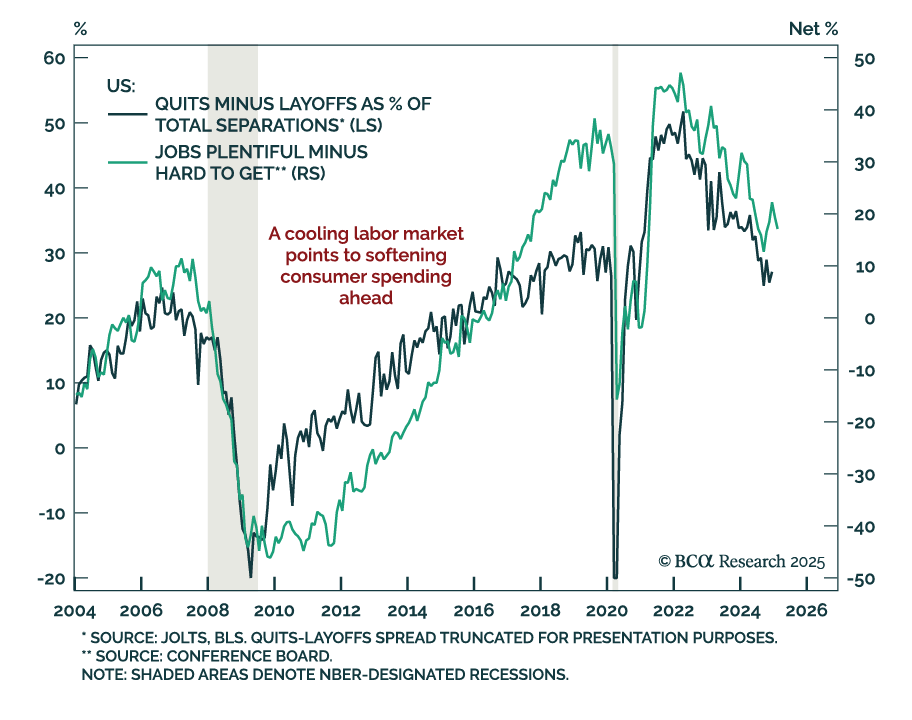

Labor Market

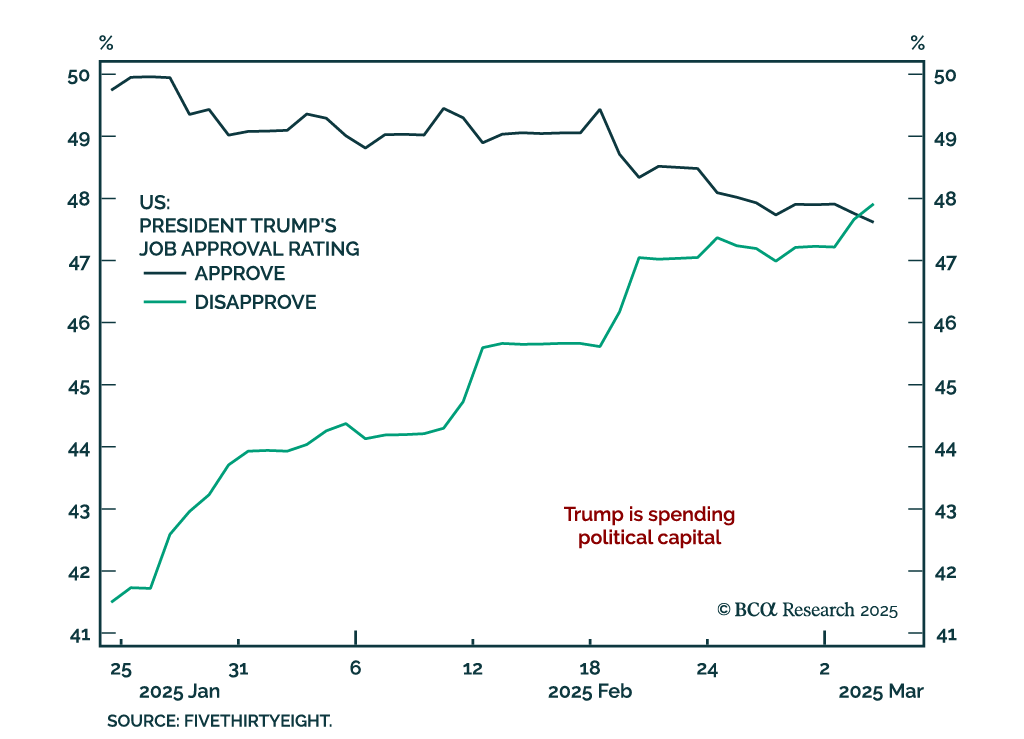

In light of President Trump’s address to Congress and the ebb-and-flow of tariff announcements, our Geopolitical strategists assessed the constraints on the administration’s disruptive agenda. Trump’s ability to implement his agenda is strongest in early…

Please join Doug Peta, Chief US Investment Strategist and co-author of The Bank Credit Analyst, for a Webcast on Wednesday, March 5 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET).

Core PCE inflation was tame this morning, but with large tariffs looming we anticipate loftier inflation readings in the months ahead.

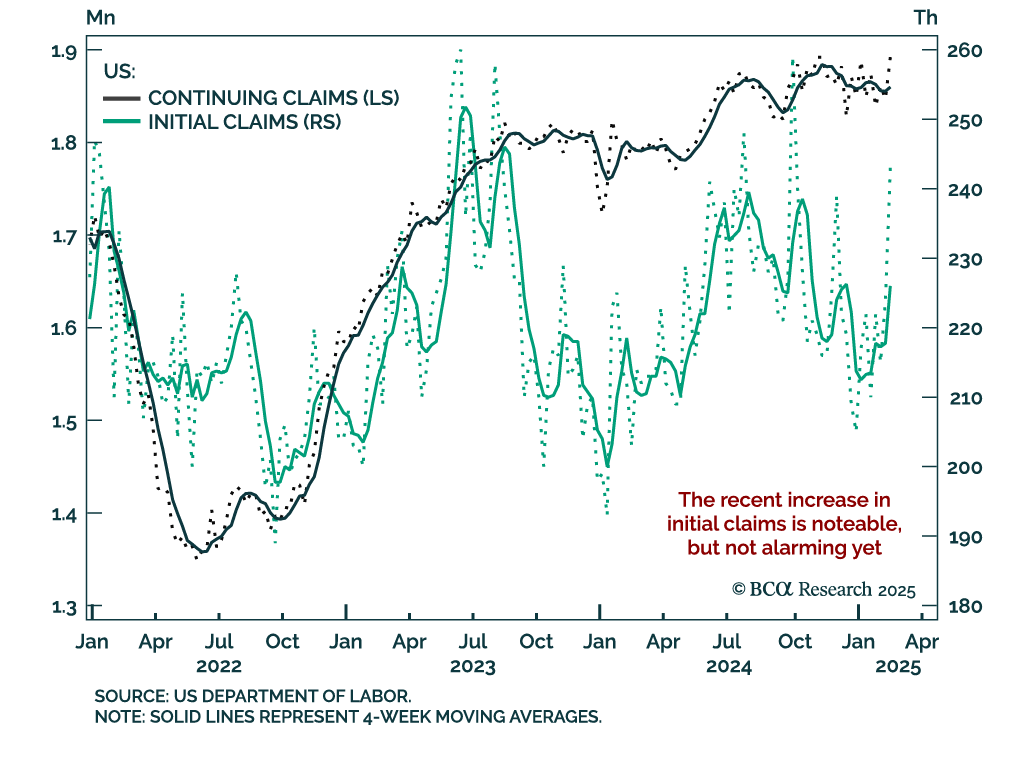

Weekly initial claims ticked up to 242k, near 2024 highs. The data is under the spotlight as the Trump administration implements a reduction of the federal workforce through the DOGE. Initial claims are not alarming yet; they remain near historical lows.…

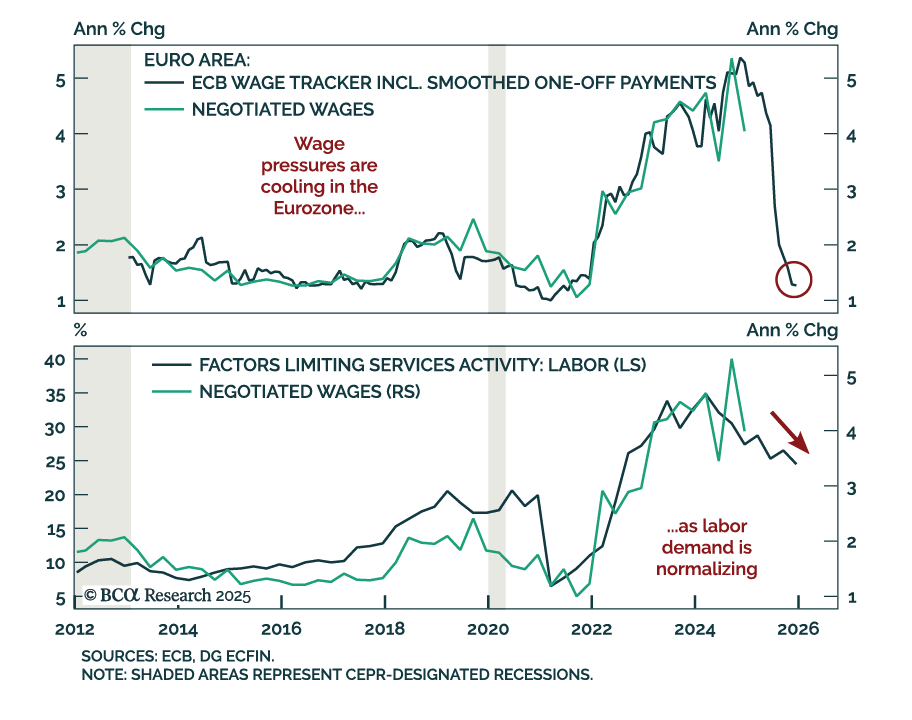

Fourth-quarter European negotiated wages growth cooled to 4.1% y/y, down from the 5.4% peak seen in Q3. The cooling is in line with the ECB’s Wage Tracker showing wage growth decelerating to 1.3% by the end of the year. Labor demand is easing in Europe,…

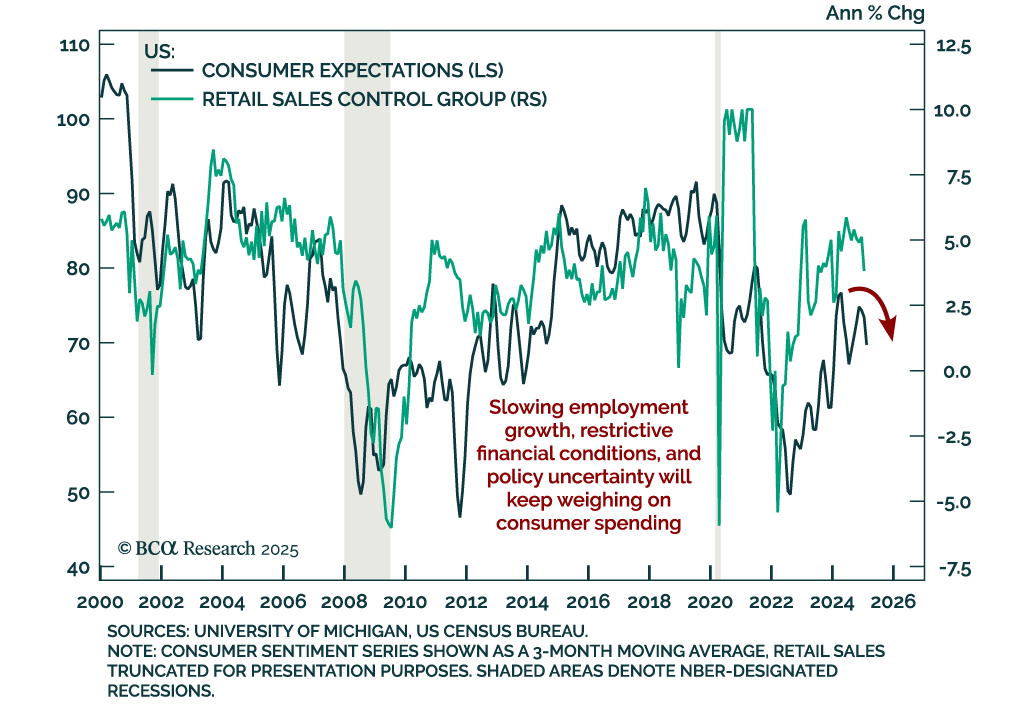

The February Conference Board Consumer Confidence index missed estimates for the third month in a row, falling to 98.3 from 105.3. Consumers’ assessment of both their current situation and their expectations worsened, with the latter falling close to 10…

The January UK CPI was slightly hotter than expected. Headline inflation beat estimates, rising to 3.0% y/y from 2.5% in December. Core inflation also jumped but was in line with expectations at 3.7%. Services were strong, albeit slightly lower than expected…

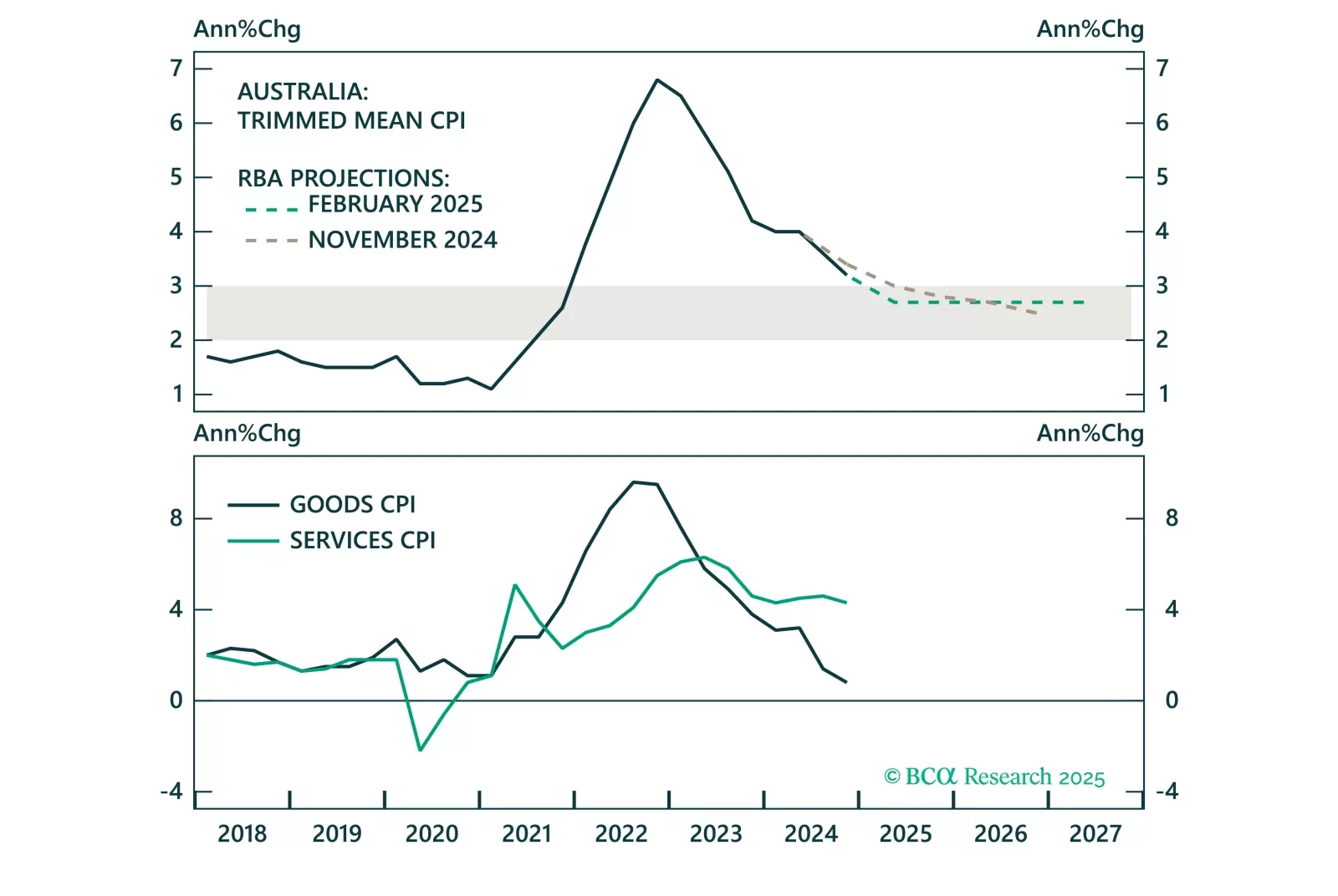

Overnight, the RBA cut the cash target rate for the first time since 2022, marking the beginning of the policy easing cycle in Australia. However, the RBA will proceed cautiously with further rate cuts, given a tight labor market and still elevated services inflation. This will keep Australian government bond yields elevated versus global yields, benefitting the Australian dollar.

January US retail sales missed estimates, with the headline number contracting by 0.9% m/m. The decline was broad-based, with spending excluding autos and gas down 0.5%, and the control group also down 0.8%. The retail sales report was impacted by the…

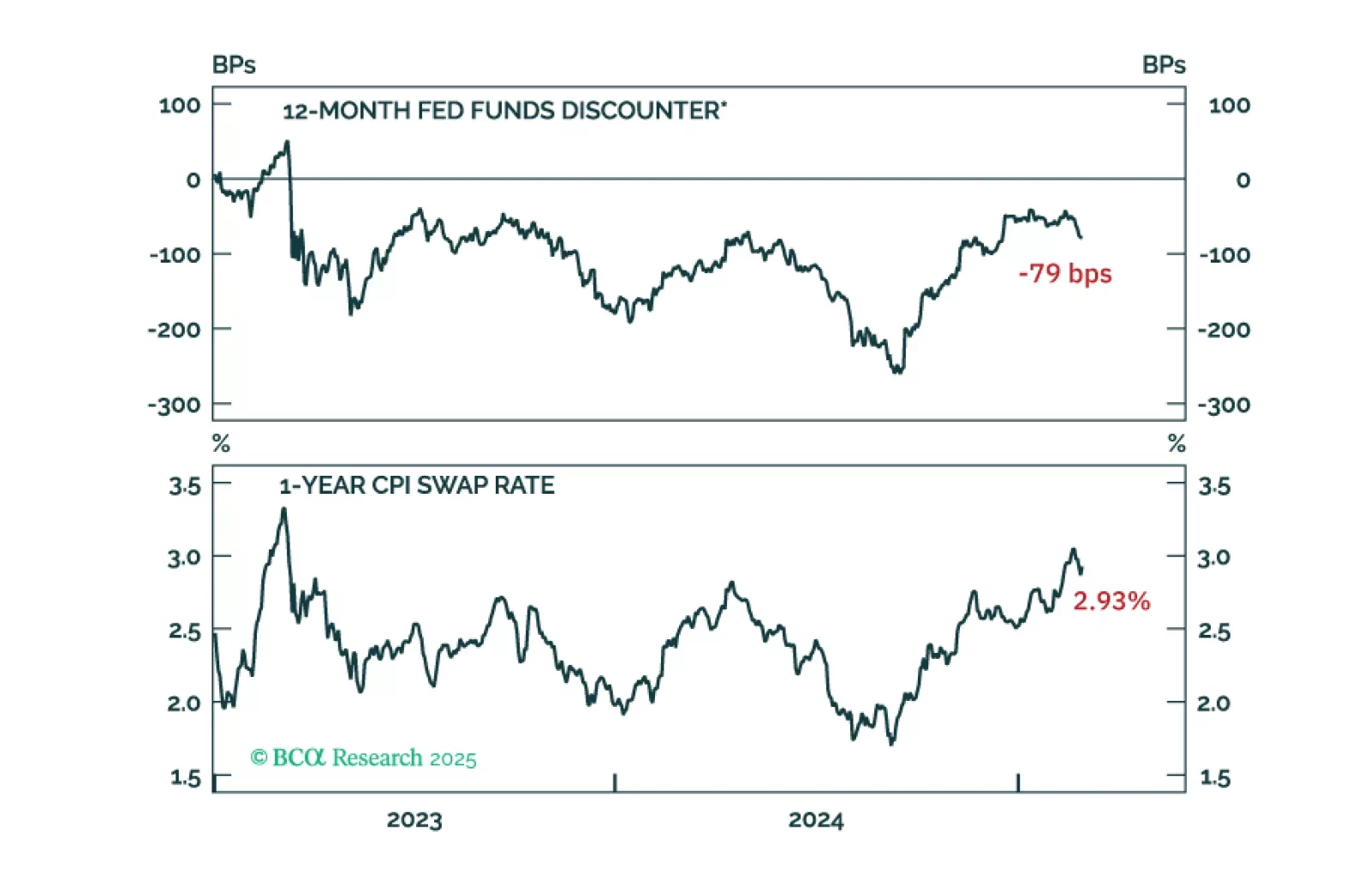

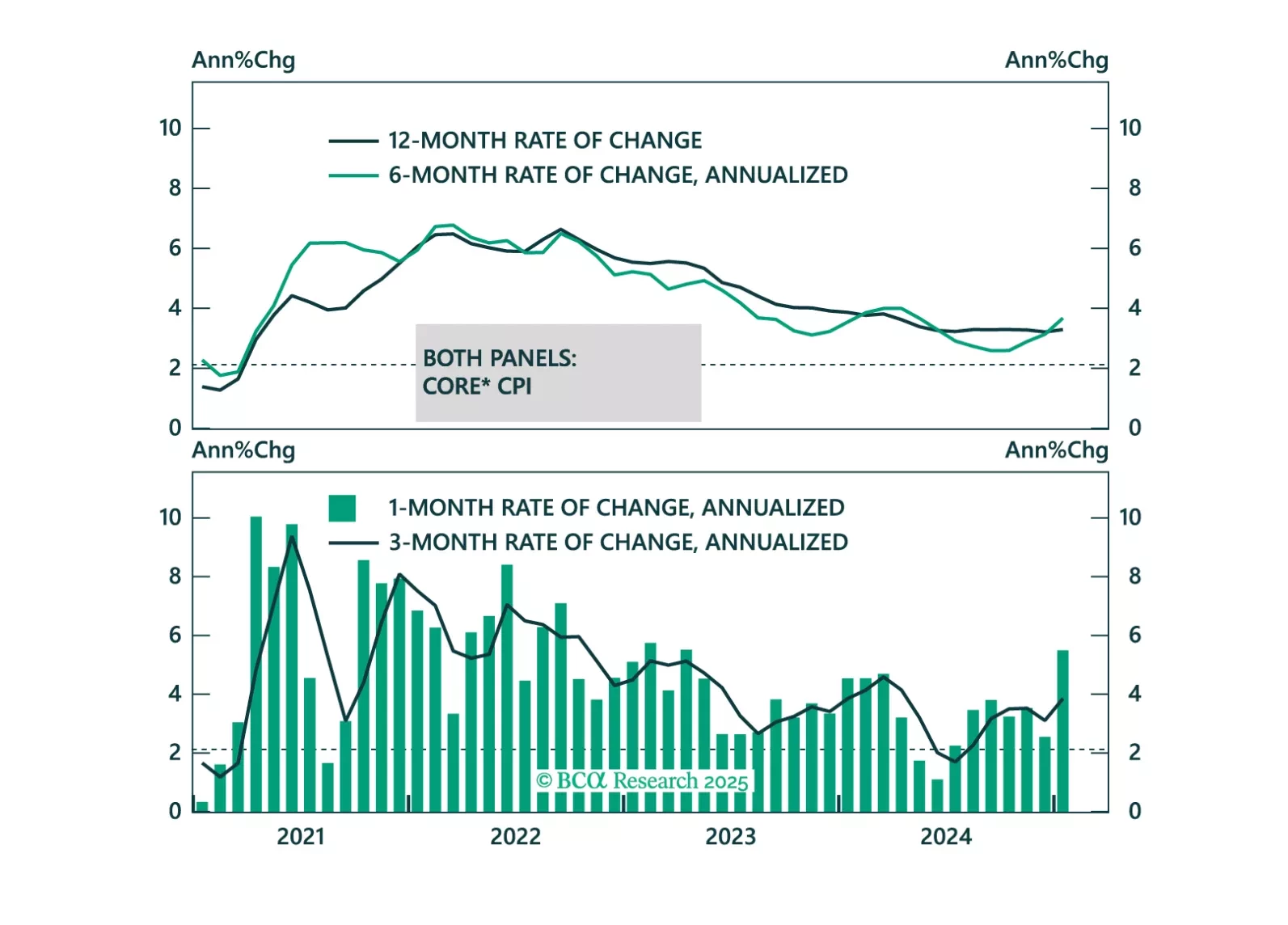

Some thoughts on this morning’s CPI report and its implications for the Fed and Treasury yields.