Sectors

One of the best things about working at the world’s largest – and oldest! – market research firm is that the “vault” contains research on almost any conceivable topic. As such, I pen this short missive to flag to the GeoMacro clients three reports on the risk of tech regulation – relevant in the context of the October 8 US Department of Justice statement that it may look to force Google to divest parts of its business.

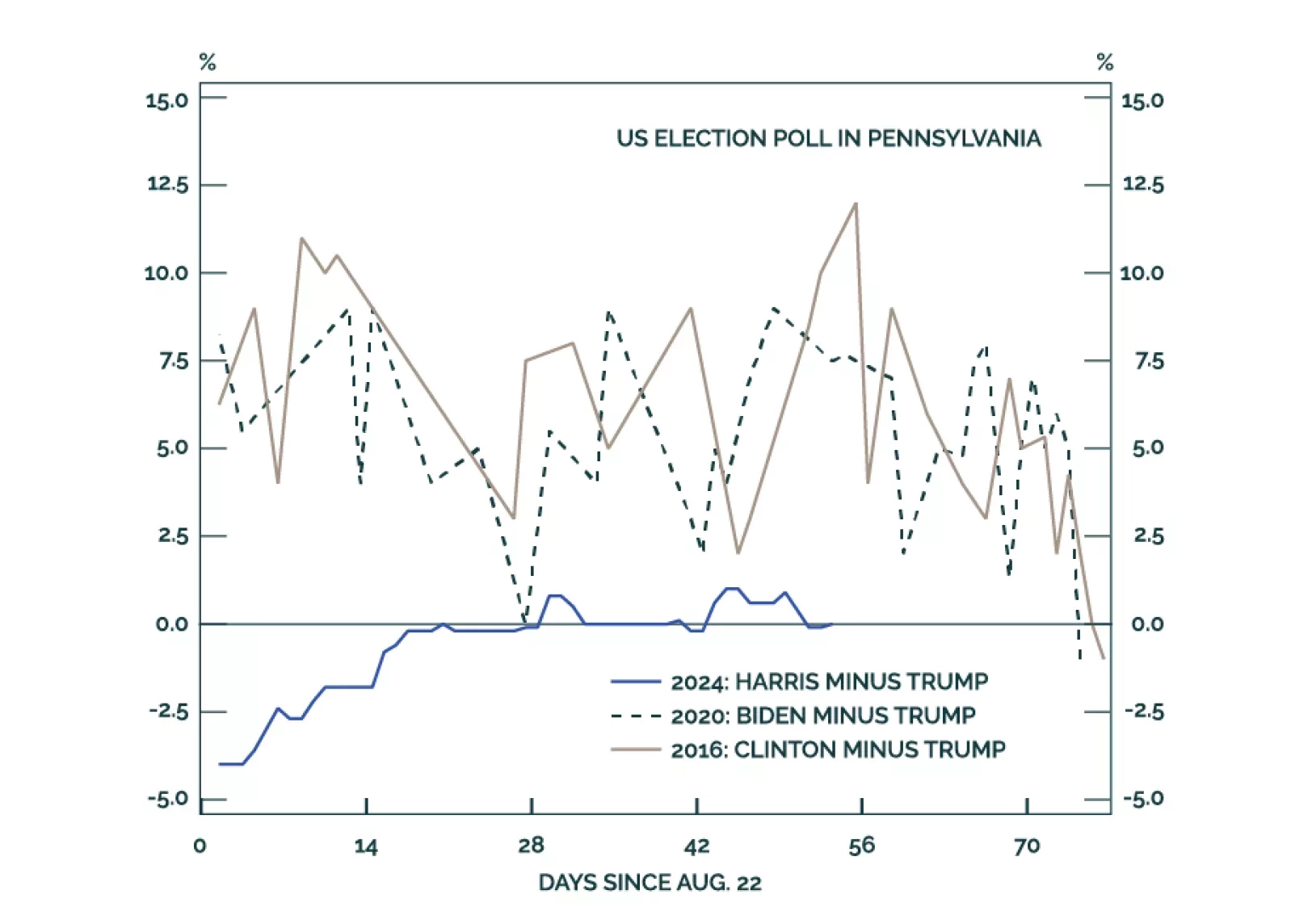

The US election underscores three long-term trends of Generational Change, Peak Polarization, and Limited Big Government. Investors should expect more volatility around the election and should assess the results before adding more risk. While we predicted the October surprise from the Middle East, more surprises are coming before the final vote is cast.

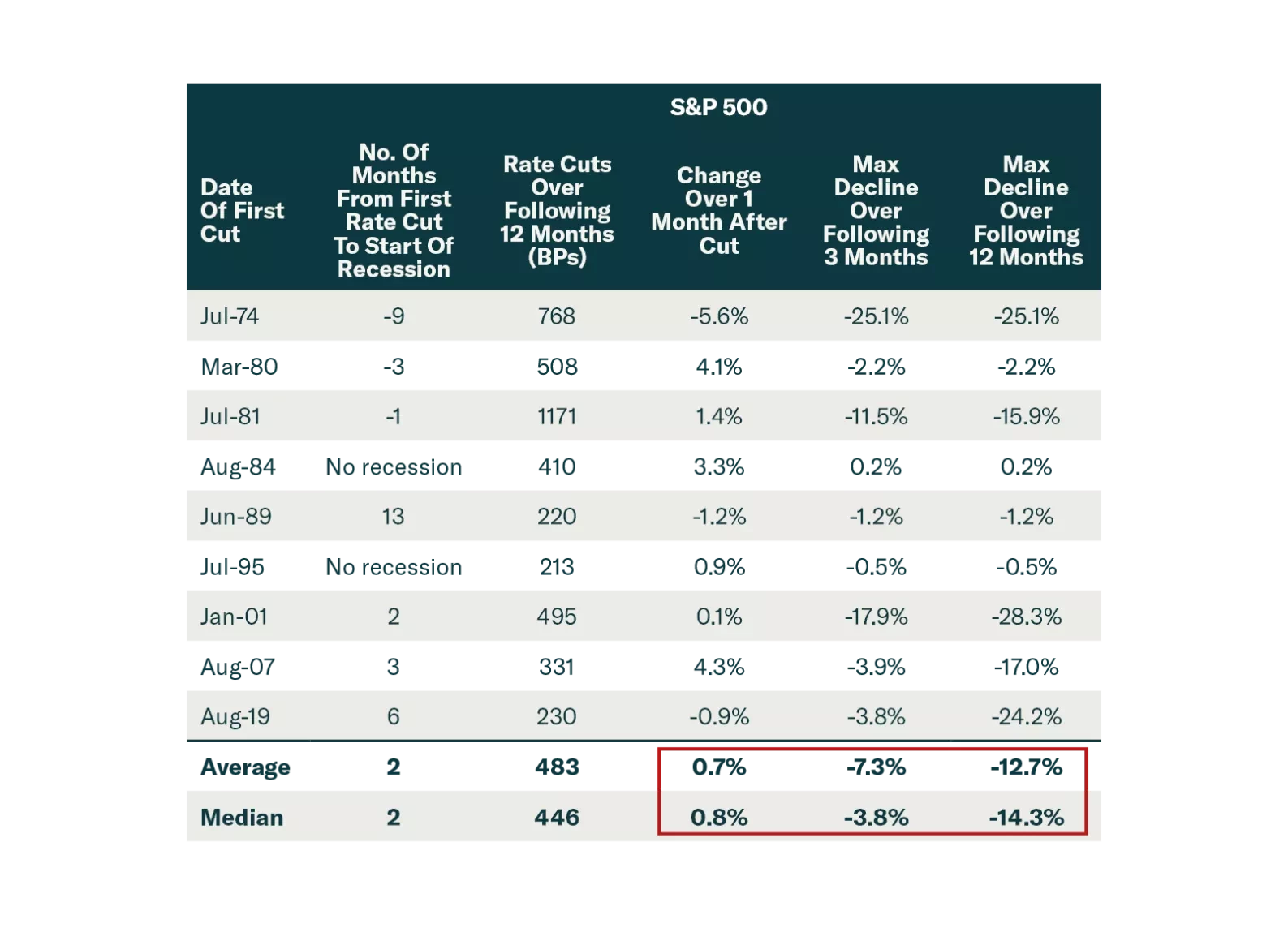

The market got excited by the 50 bps Fed cut and China stimulus. But these are a recognition that economies are slowing significantly. Stocks often rally after the first Fed cut, before falling sharply. Investors should stay defensive.