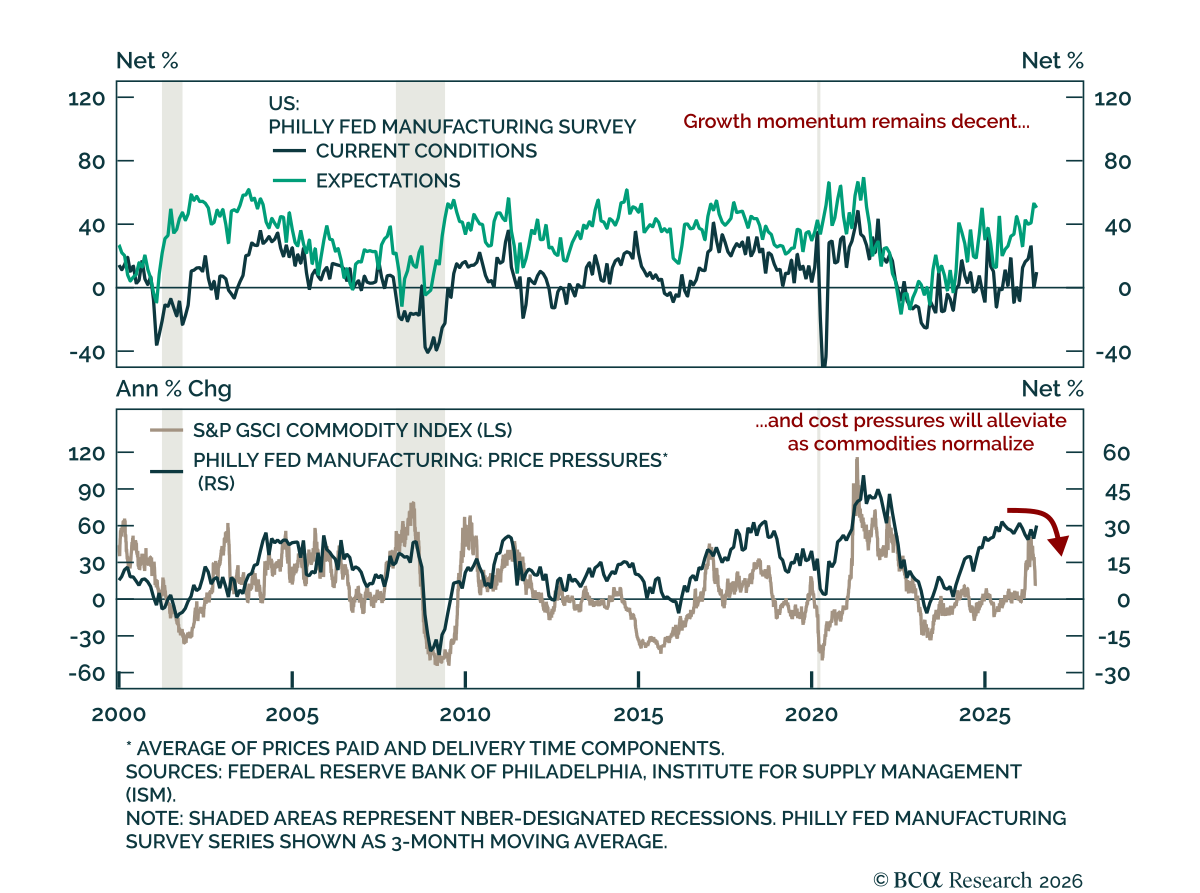

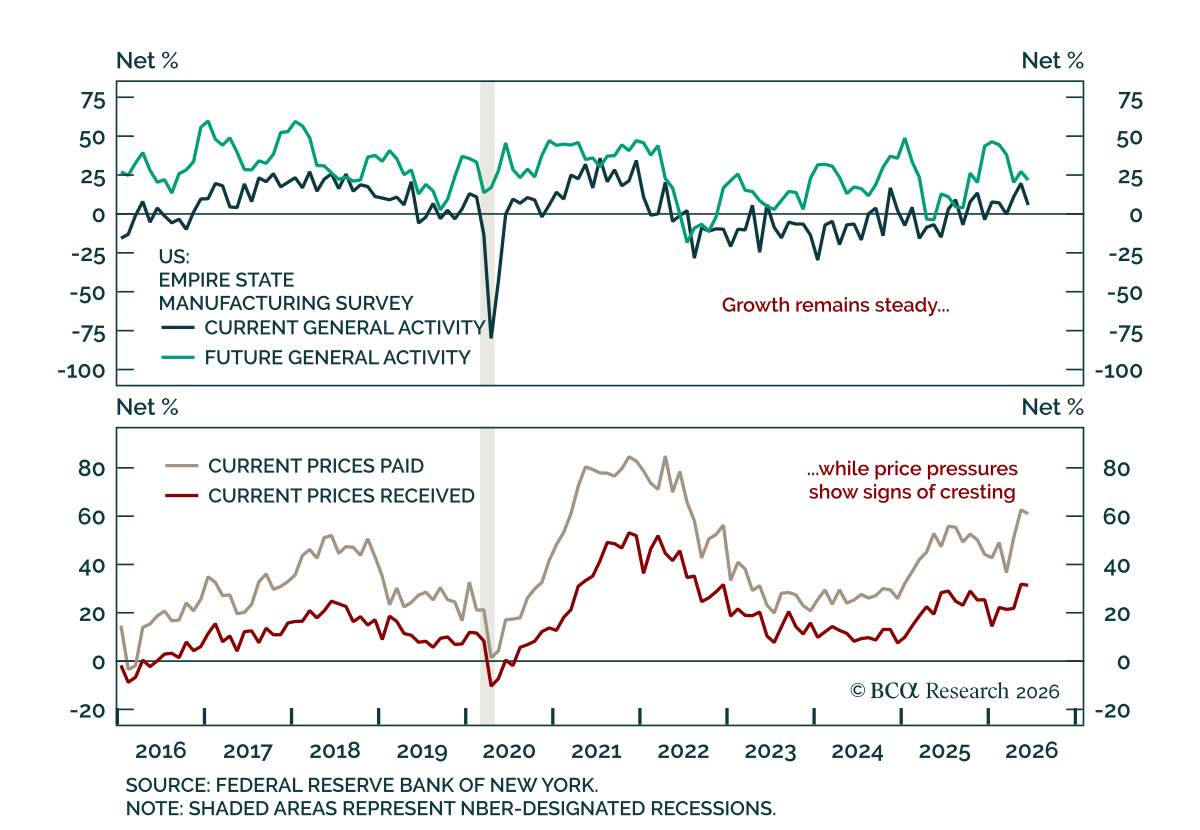

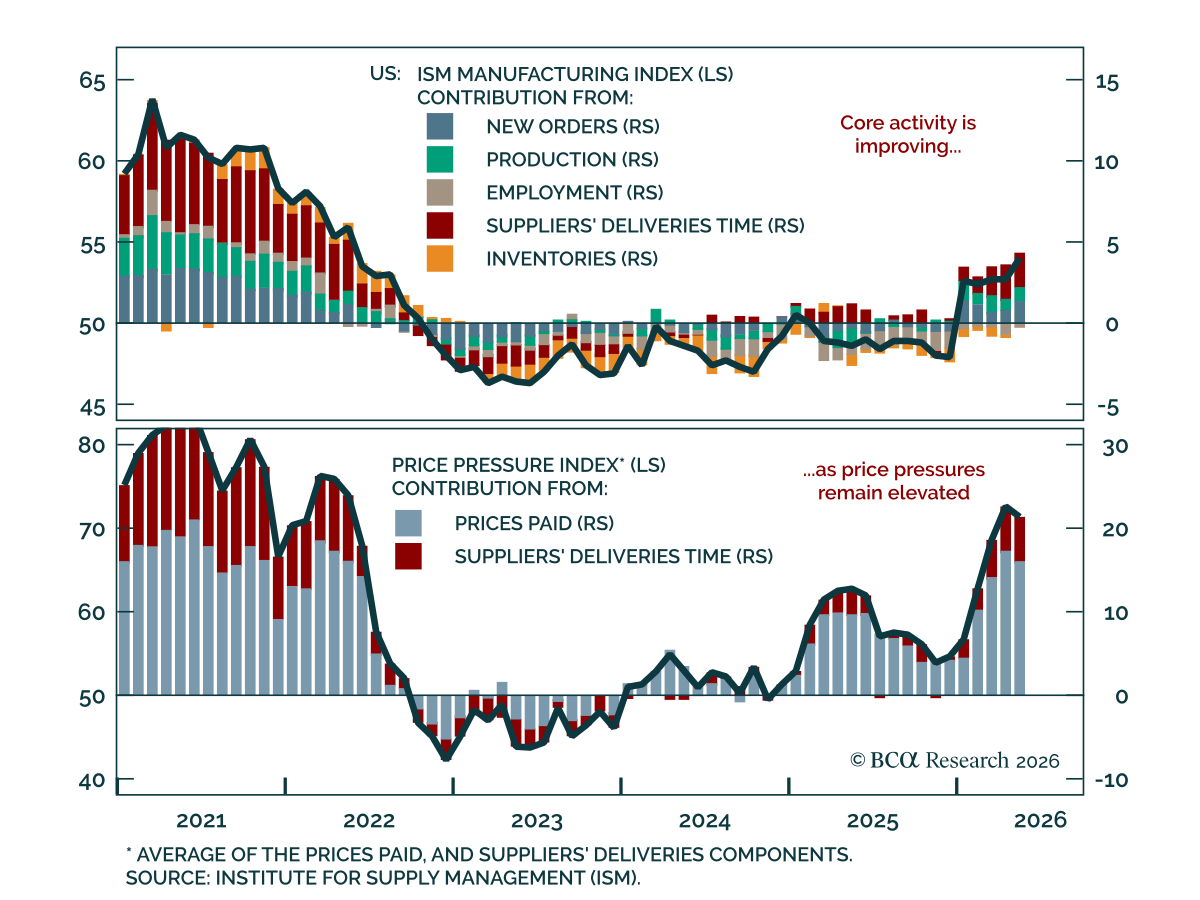

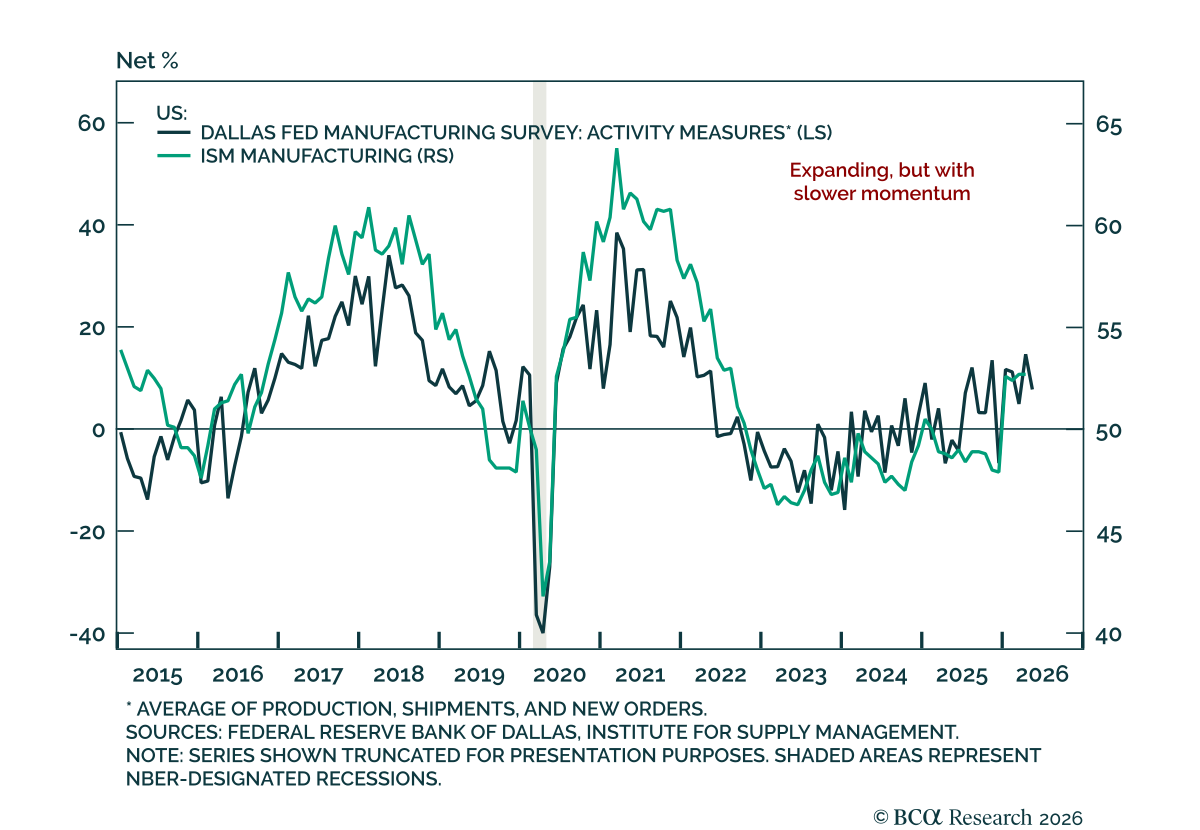

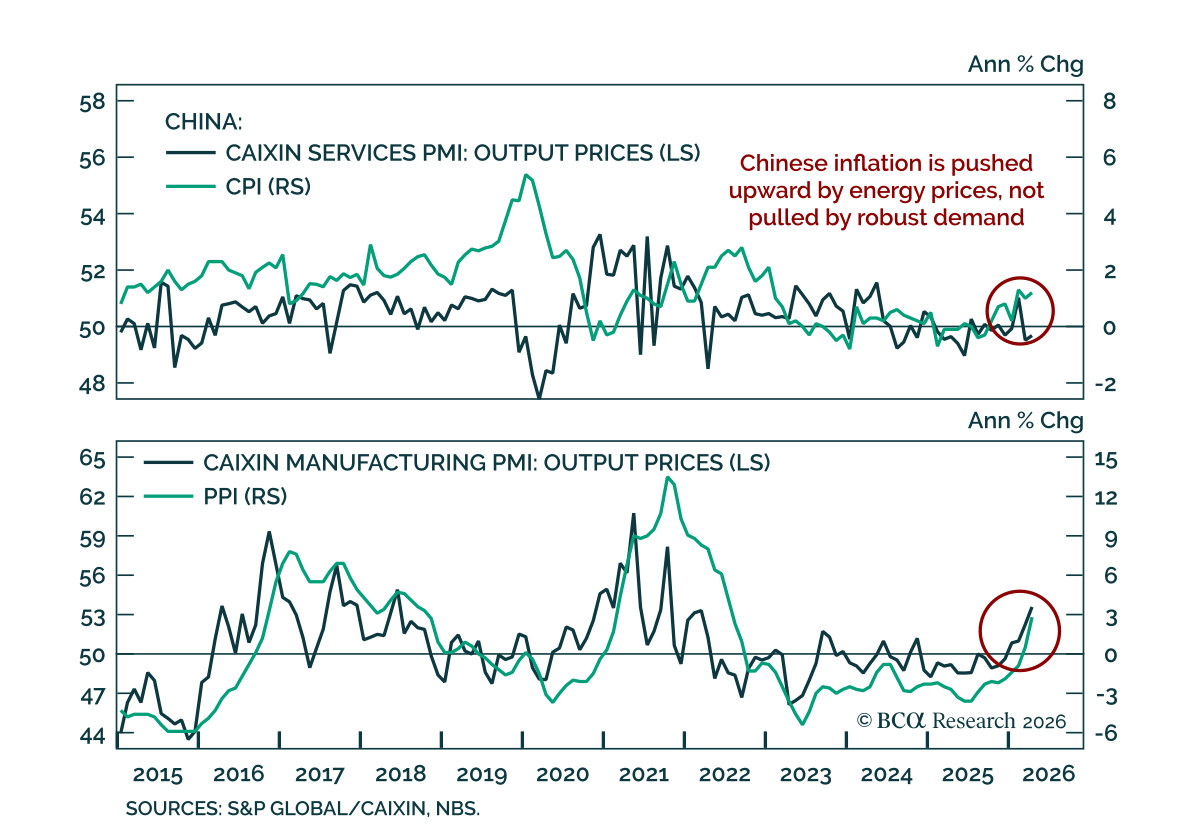

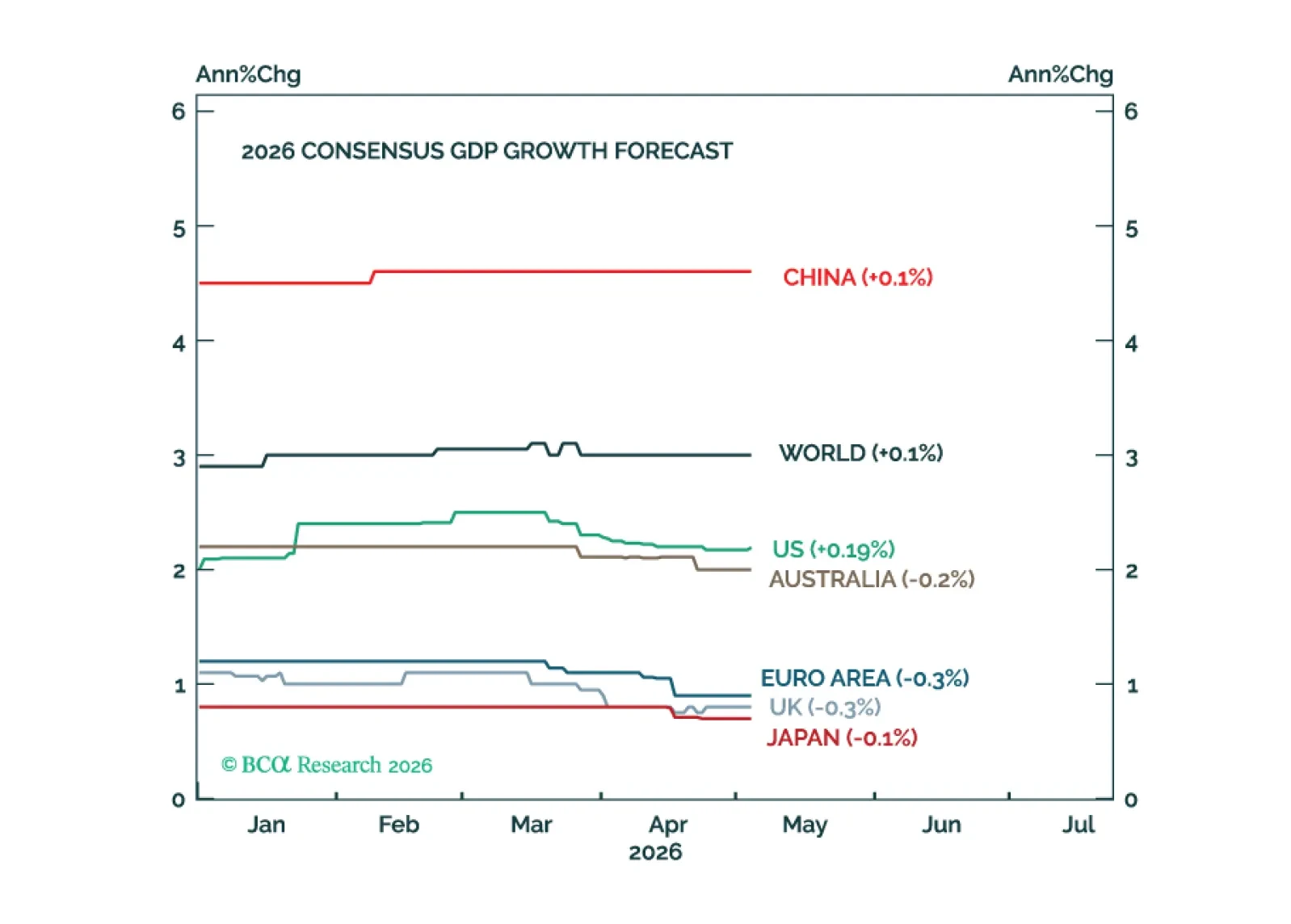

Manufacturing

South Africa’s ambitious reform agenda will take time to bear fruit. Meanwhile, the country faces a stagflationary squeeze as inflation rises while growth slows. South African stocks, bonds, and currency are all vulnerable.

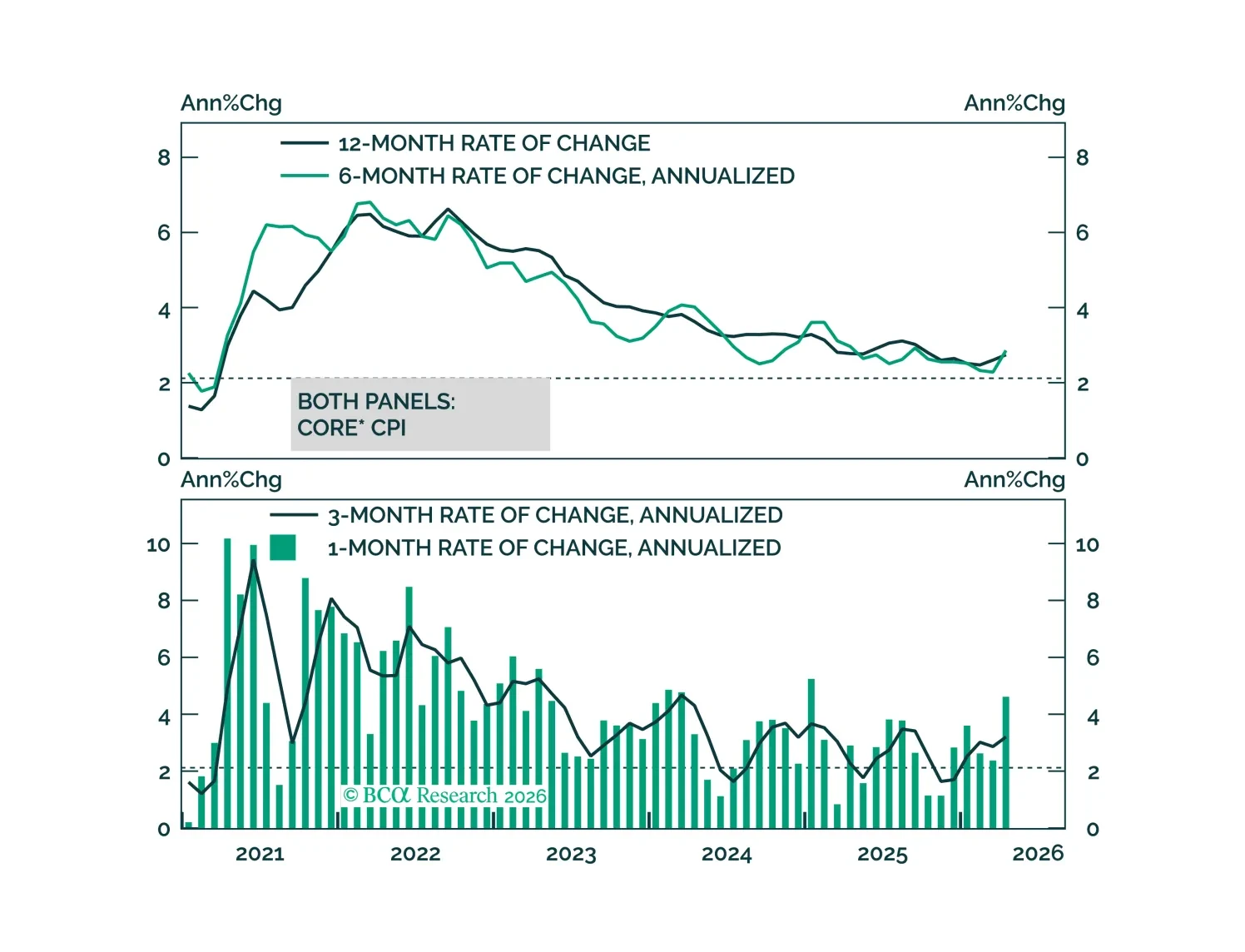

The April CPI report showed clear evidence of the direct effect of higher oil prices on inflation but, so far, limited evidence of passthrough to core.

The global economy has weathered the oil shock reasonably well so far. However, the risk of a recession will increase meaningfully if the Strait of Hormuz remains closed into June.

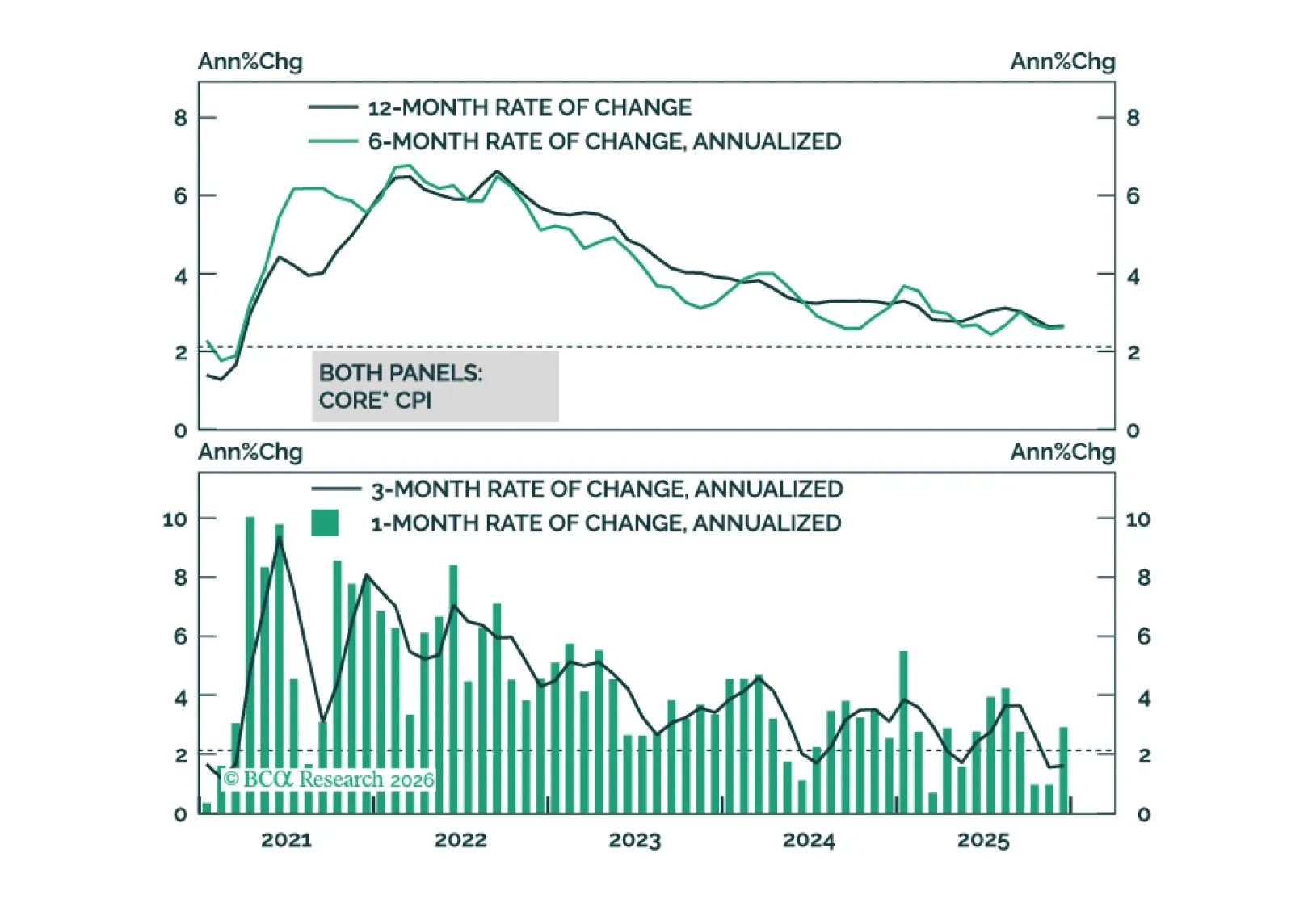

This morning’s CPI report signals that the worst of the tariff impact on inflation may already be in the rearview mirror.

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.