United States

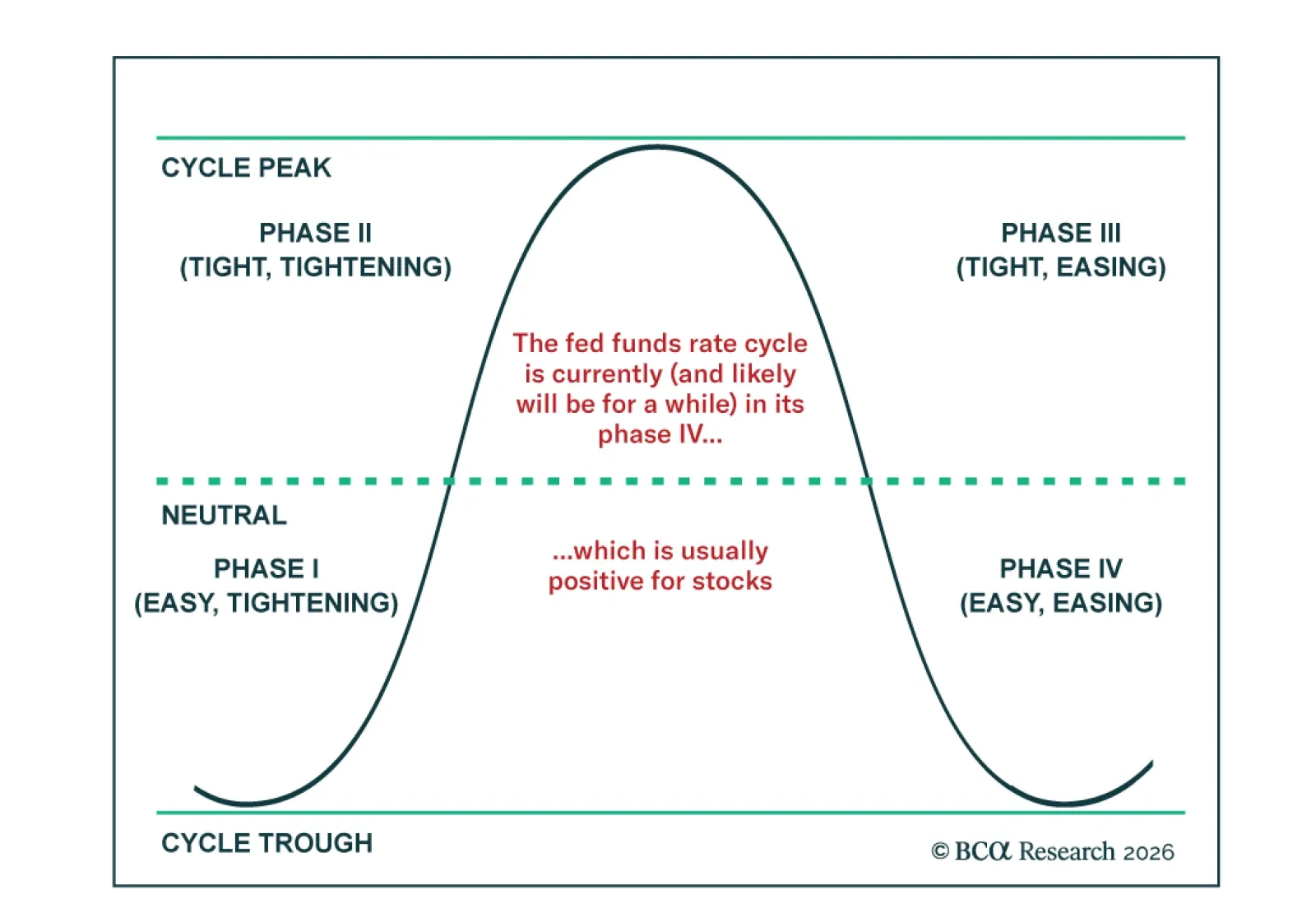

Our US Investment strategists expect accommodative monetary policy in 2026, but equities may be less responsive than in prior easing cycles. Historically, equity returns have been significantly stronger under easy policy, and further Fed cuts are expected…

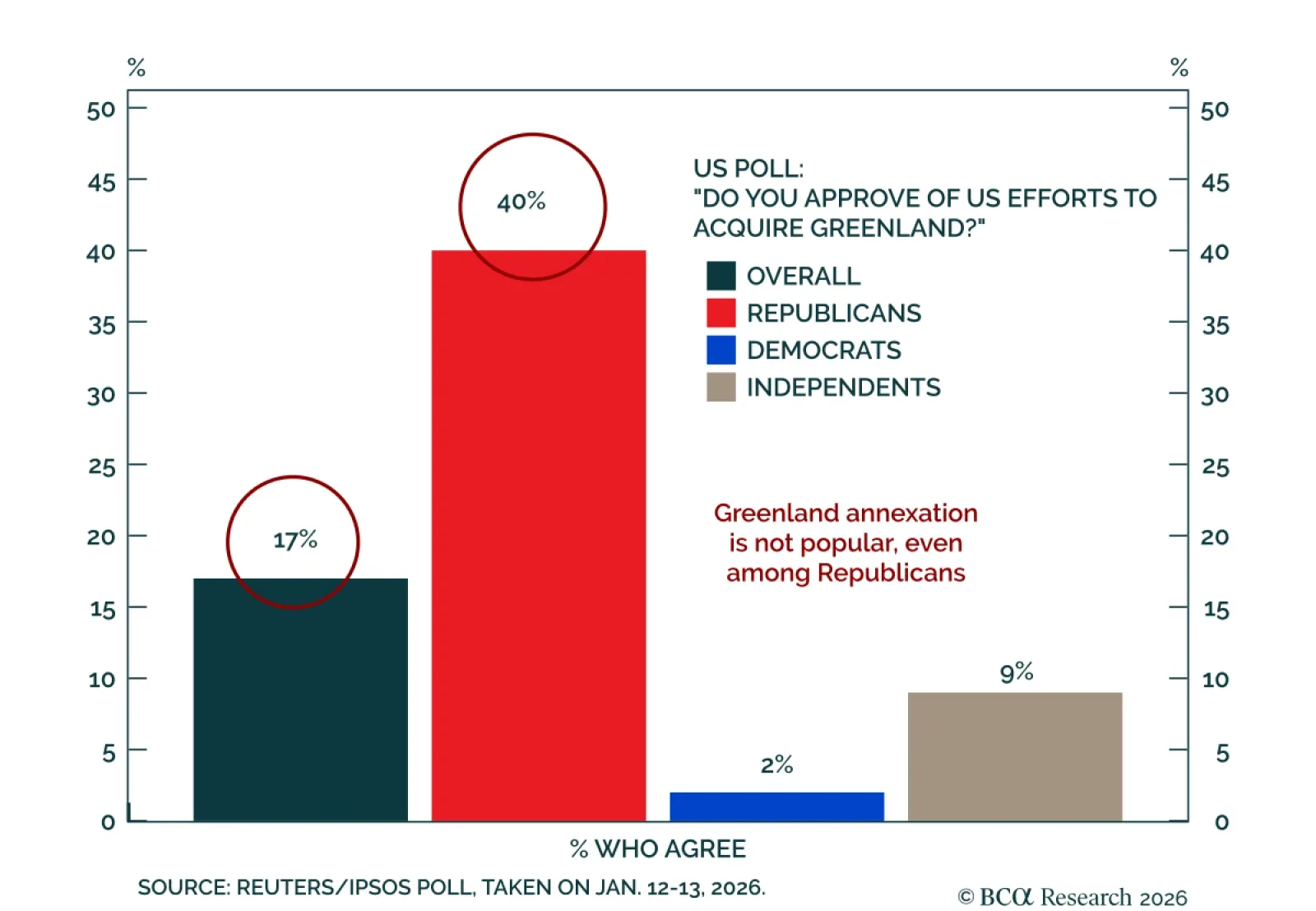

Greenland has moved to the forefront of geopolitics, but a non-military resolution remains the most likely outcome. Our Geopolitical strategists do not expect the US to seize Greenland by force or collapse NATO. Nonetheless, they judge that this is not the…

Investors should bet against the US seizing Greenland by force and collapsing NATO. But stay tactically defensive anyway.

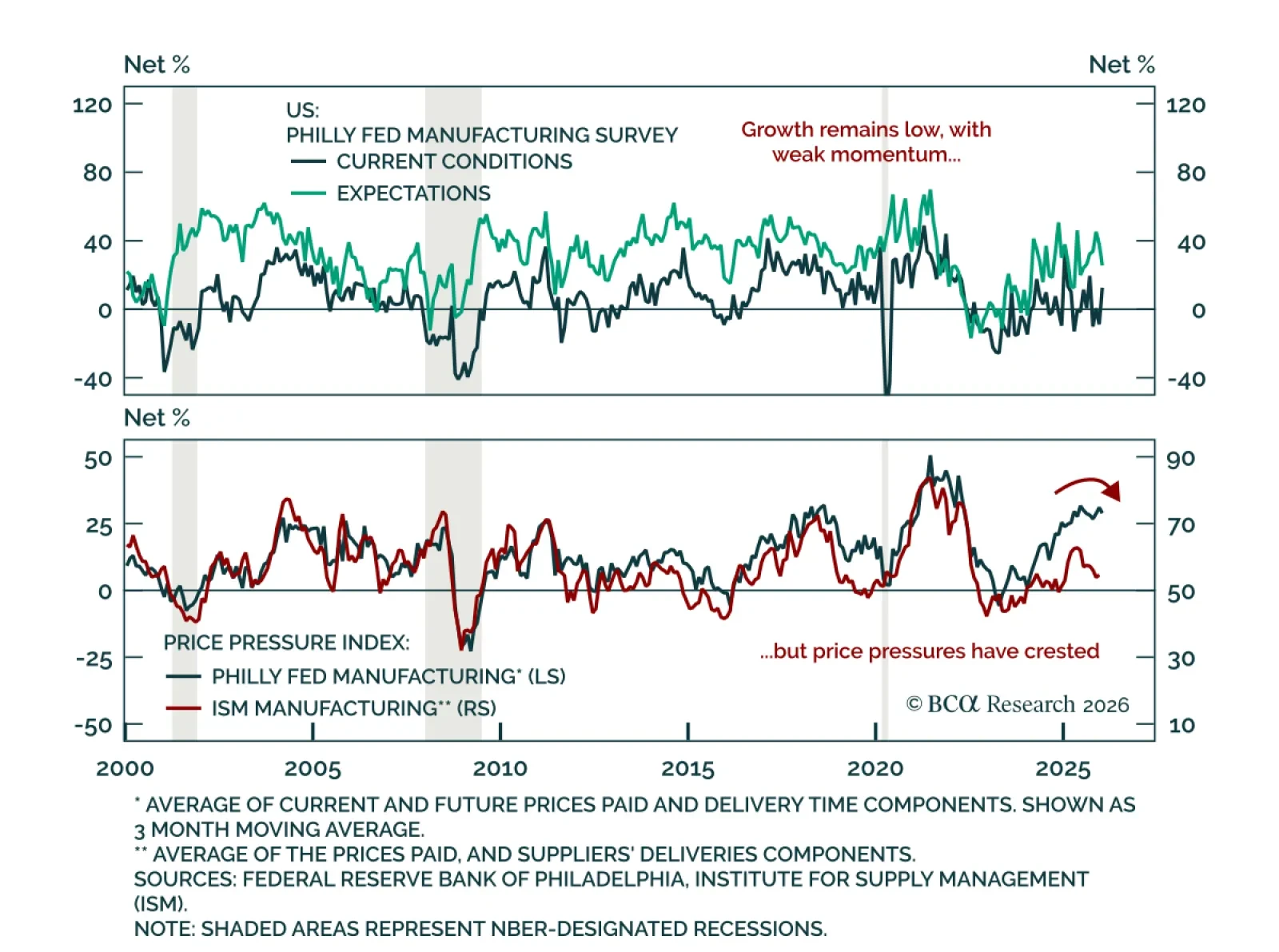

Maintain a modestly defensive allocation as manufacturing surveys signal resilience without momentum. The January Philly Fed and Empire Manufacturing surveys both beat estimates, rebounding to 12.6 from -10.2 and to 7.7 from -3.9, respectively. New orders and…

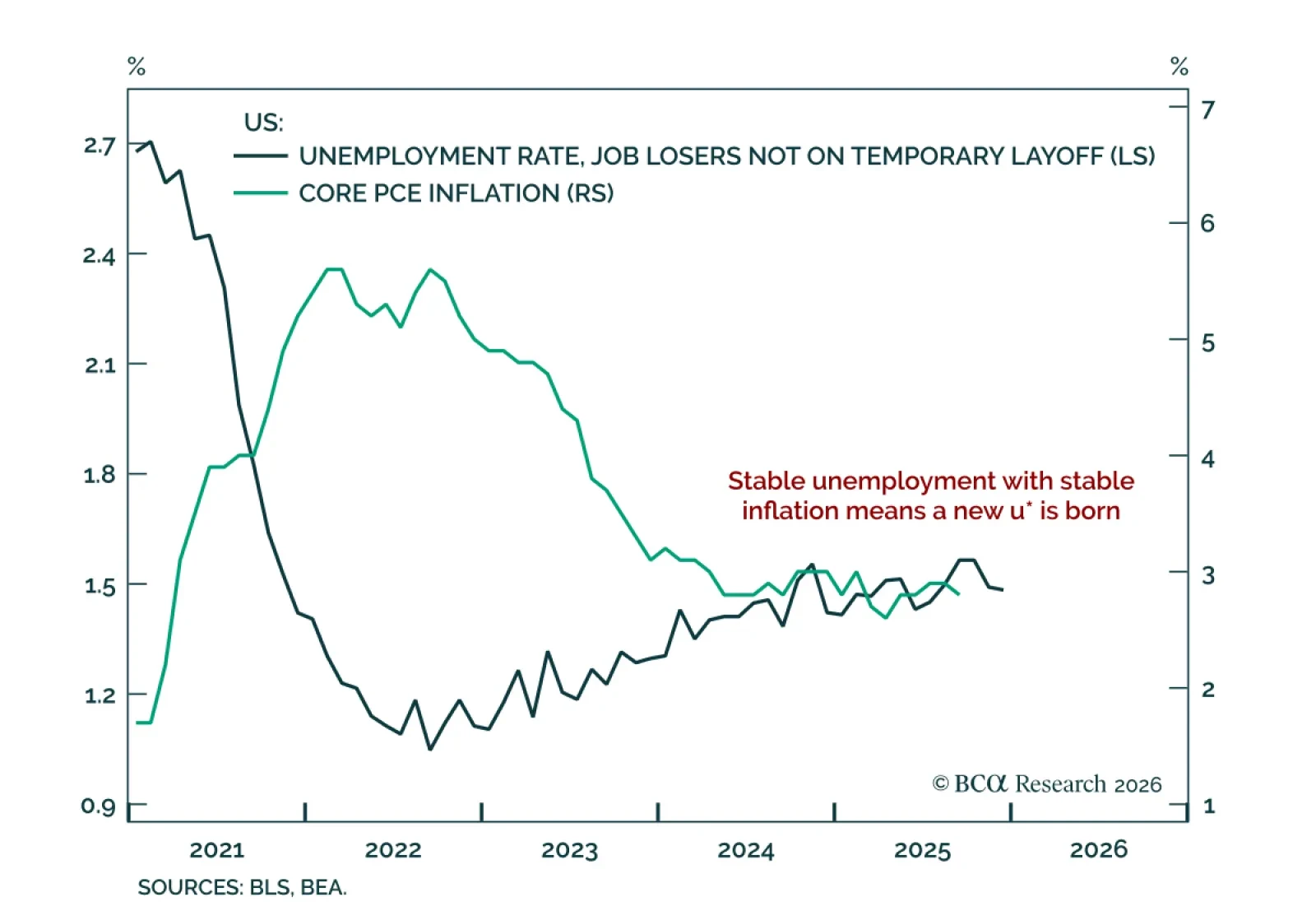

Our Counterpoint Strategists remain underweight duration, underweight US Treasuries versus other DM bonds, and underweight the dollar, as they see Fed cuts risk reigniting inflation. With both the unemployment rate and interest rate near their estimated…

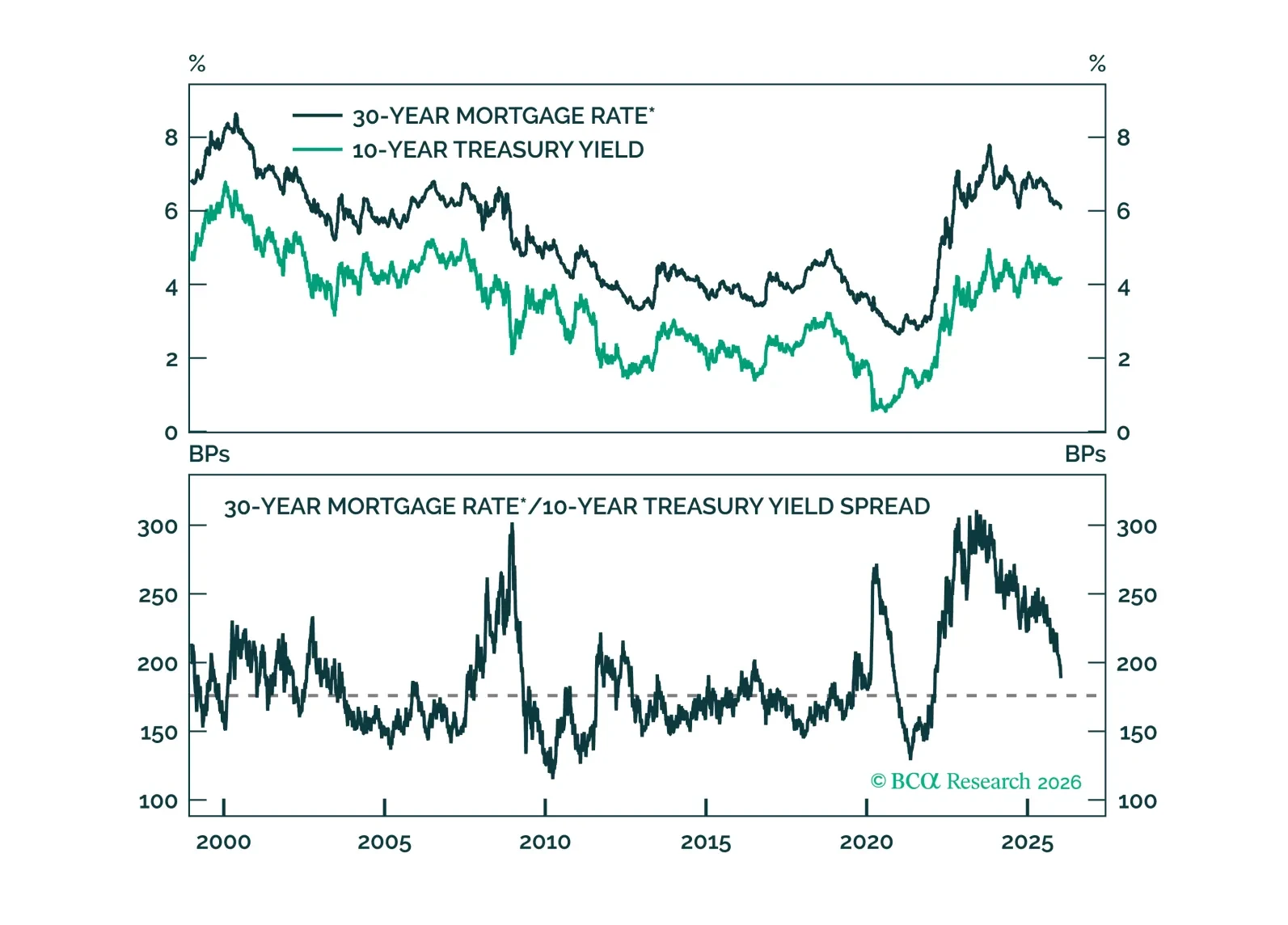

Mortgage spread tightening has run its course. Any further drop in mortgage rates will necessitate lower Treasury yields.

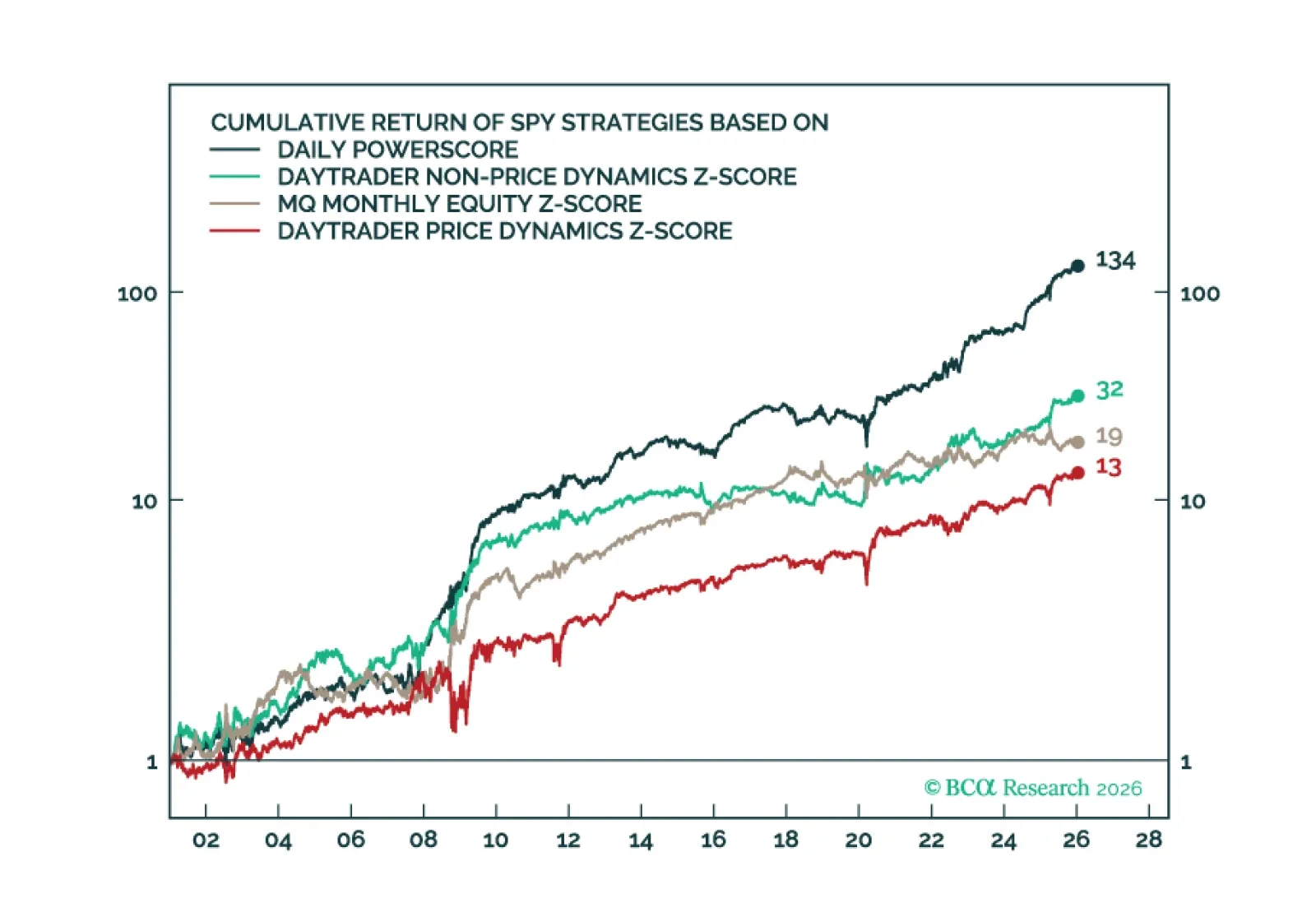

Over the past few months, we have been deploying new market-timing tools aimed at improving the accuracy of our calls. Today’s report highlights our ultra high-frequency Daily Oscillators, which provide daily signals on the near-term direction of the S&P 500 and long-term Treasuries.

Our US and Geopolitical strategists argue that, despite intensifying socioeconomic and geopolitical challenges, the long-run case for US resilience remains intact. As the country marks its 250th year, the strategic rise of the US continues to shape global…

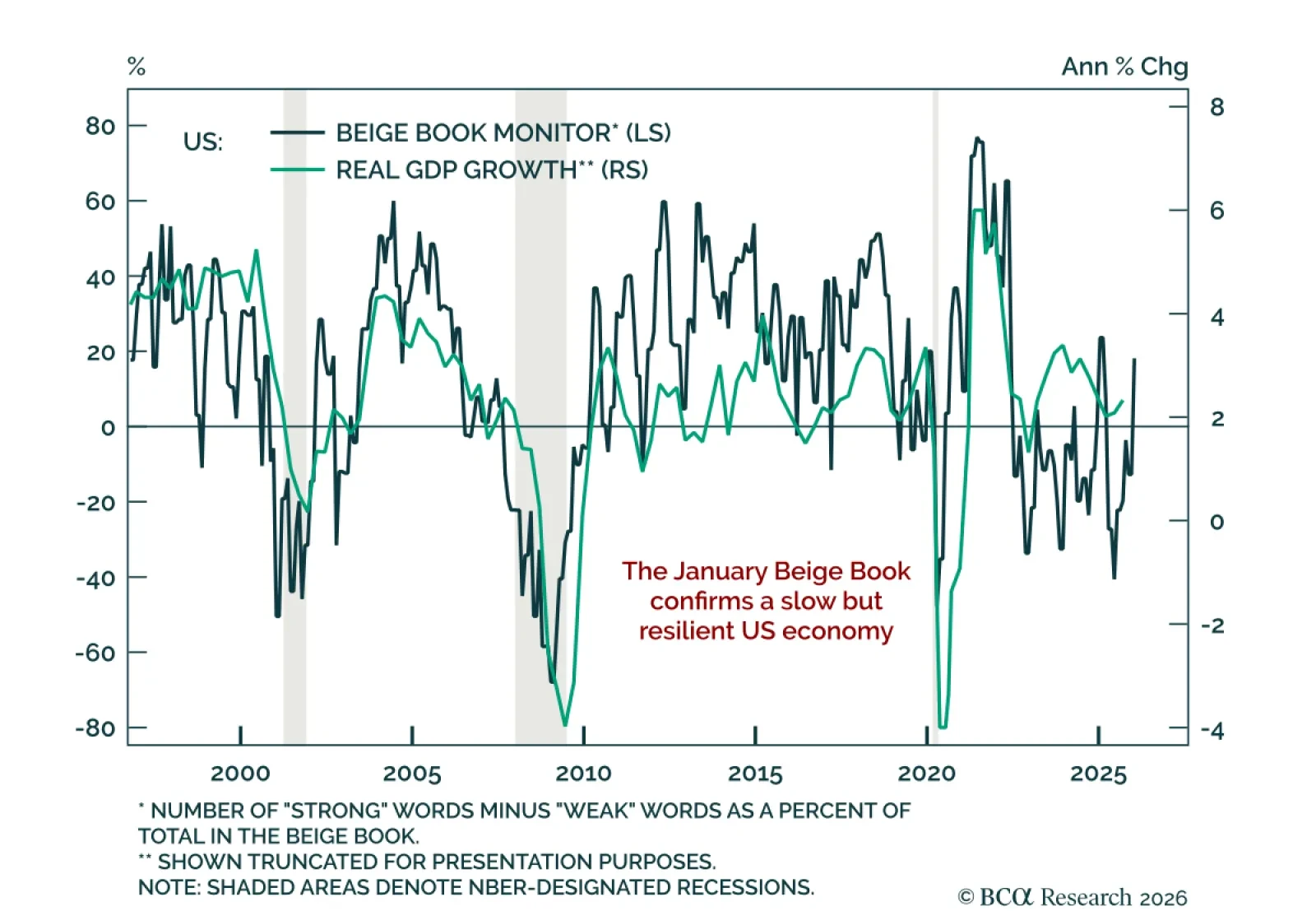

The Beige Book confirms a slow but resilient US economy. The January Beige Book points to activity increasing at a slight-to-modest pace in most Fed districts, a shift from earlier reports where most districts saw unchanged activity. Consumer spending remains…

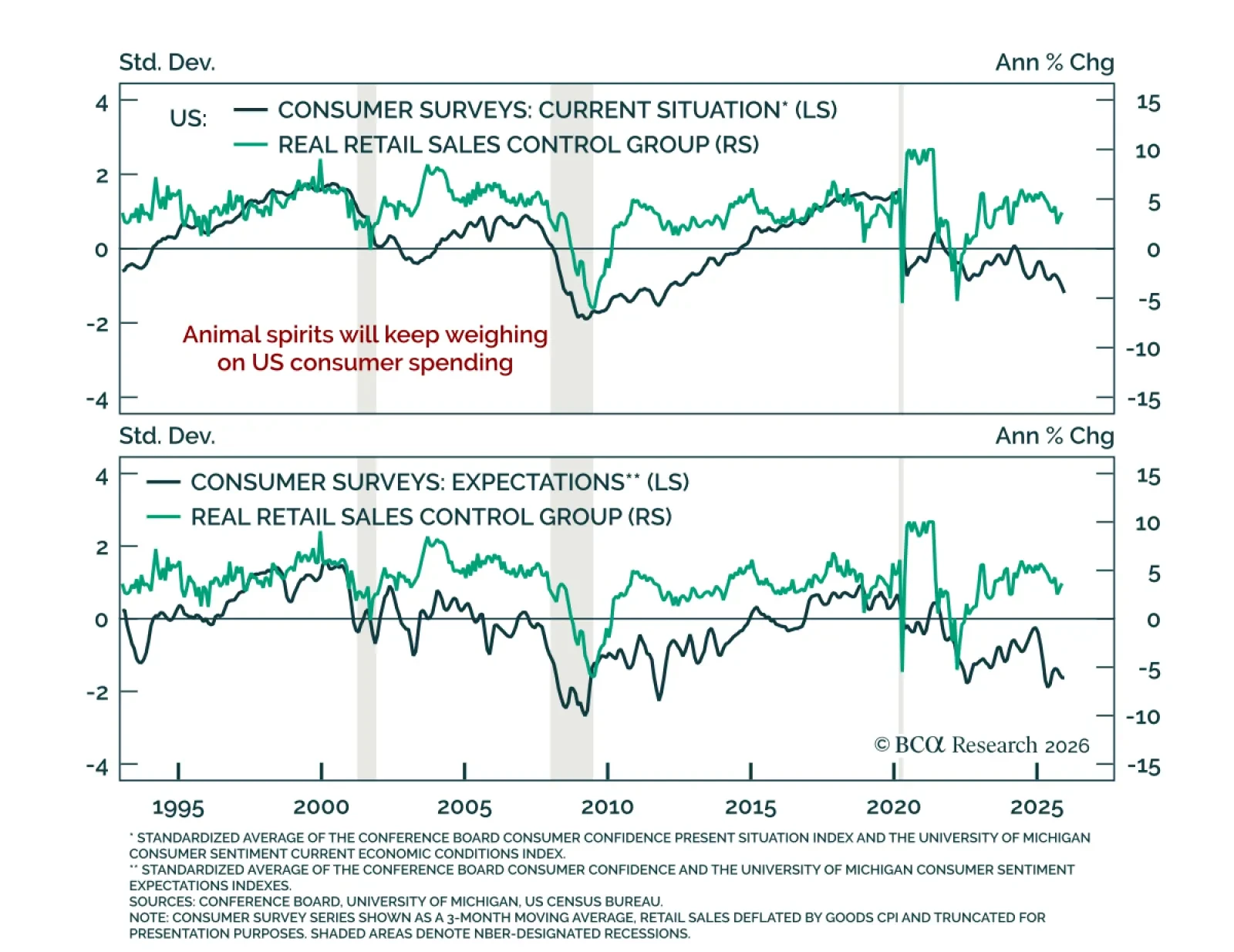

Maintain above-benchmark duration and 2-year/5-year Treasury steepeners as slowing labor income keeps downside risks for growth intact. November US retail sales beat estimates, with the headline rising 0.6% m/m after being flat in October. Core retail sales…