Monetary

Canadian headline inflation rose 1.6% year-over-year in September, lower than the expected 1.8% and down from 2.0% in August. This was also its slowest pace since February 2021. The decrease was mainly driven by gasoline prices, leaving the core (ex. food and…

Economic expectations for the both Germany and the Eurozone ticked up in October and surprised positively for the first time since they collapsed this summer. The assessment of current conditions however worsened, going from -84.5 to -86.9. The expectations…

The UK August employment report was in line with recent data showing an economy humming at a decent pace. The unemployment rate decreased 0.1pp to 4% after peaking at 4.4% before the summer. The BoE will look kindly to the continued deceleration in wage…

Our China and Emerging Market strategy teams analyzed this weekend press conference by the China’s Ministry of Finance (MoF), that provided additional details on the recently announced fiscal stimulus plan. Our colleagues view the recent announcement as…

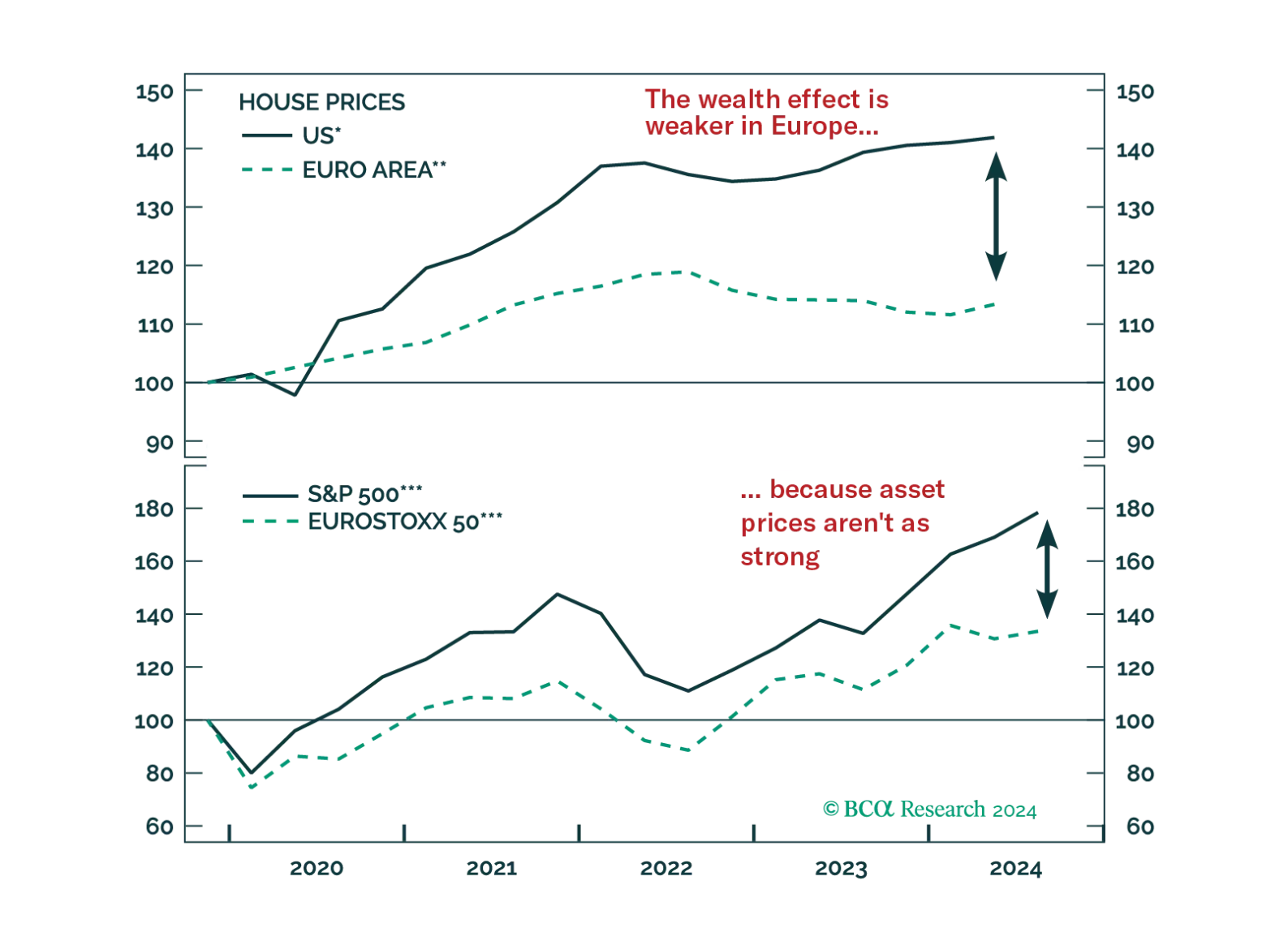

This week, we cover the main questions we fielded during our latest client trip in Europe. Among the many topics broached are Europe’s recession odds, the impact of China’s stimulus, and the outlook for European markets.

Rising stock prices and improving economic data have us re-examining our bearish thesis, but we still see deterioration in leading labor market indicators and expect it will eventually culminate in a recession. We reiterate our defensive investment recommendations.

The Bank of Japan’s Economy Watchers Survey – a gauge of sentiment among business owners – disappointed in September. The Current Conditions and the Outlook indices deteriorated from 49.0 to 47.8 and from 50.3 to 49.7, below expectations of an…

The Sentix Investor Confidence index unexpectedly improved in October from -15.4 to -13.8. A notable improvement in Expectations (from -8.0 to -3.8) drove the overall index higher, while the Current Situation subcomponent declined for a fourth consecutive…

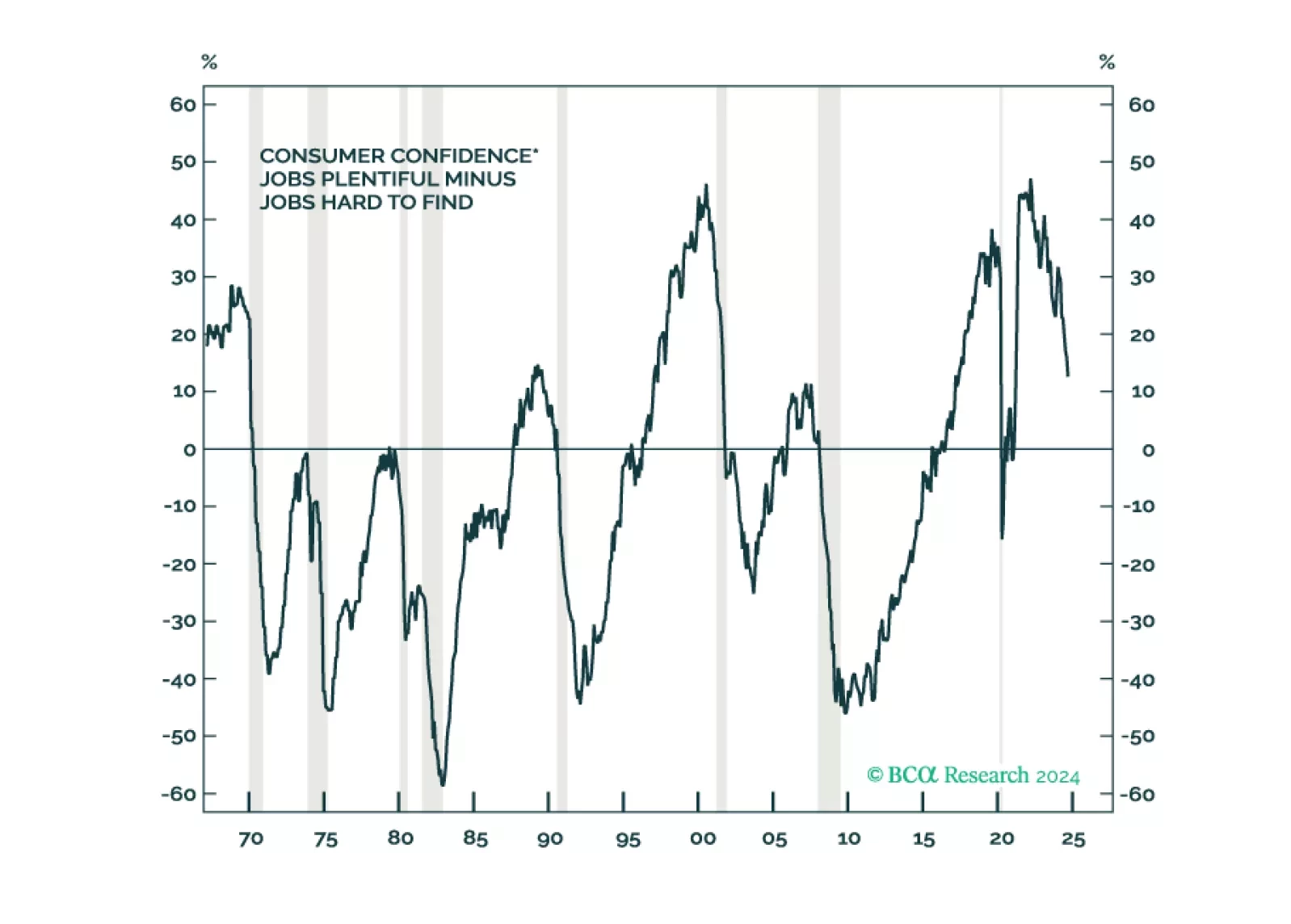

The NFIB Small Business Optimism index was mostly flat in September, ticking a mere 0.3 points higher to 91.5 in September, below expectations of a more meaningful improvement to 92.0. The NFIB Small Business Optimism has oscillated in a tight range since…

The month of October ahead of a US general election tends to be a volatile month with negative outcome for equities. As such, it is prudent to remain on the sidelines until after the election.