United States

Our preferred tactical global fixed income trades for the rest of 2022 into early 2023 are all expressions of our views on relative monetary policy shifts within the main developed market economies. These involve bets on a relatively more hawkish Fed and Bank of England versus a relatively more dovish ECB and Bank of Canada, while also betting on additional selling pressure on Italian government bonds.

We continue to anticipate that the Fed won’t pause its tightening cycle until Q1 or Q2 of 2023, and current labor market trends certainly give no indication that a Fed pause (or “pivot”) is imminent.

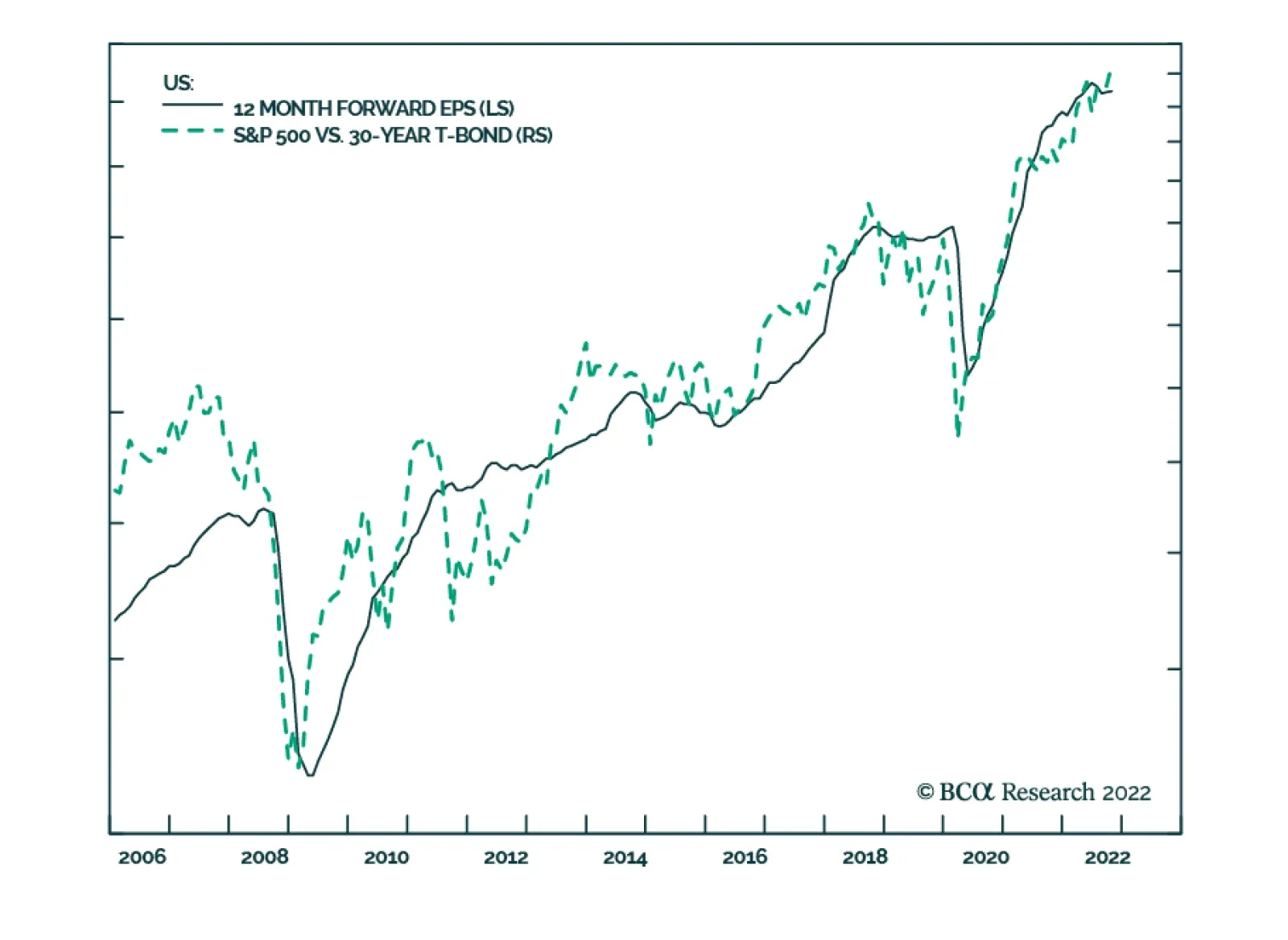

Sentiment toward stocks is depressed and European valuations have declined substantially. However, the earnings outlook remains poor. Which side will win?

Long-after-the-fact revisions to reported income, spending and savings data do not alter our assessment that a flush consumer will continue to support the US economy and allow S&P 500 earnings to surprise the bearish investor consensus.

OPEC 2.0’s decision to cut 2mm b/d of output beginning in December telescopes the loss of Russian volumes we expect over the course of the coming year. OPEC 2.0 clearly is not playing by the G7’s or the US’s rules. This will keep prices volatile.

Investors should overweight US defense stocks in a world where US war-weariness is declining and the Biden administration is likely to exhibit an increasingly hawkish foreign policy.