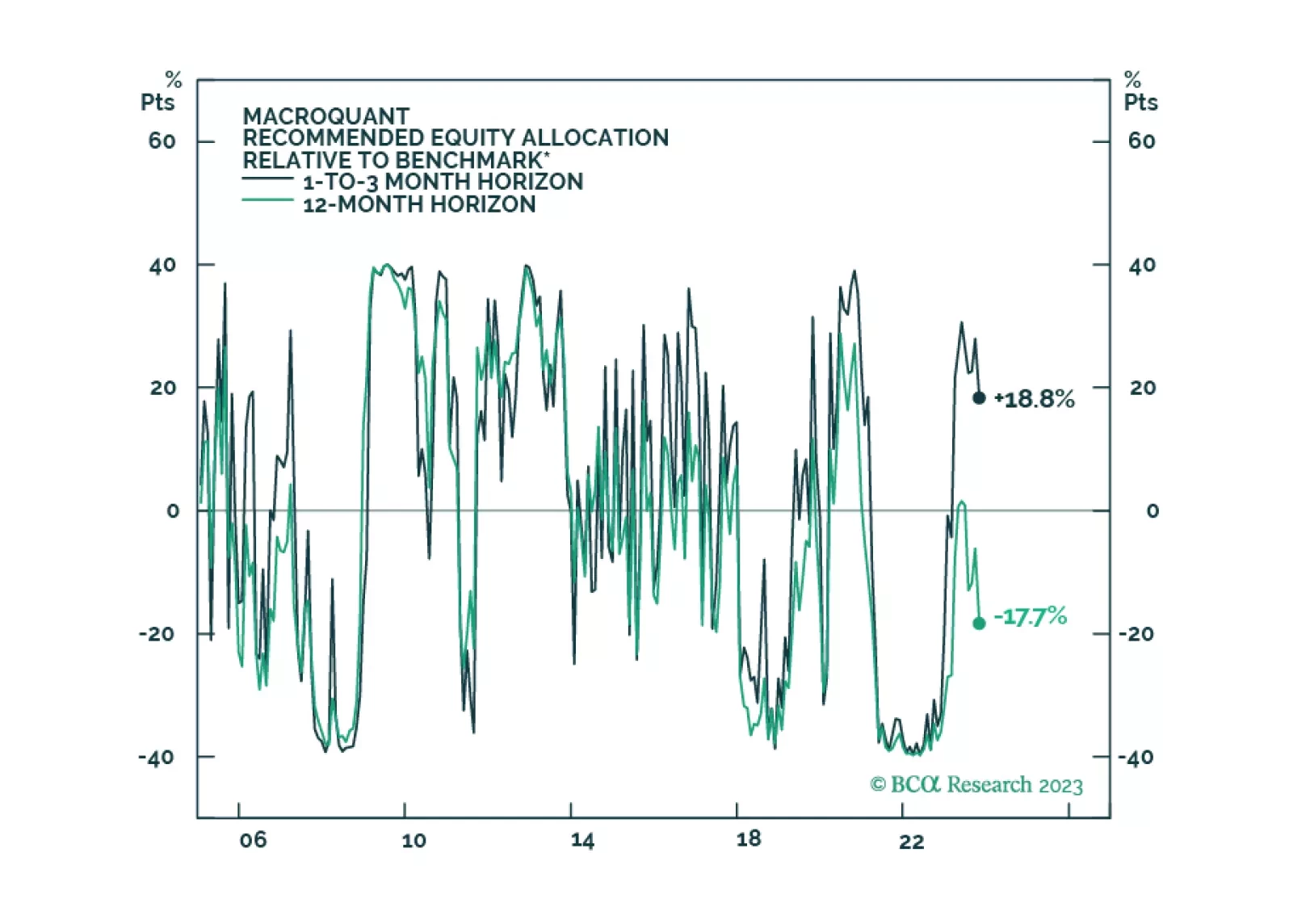

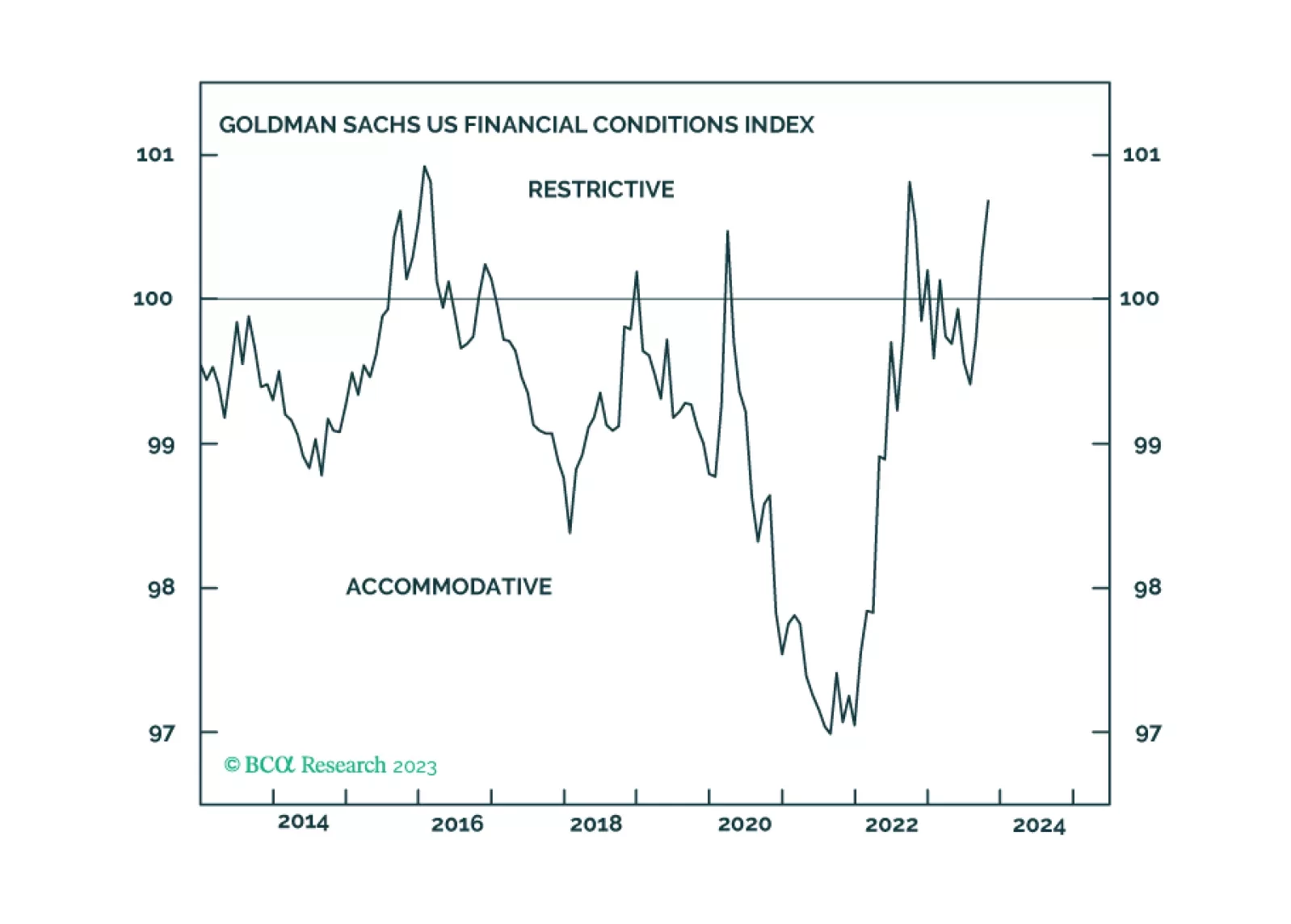

We consider several uncertainties in this week’s report, from the interest rate outlook to the source of the mountain of cash households have amassed since the pandemic began. We have not adjusted our tactical asset-allocation recommendations but will do so soon to align with the defensive cast of our cyclical recommendations.

We are approaching another phase transition from boom to bust. Stocks should rally into year-end, but investors should look to reduce equity exposure early next year while increasing bond exposure.

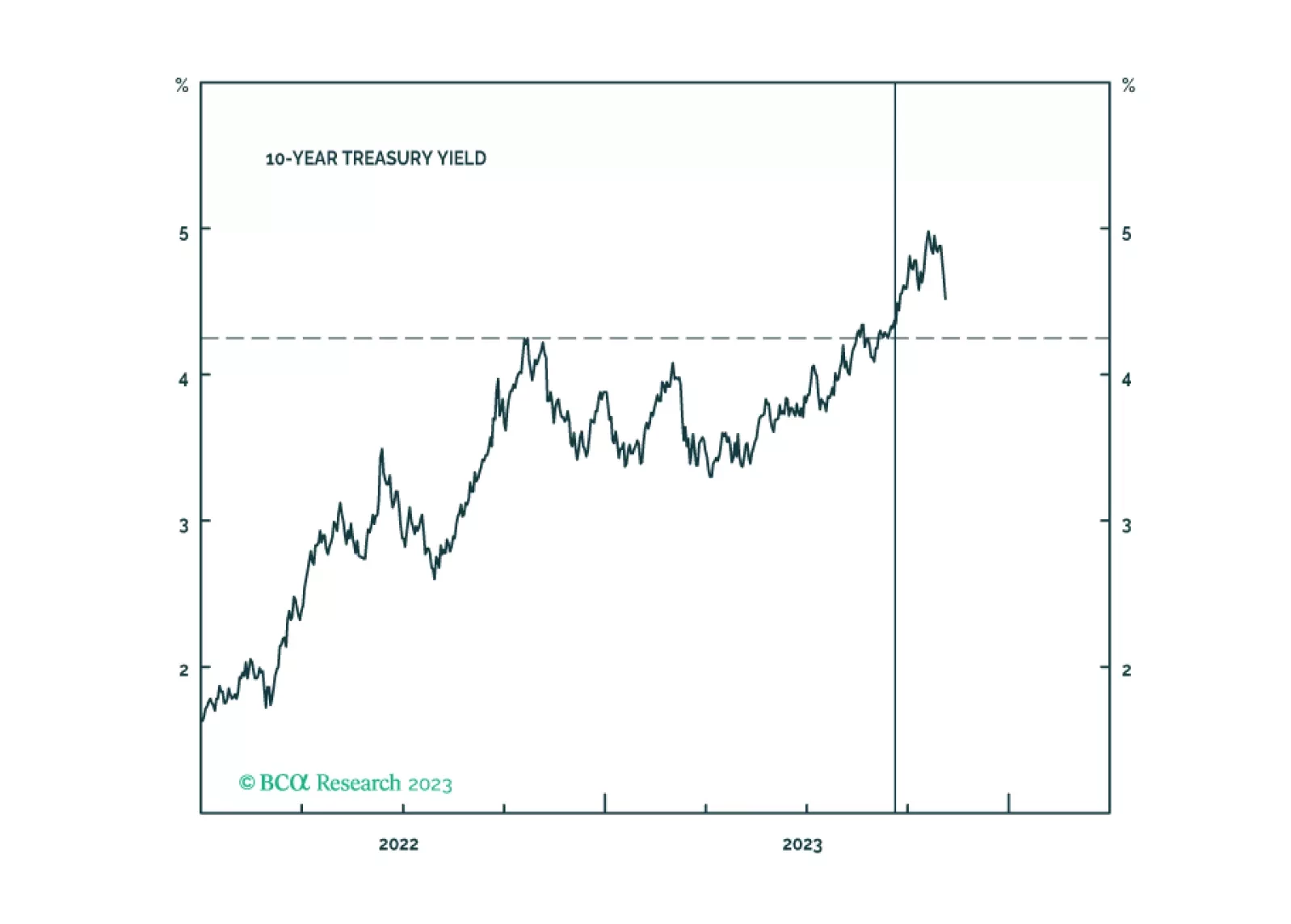

Our reaction to today’s FOMC meeting and the Treasury’s Quarterly Refunding Announcement.