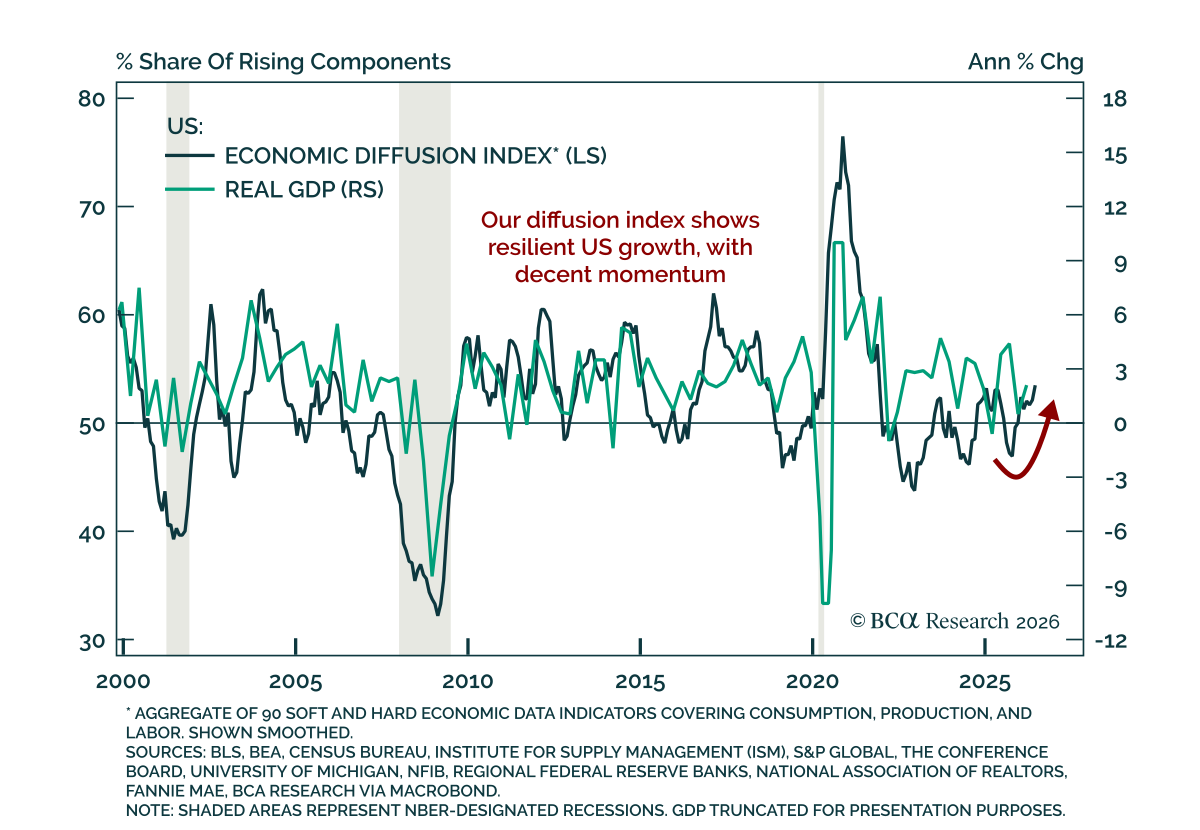

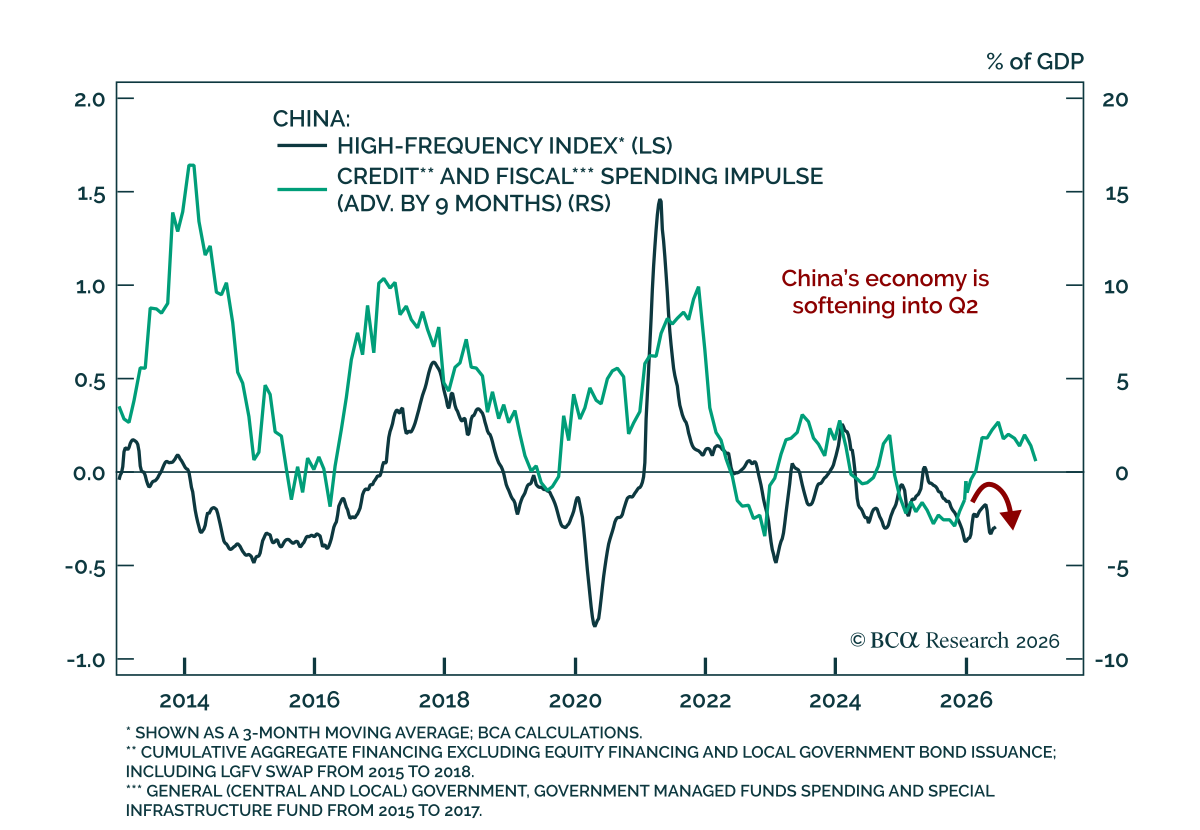

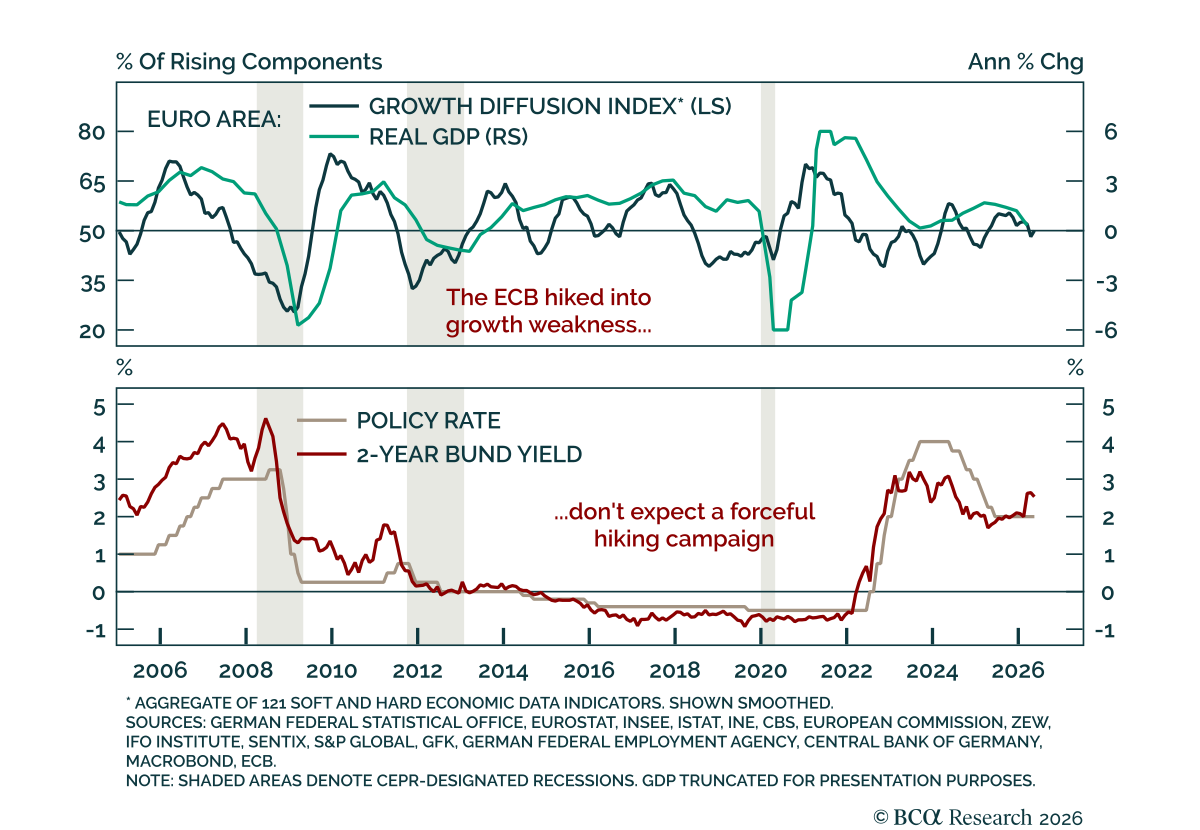

Economic Growth

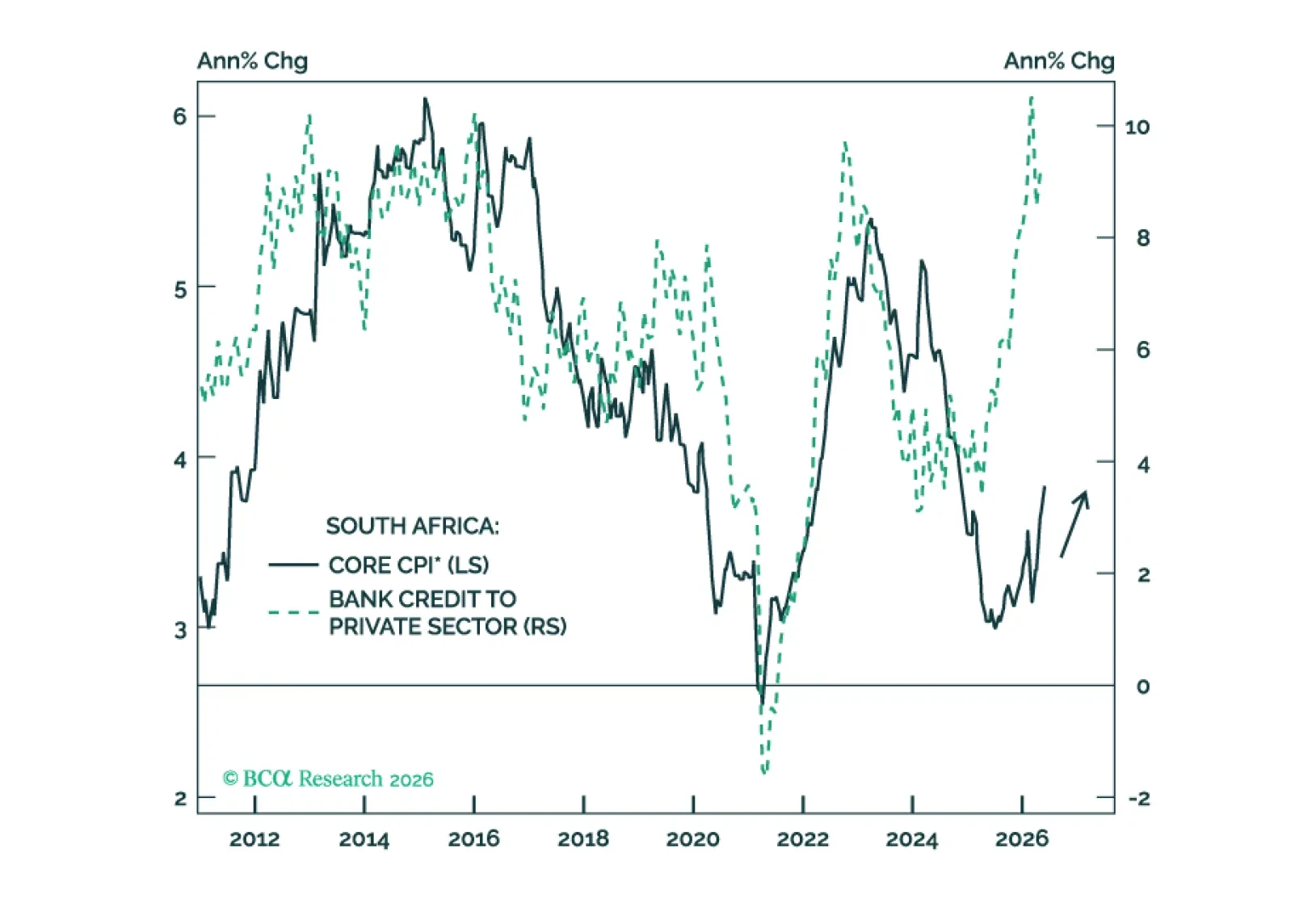

South Africa’s ambitious reform agenda will take time to bear fruit. Meanwhile, the country faces a stagflationary squeeze as inflation rises while growth slows. South African stocks, bonds, and currency are all vulnerable.

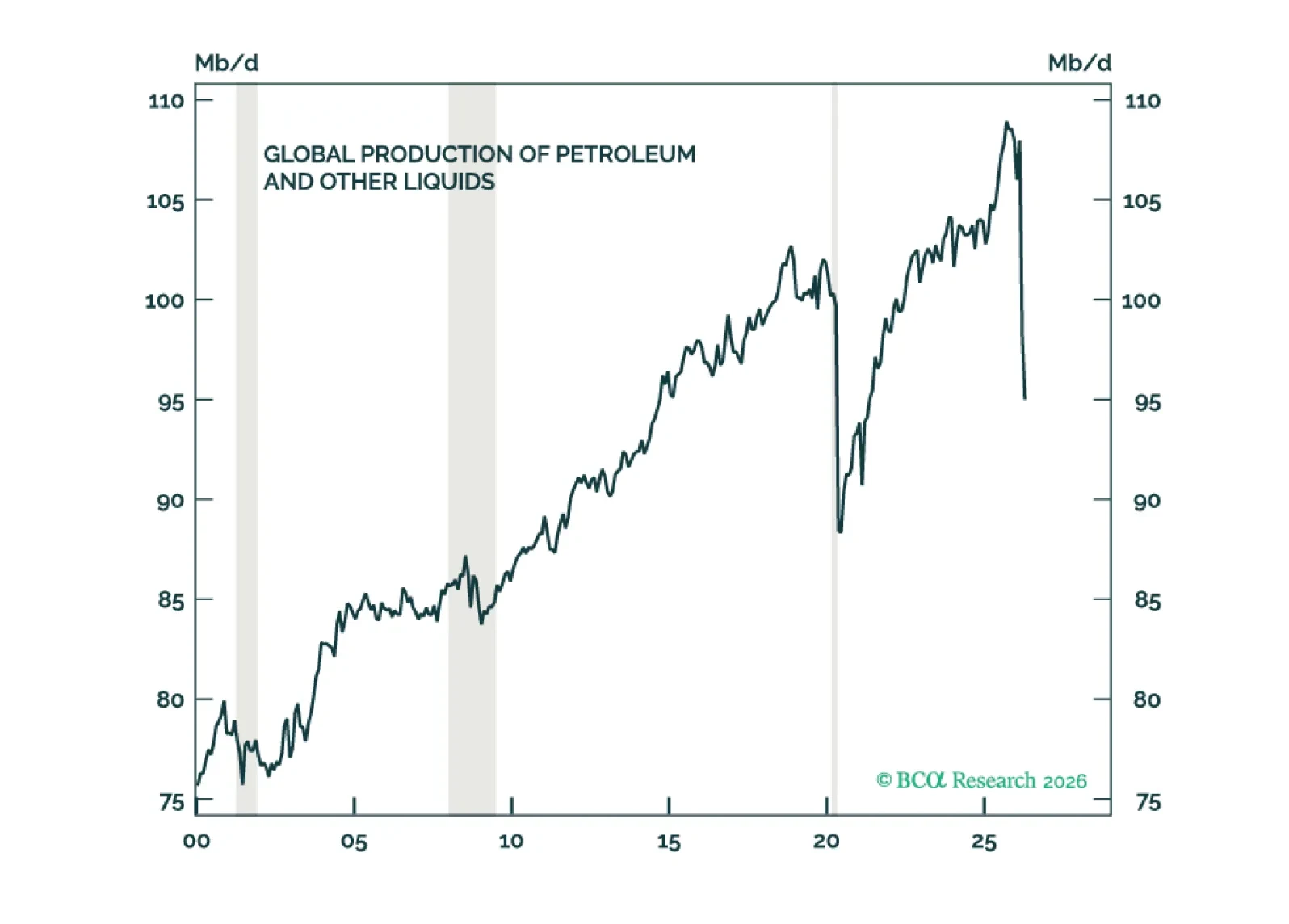

The global economy has weathered the oil shock reasonably well so far. However, the risk of a recession will increase meaningfully if the Strait of Hormuz remains closed into June.

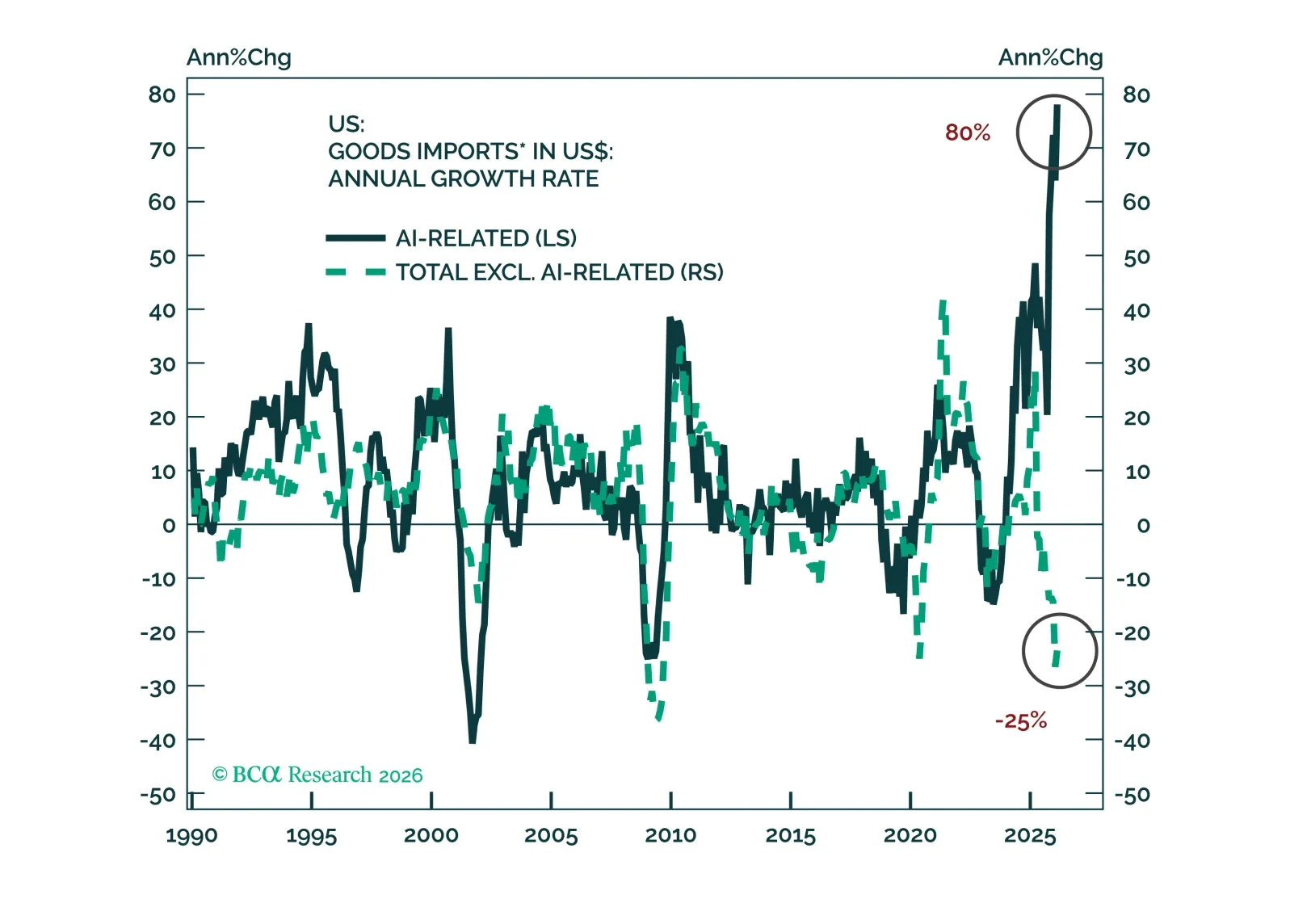

Global trade has held up despite US non-AI import volumes contracting by 25% over the past 12 months. The strength in global trade has concentrated in two areas: (1) imports of AI-related hardware and (2) developing countries’ imports, especially from China. Will these continue?

The relief rally in stocks can continue a while longer. However, much can still go wrong. As such, we are retaining a 12-month underweight to stocks but are moving to neutral on a short-term tactical horizon.