Euro Area

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

In Section I, Doug revisits the situation in the Strait of Hormuz and its implications for growth in Europe and the US. In Section II, Jonathan explores whether Kevin Warsh's appointment as Fed Chair signals a return to Greenspan-era, rules-based monetary policy.

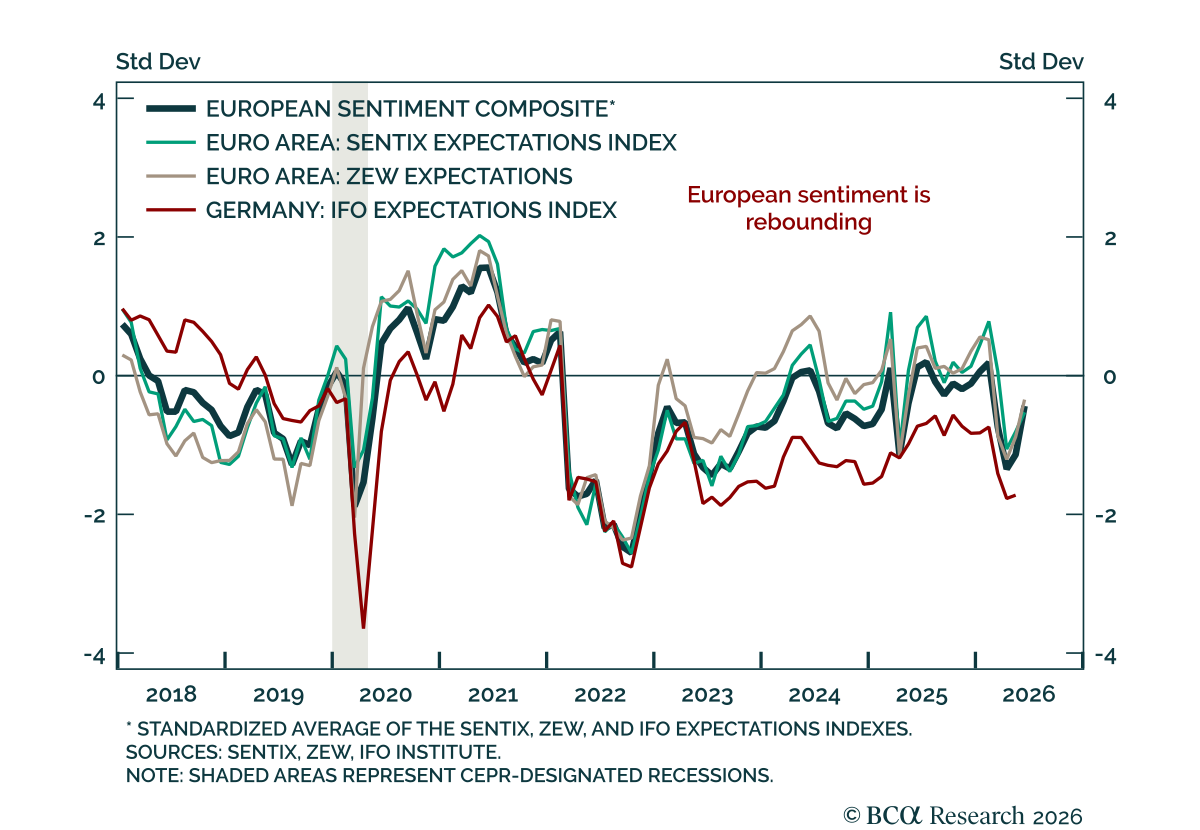

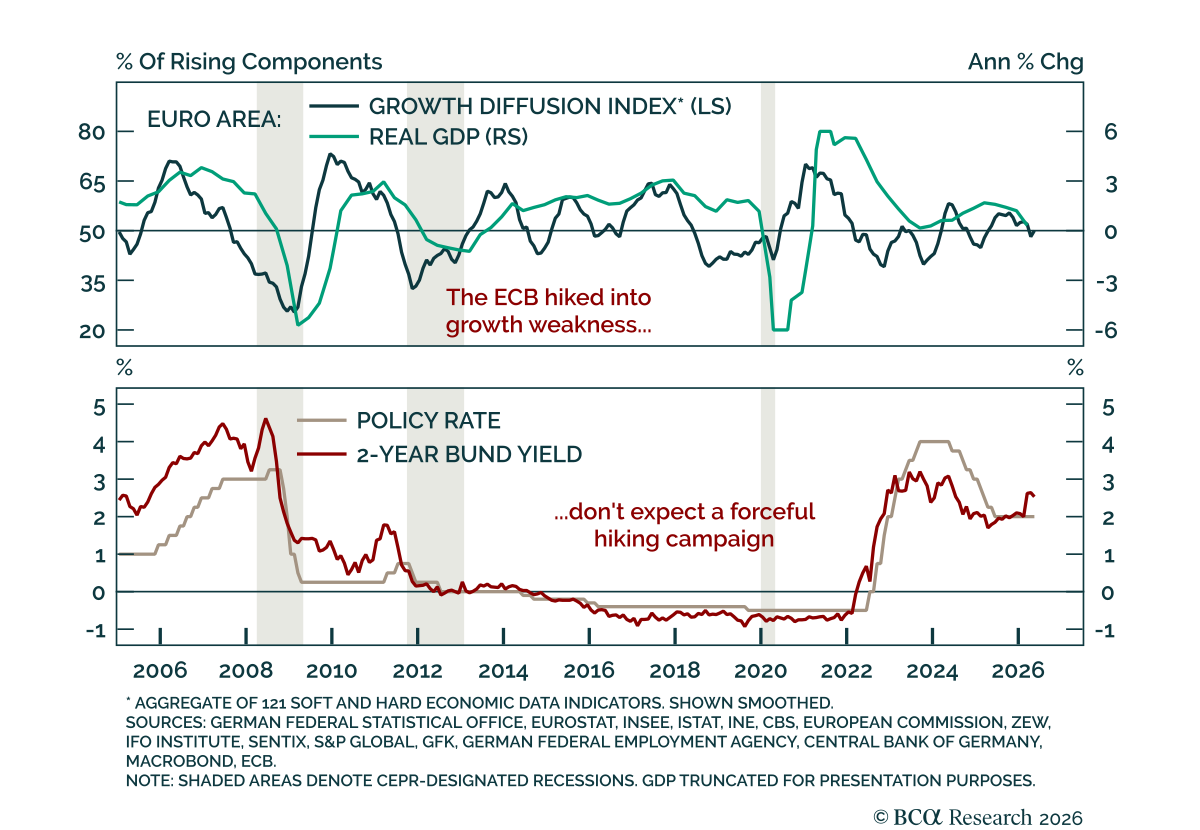

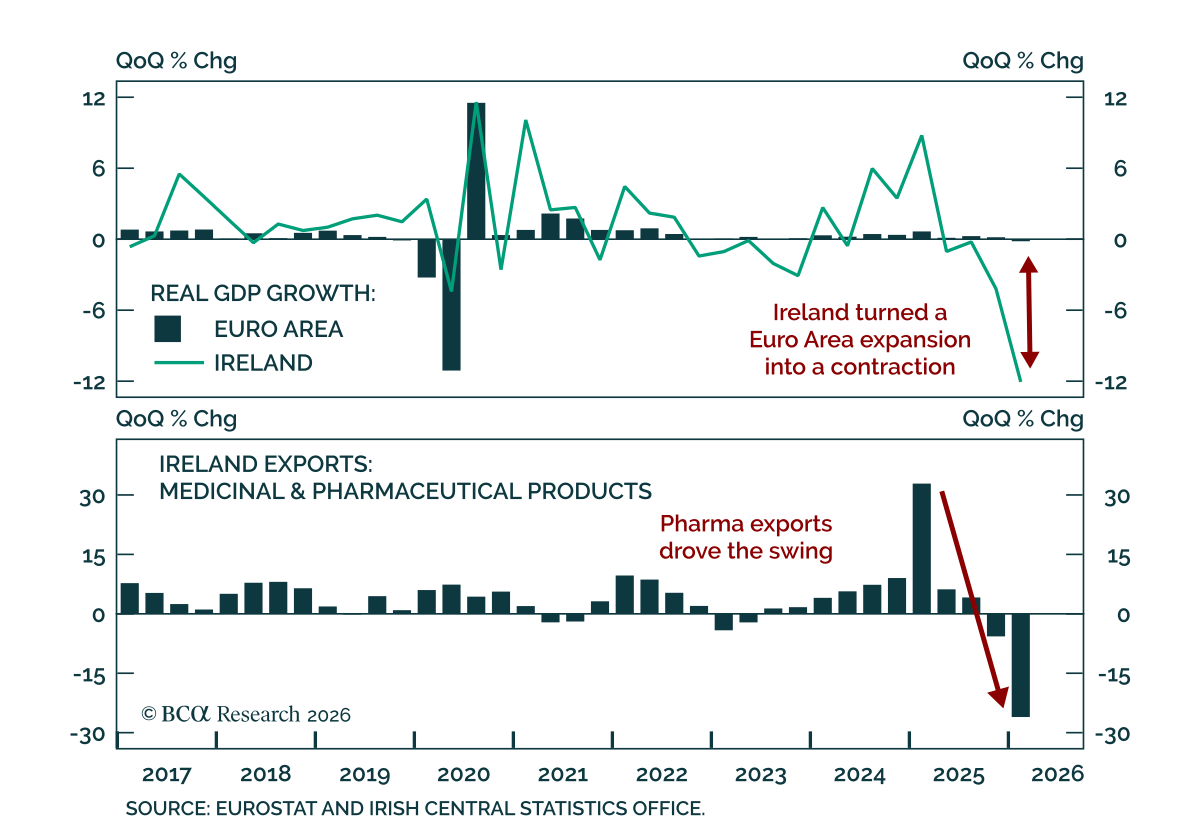

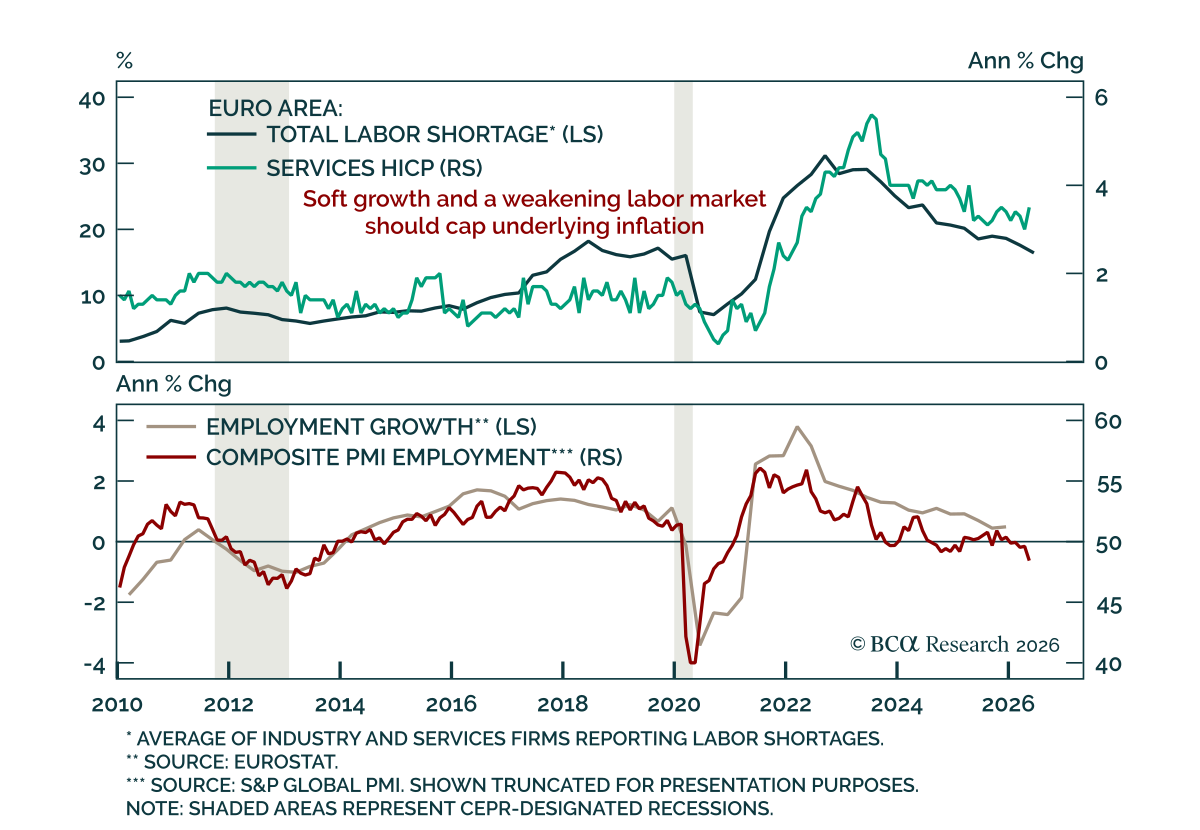

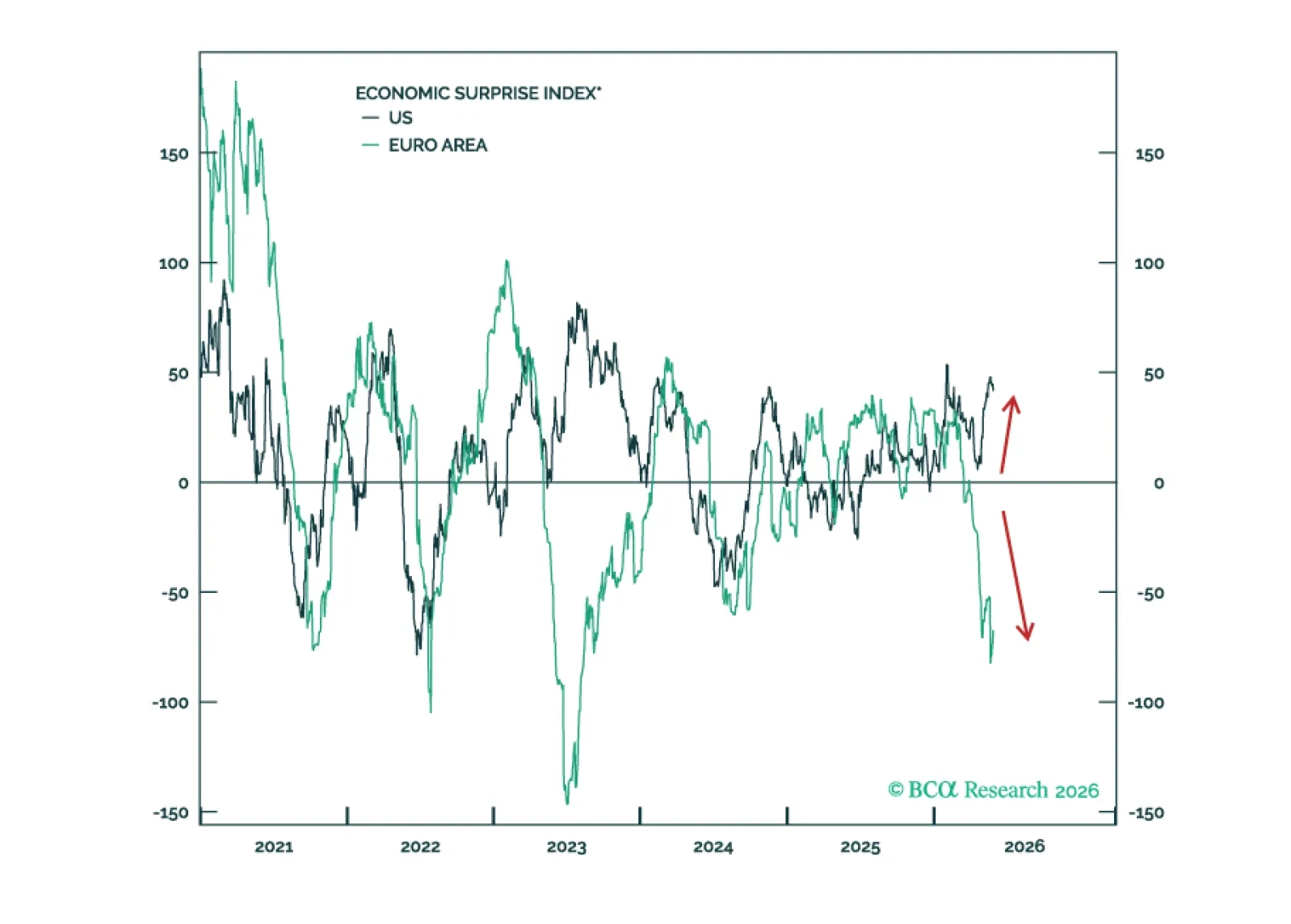

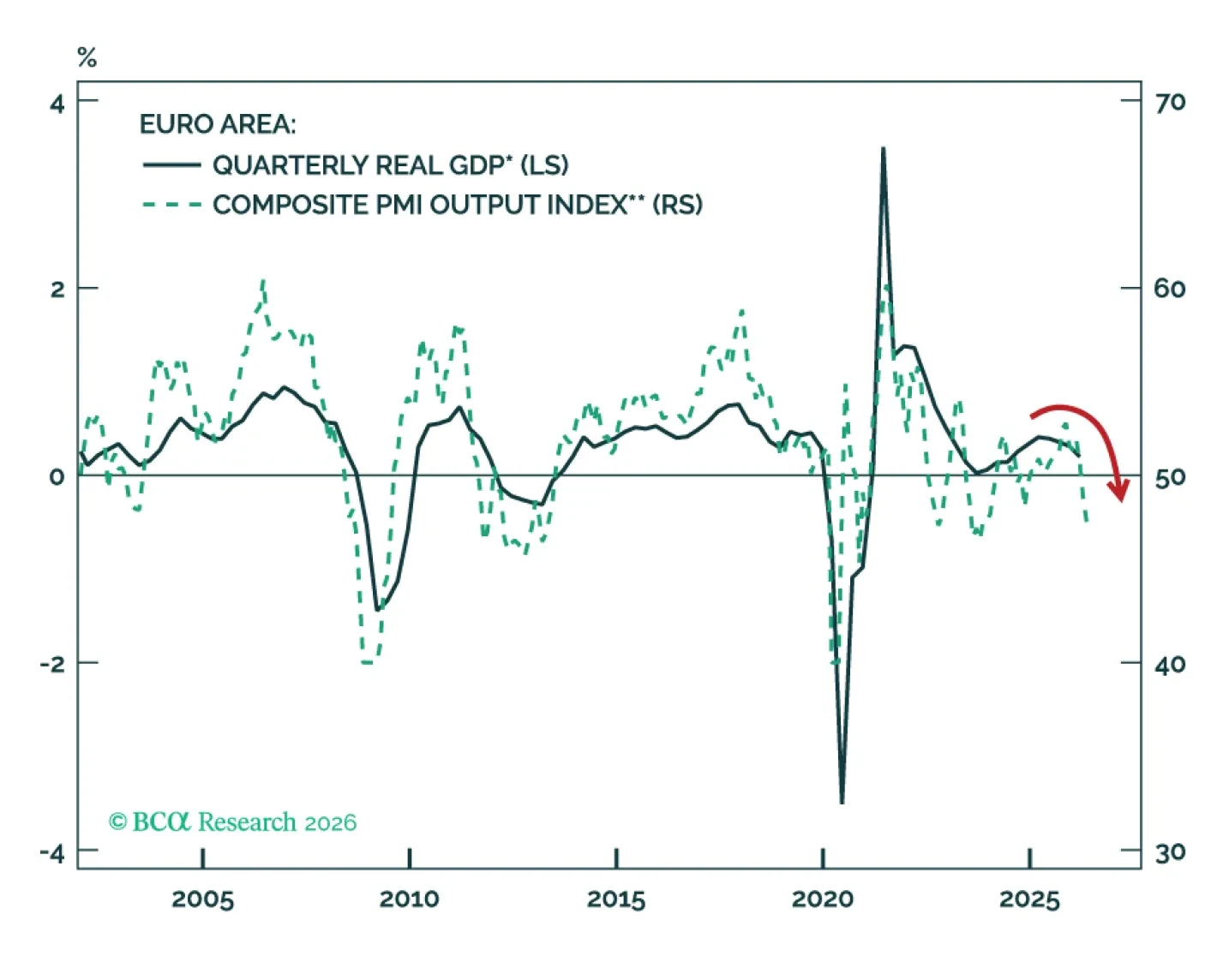

Europe is sliding from stagflation toward recession as prolonged disruptions in the Strait of Hormuz weaken growth, labor markets, and supply chains while keeping inflation elevated. Even if a US-Iran deal is reached, limited fiscal support and rising food inflation leave the Euro Area increasingly vulnerable to a deeper economic downturn.

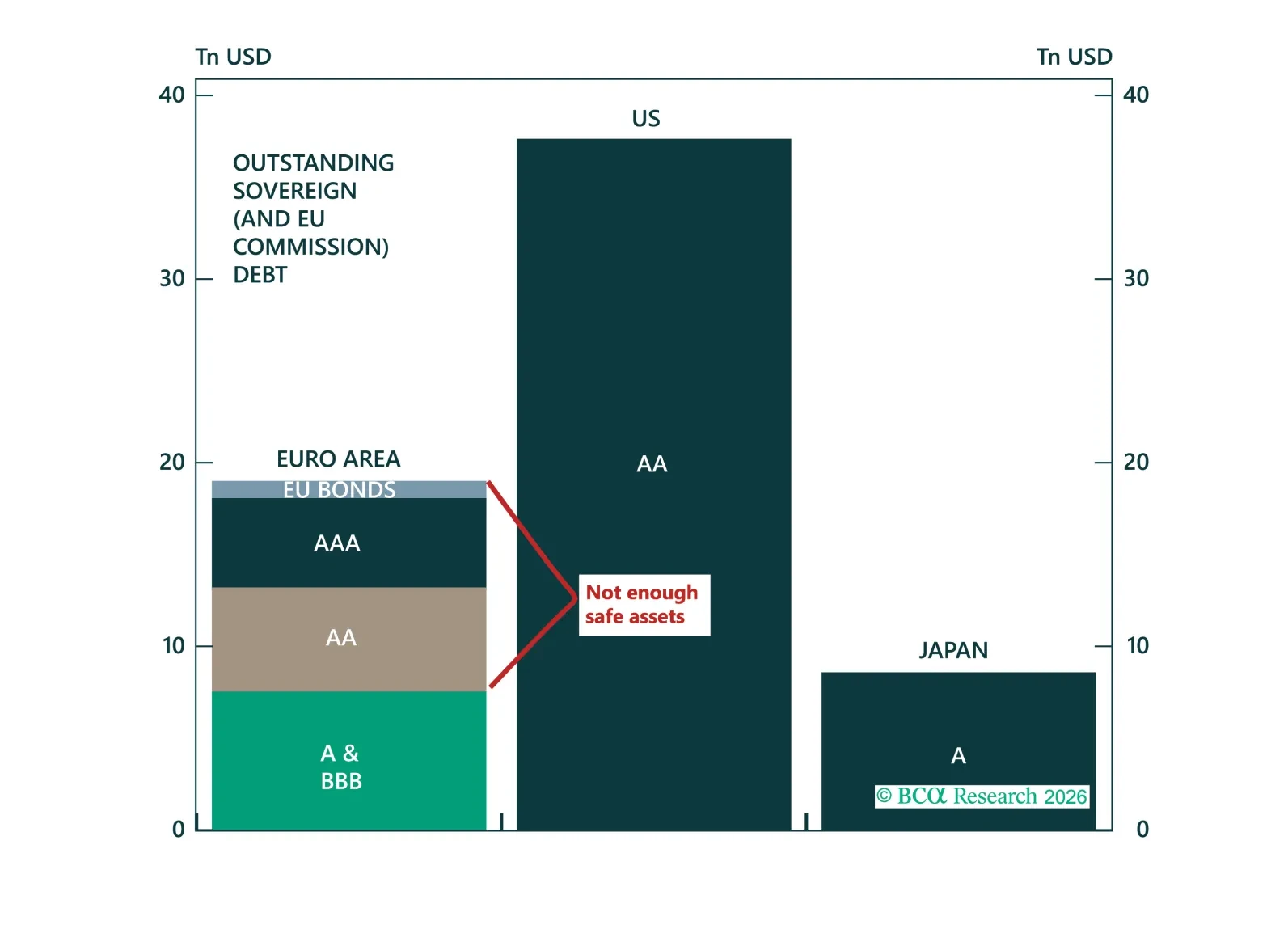

The dollar's retreat is creating the most compelling window for euro internationalisation since Maastricht, but Europe is missing the one instrument that would make it real. In this report, we make the case for the Eurobond, assess which model is most likely to prevail, and explain why the trade is long euro on dips and overweight Central and Eastern European sovereign spreads.

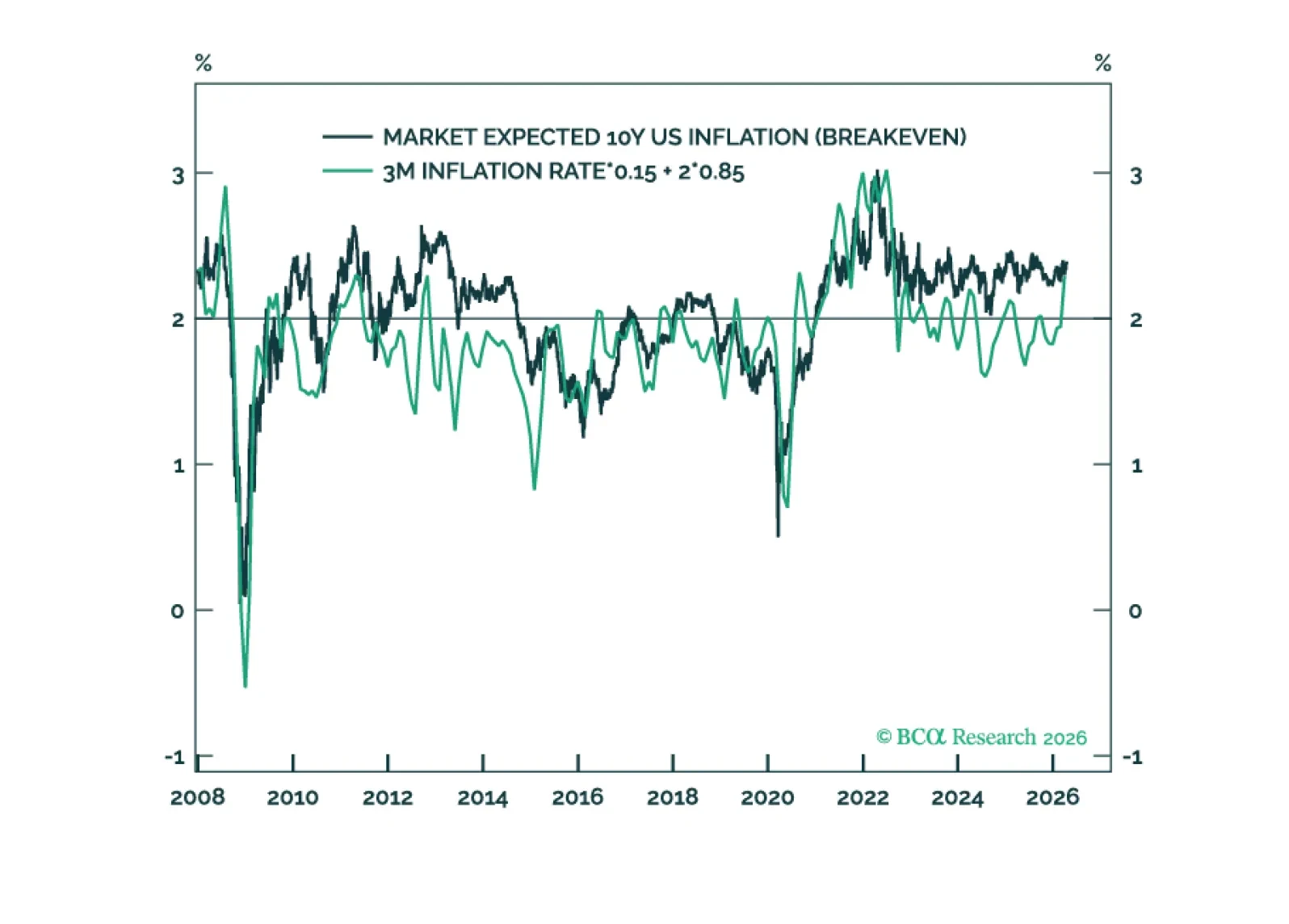

In this Special Report, we describe how inflation expectations are formed. We then demonstrate that steady state inflation expectations have un-anchored in the UK, are un-anchoring in Japan, and are at high risk of un-anchoring in the US. And we conclude with some implications for bond markets.