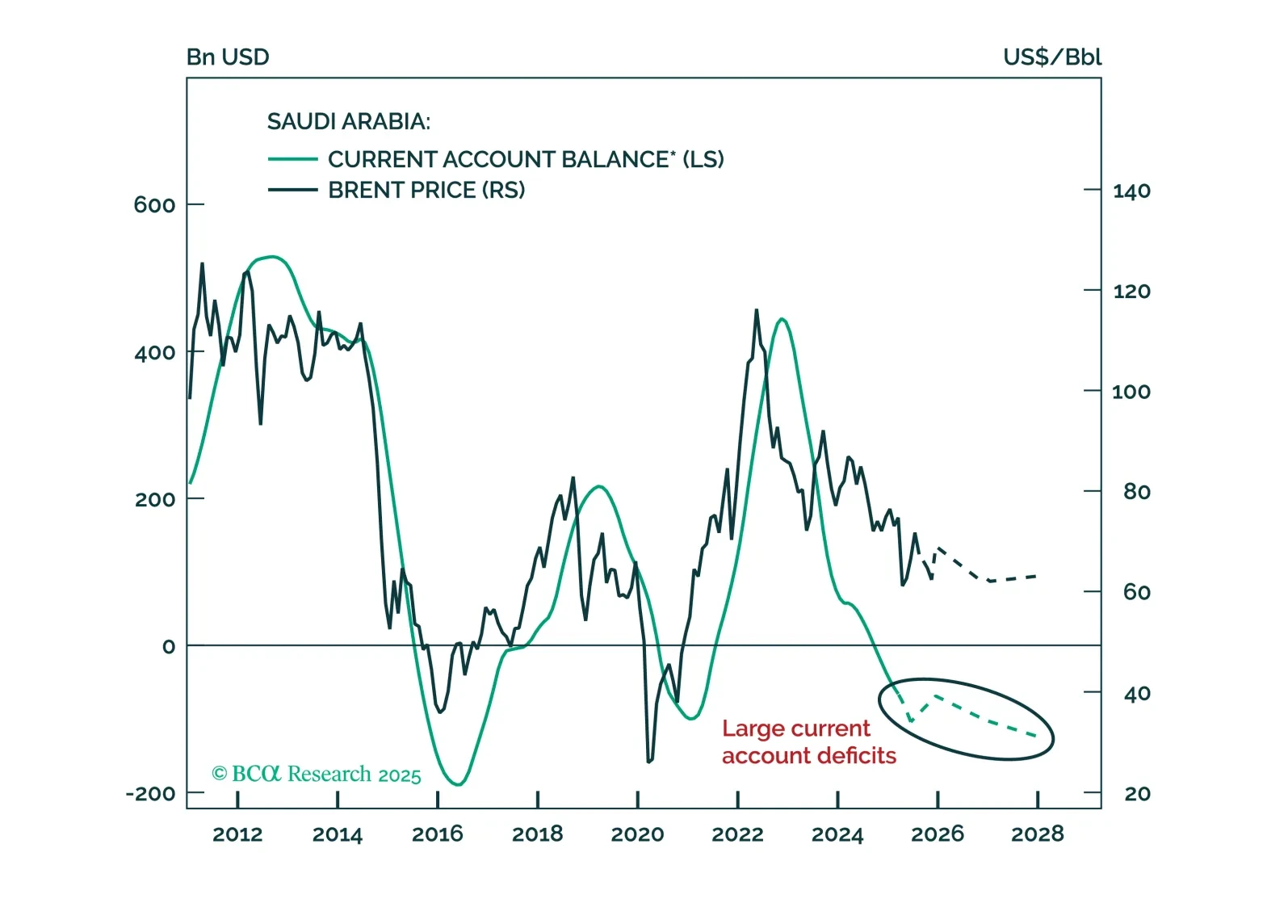

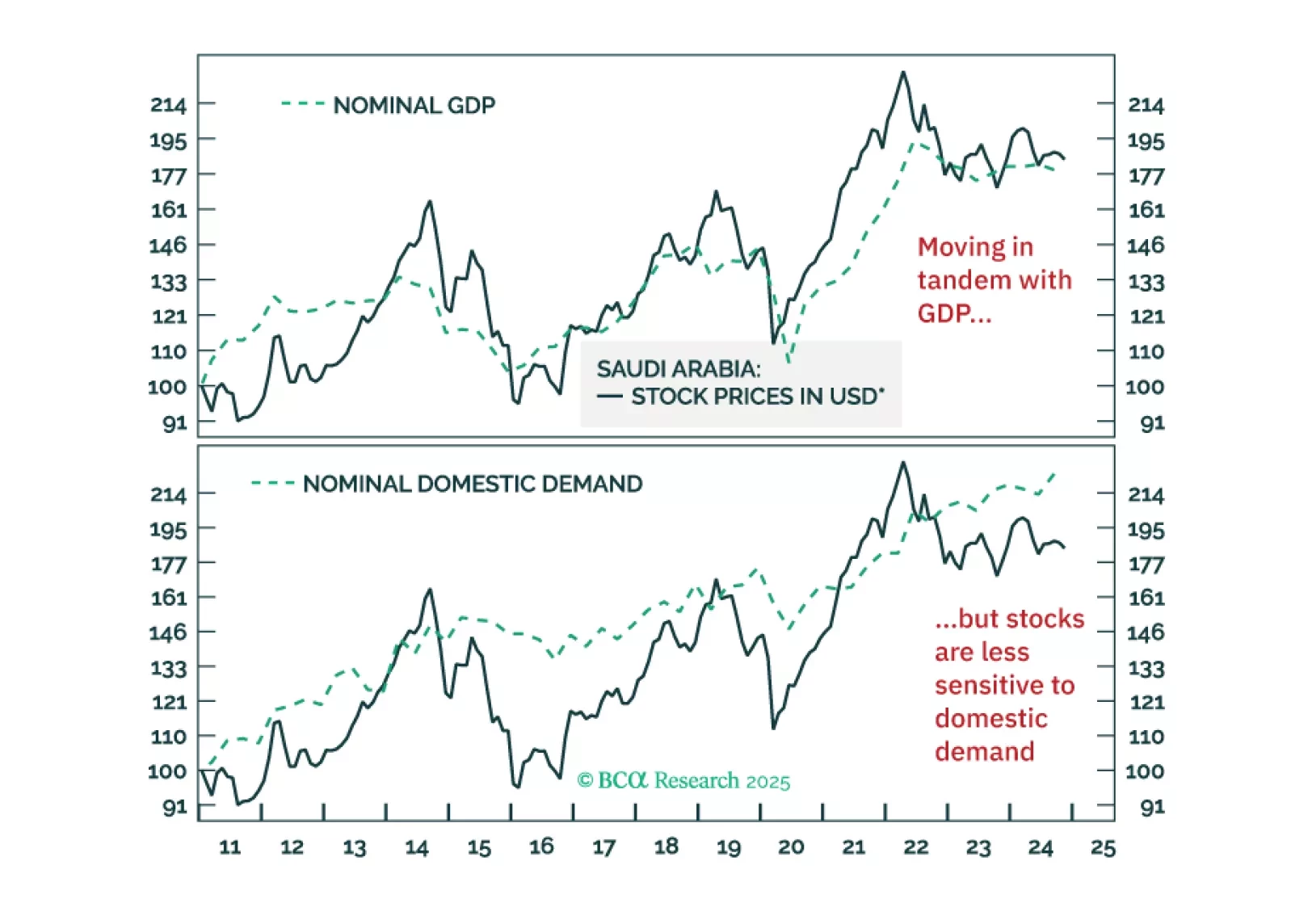

The Saudi authorities’ conscious efforts to move away from oil dependency in recent years appear to have yielded some positive results for its domestic economy.Real domestic demand (total of household, business and government expenditure plus capital investments) is growing at a decent 4.4% - even though the country’s oil export revenues have fallen over the past year (Chart 1, top panel).This contrasts with overall GDP growth rate which slipped into negative territory in 2023-24, as it remains highly influenced by oil export revenues (Chart 2).The apparent dichotomy can be explained by strong foreign and domestic borrowings. As part of its Vision 2030 plans, the kingdom is ramping up its borrowing to finance local infrastructure and other capital investments. The latter have also boosted private consumption and capital investments. The consequent strong domestic demand is corroborated by robust imports (Chart 1, bottom panel). Domestic demand and imports usually move in tandem. But, as per the national account conventions, stronger imports deduct from the overall GDP. This is why the Saudi real GDP growth rate turned negative, even as real domestic demand was rising at a decent pace. The question is, should oil prices weaken in 2025 – as BCA's Commodities & Energy Strategy service expect them to – how will Saudi domestic demand and the overall economy fare? Further, how will the Saudi financial markets perform?Not All That RosyWeaker oil export revenues will hurt Saudi GDP much more than its domestic demand. The latter will likely keep growing decently even if the overall GDP fumbles. This is assuming that Saudi authorities will not deviate from its Vision 2030 plans despite lower oil revenues.As for Saudi financial markets, the outlook is less rosy. That is because the performance of Saudi stocks is more geared towards the state of the overall economy, rather than domestic demand. Chart 3 shows that stock prices move along the trajectory of oil prices and nominal GDP much more than it do along domestic demand. This is because nominal oil revenues (volume times price) remain the principal source of income for the kingdom, which percolates down through the entire economy. As such, it has a much wider impact on the overall economy and asset prices.This also means that in case of any meaningful drop in oil prices Saudi overall growth will falter and Saudi stocks will struggle to keep pace with the EM benchmark (Chart 4): An impending slowdown in global growth next year entails that global crude demand is likely to stay muted. That will put downward pressure on crude prices.It will also prevent Saudi Arabia from ramping up its own production - as the country would like to avoid a plunge in oil prices due to excess supply. Notably, at 9.2 million barrels a day, Saudi production is around the lowest in more than a decade (save the GFC and COVID crises periods). Their share in global crude production is also equally low (Chart 5). Lower global crude prices, coupled with a likely extension of voluntary production cuts, means a further drop in Saudi export revenues. That will keep the kingdom’s nominal growth suppressed, which will hurt stock performance.Policy CliffIn their 2025 budget, Saudi authorities plan to reduce fiscal spending meaningfully to USD 332 billion, which is 4.5% lower than the estimated expenditure for 2024. Should the authorities stick to their plans, that will surely be a major headwind to growth:A restrictive fiscal stance will weigh on domestic demand and liquidity. Higher fiscal spending creates new demand and encourages new economic activity. That, in turn, spurs new bank borrowings, pushing up the money supply. If fiscal spending contracts next year, the country’s broad money supply will slow materially (Chart 6). That is neither positive for the economy nor for share prices.To put matters into proper context, the kingdom’s annual fiscal outlay, at around 35% of GDP, is much larger than the country’s annual net bank credit origination, at around 7% of GDP (Chart 7). Annual spending via extra-budgetary channels, such as PIF, the sovereign wealth fund, is even lower at around 3% of GDP. Budgetary outlays, therefore, play a greater role in driving domestic demand. Saudi interest rates, meanwhile, remain too high for the state of the economy. Because of the pegged currency, the Saudi central bank is forced to set interest rates in line with those of the US. This is despite growth rates in the two economies having diverged materially: The Saudi economy is growing at 1.3% in nominal terms, while the US is at 4.3% (Chart 8).The upshot is that the rather high borrowing costs will weigh on Saudi private sector credit growth, another impediment to boosting economic activity. One plausible reason the Saudi fiscal authorities are planning to curtail spending is to rein in public debt. The persistent fiscal deficits and funding requirements for the Vision 2030 projects have led to a rapid rise in borrowings. From a mere USD 12 billion in 2014, gross public debt has surged to 306 billion (28% of GDP) currently (Chart 9).In the coming year, debt will rise further given the weak fiscal revenue outlook (oil revenues make up 64% of total budget revenues), and the authorities’ commitment to Vision 2030 plans, which entails significant public spending.Notably, the Saudi debt surge has coincided with widening Saudi sovereign spreads relative to their EM counterparts (Chart 10).In sum, the specter of weaker revenues is encouraging Saudi fiscal authorities to keep expenditure in check. That explains their budgetary plans for lower fiscal spending in 2025. This will weigh on share prices. Investment Conclusions Equities: Given our cautious view on oil prices, we do not recommend that absolute-return investors venture into this bourse just yet. Dedicated EM equity portfolios should continue to have a neutral allocation to this bourse (Charts 2 and 3, above). Incidentally, our Geopolitical Strategy service expects further escalations in geopolitical risks in the Middle East. However, such escalation in the region will hurt Gulf bourses regardless of any possible oil price spike.Sovereign Bonds: Given that the country’s public debt is set to rise further, Saudi relative spreads versus EM may not narrow anytime soon. Investors should downgrade Saudi credit from overweight to neutral in EM credit portfolios (Chart 10).Rajeeb PramanikSenior EM Strategistrajeeb.pramanik@bcaresearch.com