China

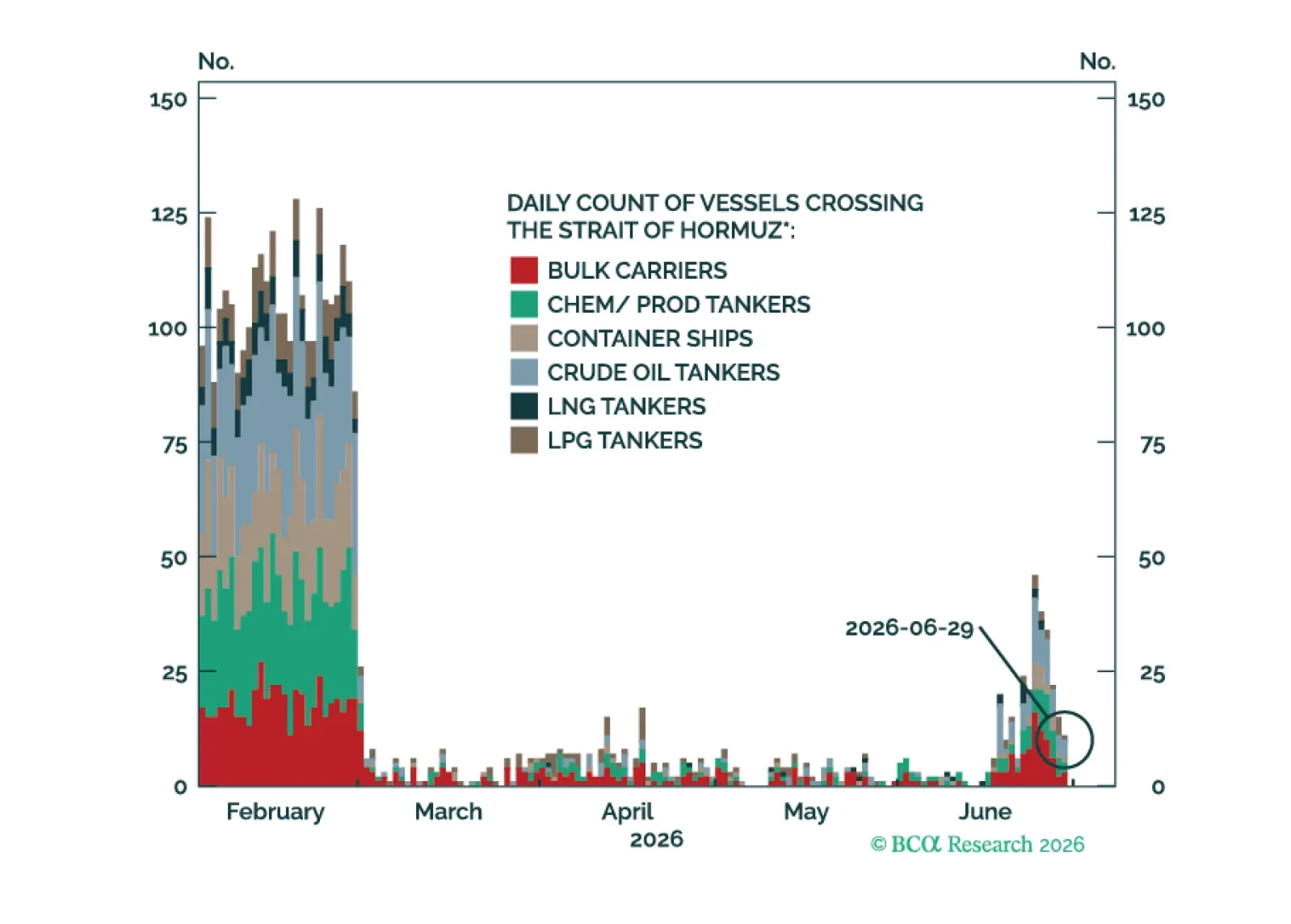

Geopolitical risk may rotate to Russia/Ukraine in Q3, while the Middle East could reignite in Q4.

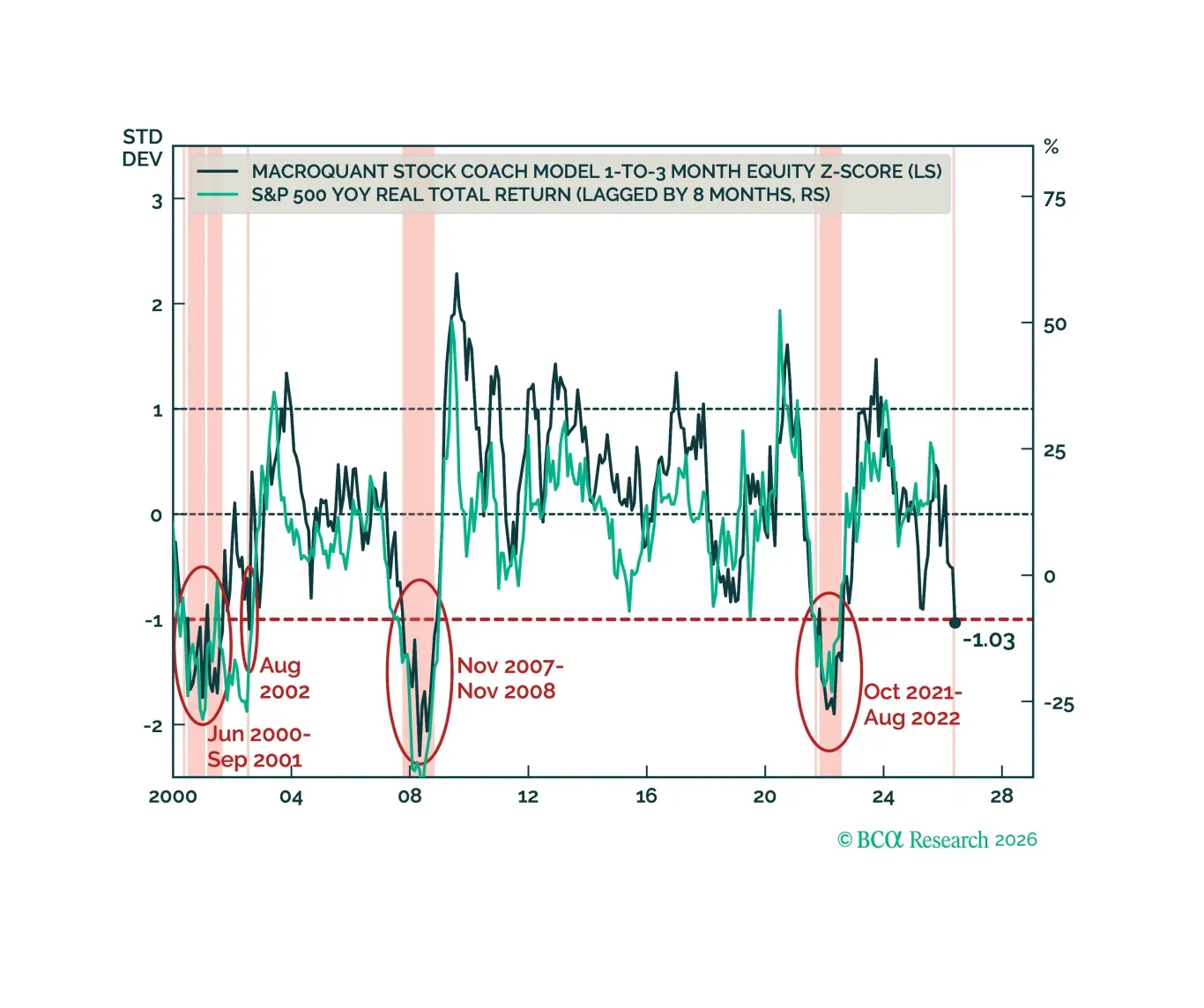

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

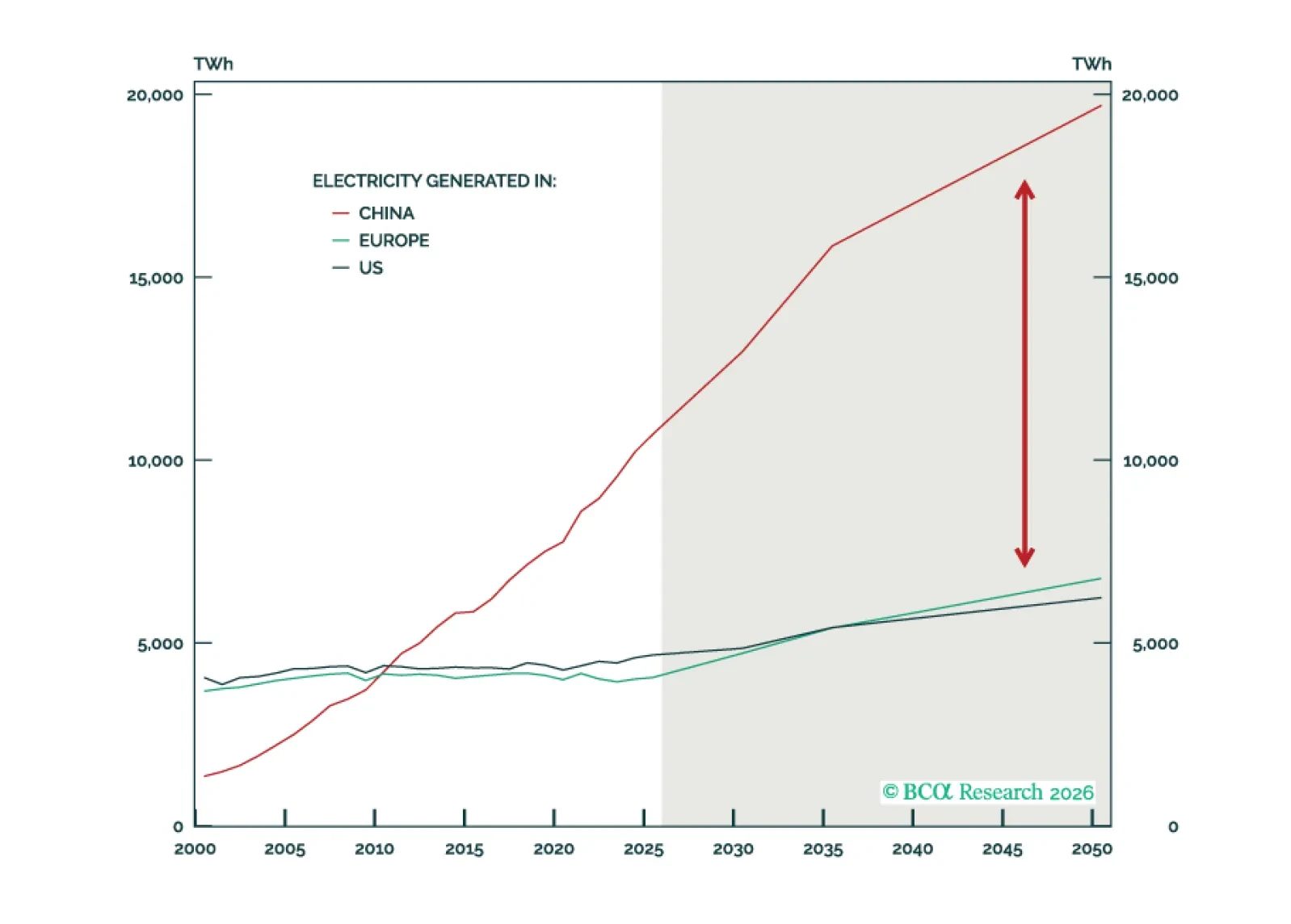

China holds a structural advantage in this "Age of Electricity" by operating the world's largest electricity system. However, this advantage has inherent limits, and the US remains competitive despite its challenges.

This report addresses five frequently asked questions from our Greater China clients over the past few months.

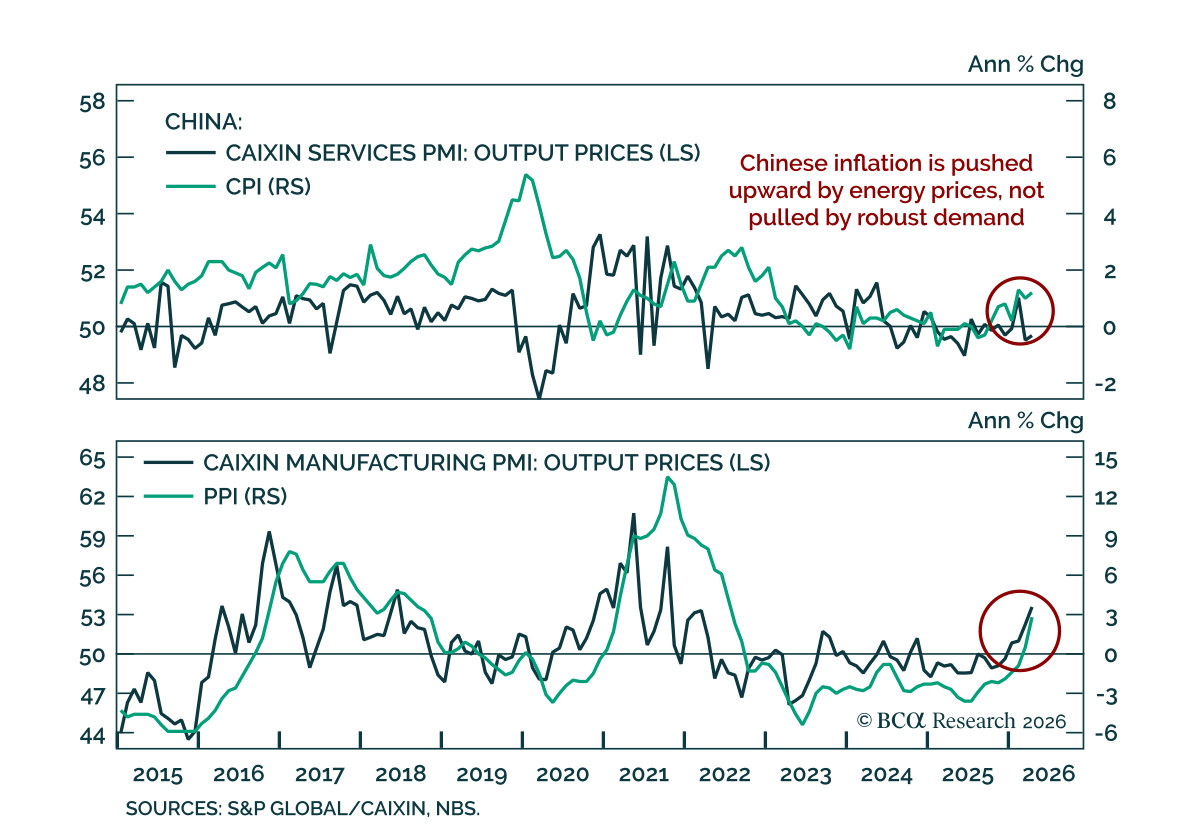

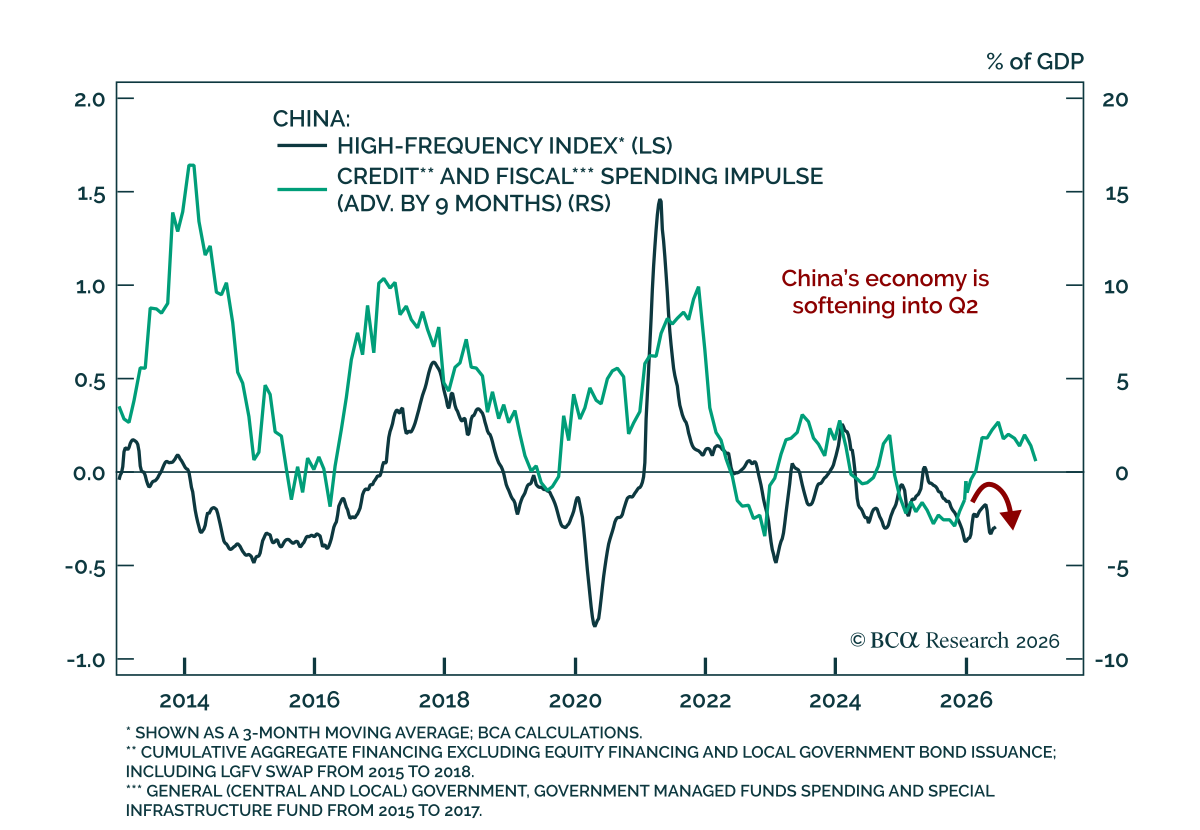

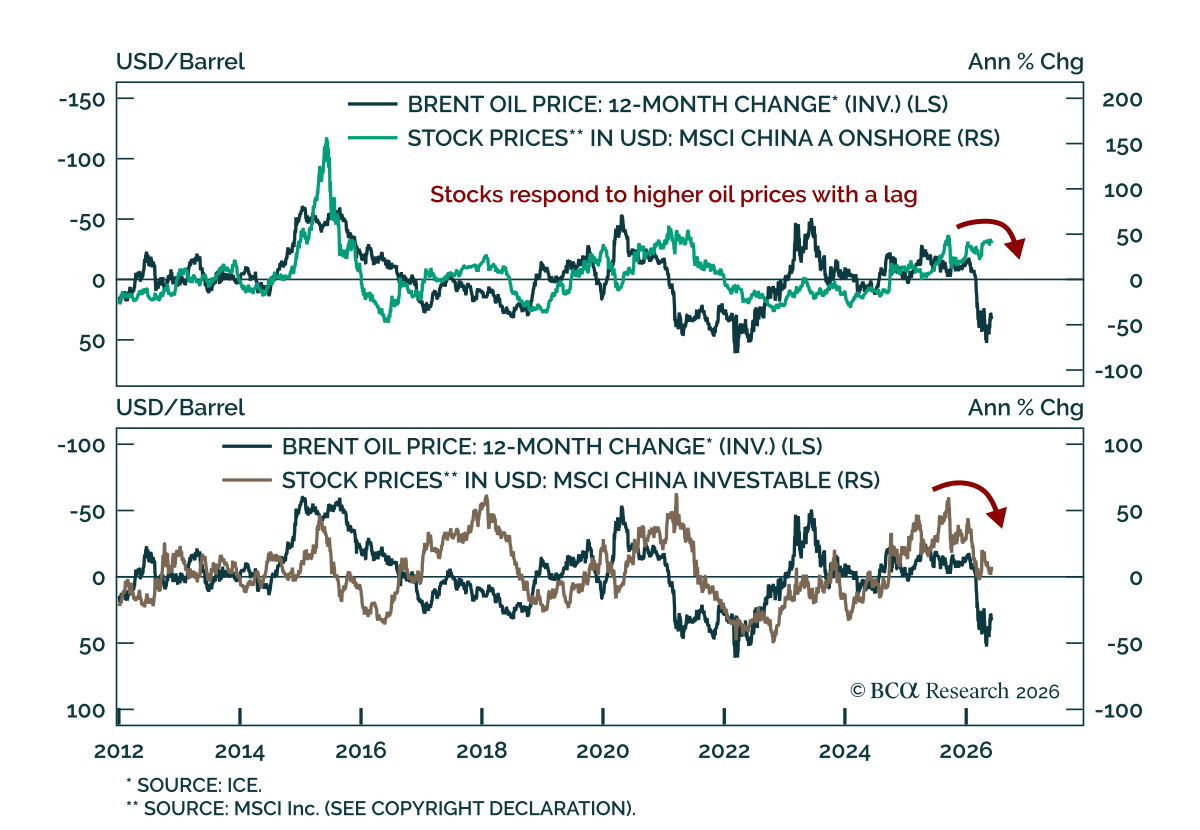

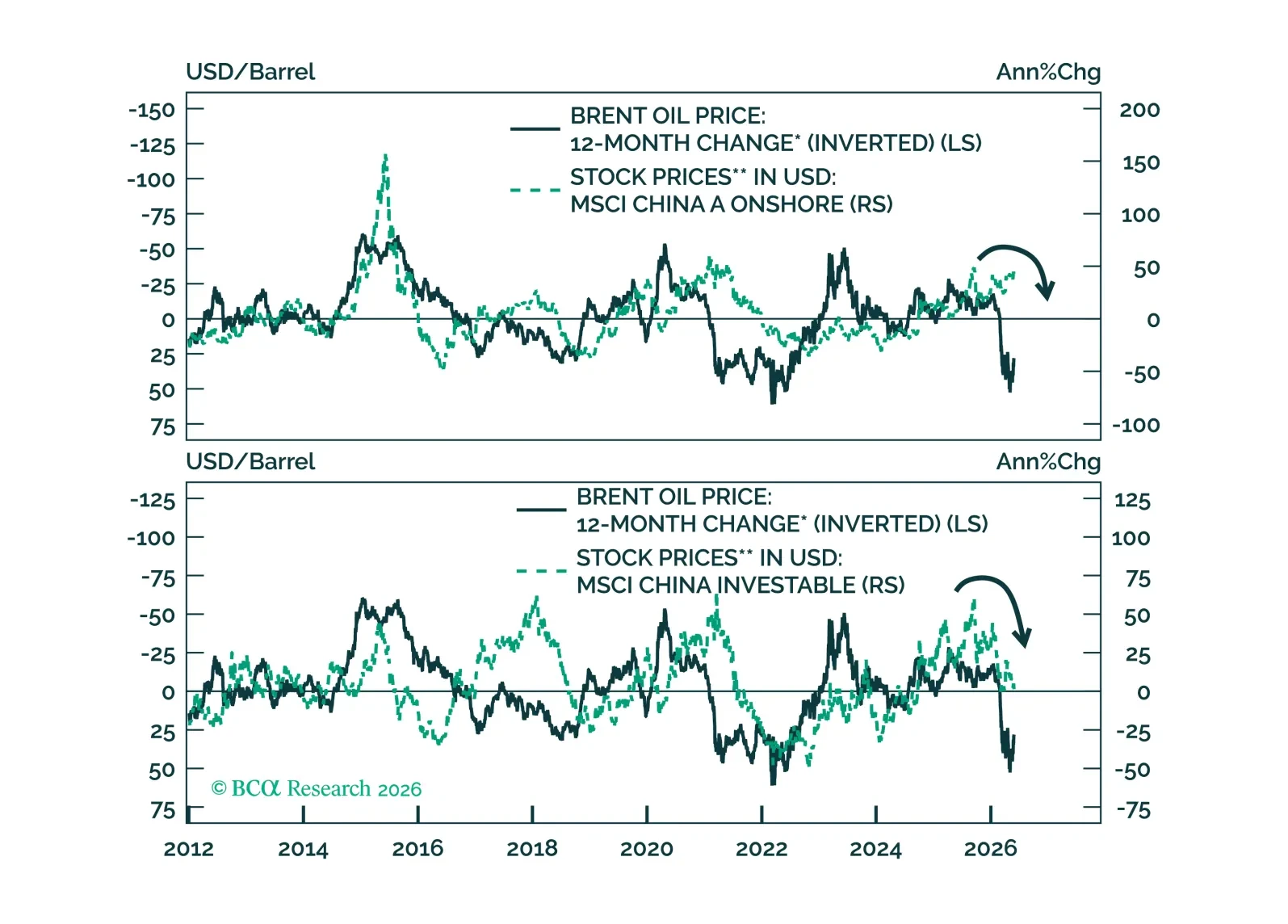

Oil shocks hit economies with a lag. China will feel the delayed pain of surging oil prices, pushing Beijing toward infrastructure spending as its main tool to prop up growth.

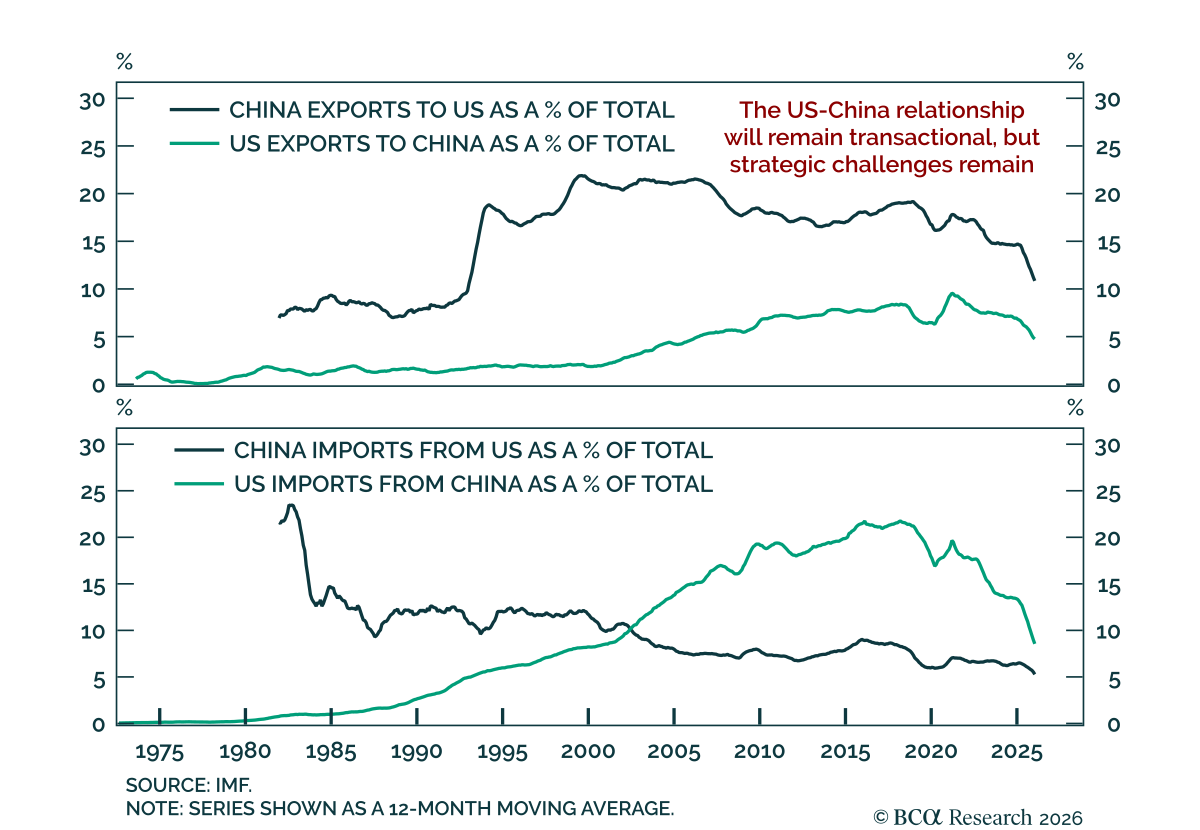

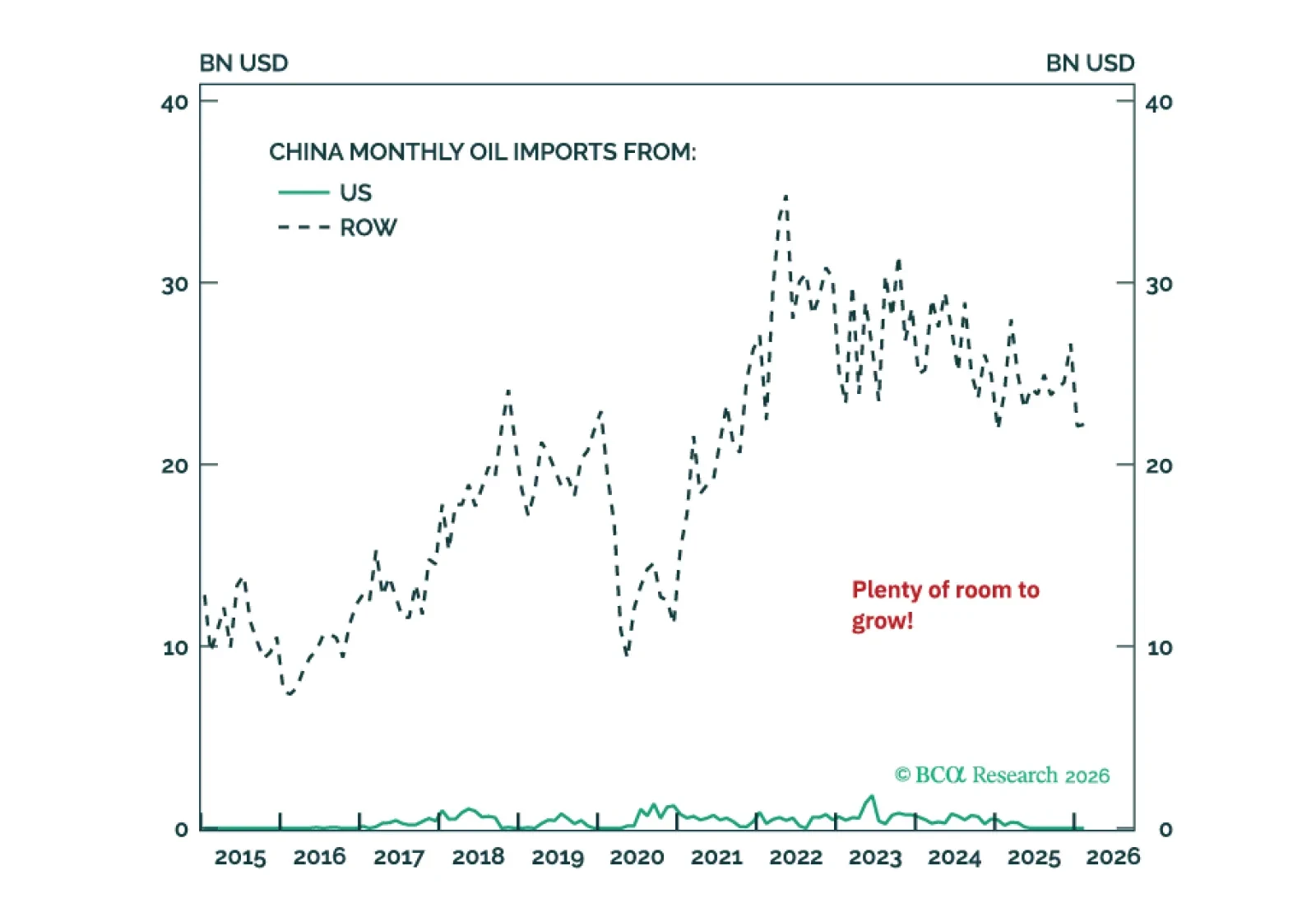

The US-China trade truce is getting bigger and better, but a grand strategic bargain on Iran and Taiwan is not happening.