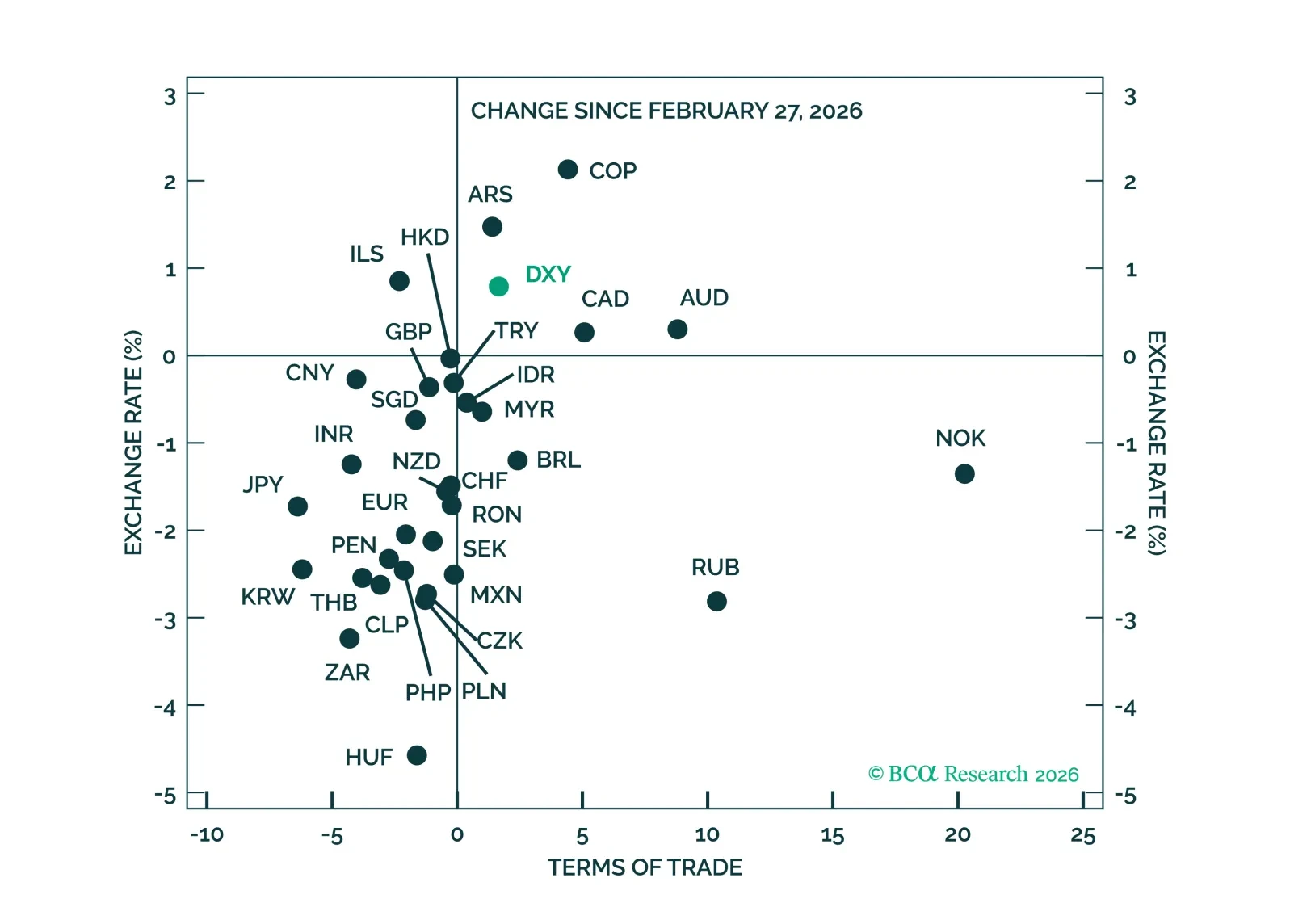

US Dollar

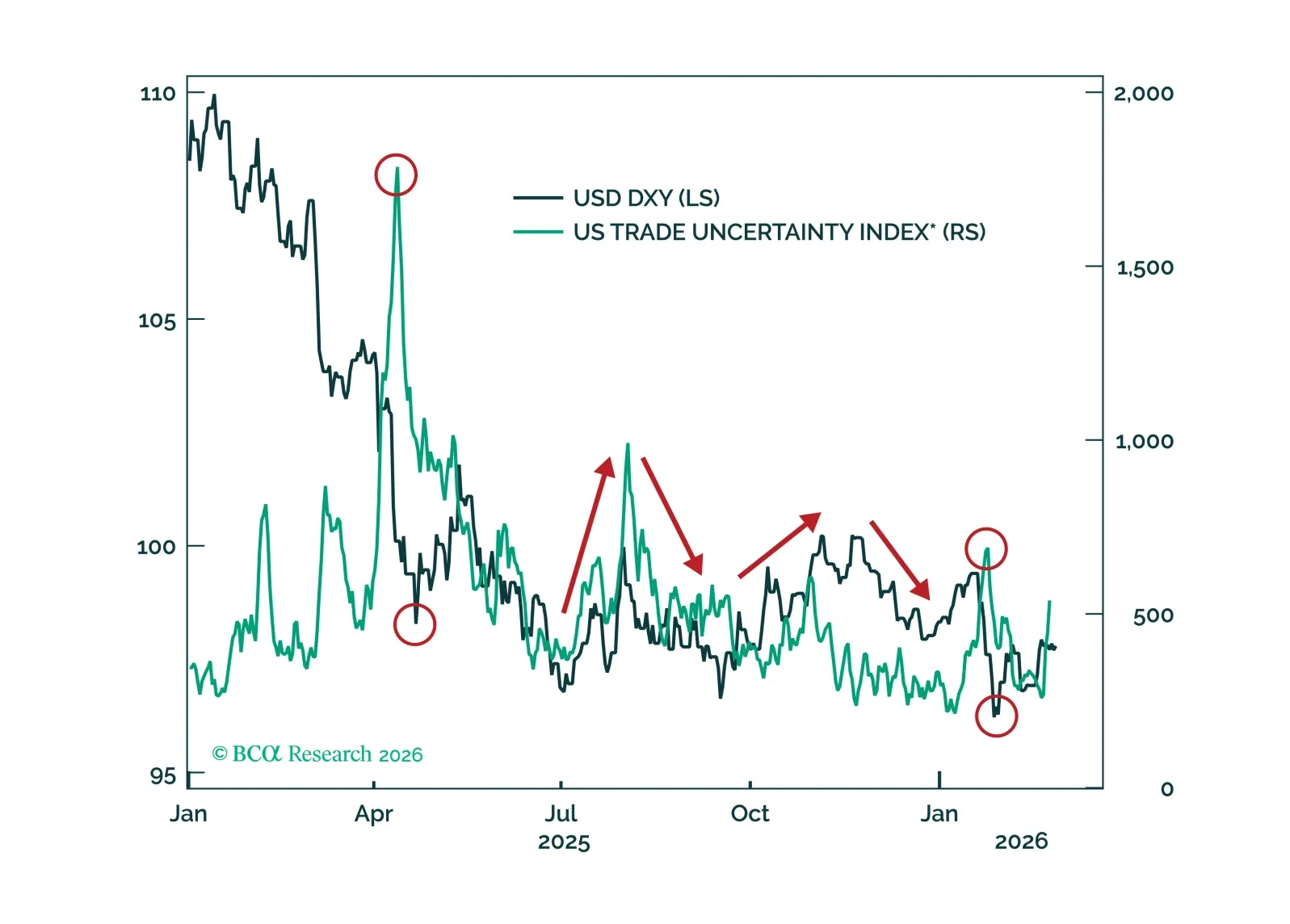

The dollar has had a strong run but its key supports from Fed repricing, positioning, and terms of trade are starting to fade. We close our tactical long USD positions and turn to short USD/JPY, where intervention risk makes yen shorts look increasingly dangerous.

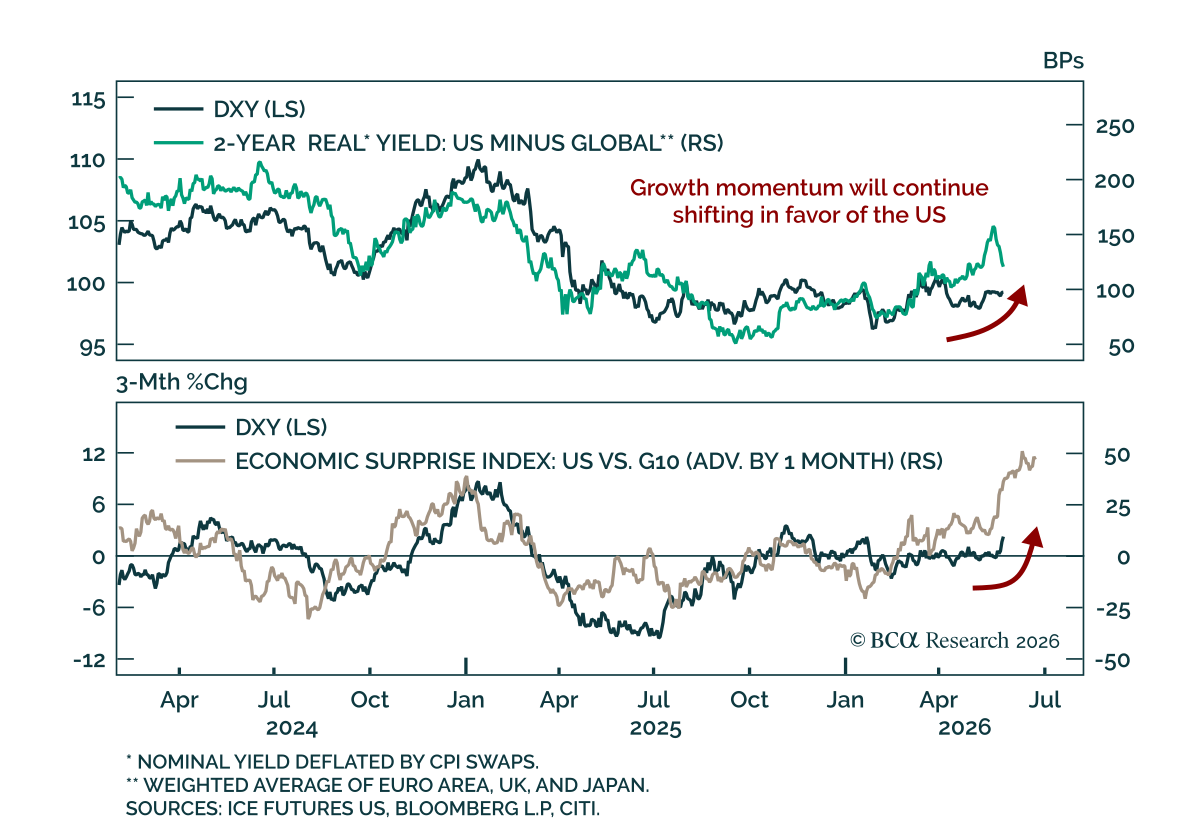

The dollar's muted response to the Iran conflict has led many to question its safe-haven appeal. We argue the opposite – the dollar's defensive properties have returned, while improving growth and rate dynamics should underpin further USD strength in the months ahead.

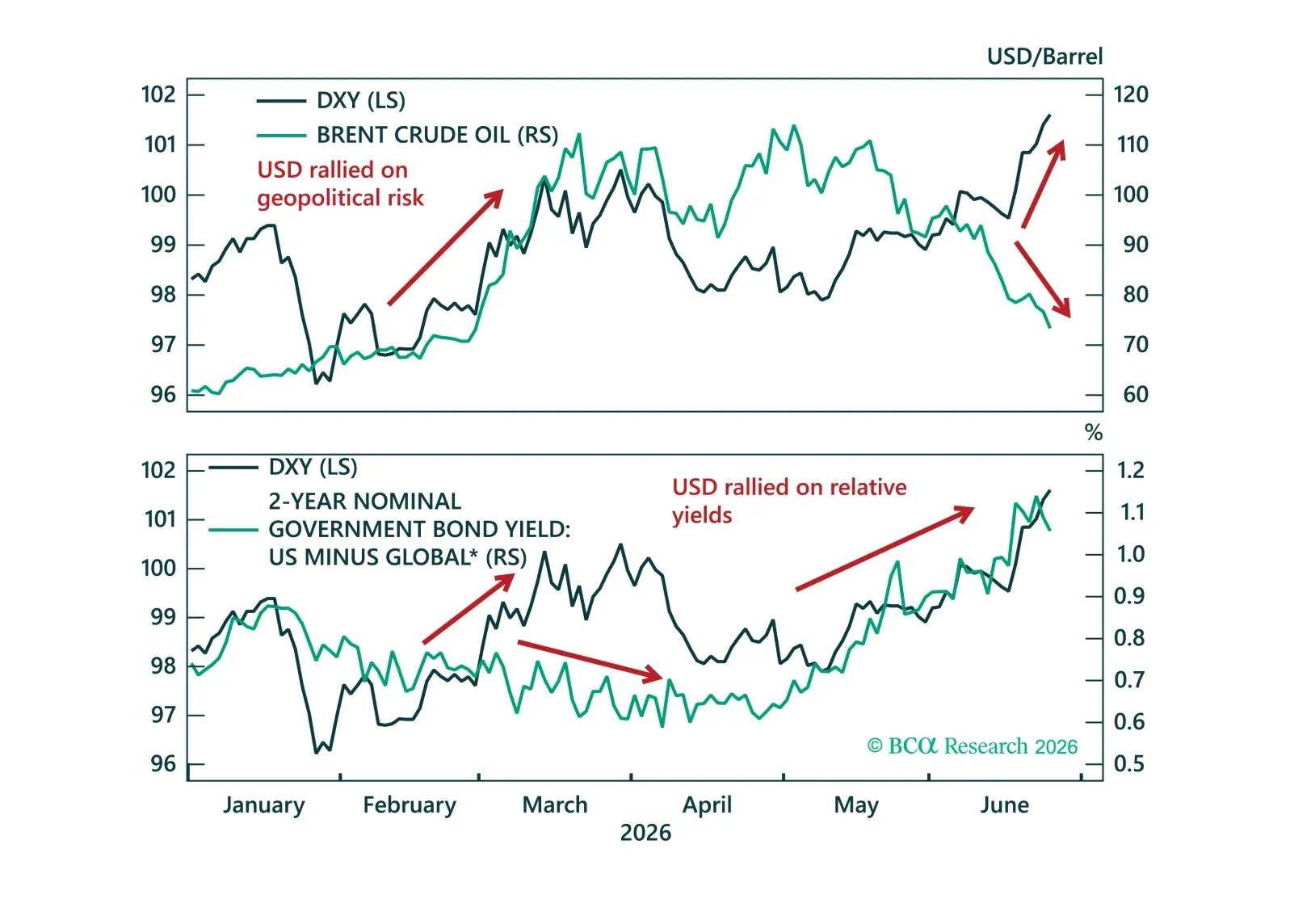

The dollar’s pullback masks a quiet improvement in its cyclical backdrop, with growth, monetary policy, and flows turning in its favor. As markets fully price out geopolitical risk, the USD should decouple from oil and better reflect these gains, despite lingering structural headwinds.

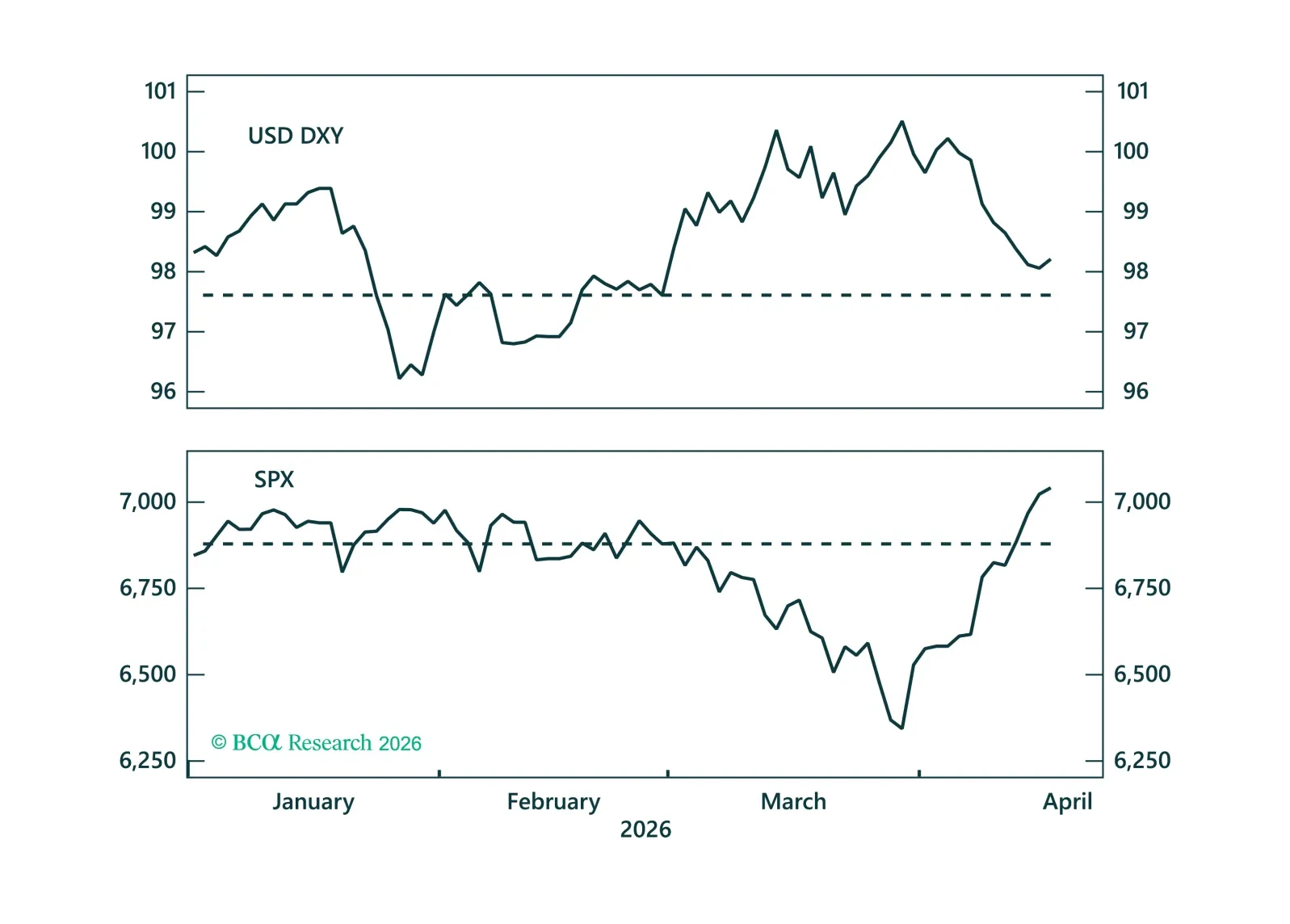

The relief rally in stocks can continue a while longer. However, much can still go wrong. As such, we are retaining a 12-month underweight to stocks but are moving to neutral on a short-term tactical horizon.

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

Investors are too complacent on the closure of the Strait of Hormuz. Upgrade cash and downgrade equities, both to neutral.

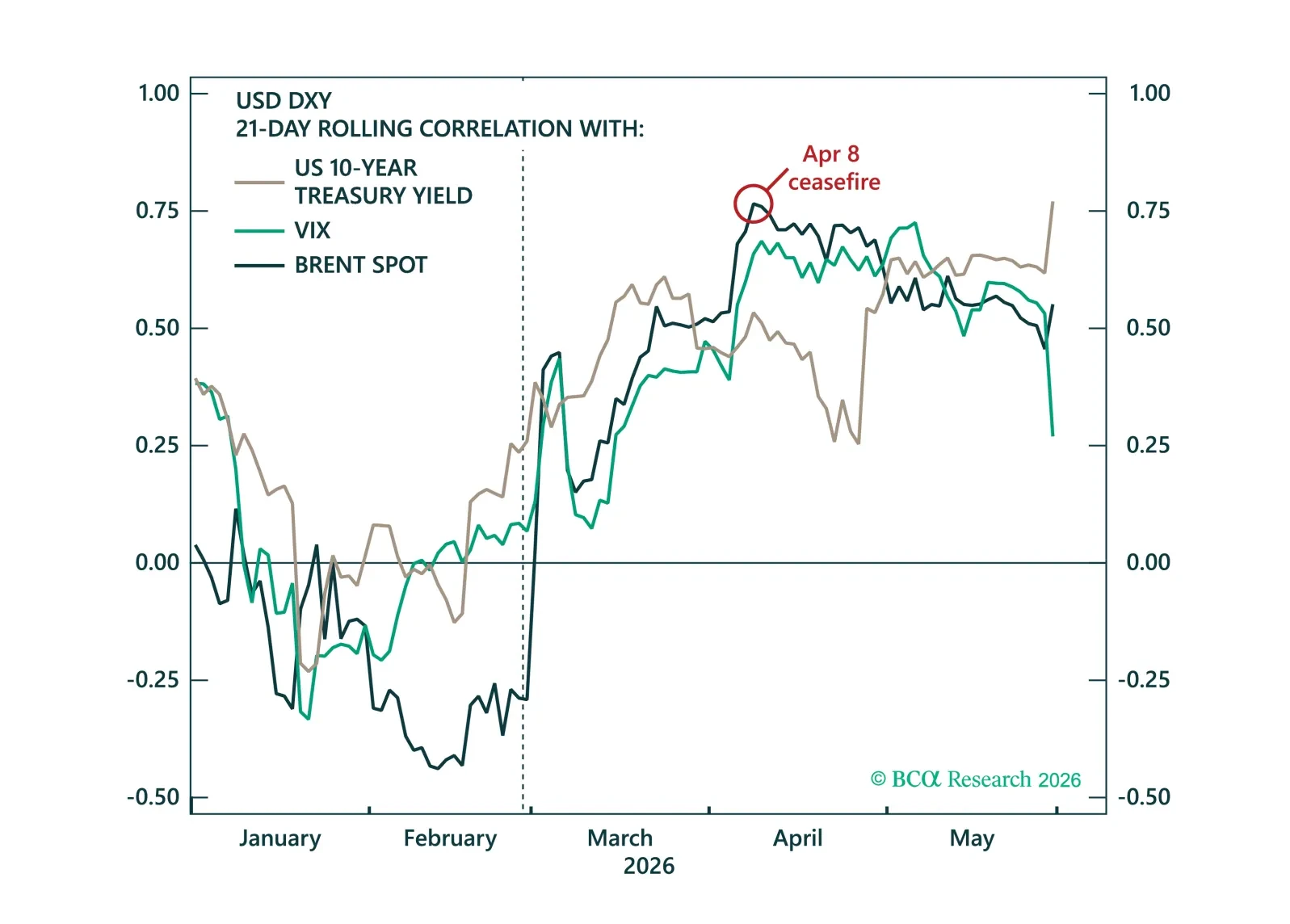

The Iran war remains a terms-of-trade shock rather than a classic flight to safety – for now. As oil risks skew higher, policy repricing and growth differentials should continue to favor a tactical rebound in the USD.

Policy risks are set to fade just as markets underestimate hawkish Fed repricing and crowd into short-USD positions, setting the stage for a tactical dollar rebound into the election cycle. Go long USD/CHF to capture the rate differential and receding policy uncertainty.