Manufacturing

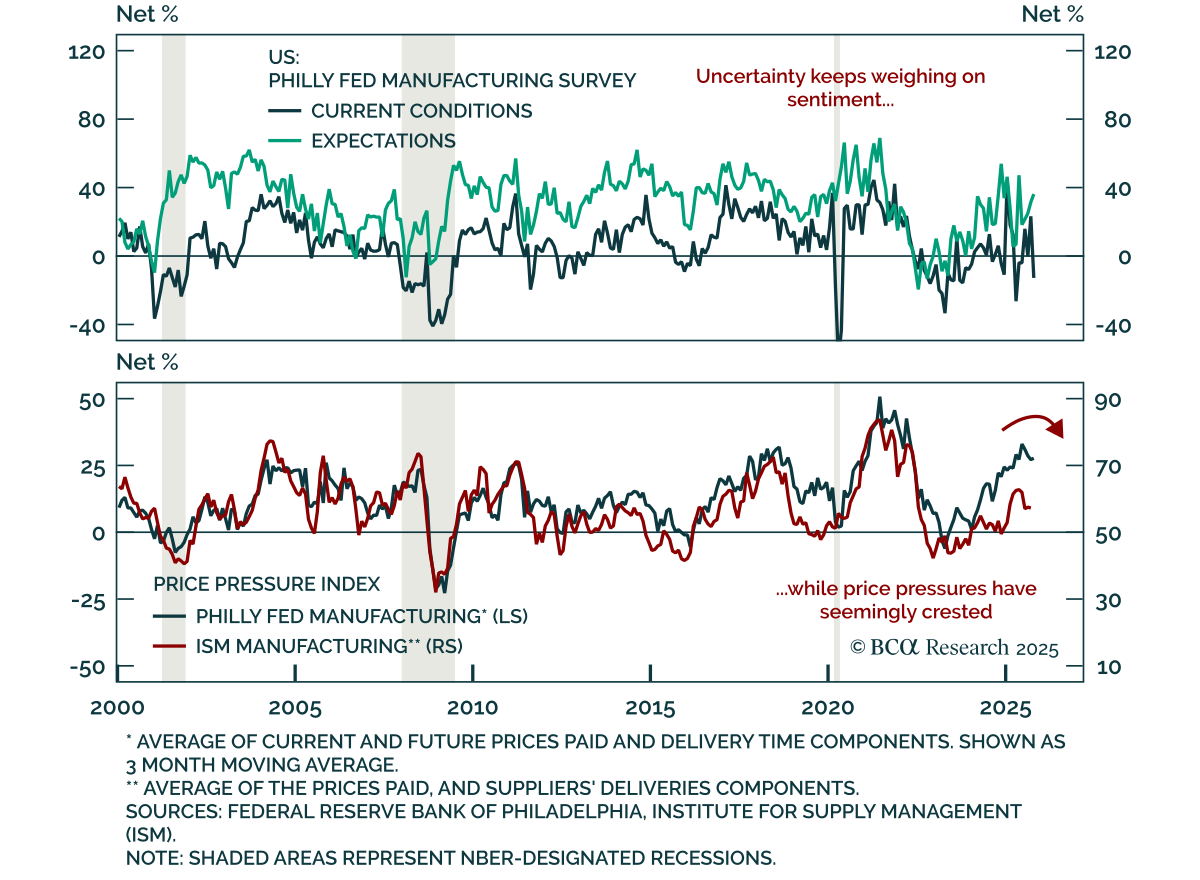

The October Philadelphia Fed manufacturing survey was mixed, showing weak headline data but steadier underlying components. The headline index fell to -12.8 from 23.2, the lowest level since April 2025. Underlying details were not as dire: shipments moderated…

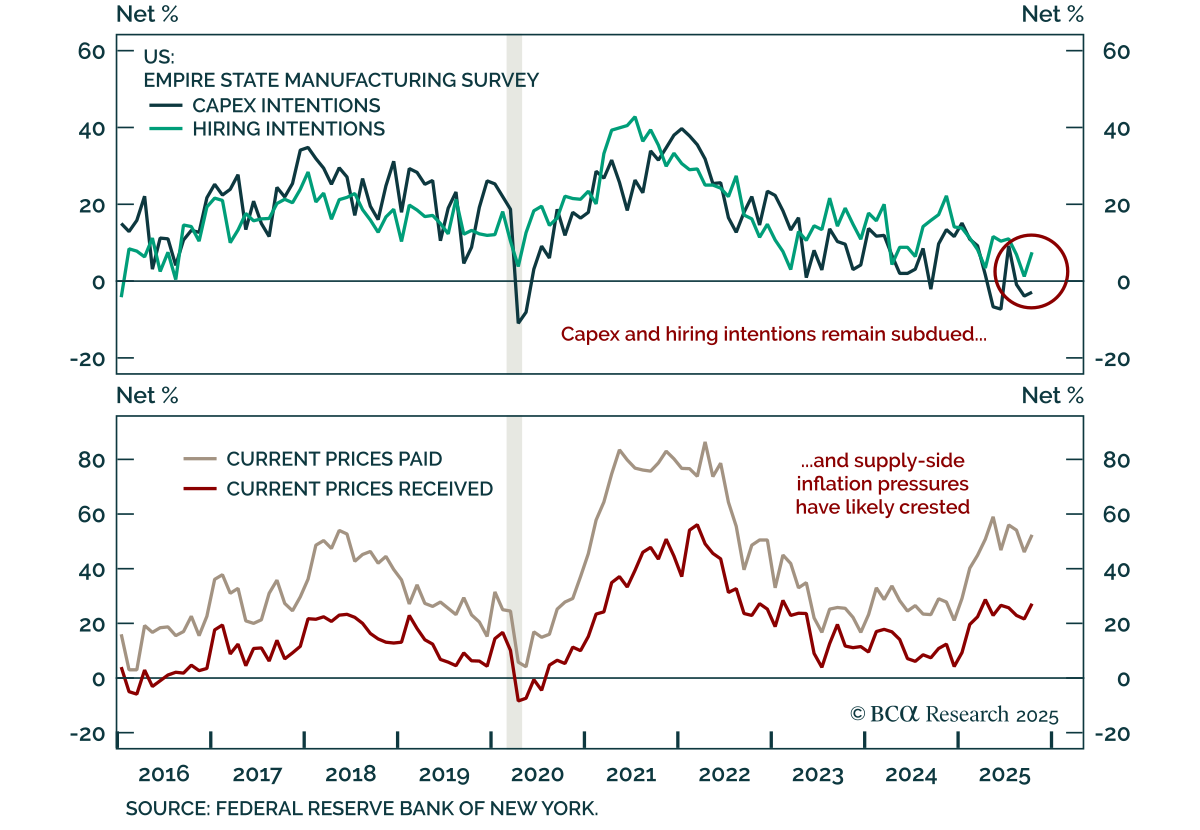

The October Empire Manufacturing survey beat estimates, but weak investment and hiring intentions temper its positive signal. The index rose to 10.7 from -8.7, indicating modest activity growth. New orders ticked up, and shipments increased after plunging…

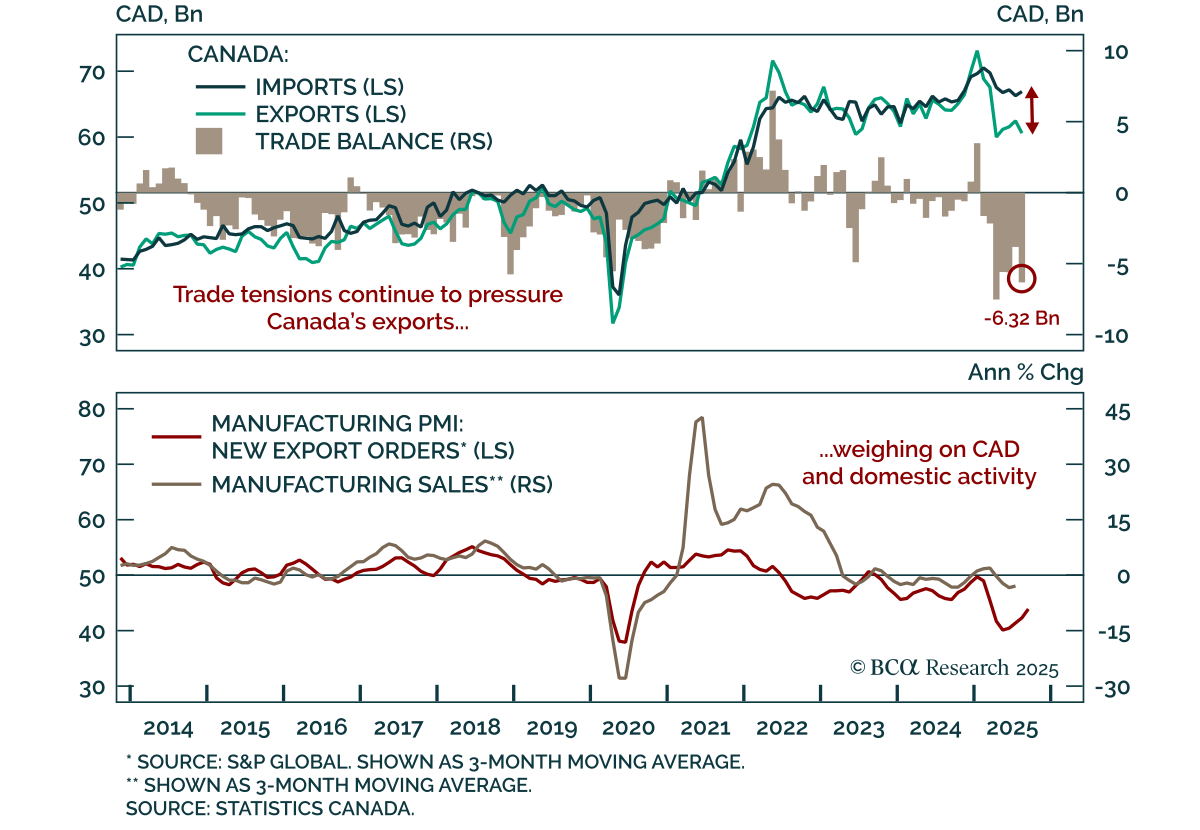

Trade concerns continue to weigh on Canada, reinforcing a cautious macro outlook with near term downside for bond yields and the CAD, though the currency selloff is getting stretched and could soon present an attractive entry point.Canada’s goods trade…

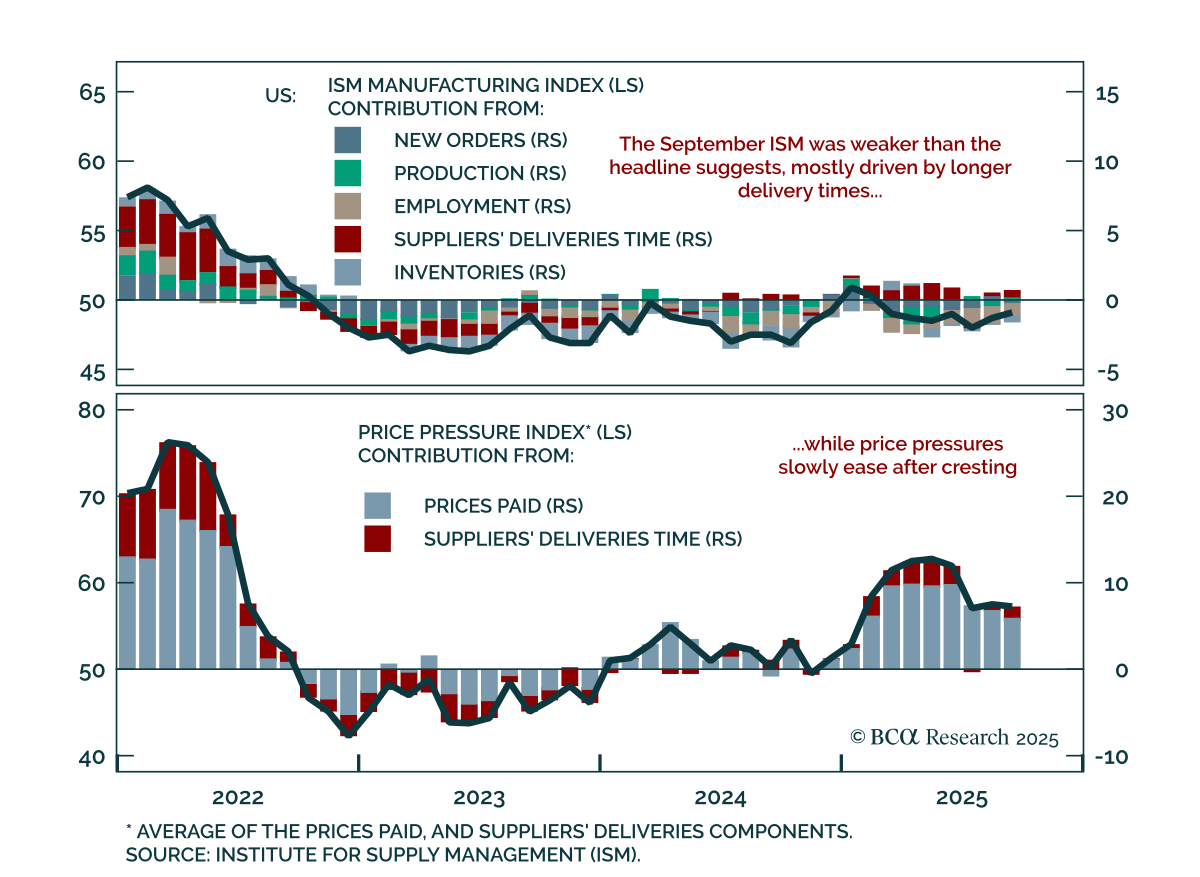

The September ISM Manufacturing index beat expectations at 49.1, but details confirm weak momentum and tariff-driven pressures. The headline improved from 48.7 in August, its second consecutive monthly gain, but the uptick came mainly from longer supplier…

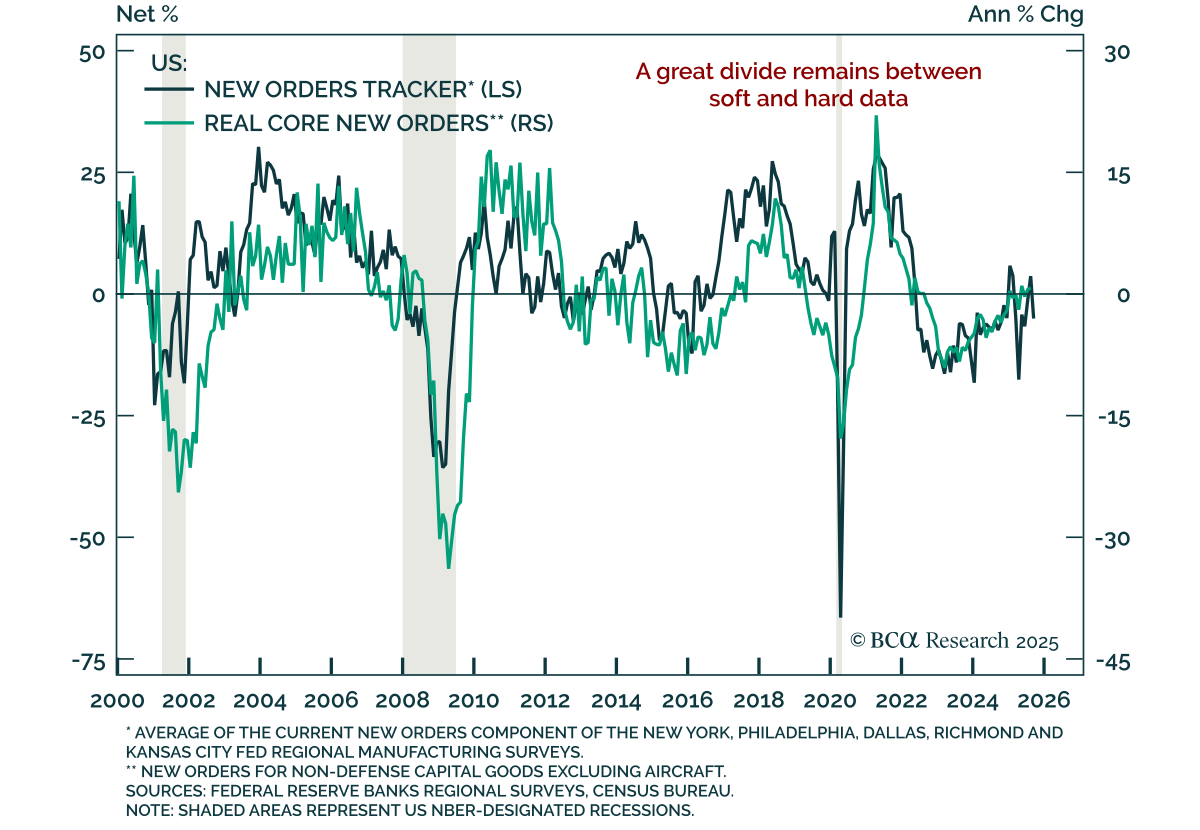

August core durable goods orders beat estimates, but weak shipments and survey data reinforce our modestly defensive stance. Core orders rose 0.6% m/m against expectations of a modest decline, though they decelerated from July’s downwardly revised 0.8% gain.…

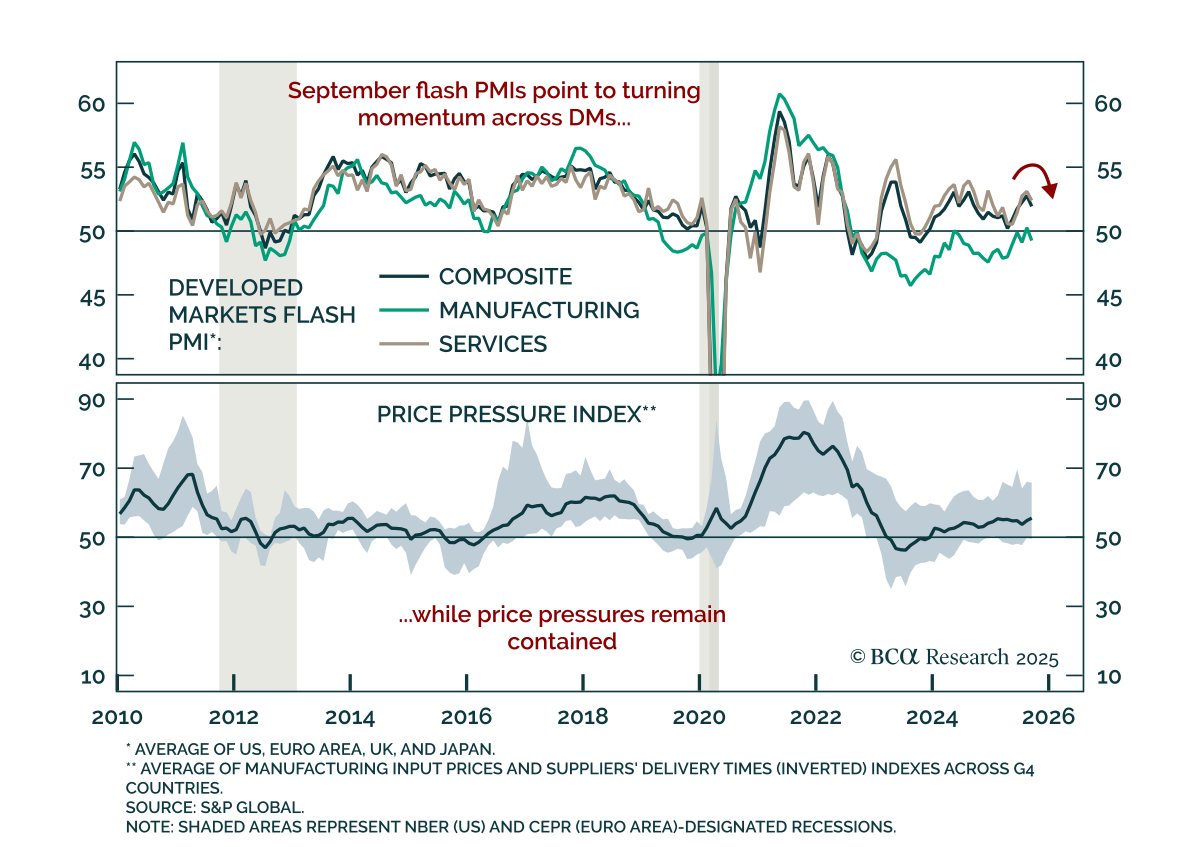

September flash PMIs show slowing global momentum, reinforcing US equity outperformance and underweights in industrial metals. The US composite slipped to 53.6 from 54.6, led by weaker manufacturing. Europe was mixed: Services strengthened modestly but…

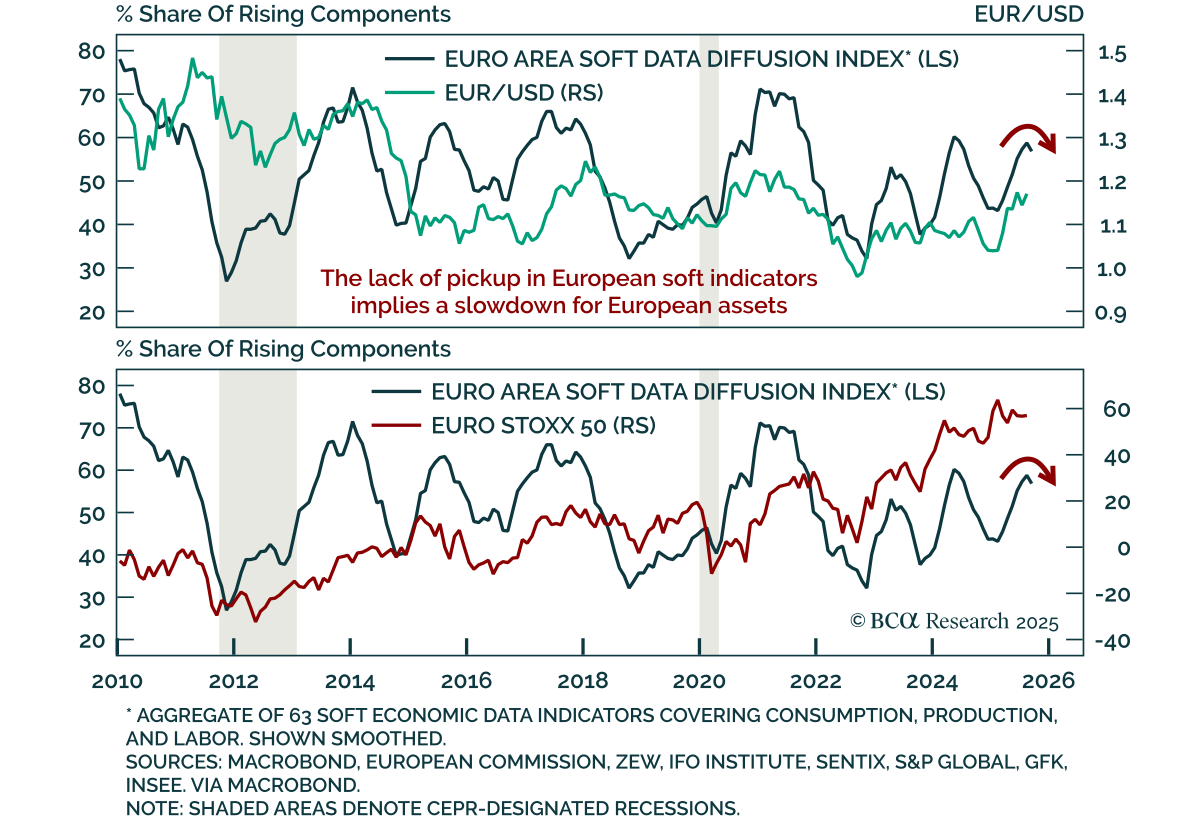

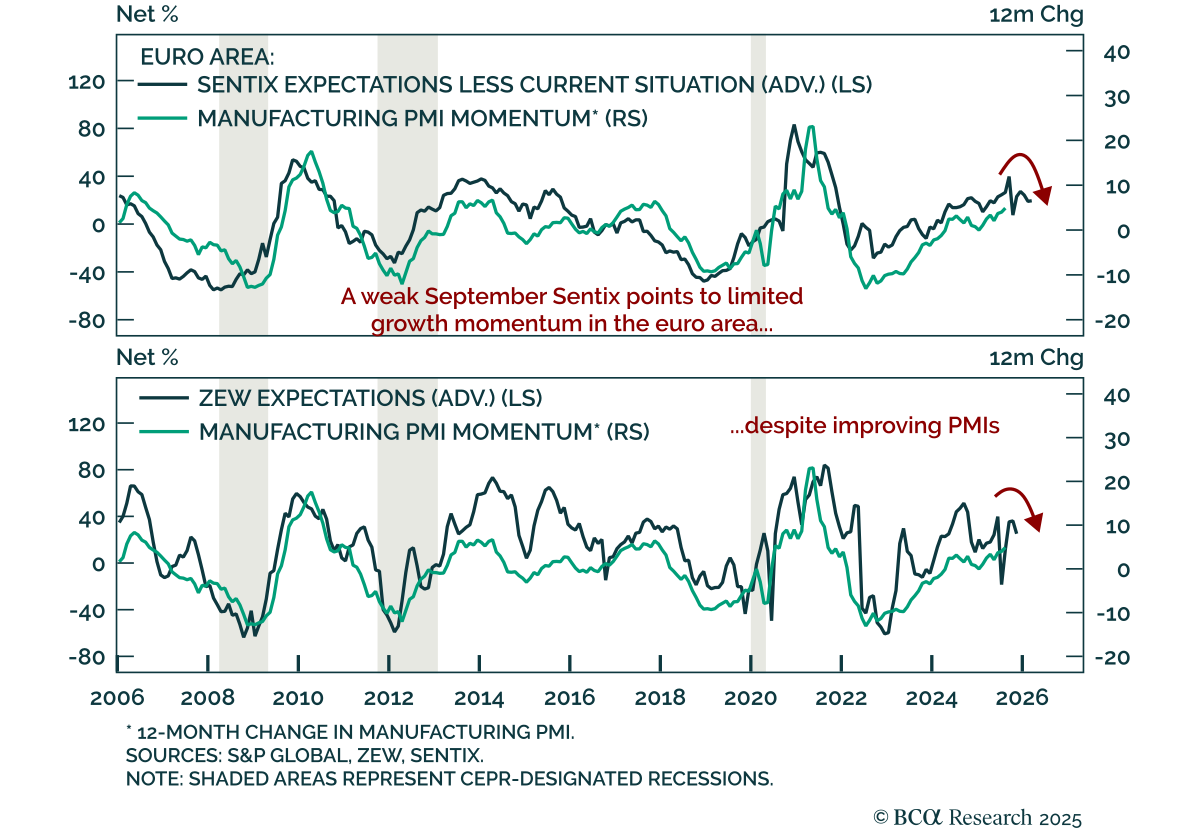

European sentiment indicators weakened again in August and September, reinforcing tactical US outperformance. While the September flash consumer confidence print beat expectations, it is still sluggish. Surveys such as Sentix and ZEW, both leading indicators…

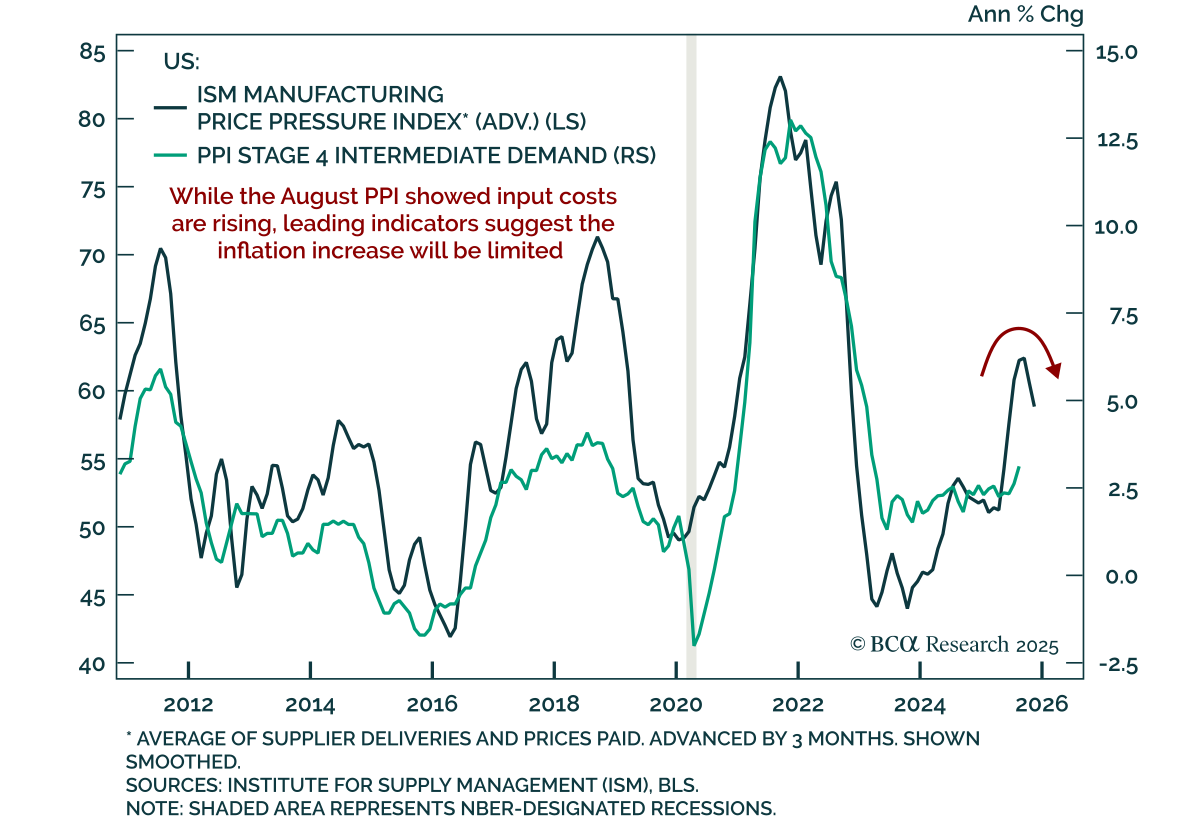

August PPI inflation cooled, reinforcing the case for Fed easing and long duration with steepeners. Headline PPI fell 0.1% m/m, bringing the annual rate down to 2.6% after July’s 0.7% gain. Core PPI (ex-food, energy, and trade) rose 0.3% m/m (2.8% y/y).…

European sentiment continues to weaken, reinforcing the tactical case for US outperformance over Europe. The September Sentix Investor Confidence index fell to -9.2 from -3.7, defying expectations for an increase and signaling that August’s deterioration is…

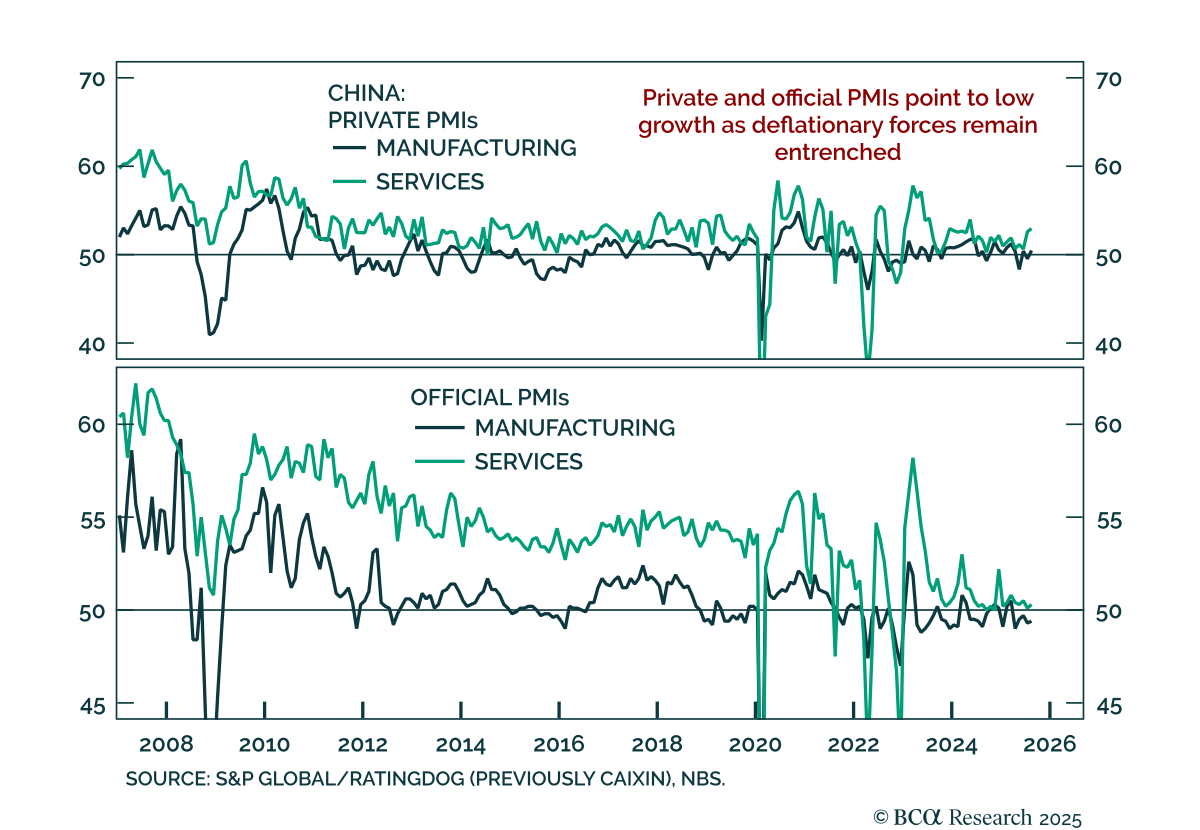

China’s August PMIs improved, but underlying data point to persistent weakness and limited momentum. The official NBS composite rose to 50.5 from 50.2, with manufacturing still in contraction at 49.4 and services edging higher to 50.3. Private PMIs showed…