United States

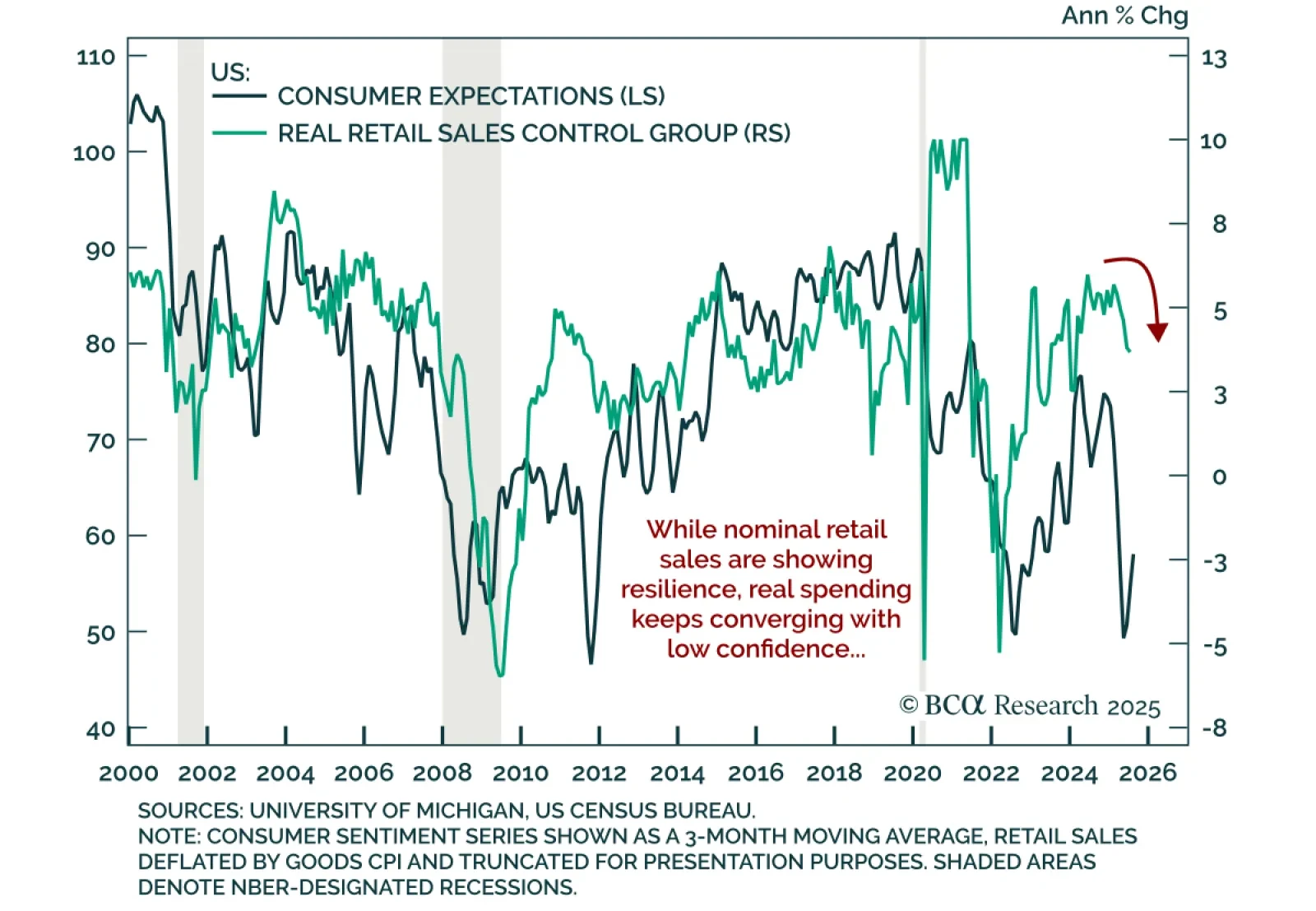

Retail sales and consumer sentiment data point to slowing underlying momentum despite headline resilience. Retail sales rose 0.5% m/m in July, below estimates and decelerating from 0.9% in June. The control group beat estimates at 0.5% but also slowed.…

The cost of tariffs is falling on the US consumer, not foreign exporters or US firms.

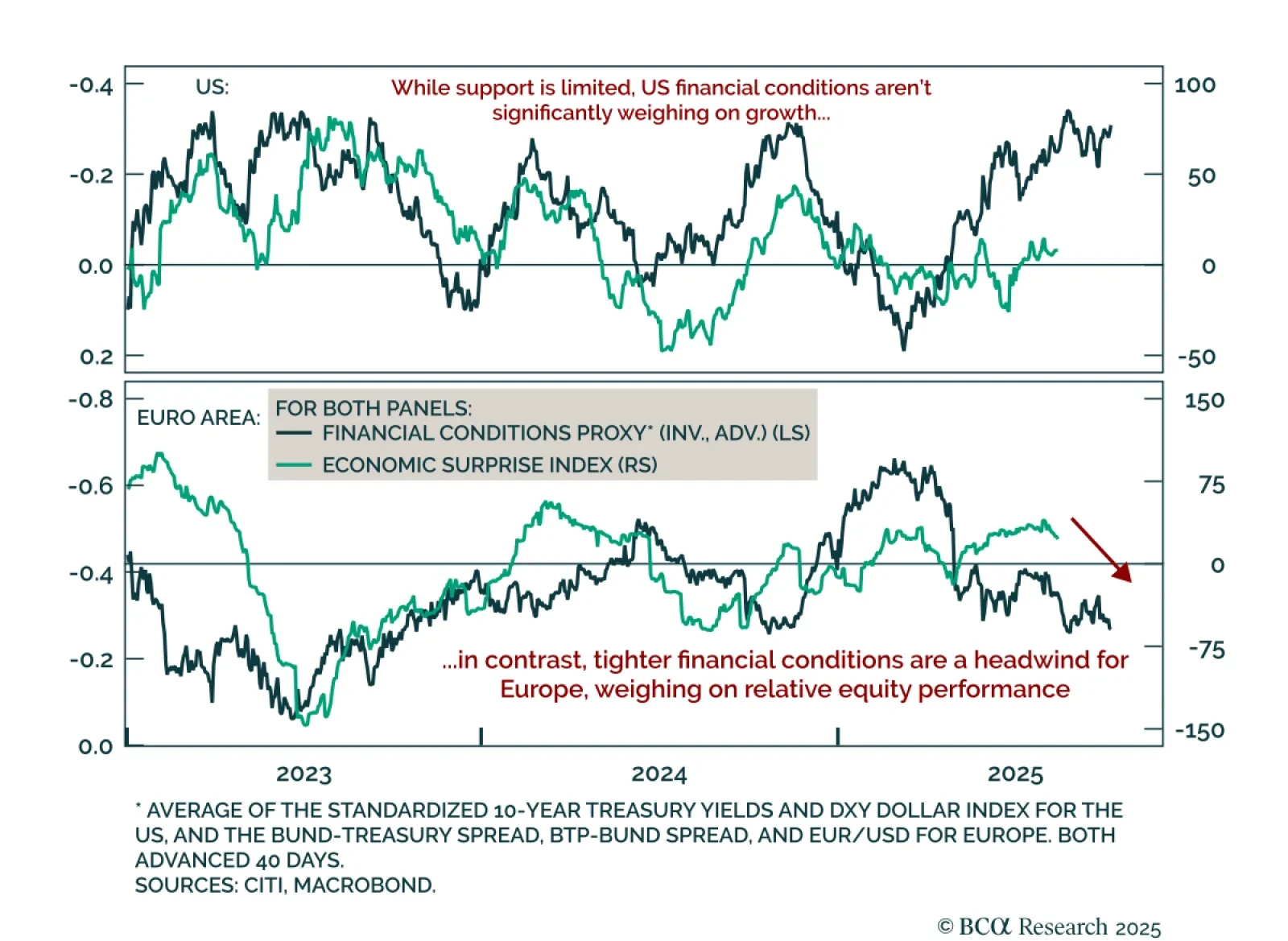

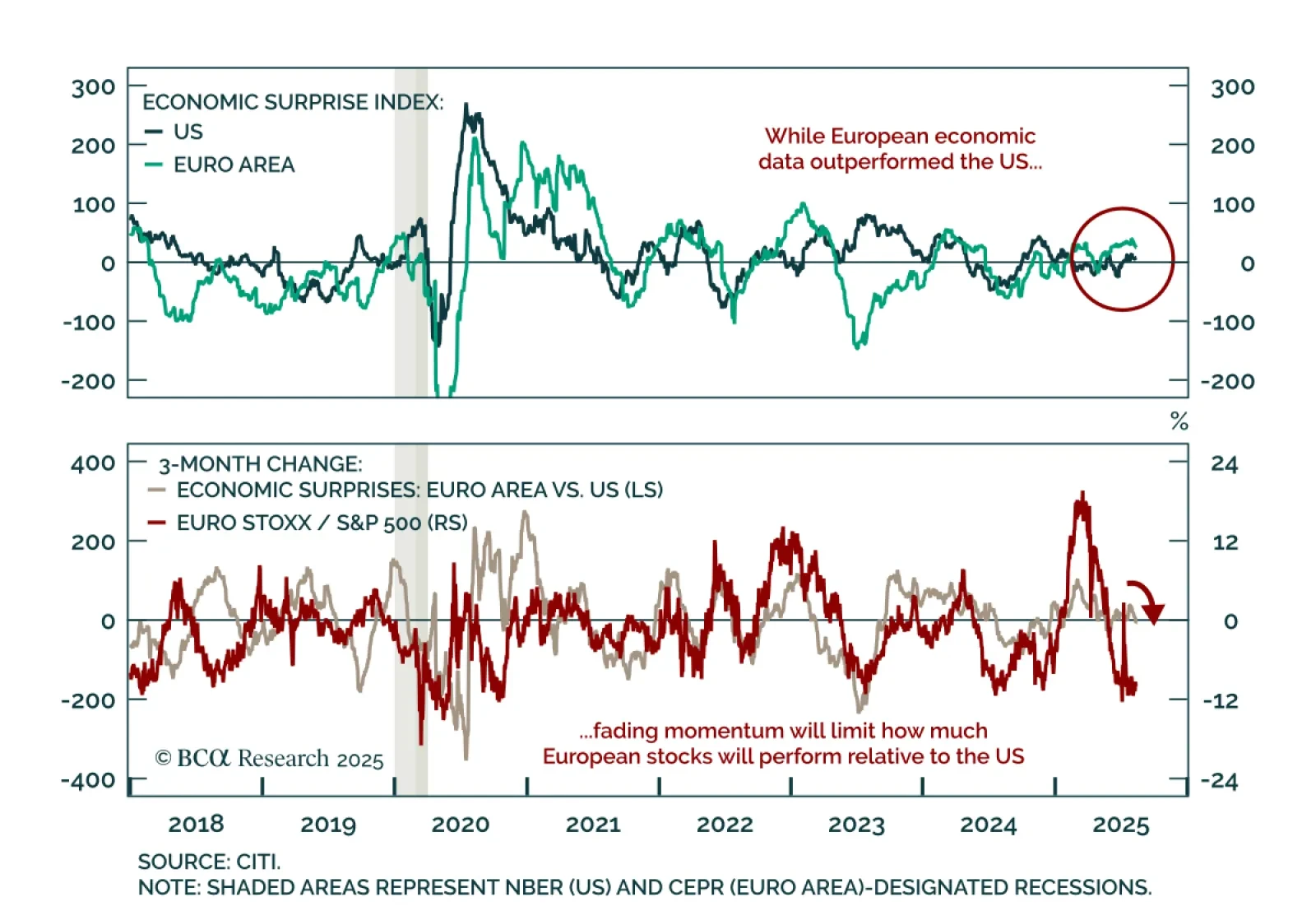

Dollar softness has had little growth impact, and European equities should keep lagging. A key 2025 trend has been USD depreciation, but the associated easing in financial conditions has offered minimal support to US growth, reflecting higher term premia…

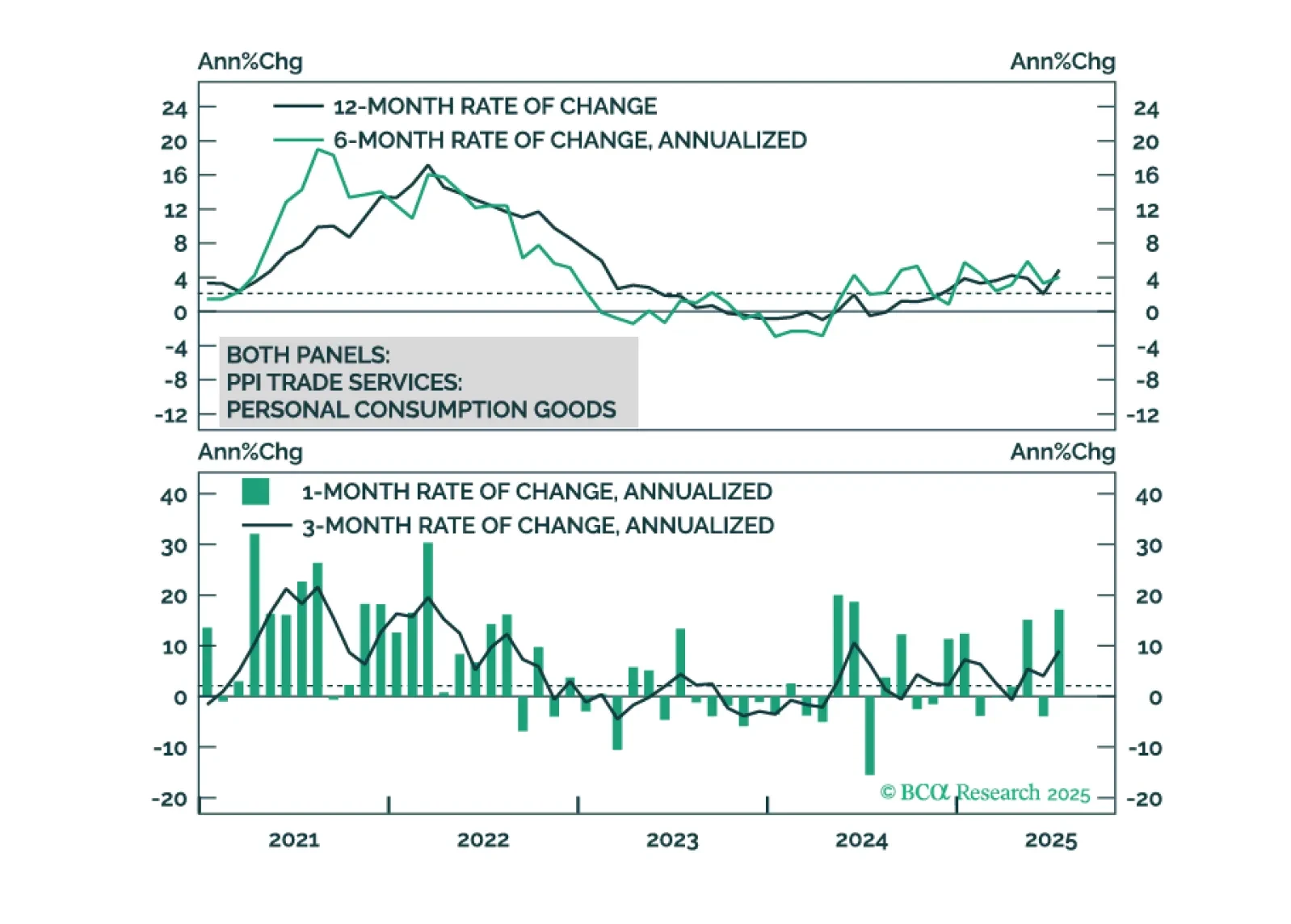

July PPI surprised sharply to the upside, but inflation pressures are likely to remain limited. Headline PPI rose 0.9% m/m (3.3% y/y) in July from 0.0% m/m (2.3% y/y) in June, while core PPI gained 0.6% m/m (2.8% y/y). PPI components feeding into PCE…

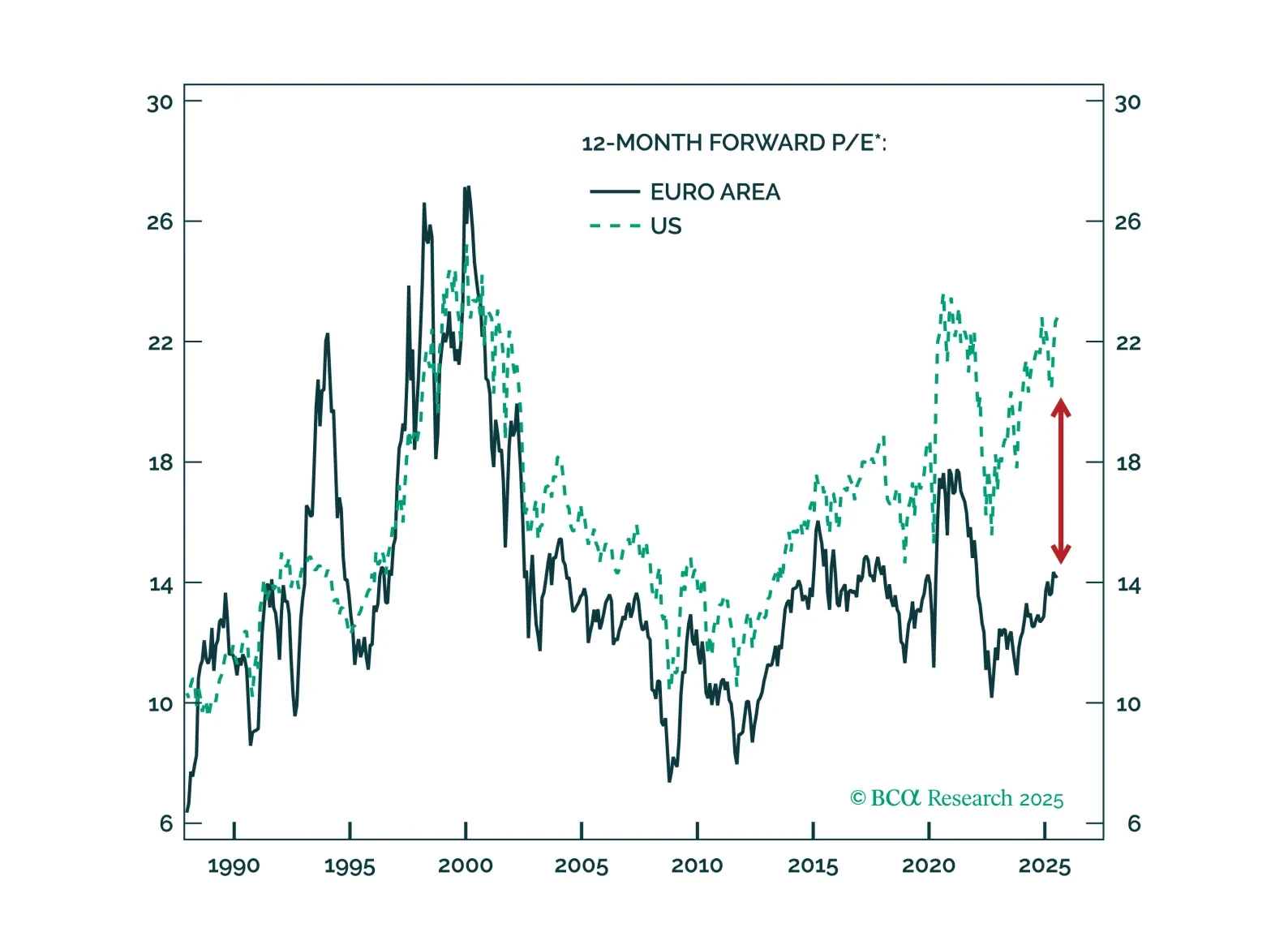

The outlook for European equities is becoming more appealing relative to US equities. Many structural headwinds are fading in Europe, and valuations remain historically cheap. Investors should position accordingly to benefit from the region’s cyclical rerating.

US equities are set for tactical outperformance versus Europe, but dips or underperformance in European assets remain entry points for long-term investors. European stocks have stalled below prior highs, while the S&P 500 has rebounded to record levels…

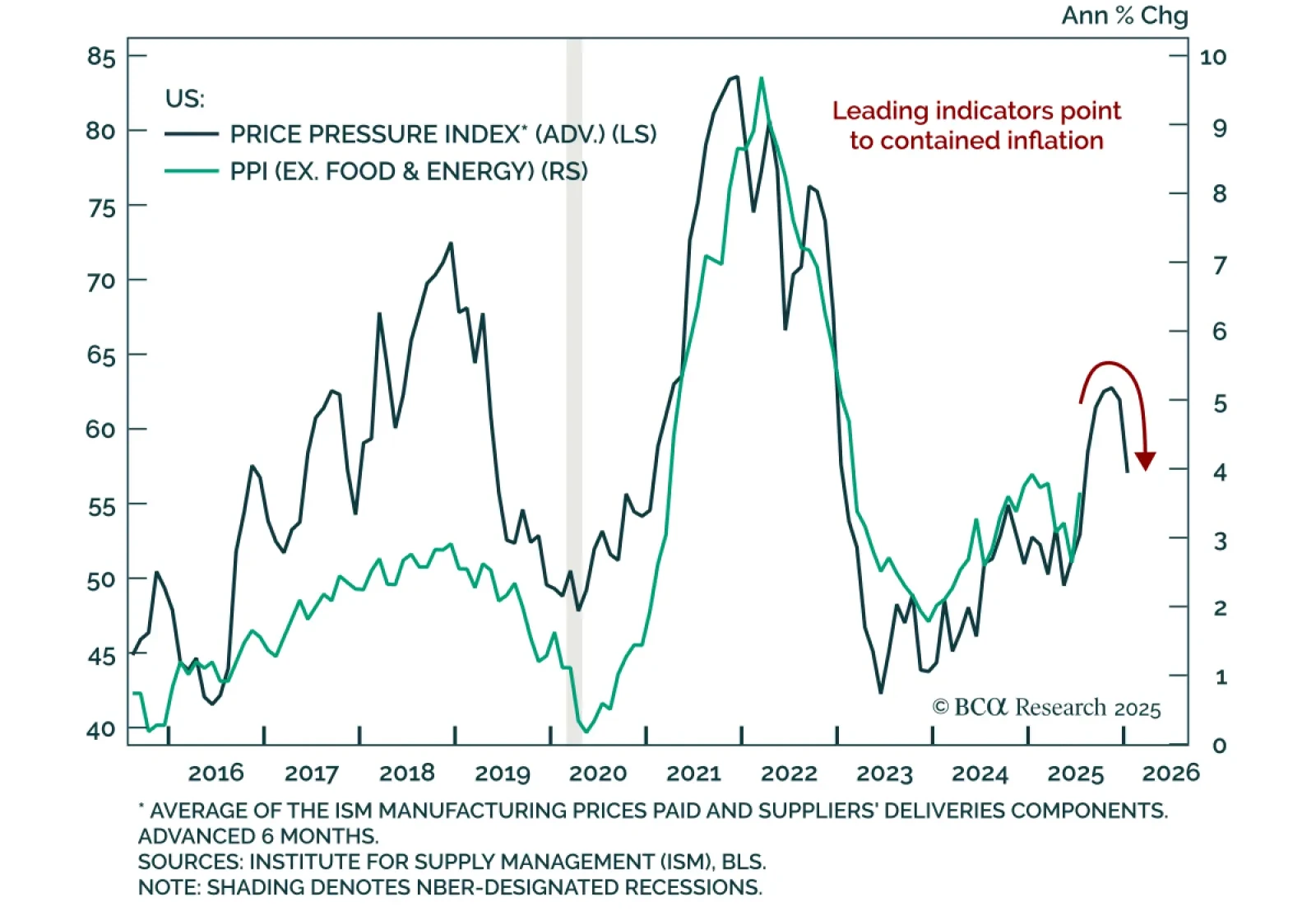

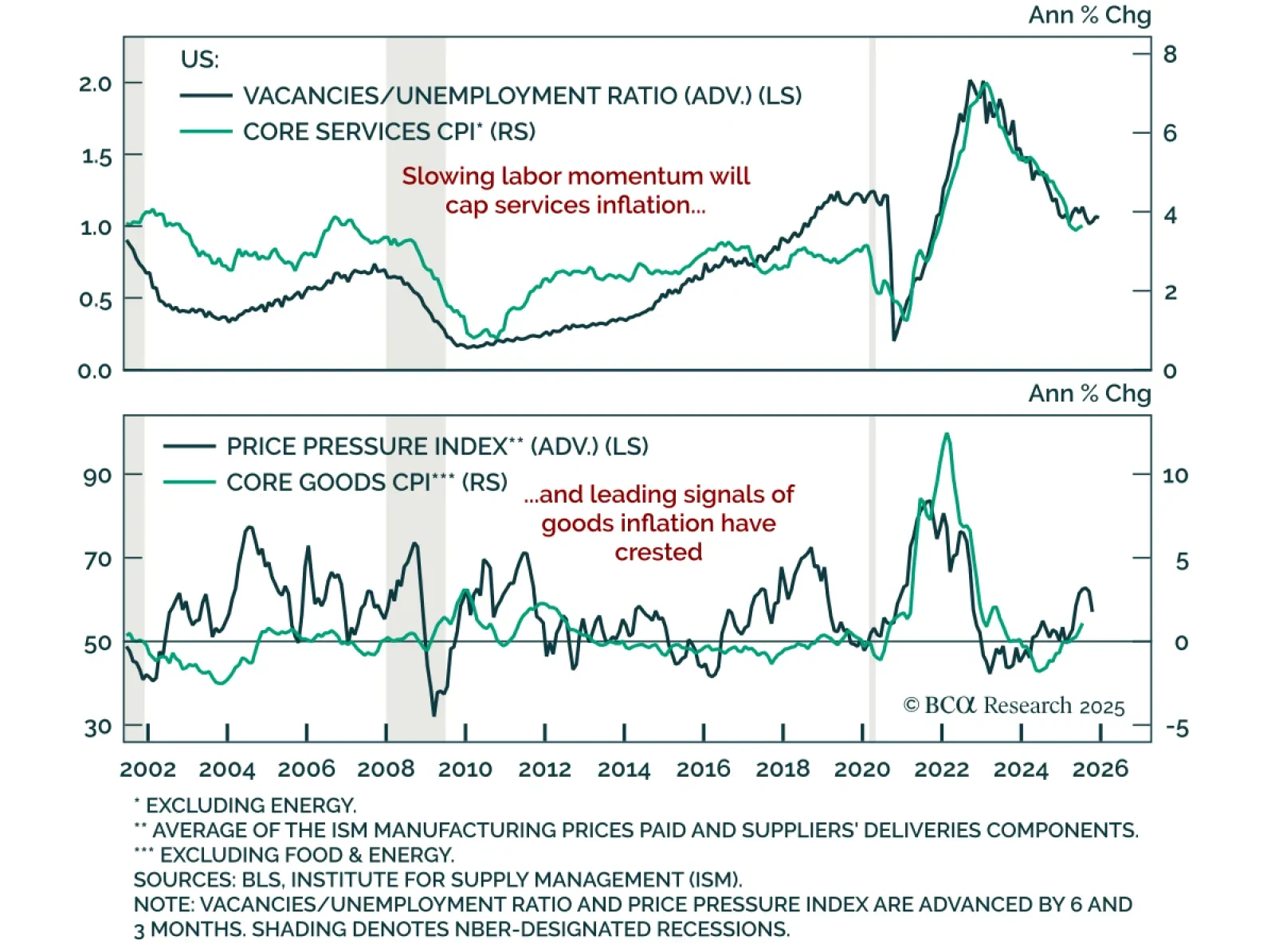

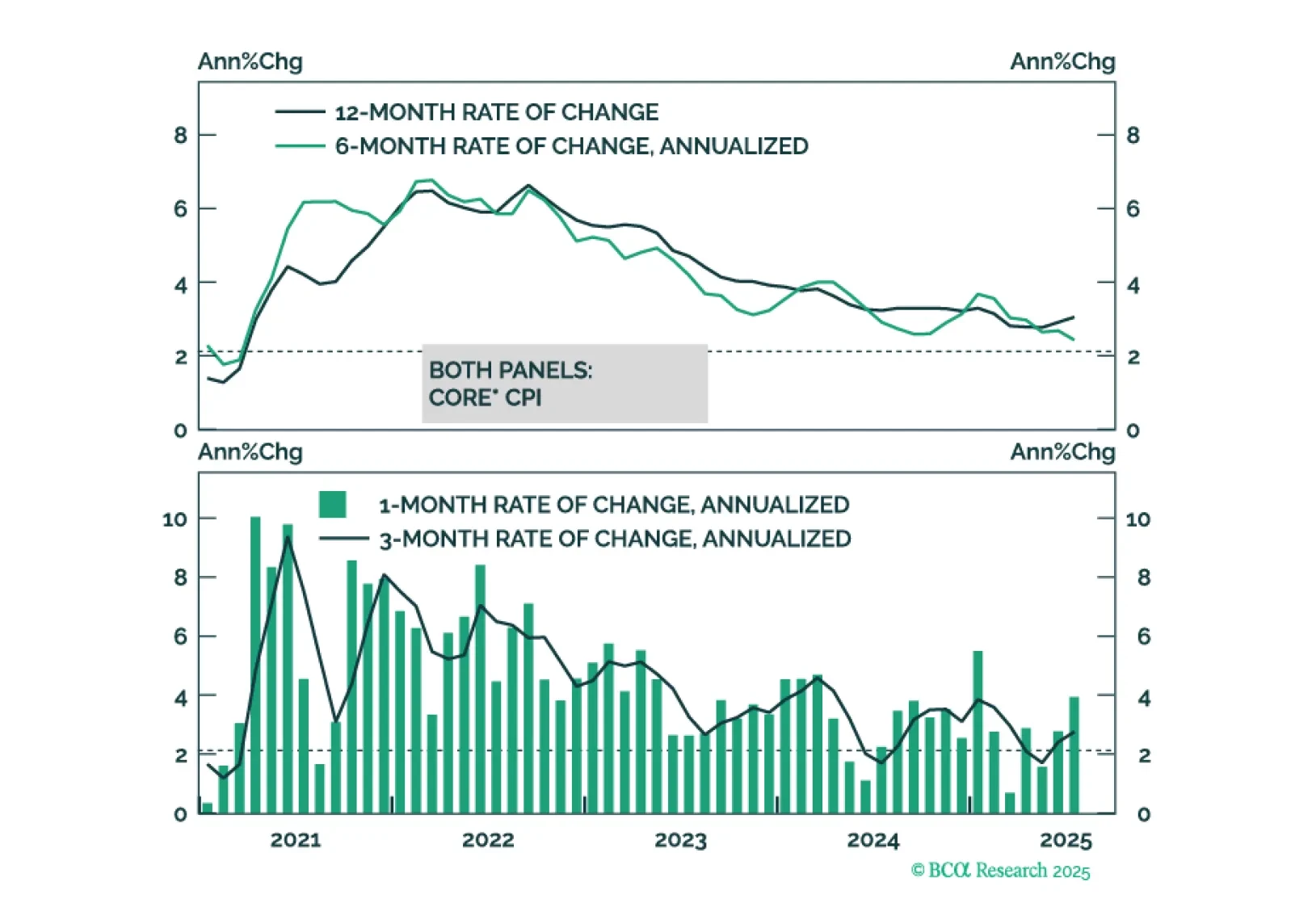

July US CPI met expectations as leading indicators point to disinflation, supporting our long duration stance and preference for 2s5s steepeners. Headline CPI rose 0.2% m/m (2.7% y/y), while core increased 0.3% m/m and accelerated to 3.1% y/y. Both goods…

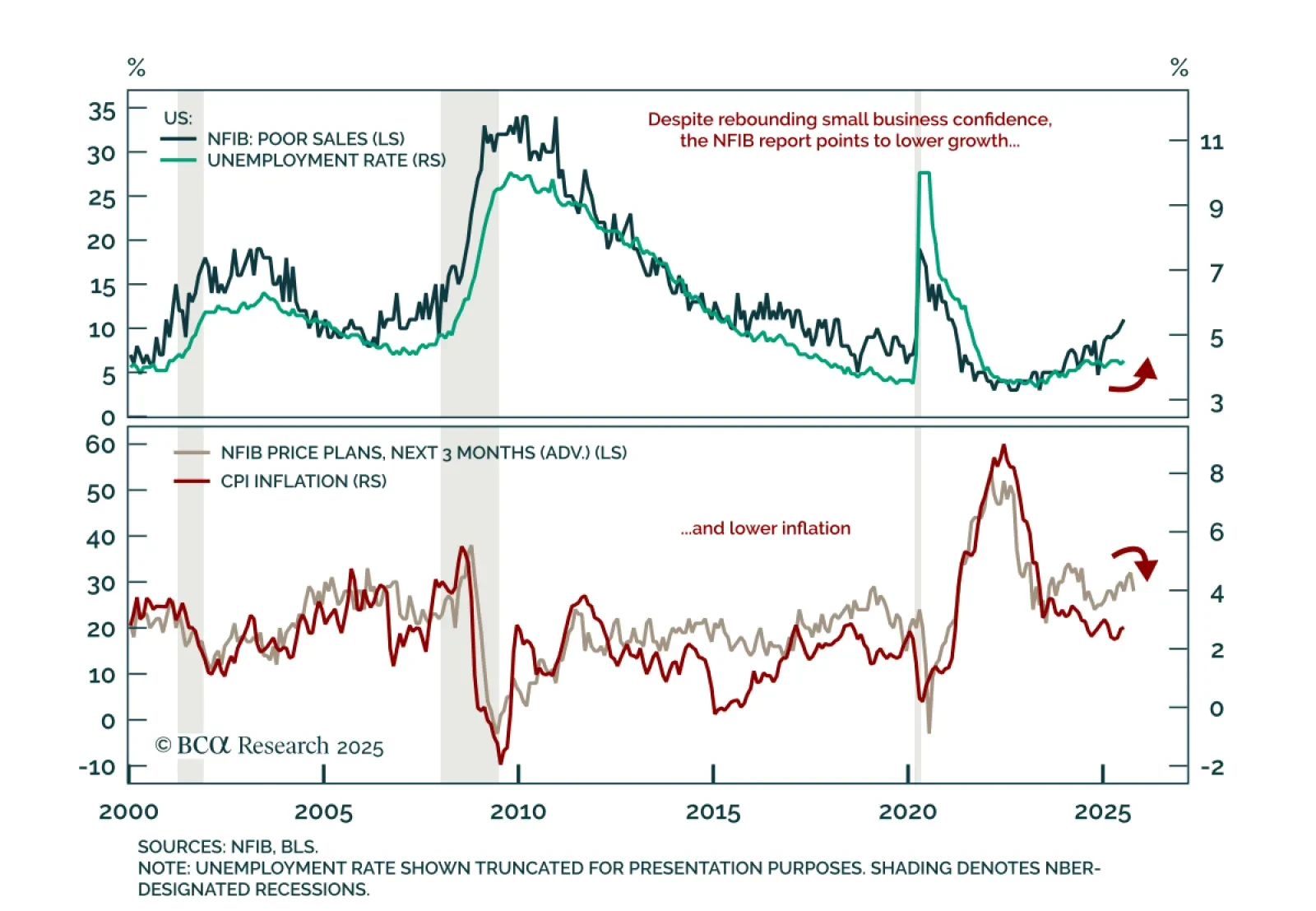

The July NFIB survey showed a rebound in expectations, but underlying weakness reinforces left-tail risks and supports a moderate risk-off allocation. The headline index rose to 100.3, a five-month high, but remains below December 2024 levels. The…

This morning’s CPI report marginally tips the scales in favor of a September rate cut.

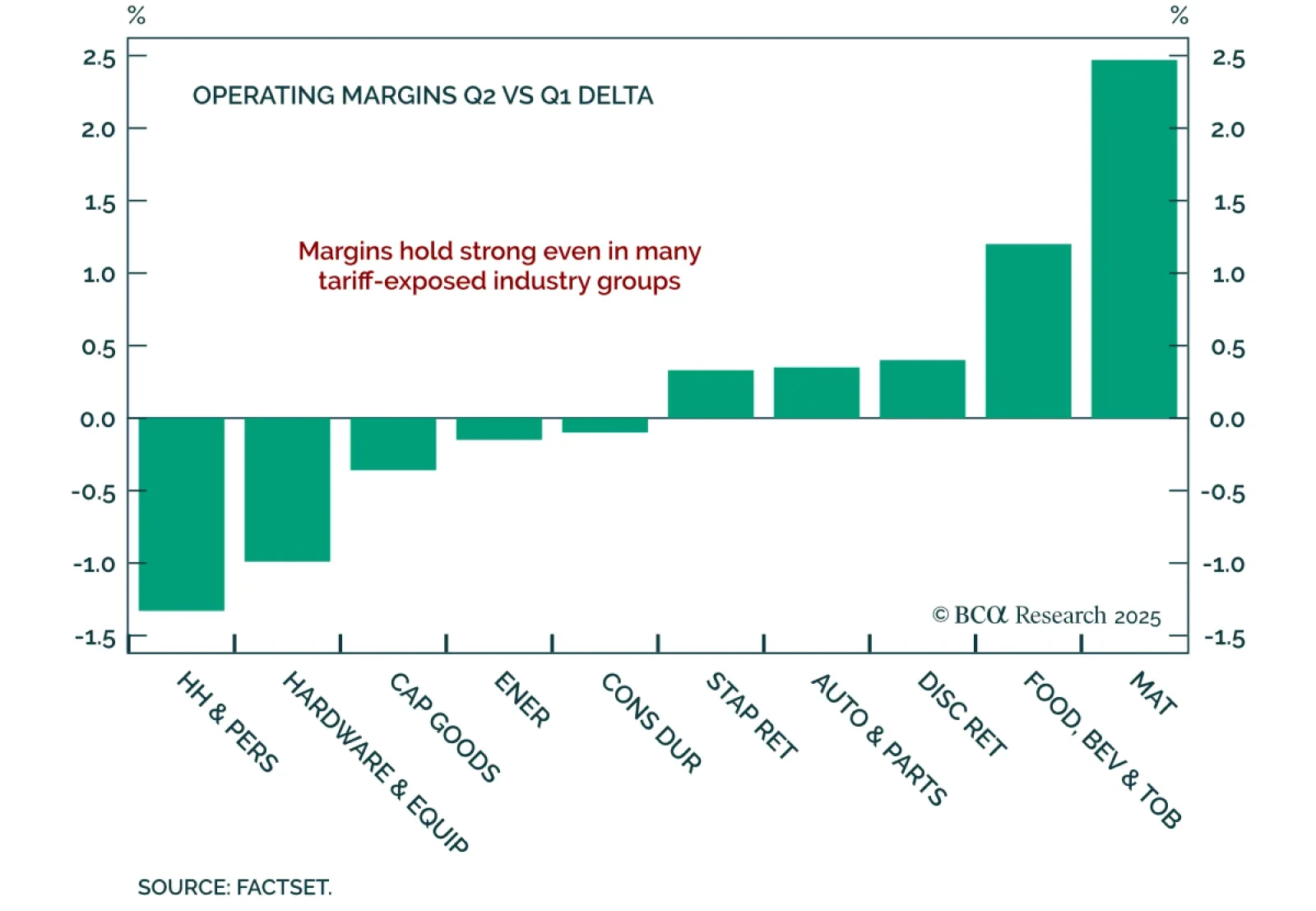

Our US Equity strategists view Q2 earnings as confirmation of corporate resilience, but caution that the full impact of tariffs is still ahead. Strong results show that companies have weathered tariff-related costs through effective mitigation…