Equities

Expectations for US inflation at 3.3 percent are inconsistent with expectations for the Fed to slash rates, so one of these expectations is likely wrong. We describe how to play this mispricing. Plus, a new position is to go overweight global consumer discretionary (RXI).

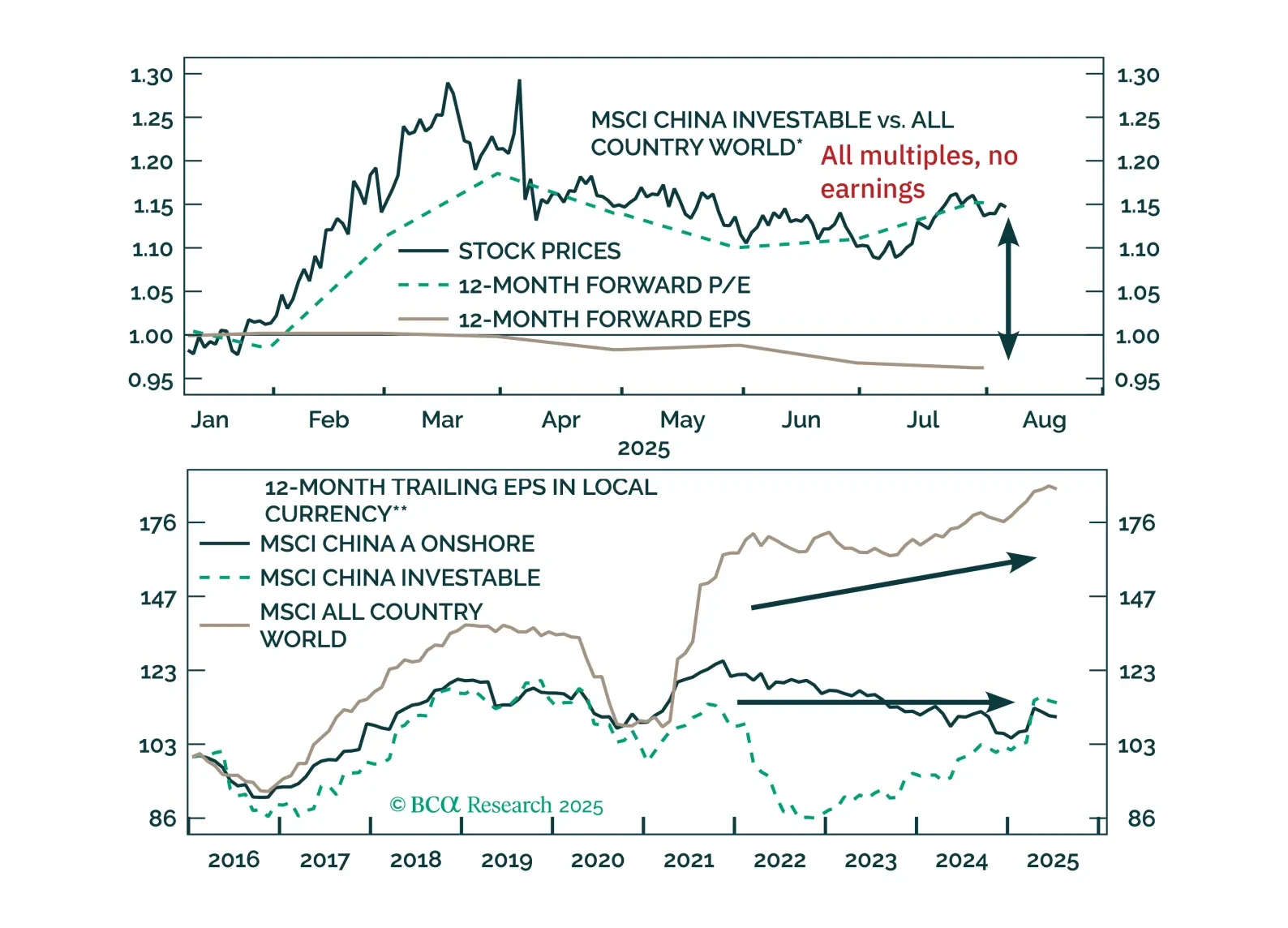

Chinese stock prices have significantly decoupled from the country’s business cycle, with the full impact of US tariffs yet to be realized. The valuation-driven equity gains without a cyclical economic recovery will be vulnerable to a reversal.

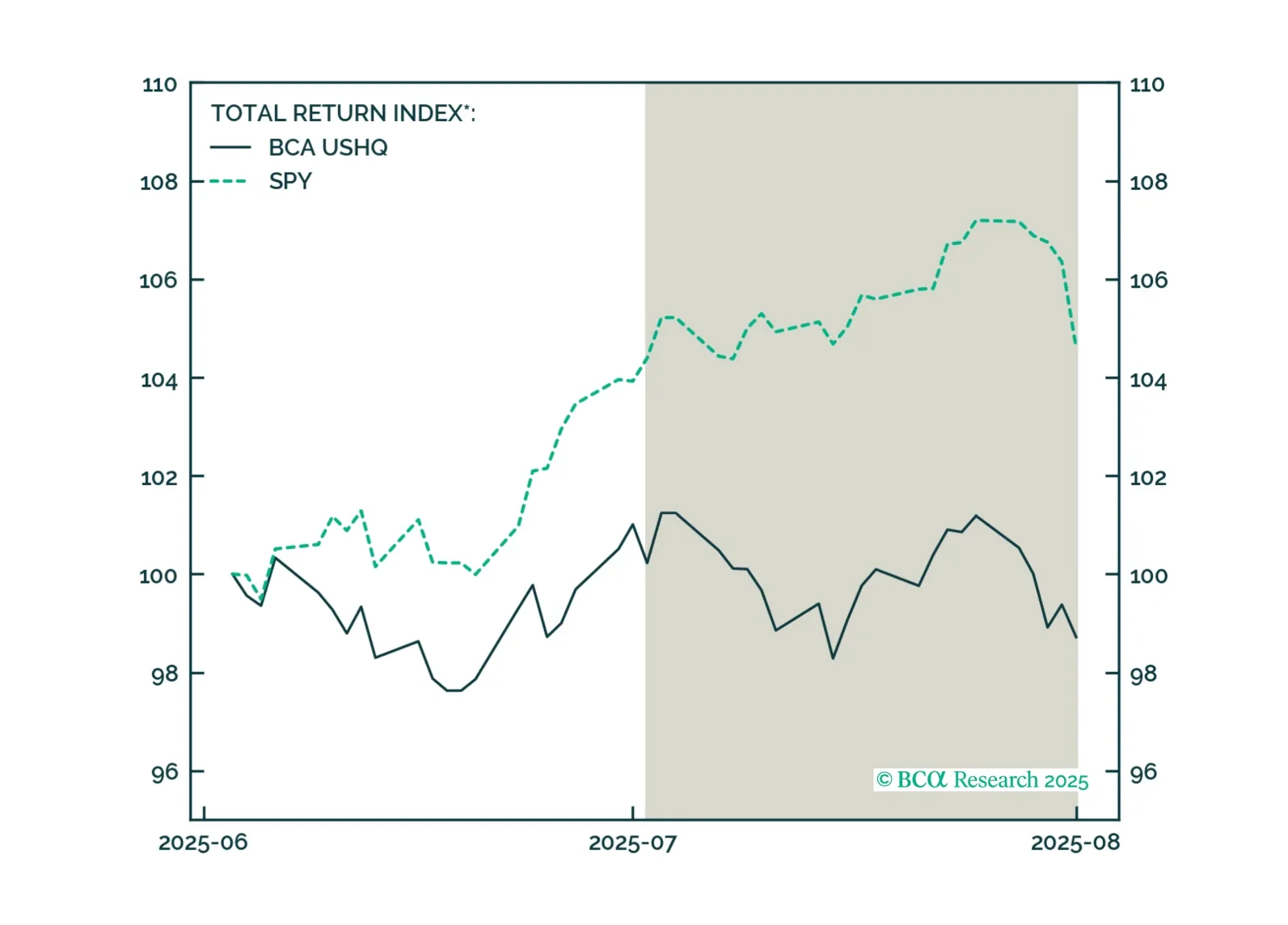

The US High Quality (USHQ) portfolio underperformed its benchmark through July, returning -1.5%, whilst its SPY benchmark returned 0.2%. On a trailing three-month basis, performance was notably weak vs. benchmark, with USHQ underperforming by approx. 750bps.

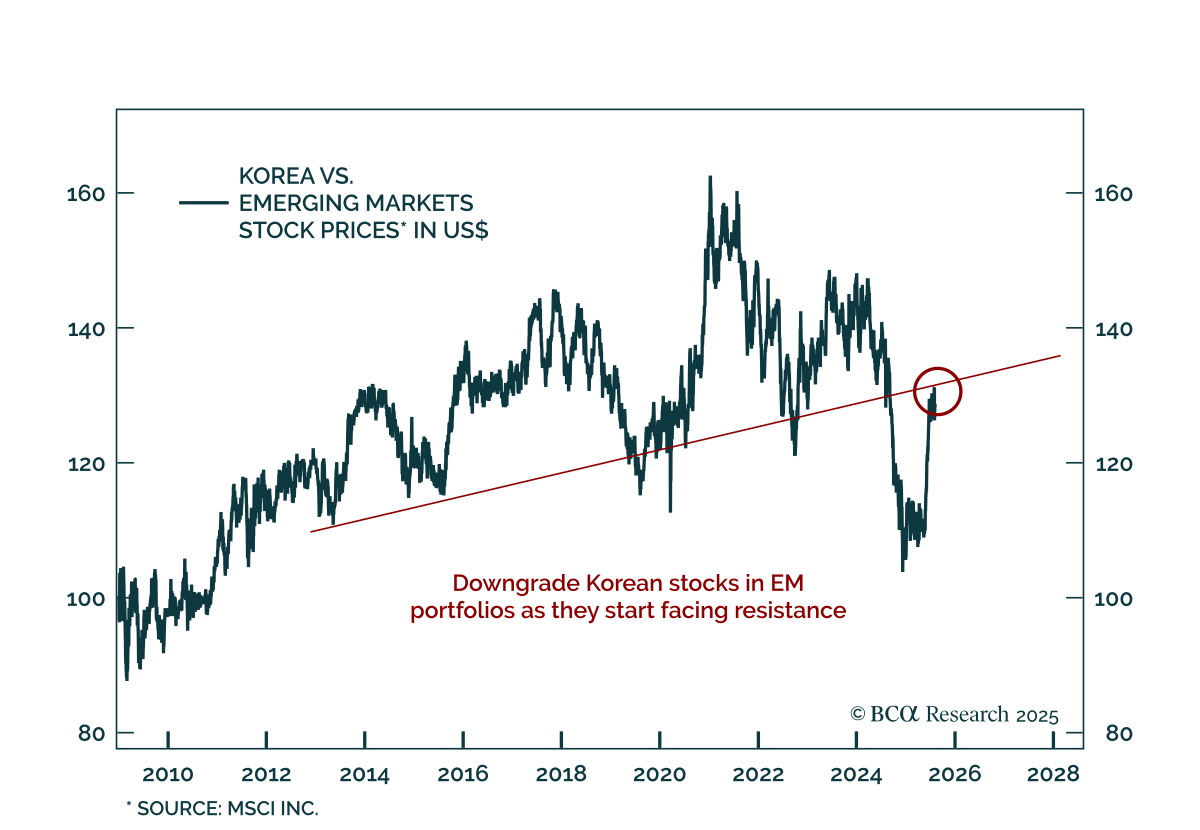

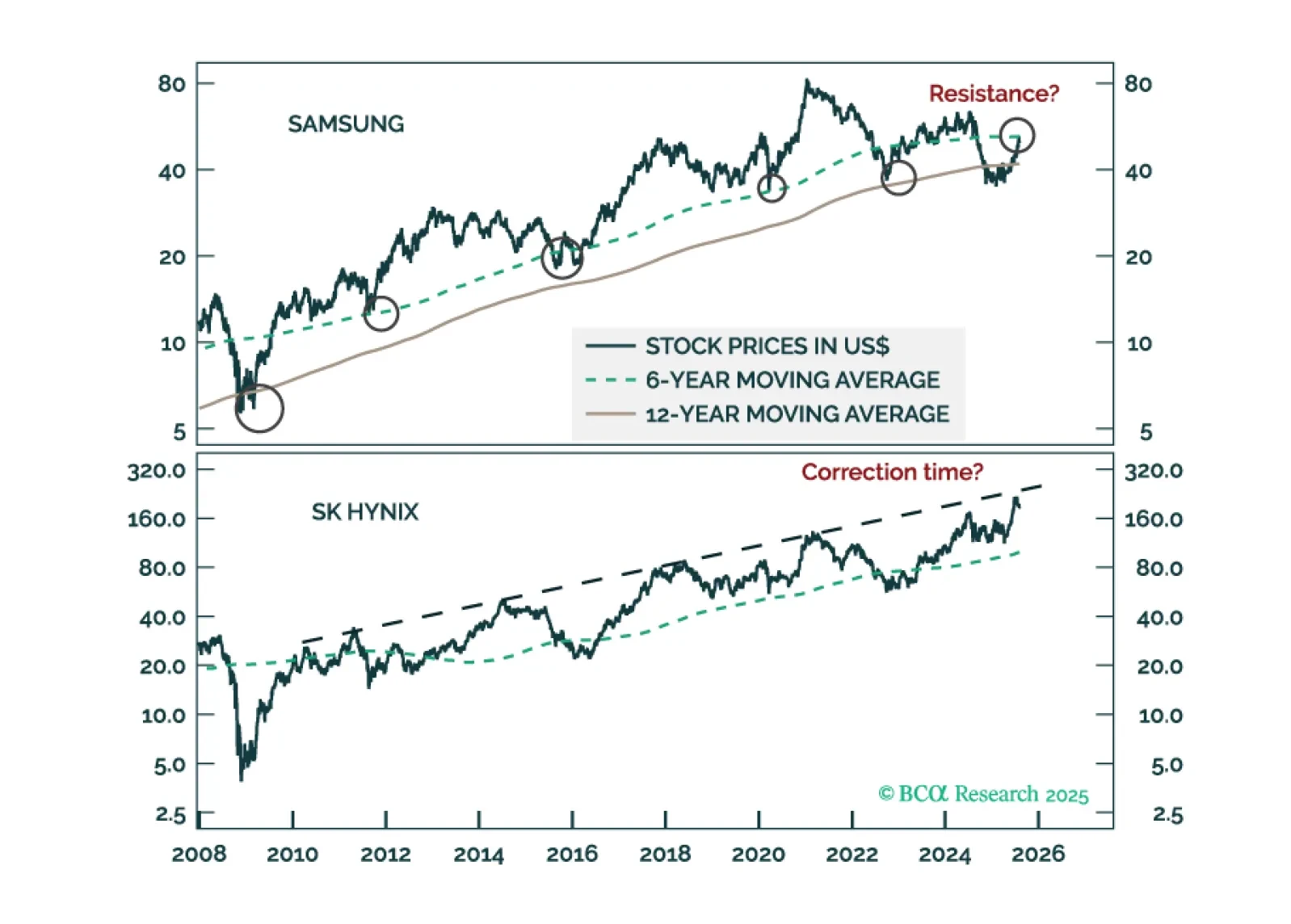

A deflationary shock from shrinking exports will ripple throughout the Korean economy. We are downgrading the KOSPI from overweight to neutral and reiterating a long position in 10-year domestic bonds, currency unhedged.

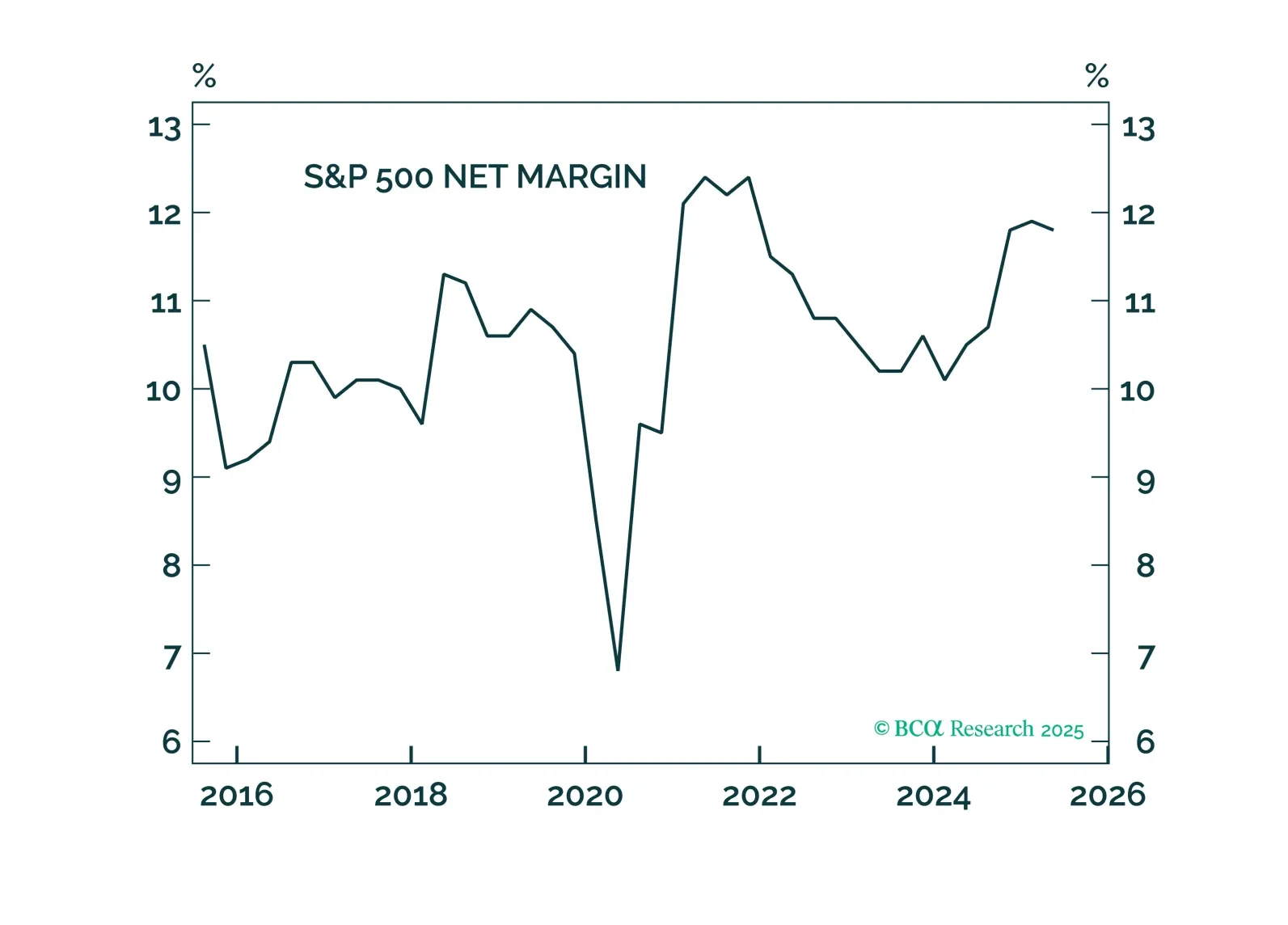

The Q2 reporting season underscores the resilience of corporate earnings, supporting our bullish outlook for equities, an outlook further bolstered by expectations of fiscal and monetary easing. However, for now, we are booking profits, closing overweights in Technology and Growth, and initiating a new overweight in Real Estate.