United States

We give a one-third probability of a federal government shutdown. It probably will not happen before November. At worst, government shutdowns only cause temporary market volatility.

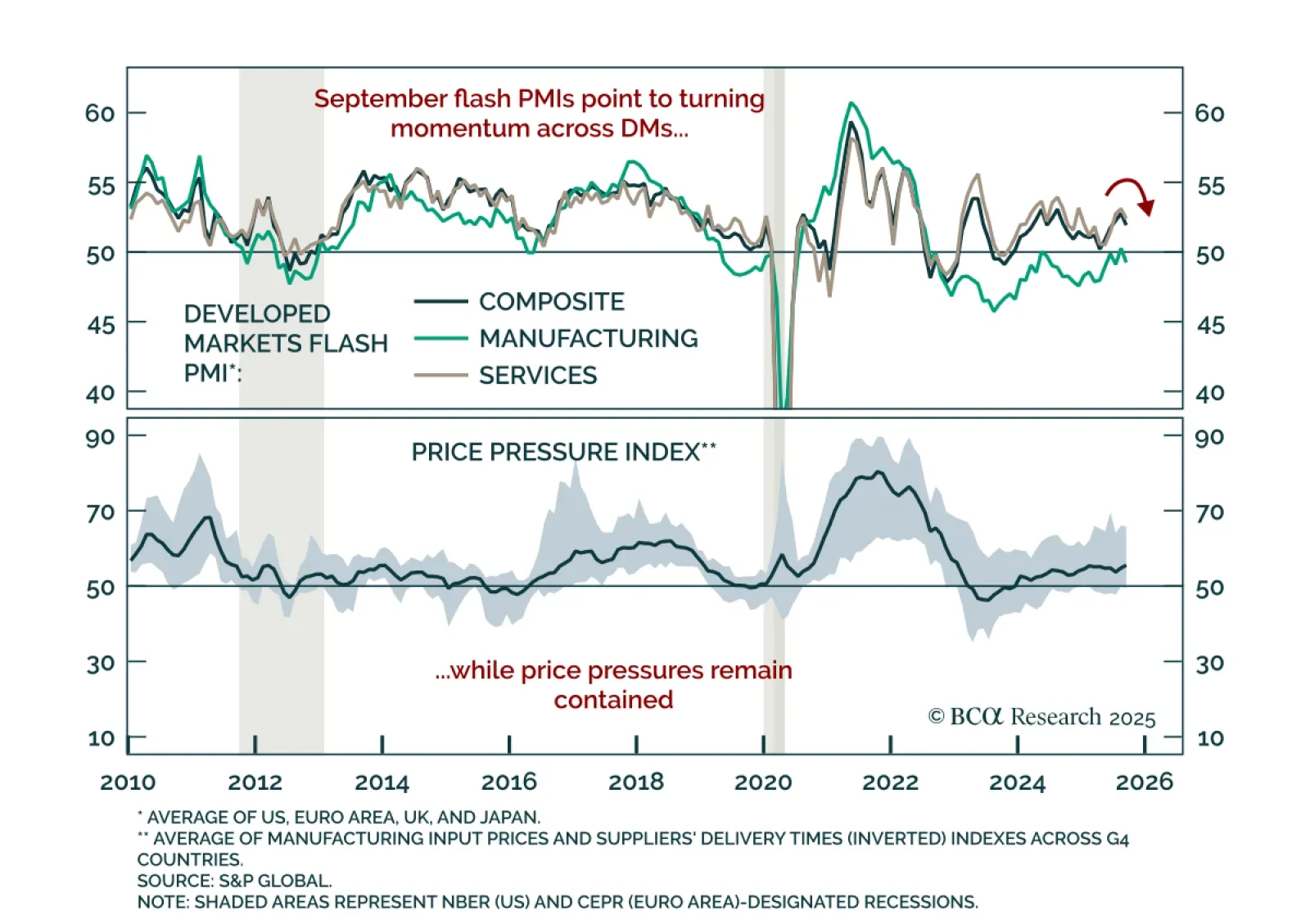

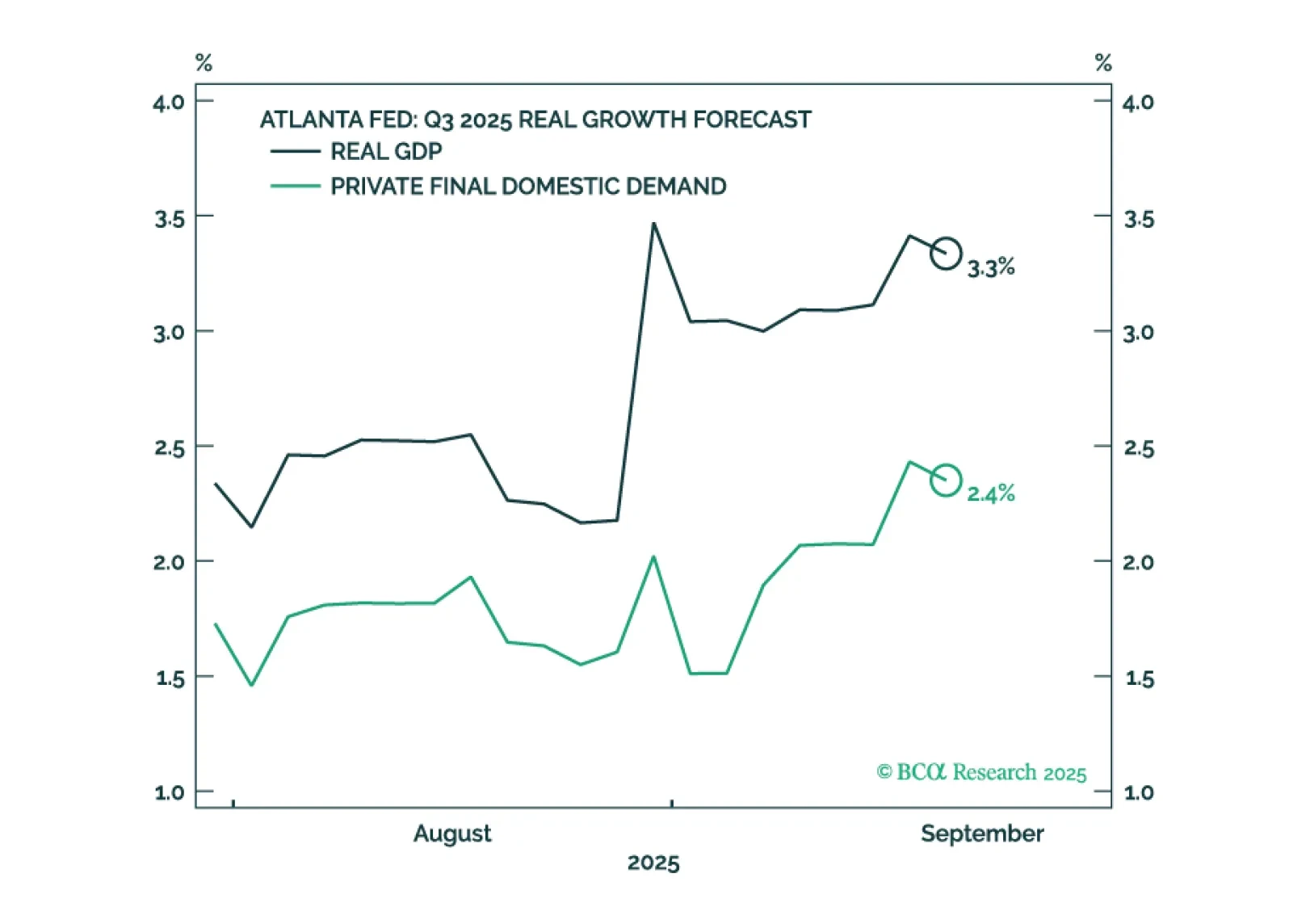

US GDP growth appears to have accelerated even as employment growth has faltered. We will make a final decision in early October when we publish our next Strategy Outlook, but most likely, we will cut our 12-month US recession probability to 40%-to-50% from 60% and turn tactically neutral on stocks, while still retaining a modest equity underweight over a 12-month horizon.

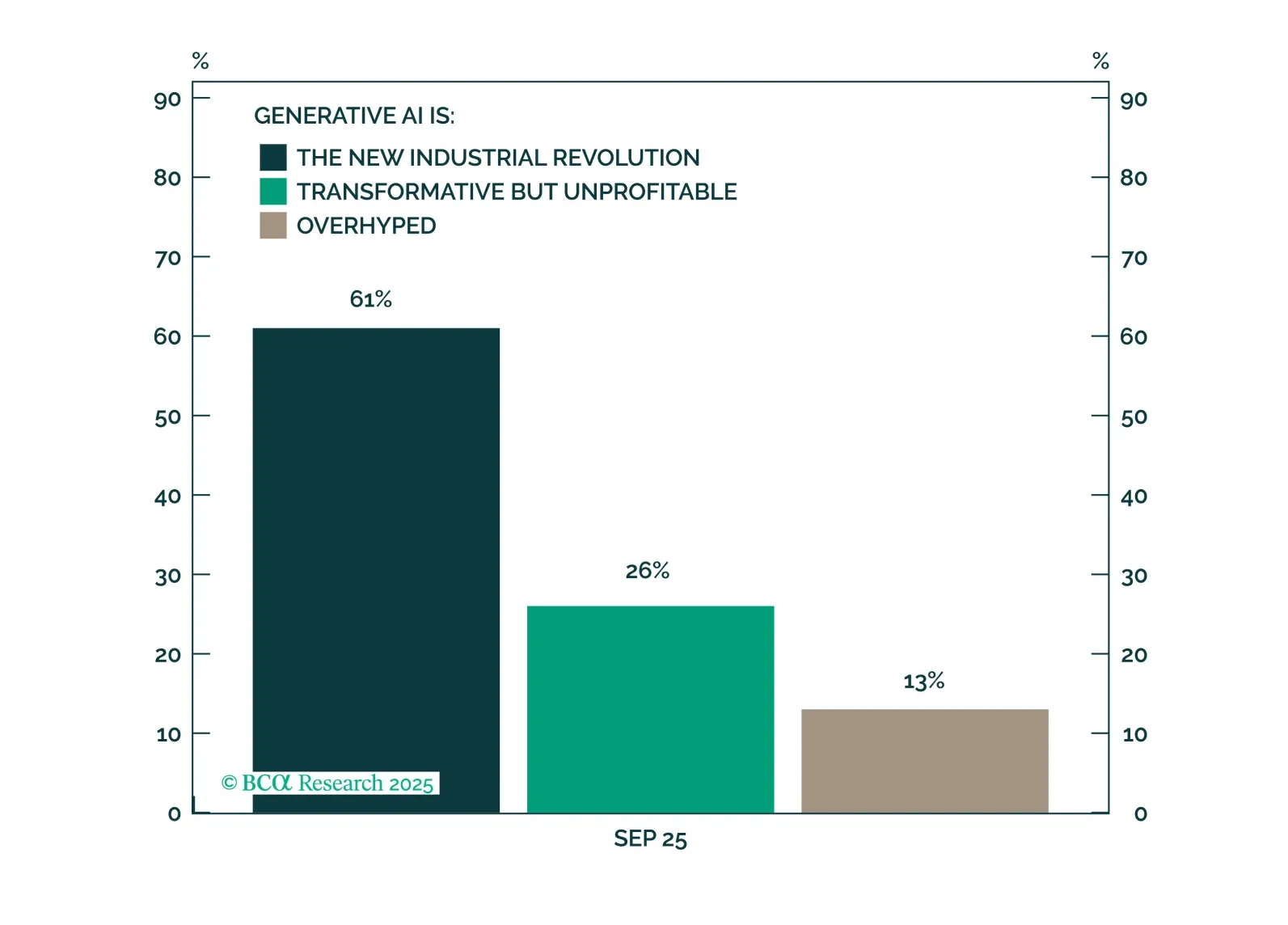

According to our latest client poll, most respondents are optimistic about the Generative AI's potential. Investors remain divided on whether current equity valuations reflect a bubble. Economic concerns continue to center on bond yields and the risk of stagflation, while relatively few clients anticipate a recession. In terms of portfolio positioning, an overweight in Technology received the strongest endorsement.

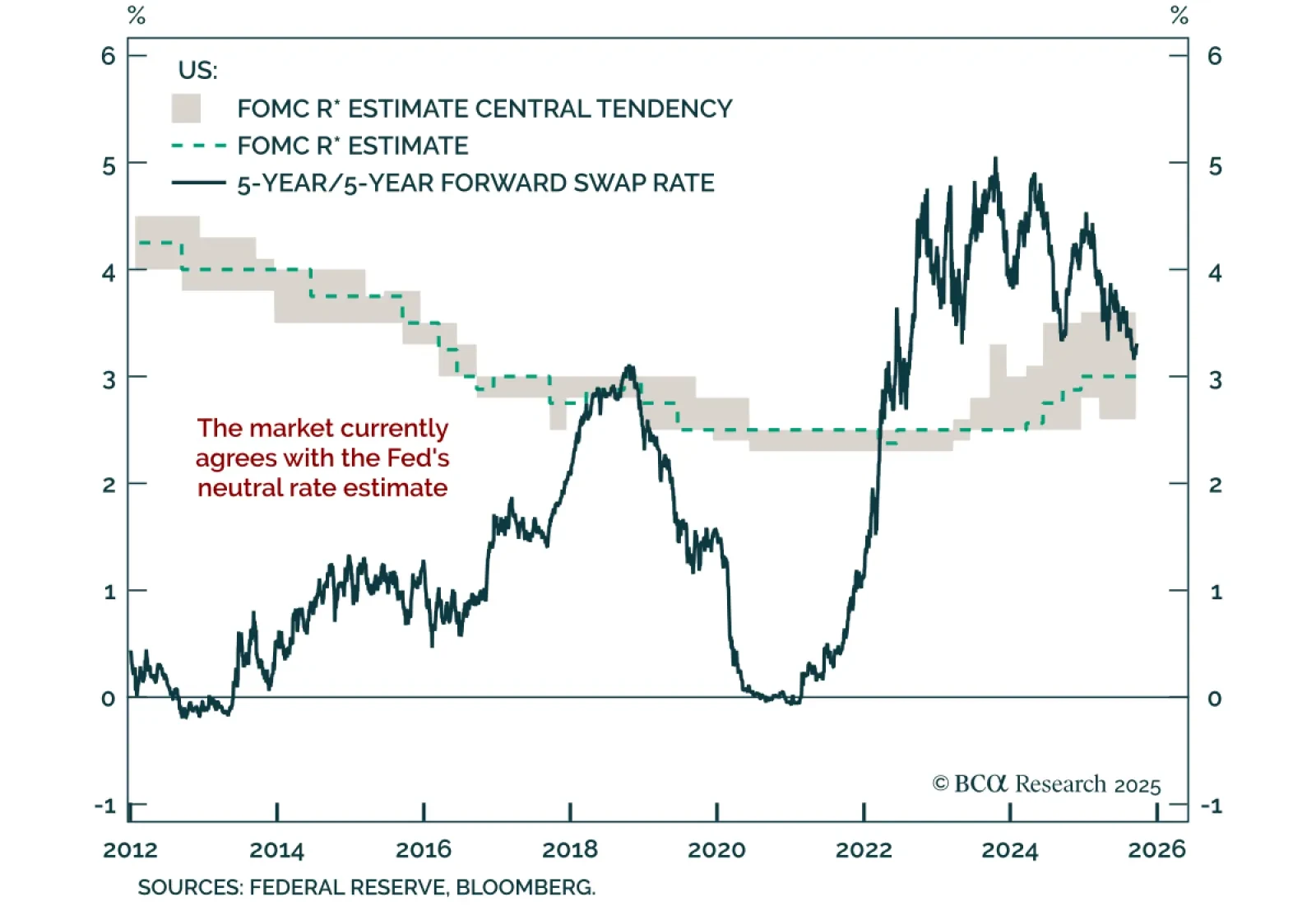

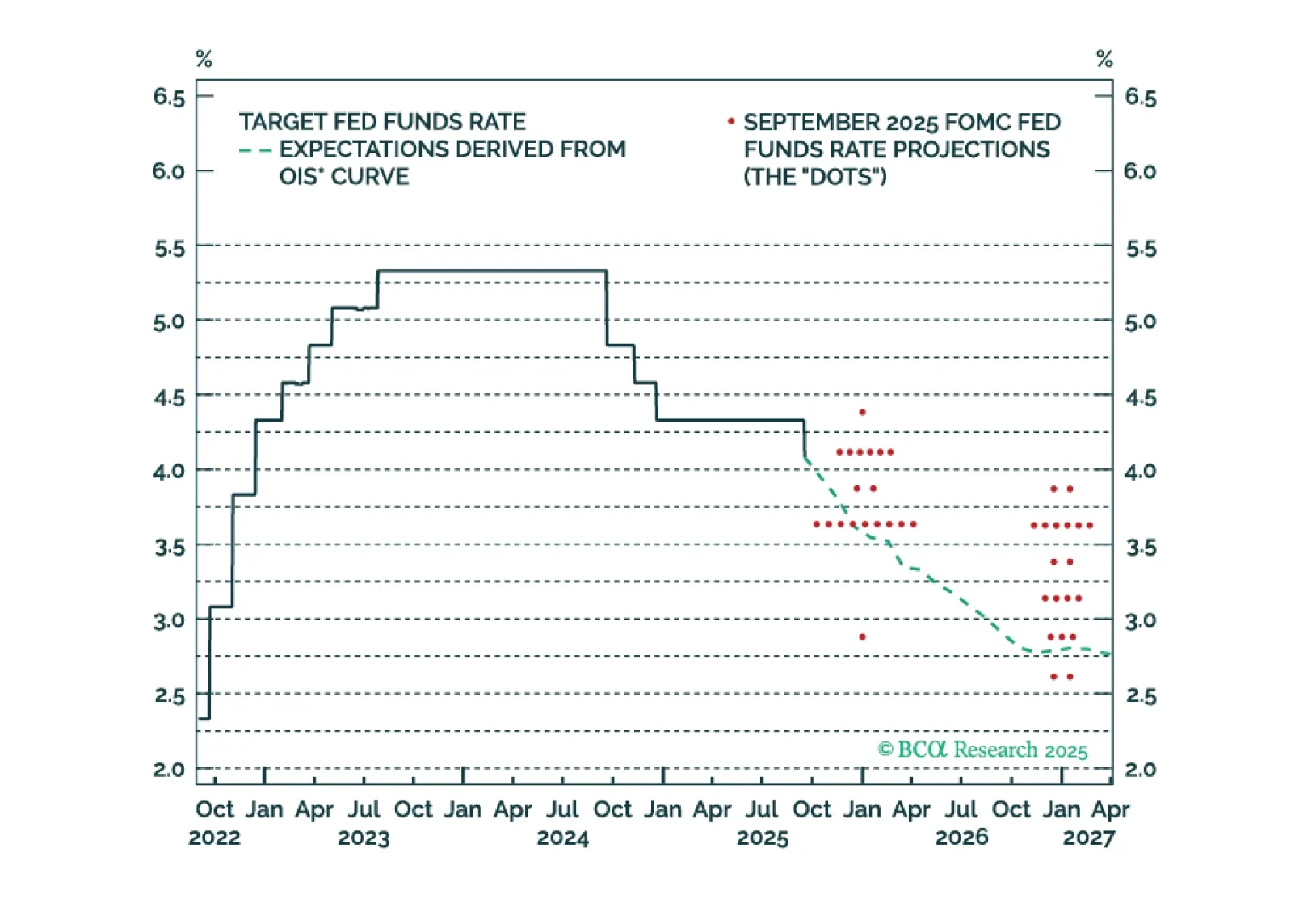

Median Fed unemployment rate projections are overly optimistic. The Fed will end up cutting more in 2026 than it currently anticipates.

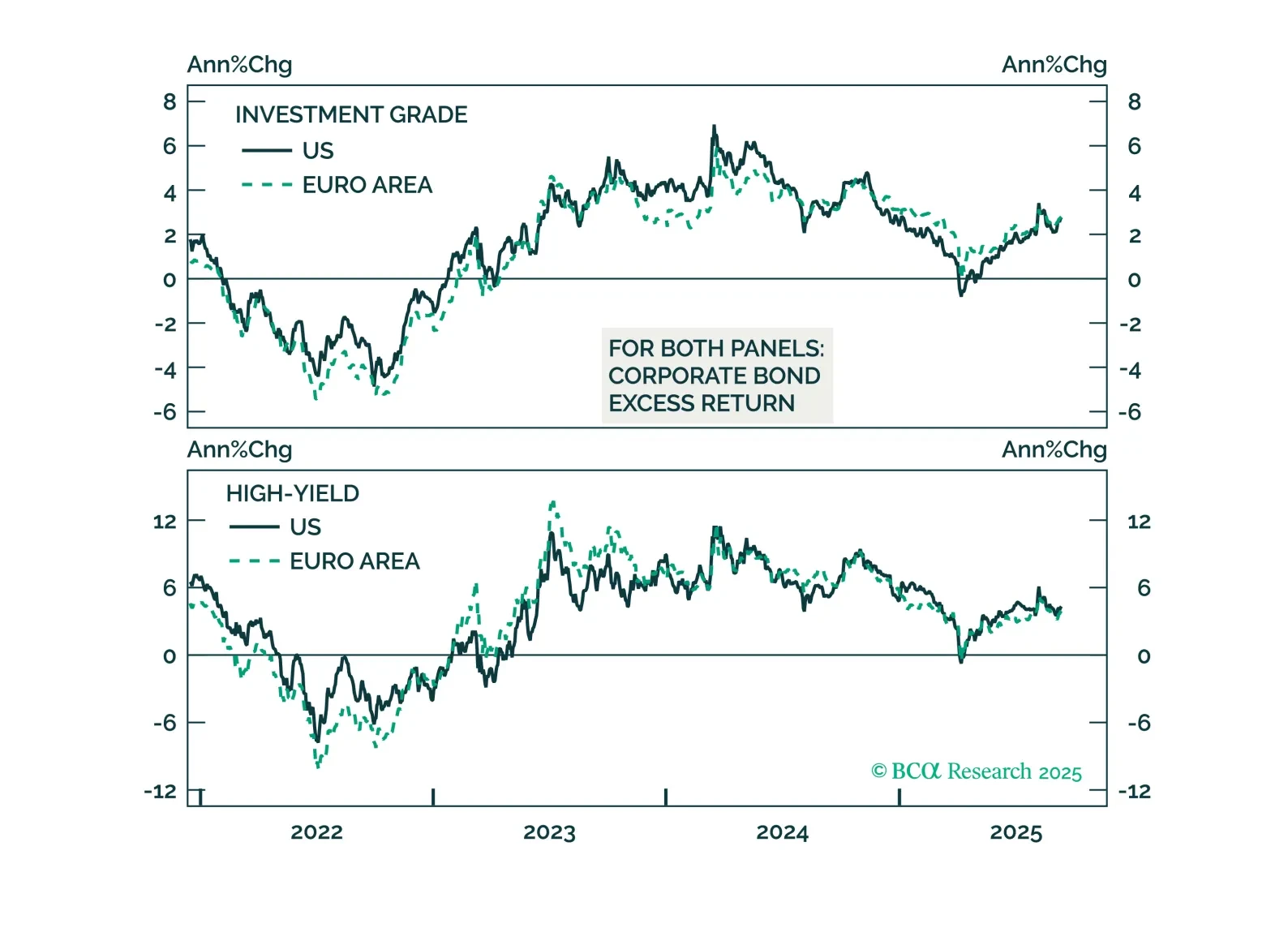

Structural tailwinds help explain tight credit spreads. In Europe, we see room for further tightening. Stay underweight US credit amid cyclical risks, but upgrade Euro Area IG to overweight and HY to neutral.