Asset Allocation

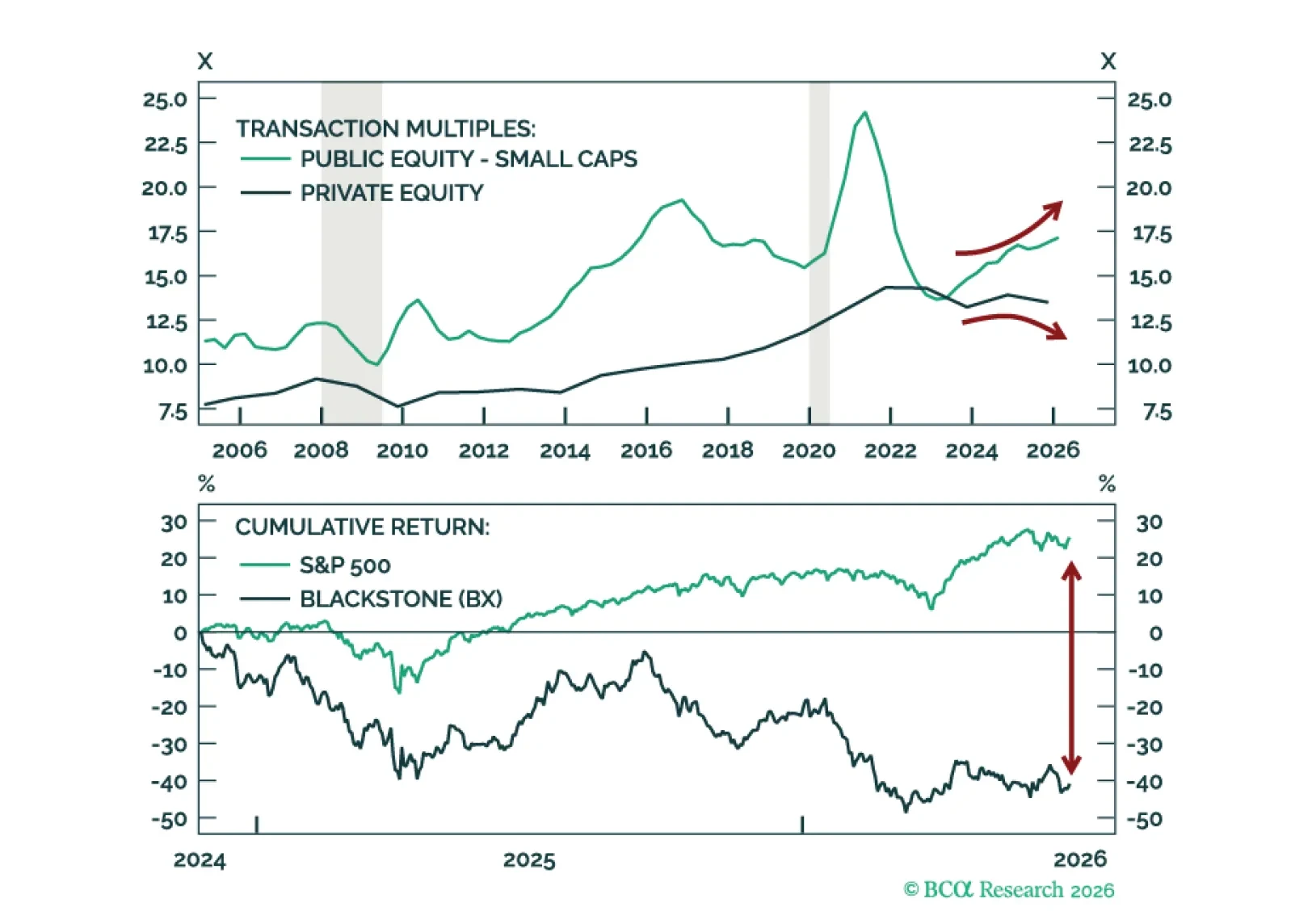

Beginning with this Quarterly report, The Global Asset Allocation and Private Markets teams are combining our quarterly outlooks into a single, unified framework, reflecting a more integrated approach to portfolio construction. In this joint outlook we upgrade Private Equity to overweight. Sentiment has soured, LPs are starved of distributions, flows have collapsed, valuations are trending lower, Secondaries are outperforming Primaries, and GP stocks are experiencing their worst underperformance on record. All signs of a durable bottom.

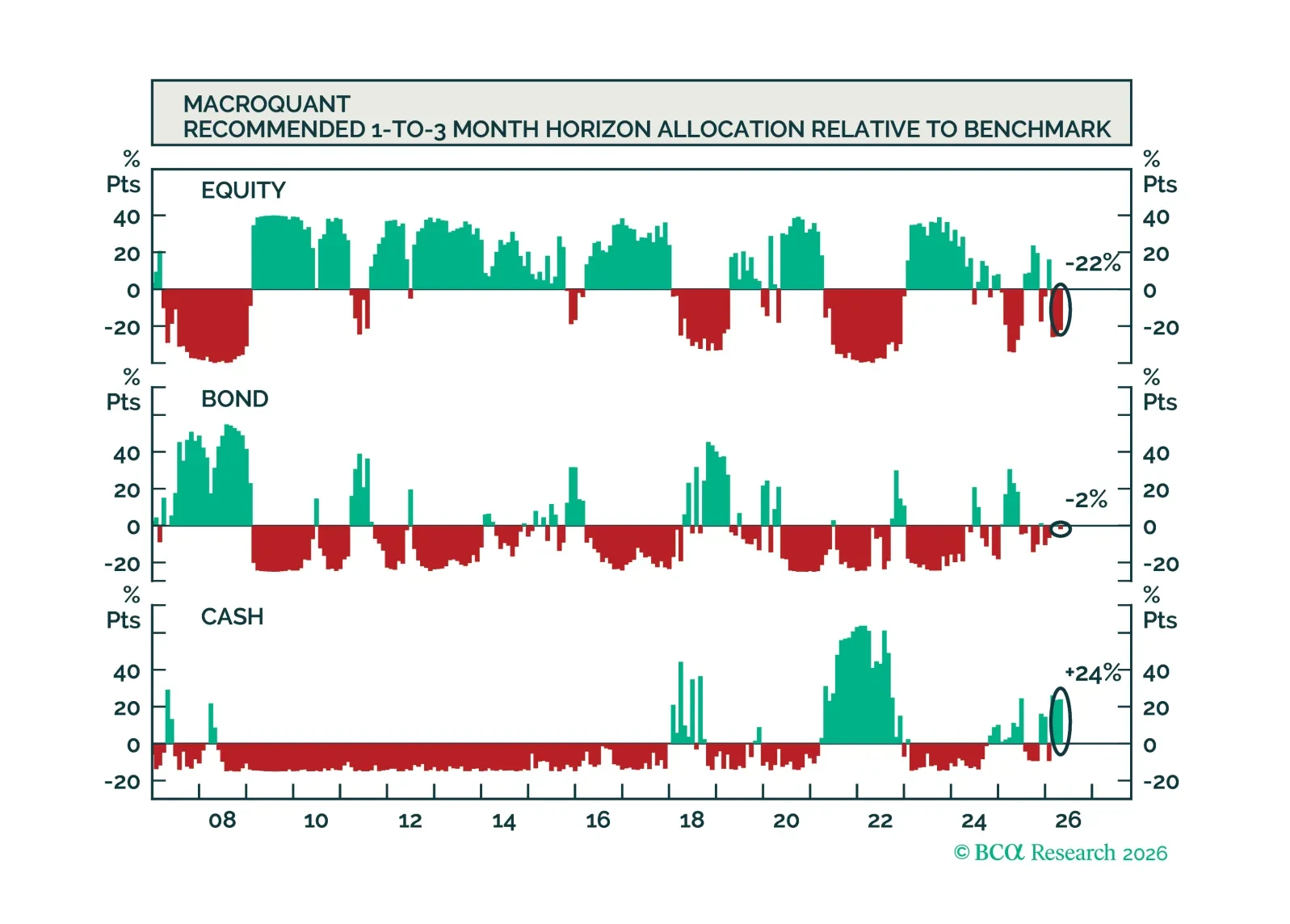

MacroQuant recommends underweighting equities and adopting a benchmark duration stance in fixed-income portfolios. The model is very positive on the US dollar, bearish on gold, neutral on copper, and bullish on oil.

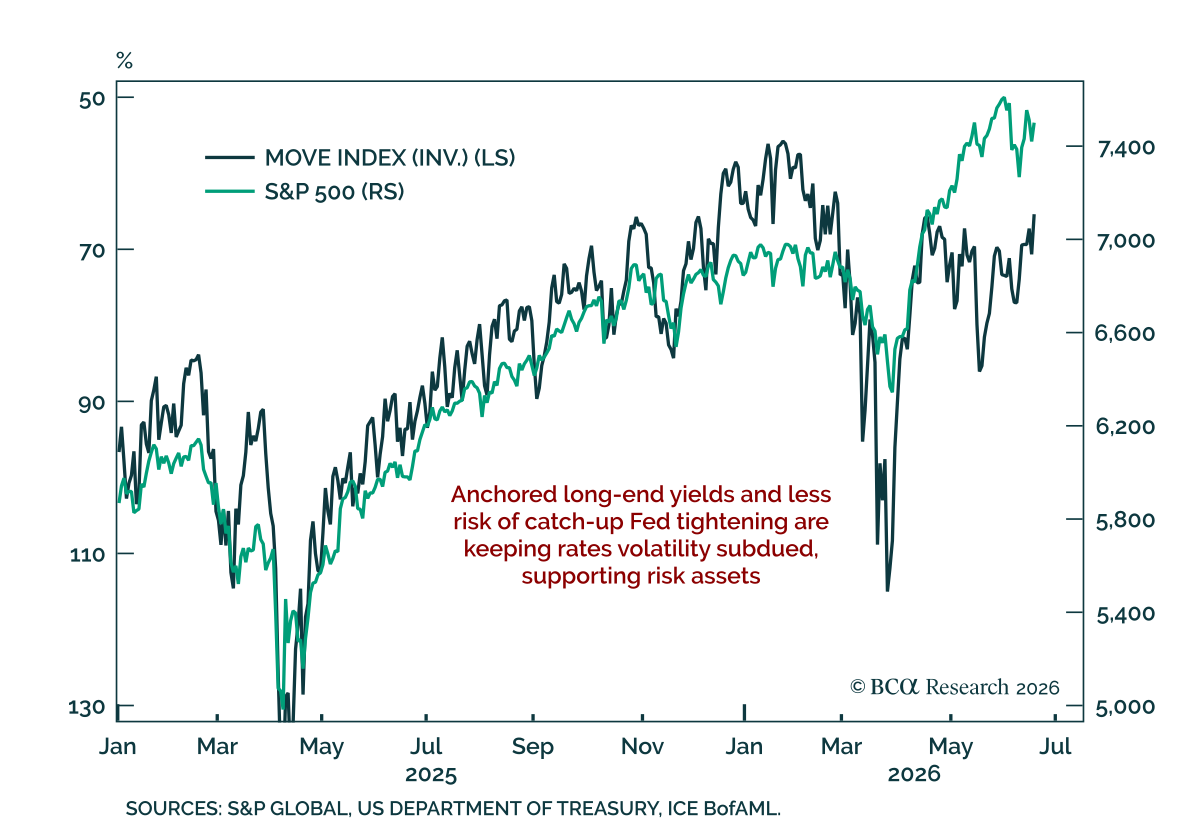

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

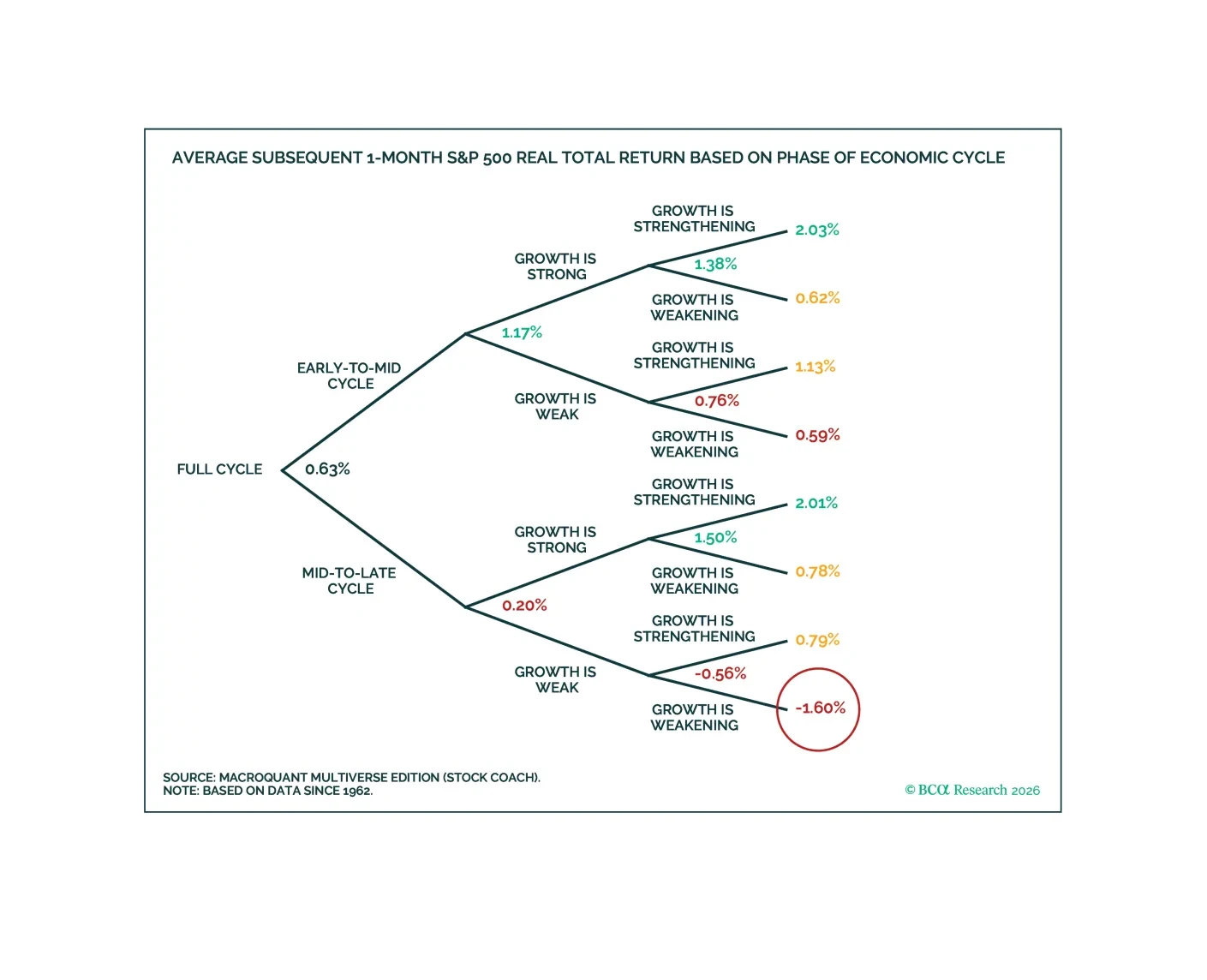

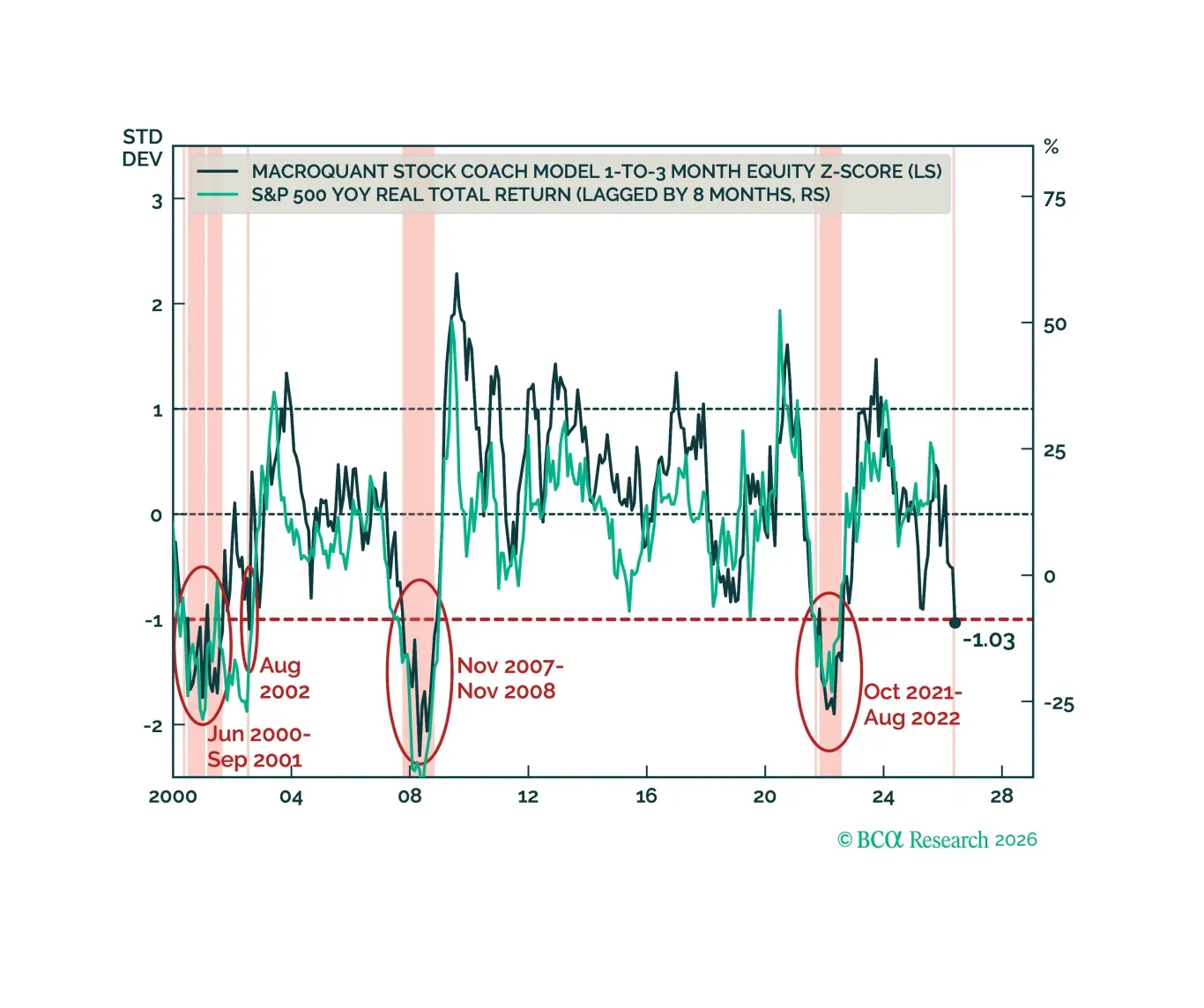

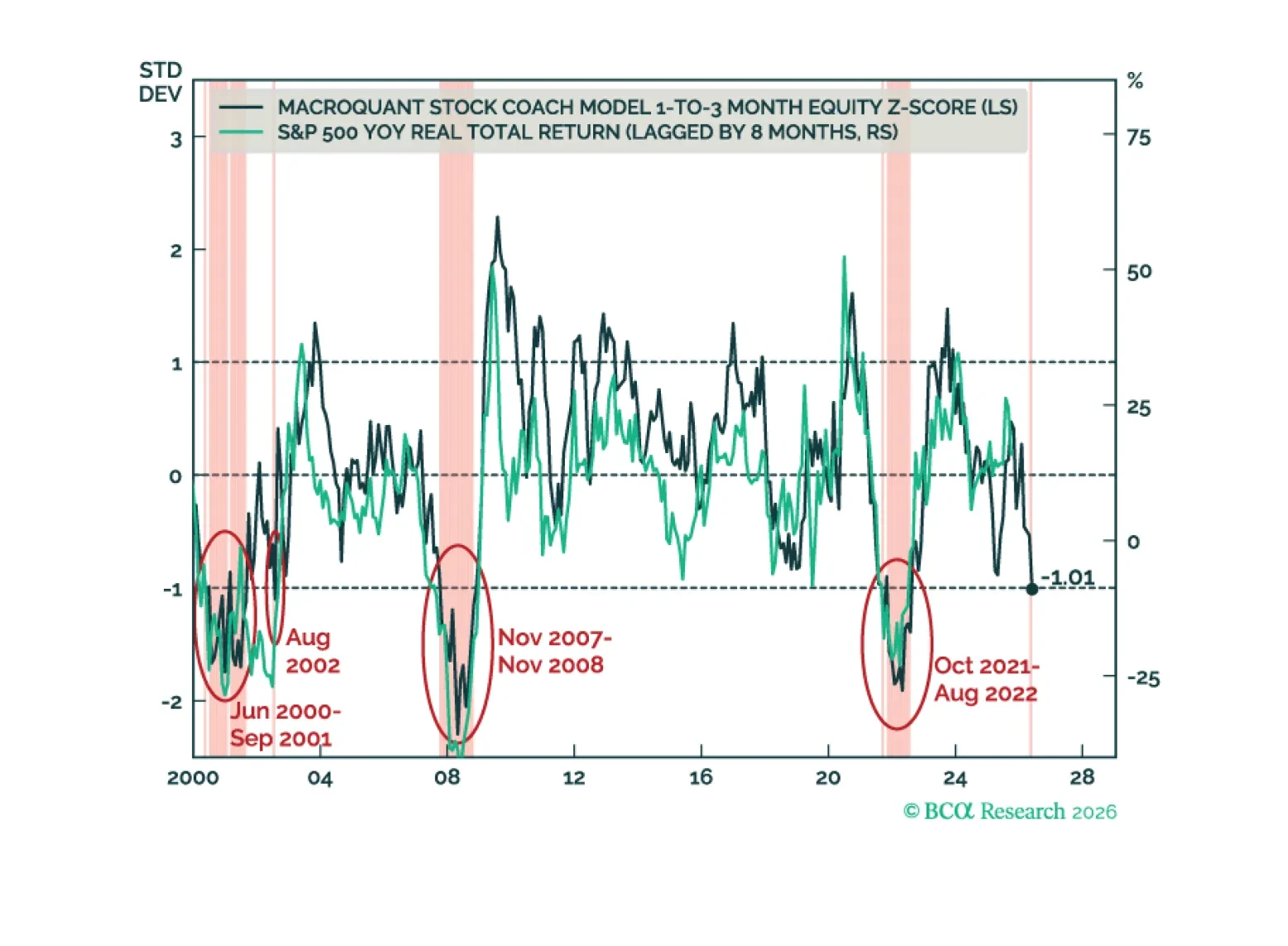

On Friday, the MacroQuant equity z-score fell to -1.01, below the critical -1 threshold that often coincided with bear markets in the past. With that in mind, today, I am downgrading stocks to a slight underweight on both a 3-month and a 12-month horizon.

So far most of the value in the AI supply chain has been captured by hardware companies. However, as model providers shift to usage-based pricing, value will begin to accrue to models and applications. Communications Services and Software should benefit from this shift. This broadening of the AI story, along with solid economic momentum should keep the rally going for the rest of the year. Remain overweight equities. Downgrade Energy to Neutral. Buy Software.

MacroQuant recommends a slight underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is very positive on the US dollar, downgrades gold to underweight, upgrades copper to overweight, and remains very bullish on oil.

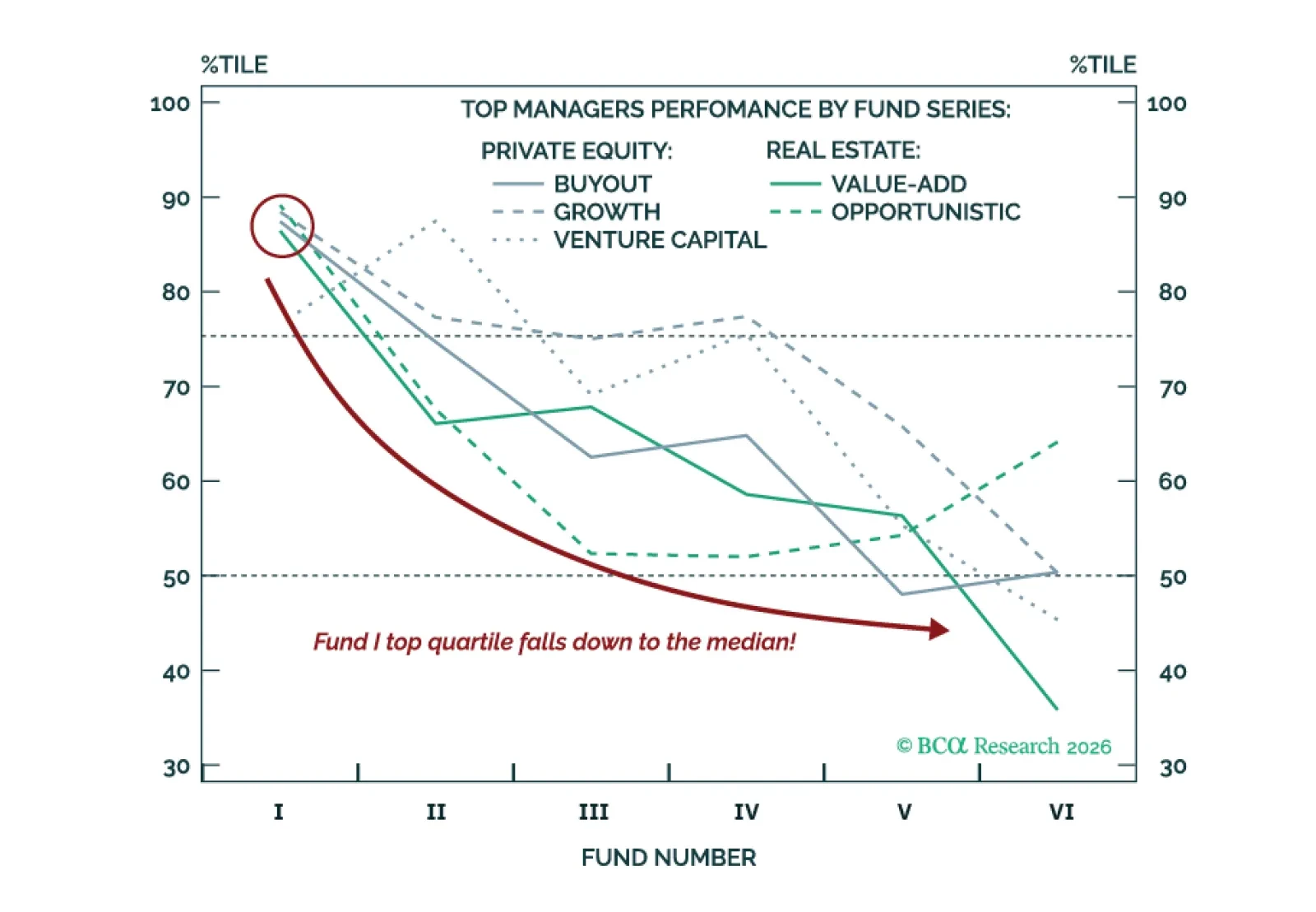

In Private Markets, yesterday’s winners often see outperformance fade. Top-quartile managers often regress toward the median as fund series mature. For investors evaluating the next Real Estate or Private Equity manager: Bias toward underweighting Funds V and beyond.