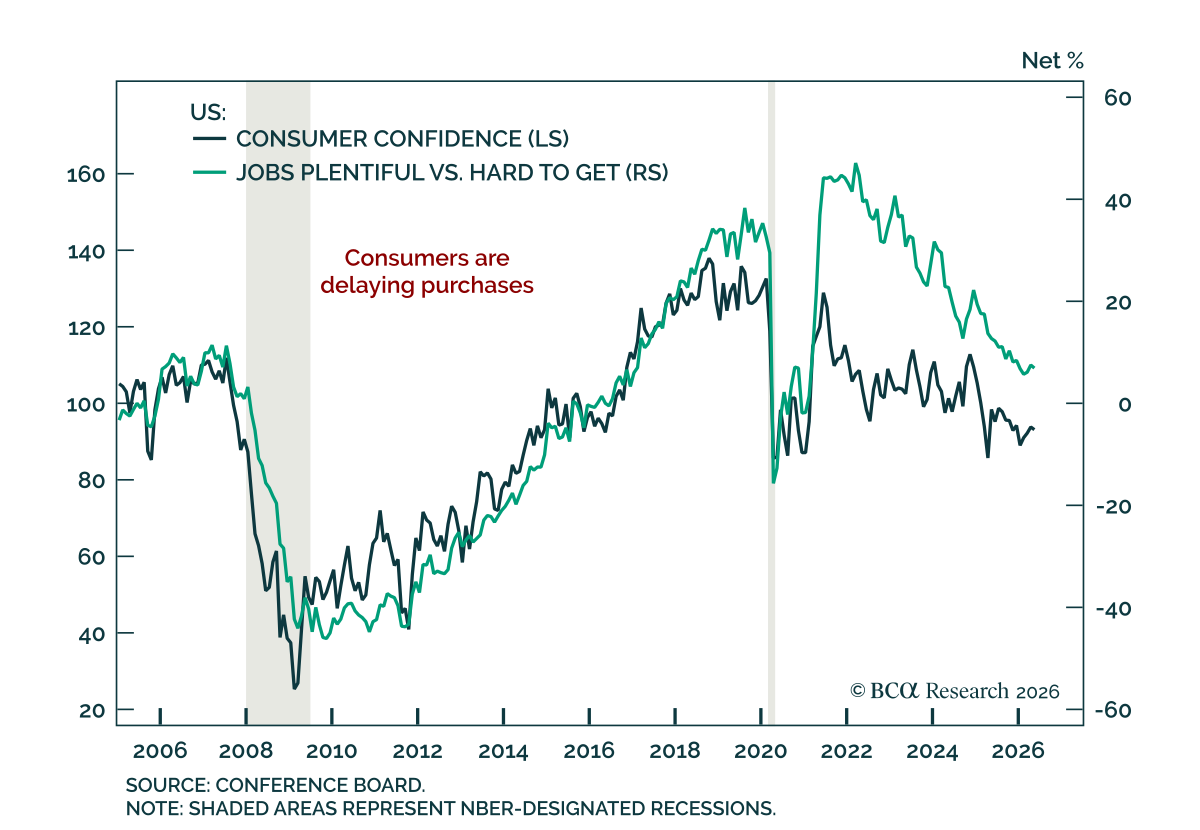

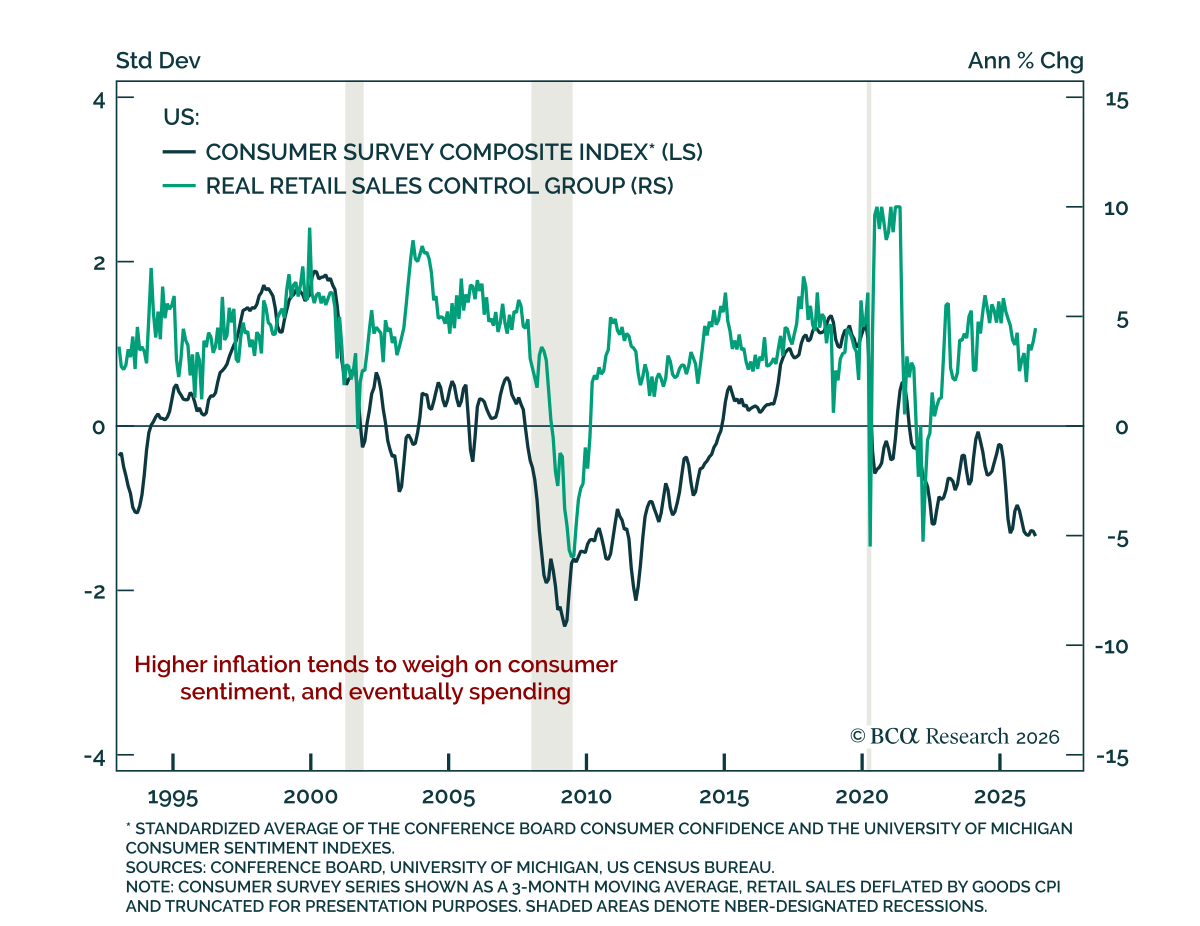

Consumer

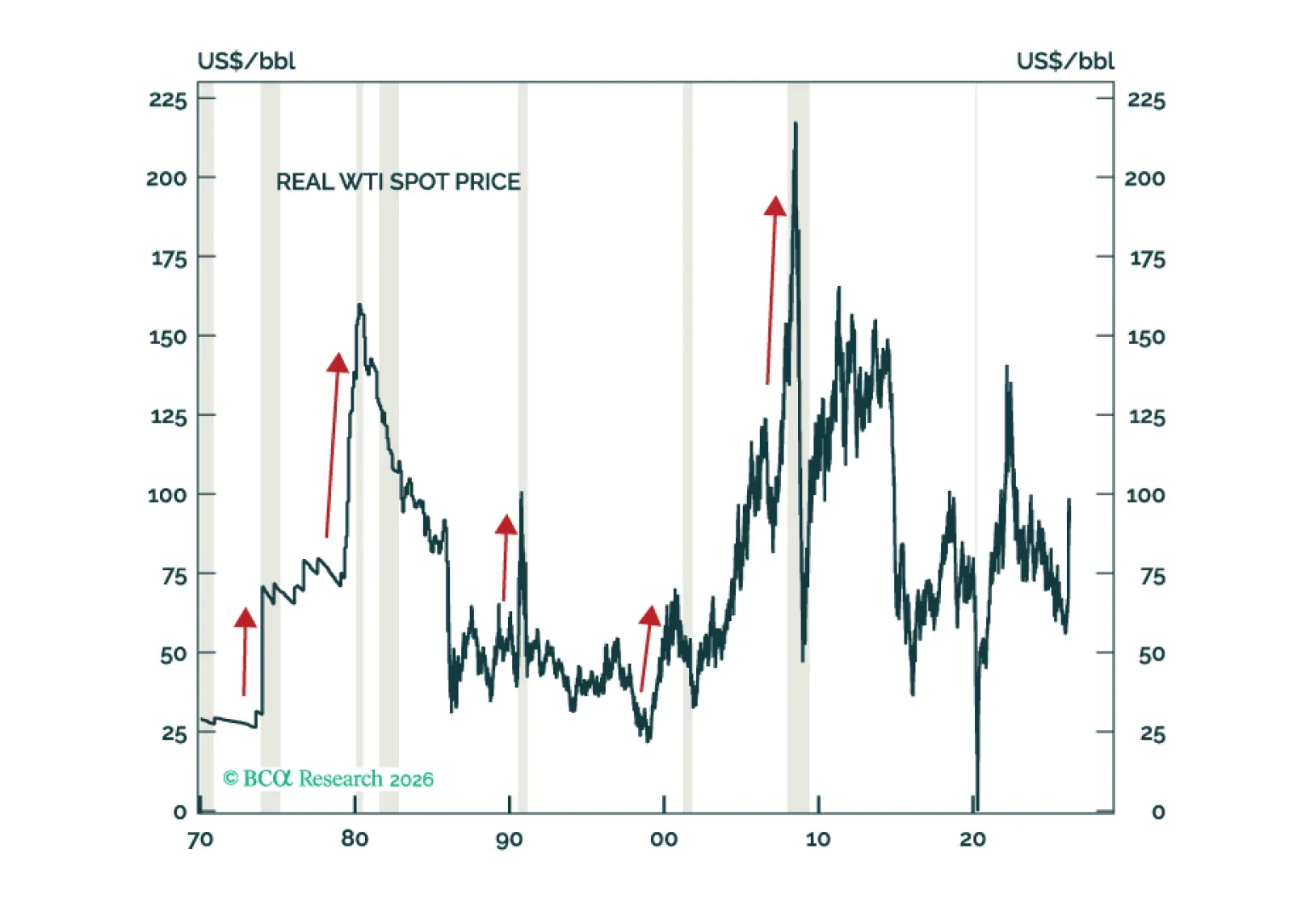

The global economy has weathered the oil shock reasonably well so far. However, the risk of a recession will increase meaningfully if the Strait of Hormuz remains closed into June.

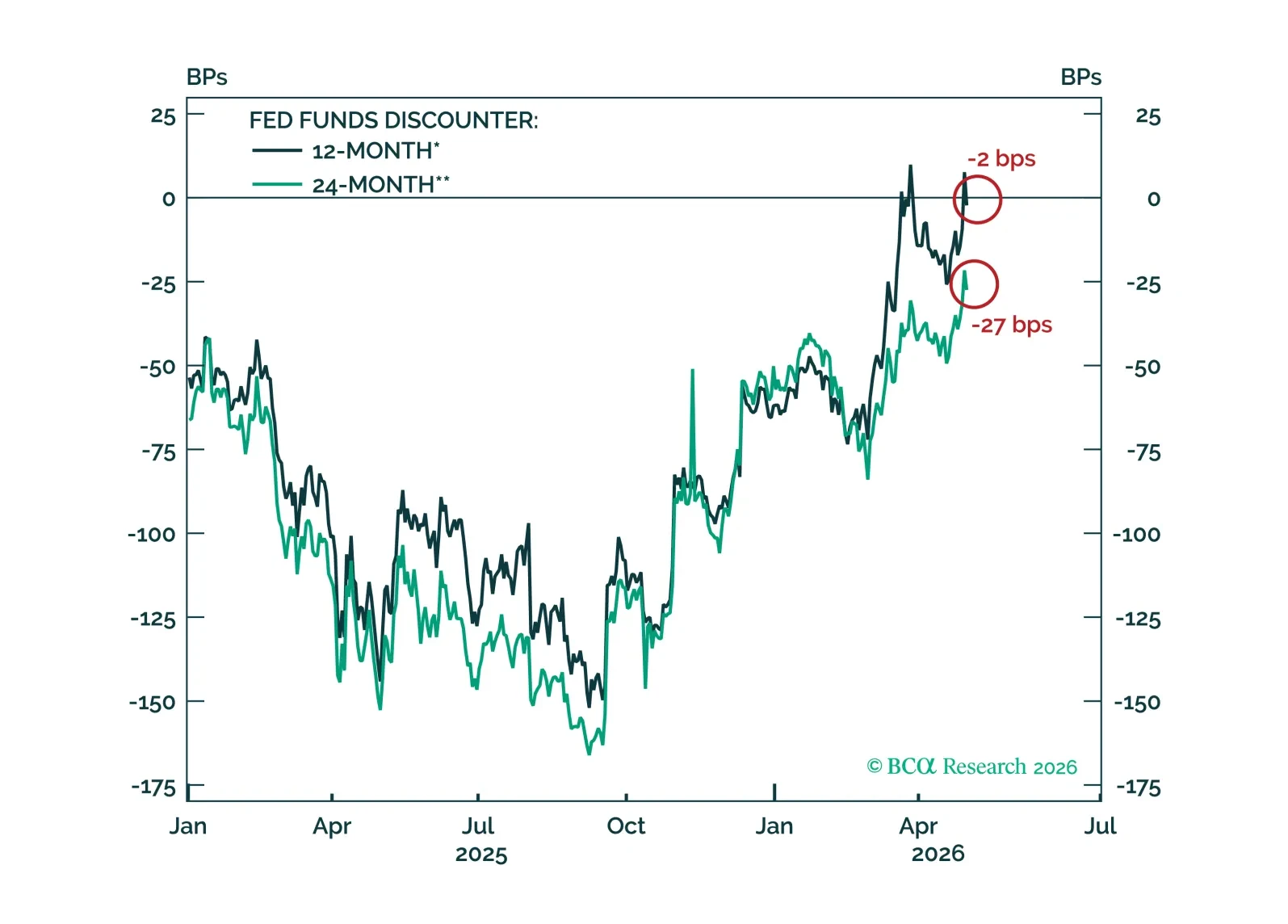

So far, there is no evidence of second-round effects from the oil price shock showing up in the US economy. Fed rate hikes are off the table unless those effects emerge.

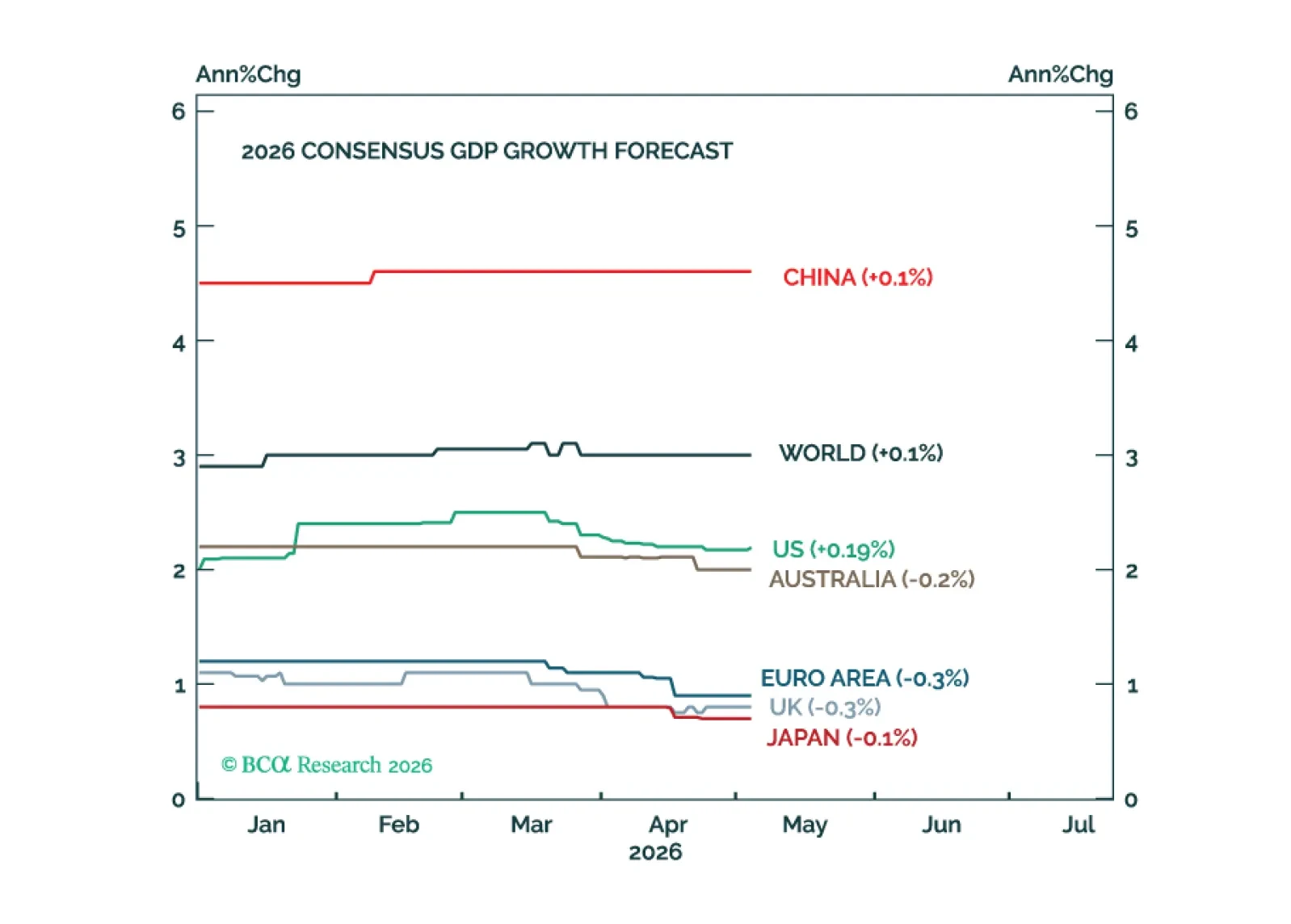

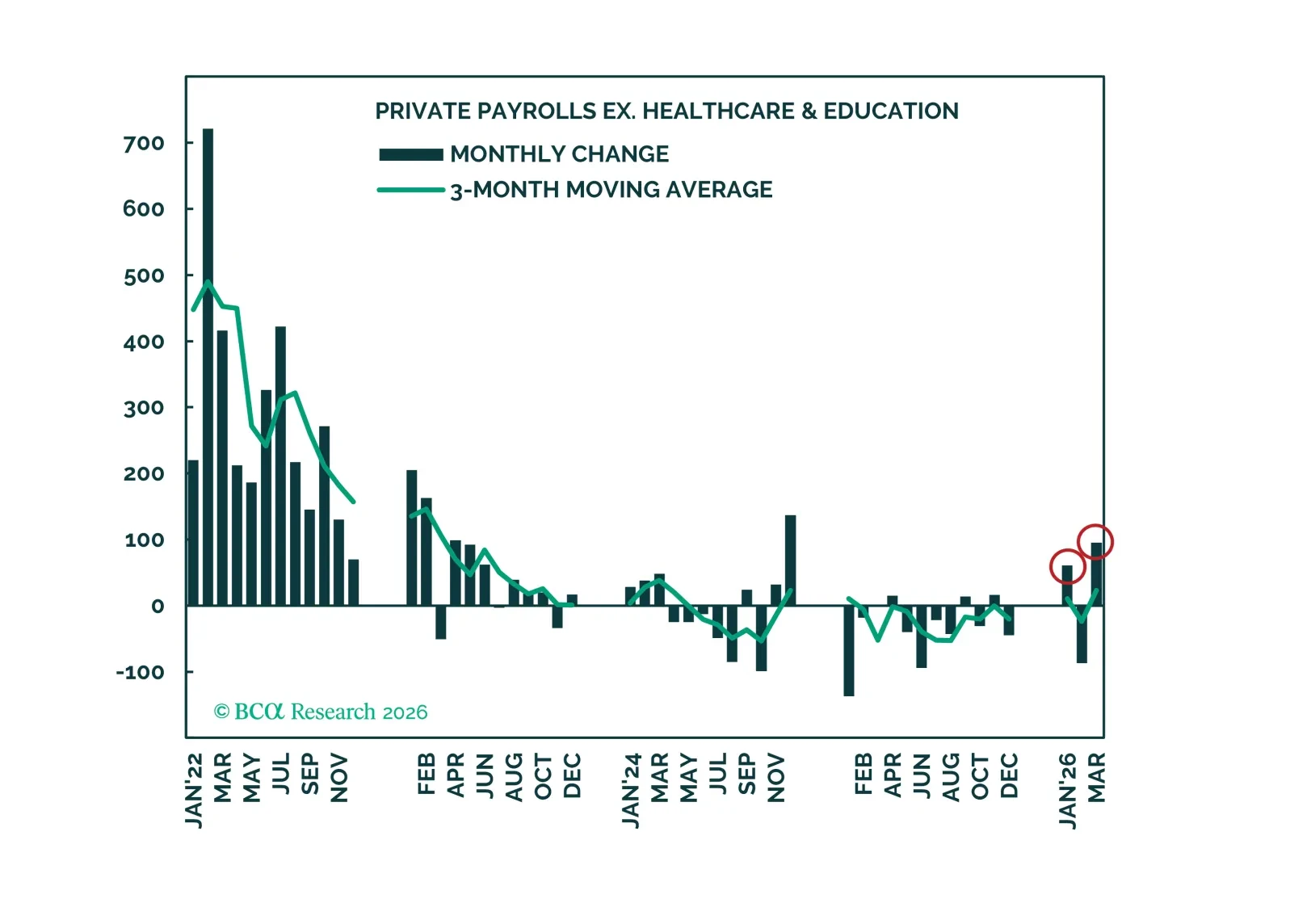

The labor market showed signs of reviving in the first three months of this year, but it is yet to be determined how consumers will react to the energy supply shock. We reiterate our benchmark asset allocation recommendations, but are skeptical that S&P 500 earnings growth will meet outsized expectations over the rest of 2026.

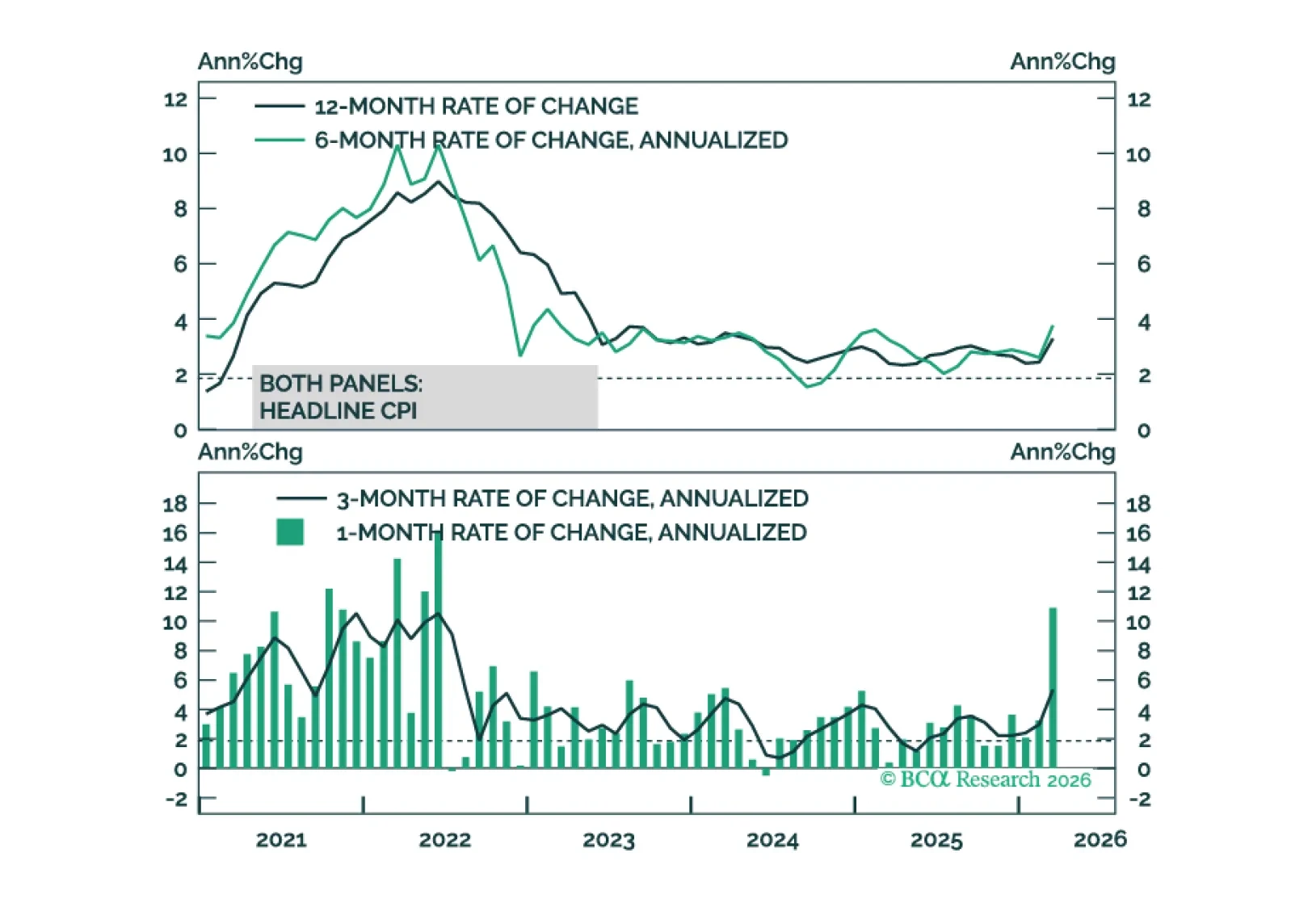

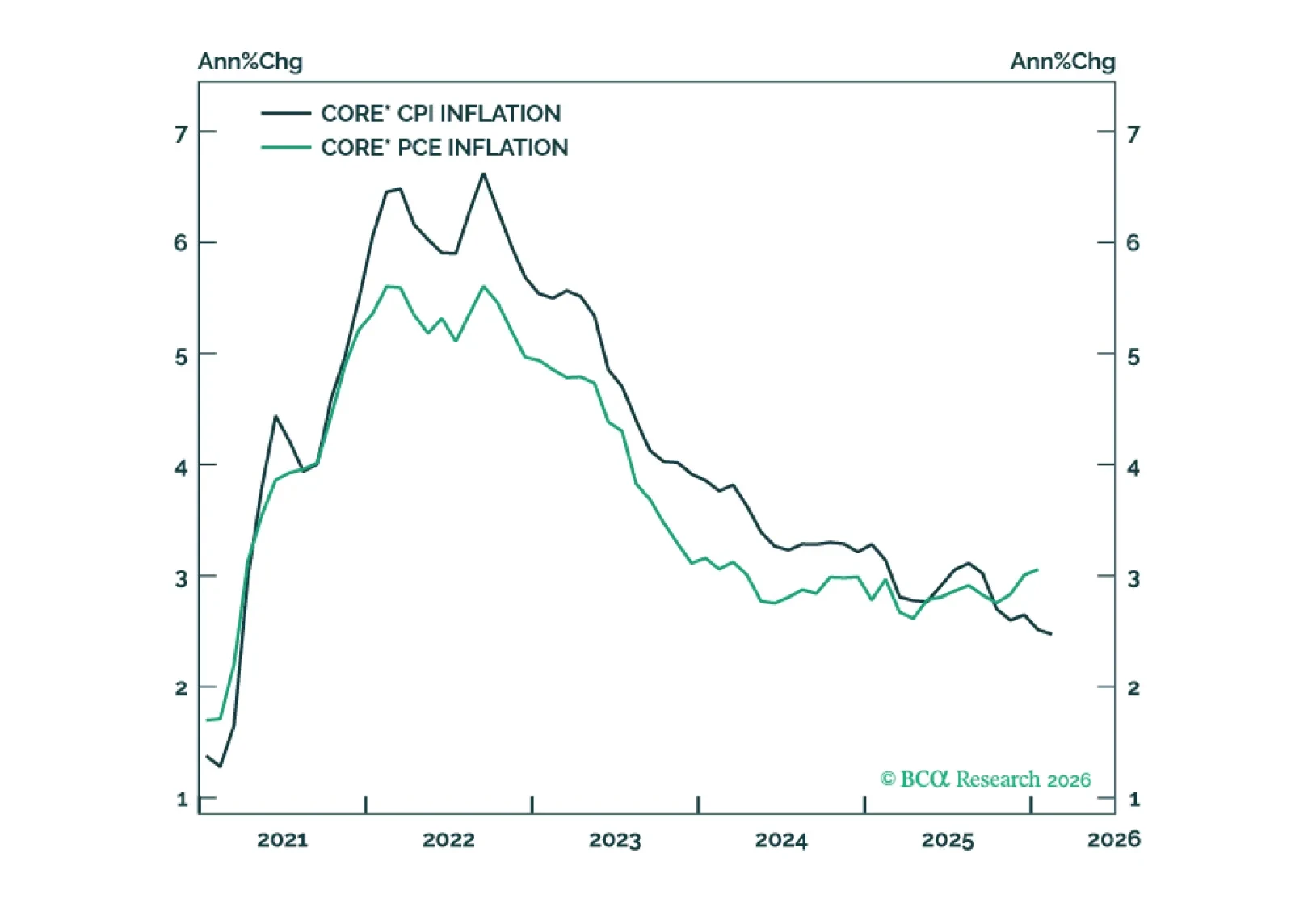

Inflation’s underlying trend was headed lower prior to the Iran war. This makes the recent back-up in bond yields look like an attractive buying opportunity.

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

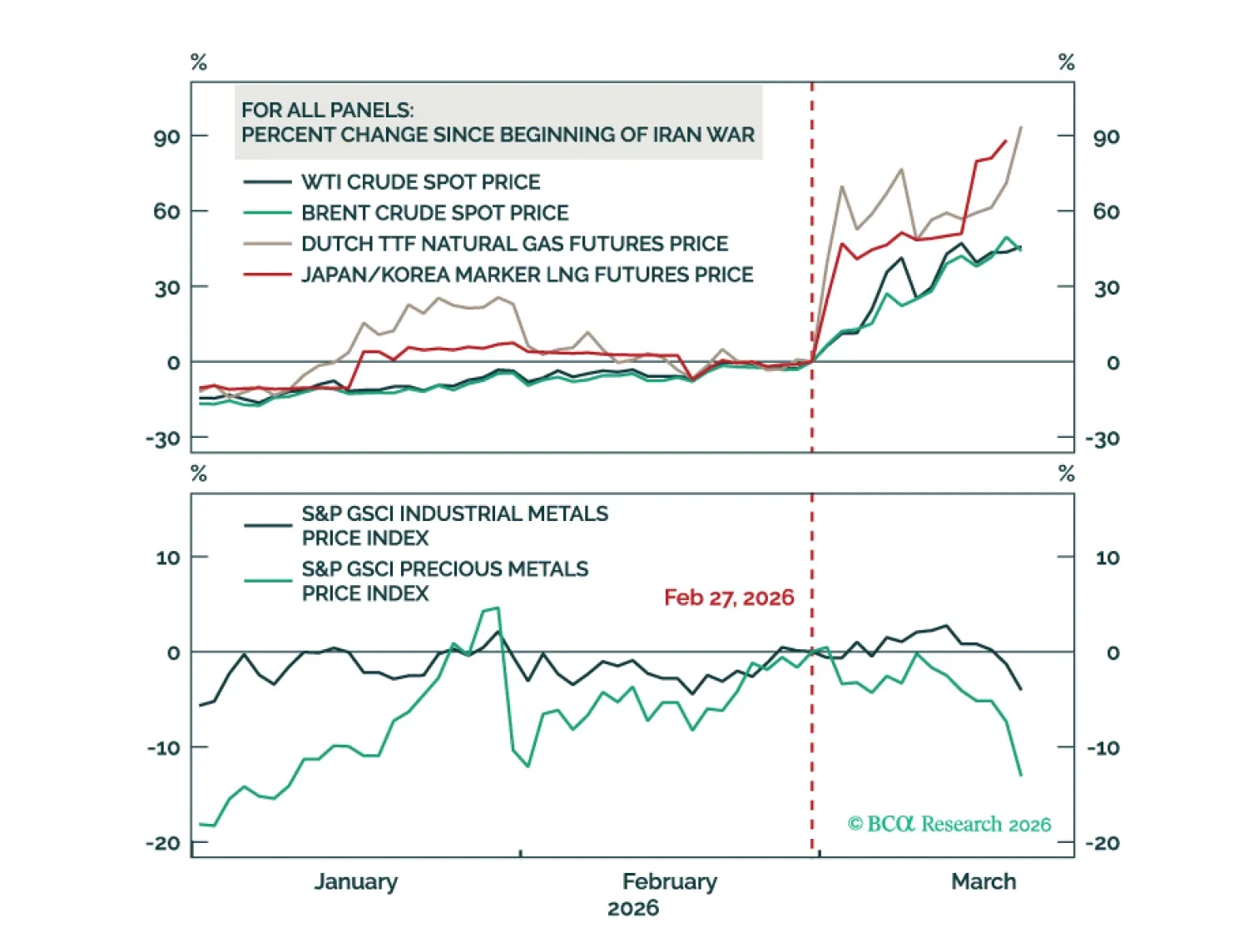

Higher oil prices threaten the global economy, warranting an underweight stance on equities. Over the long haul, industrial metals will fare better than crude.

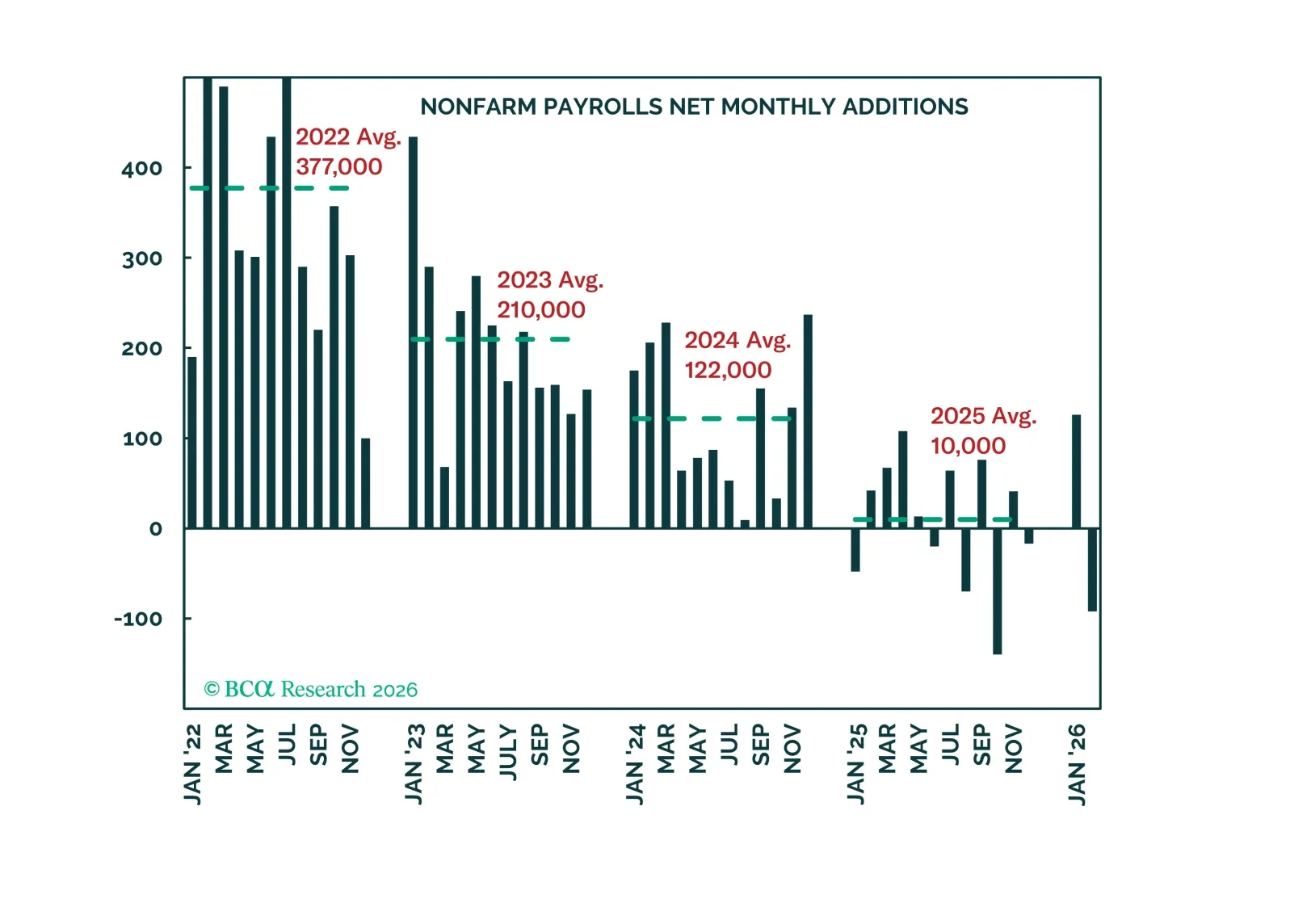

Job creation remains stalled, but consumers are carrying on and S&P 500 earnings have been growing by double digits. Although the repercussions from the war in the Middle East are not yet clear, the US economy was doing just fine before it began.

The gap between PCE and CPI inflation will narrow within the next few months, mostly driven by core PCE inflation converging toward its trimmed mean.