Energy

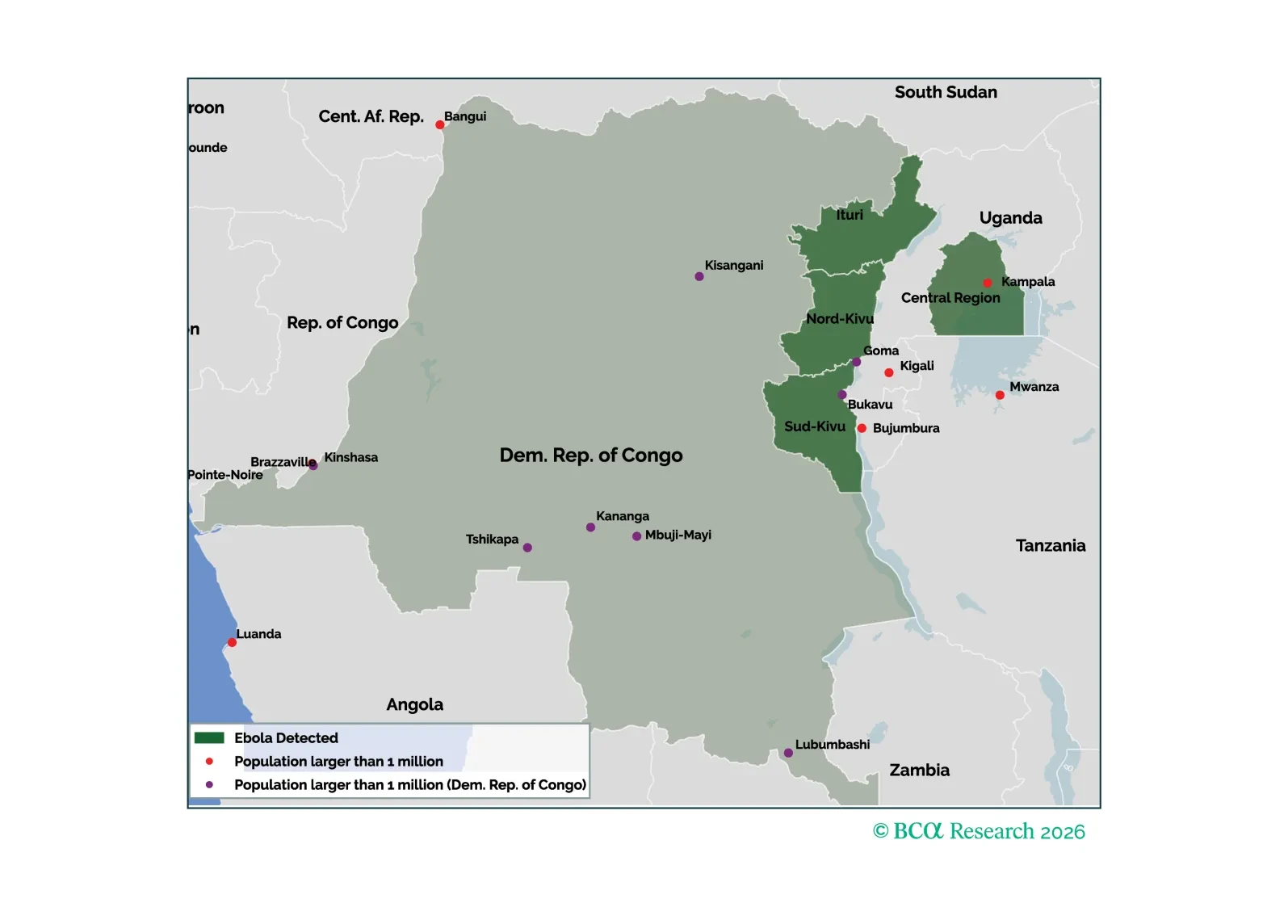

Ebola remains one of the world's deadliest viral diseases, but it is far less transmissible than COVID-19 or influenza. The most likely outcome remains containment rather than a global pandemic.

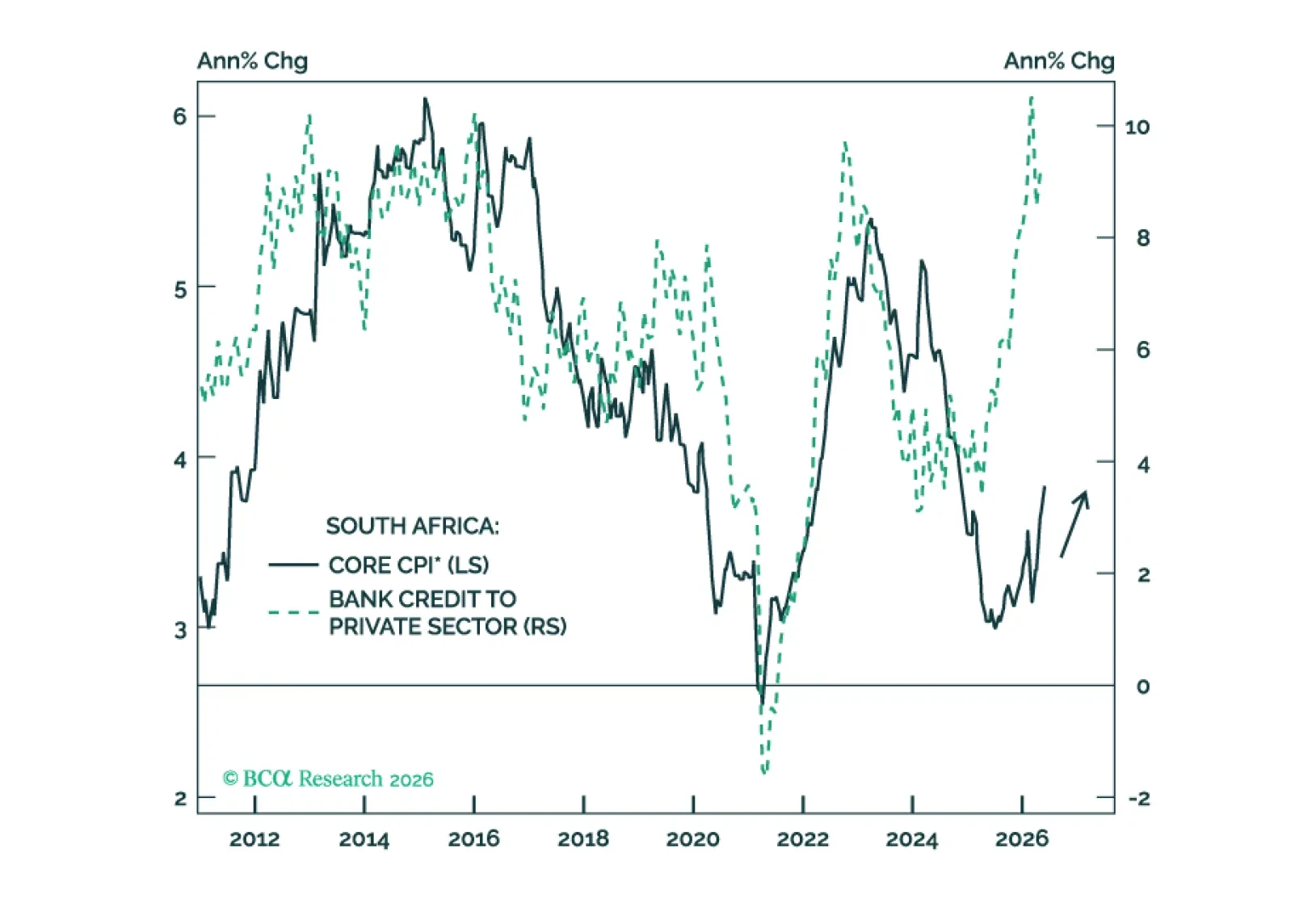

South Africa’s ambitious reform agenda will take time to bear fruit. Meanwhile, the country faces a stagflationary squeeze as inflation rises while growth slows. South African stocks, bonds, and currency are all vulnerable.

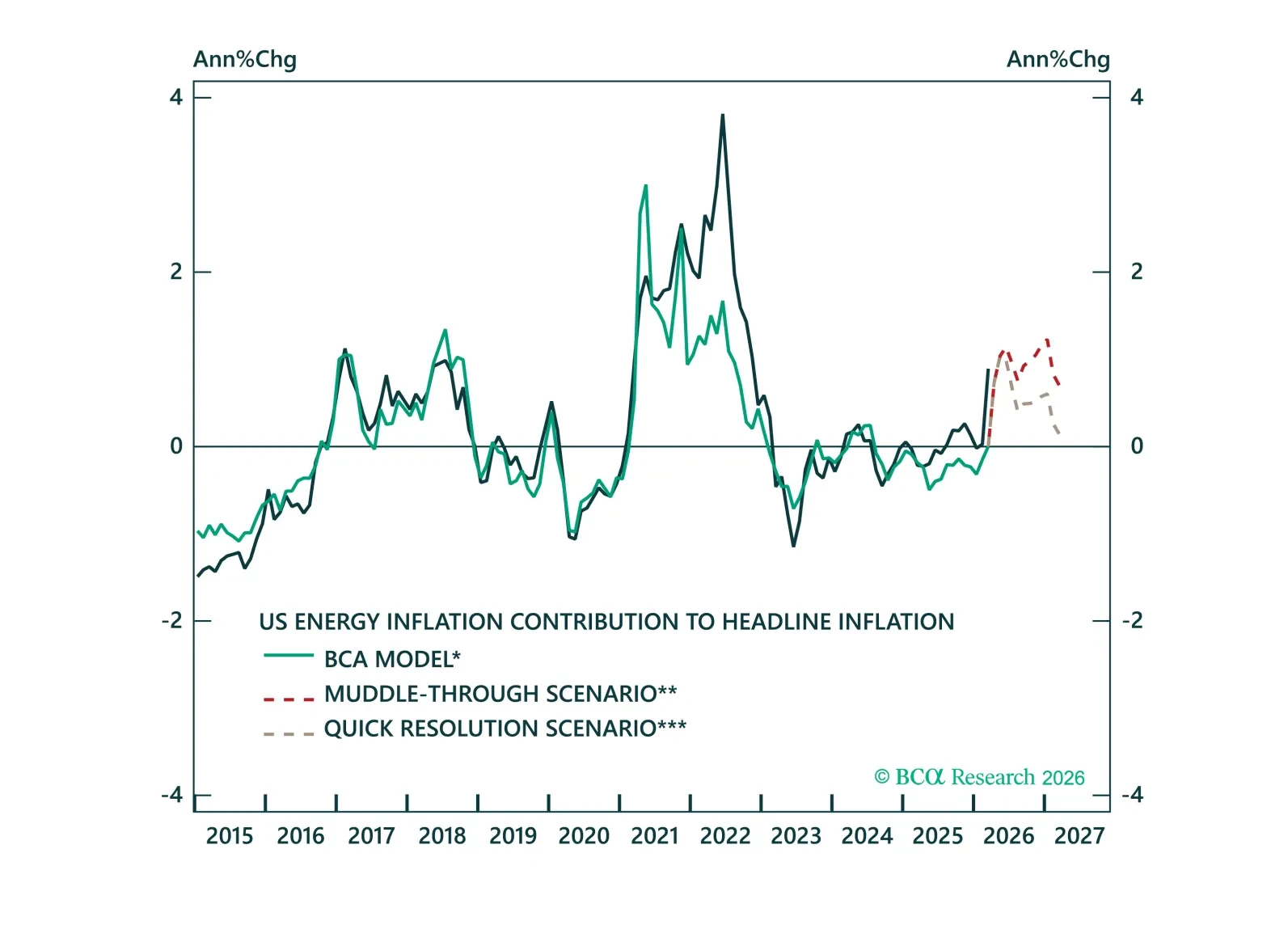

Volatility is high, but the path for yields is clearer than it looks. Across three oil scenarios, we show how policy responses shape fixed income markets and why the balance of risks still points to lower yields.

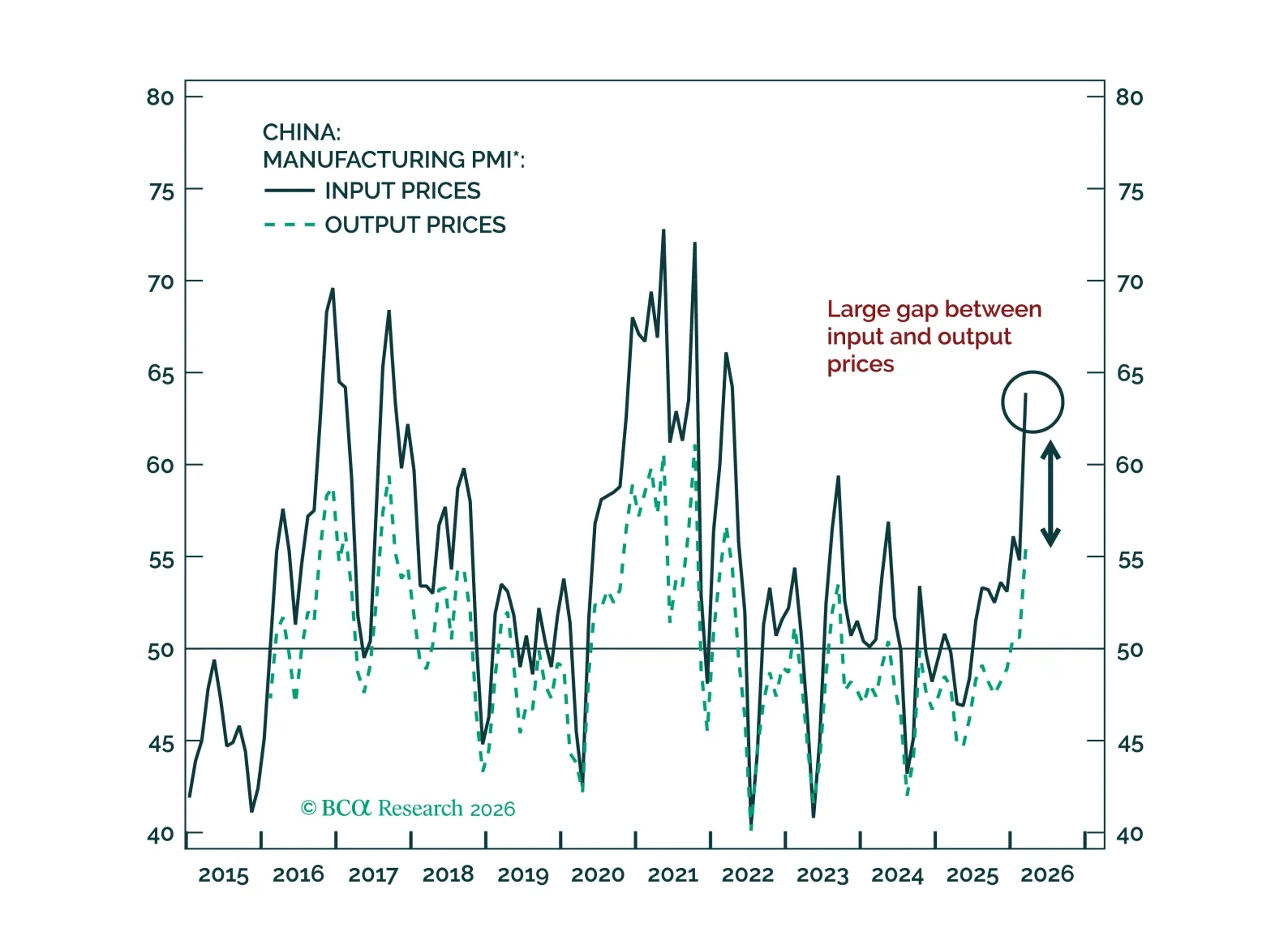

The ceasefire announced on Tuesday may signal peak intensity in the Middle East crisis, but sustained energy price pressures will continue to challenge Chinese corporate profitability.

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

Higher oil prices threaten the global economy, warranting an underweight stance on equities. Over the long haul, industrial metals will fare better than crude.

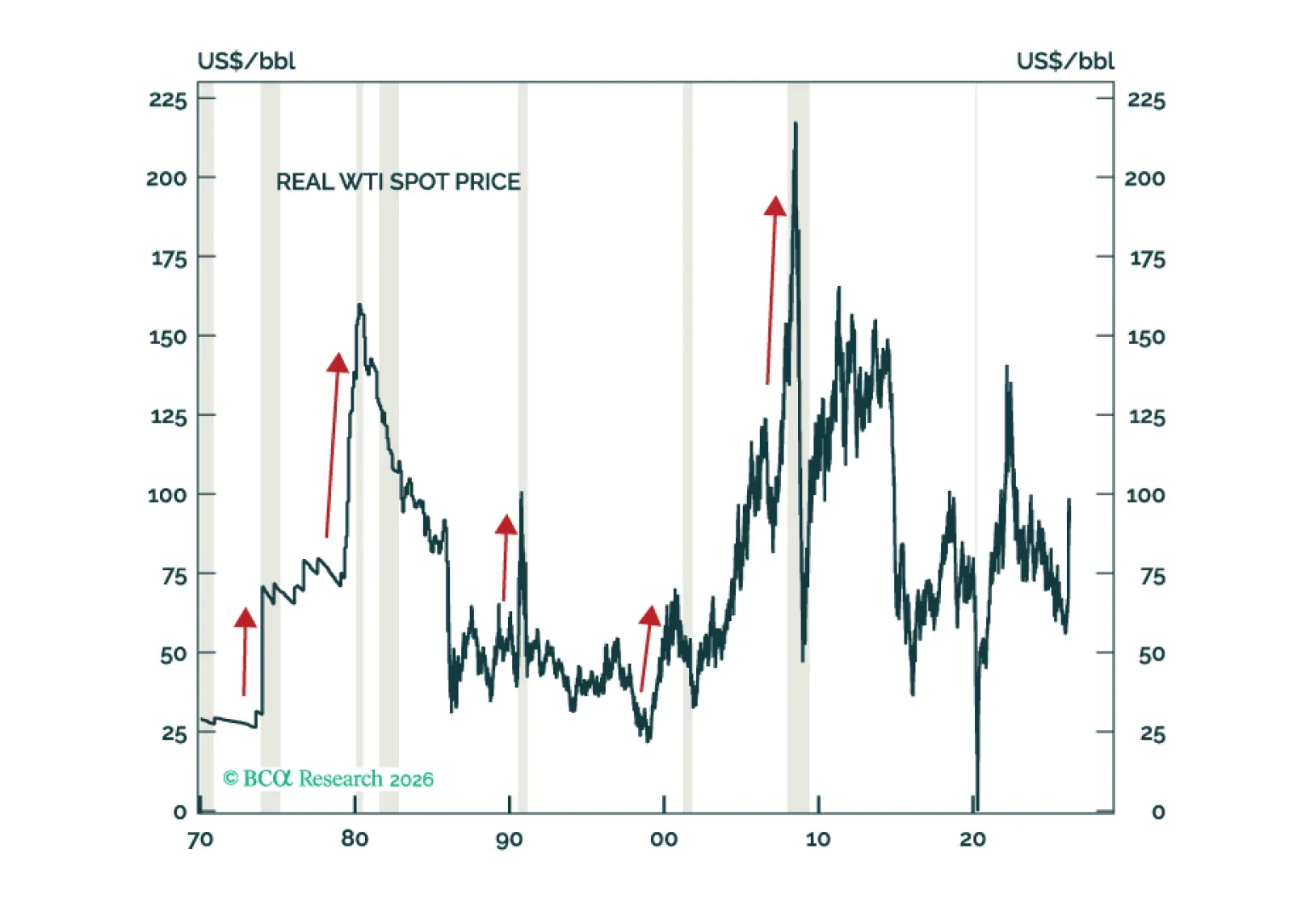

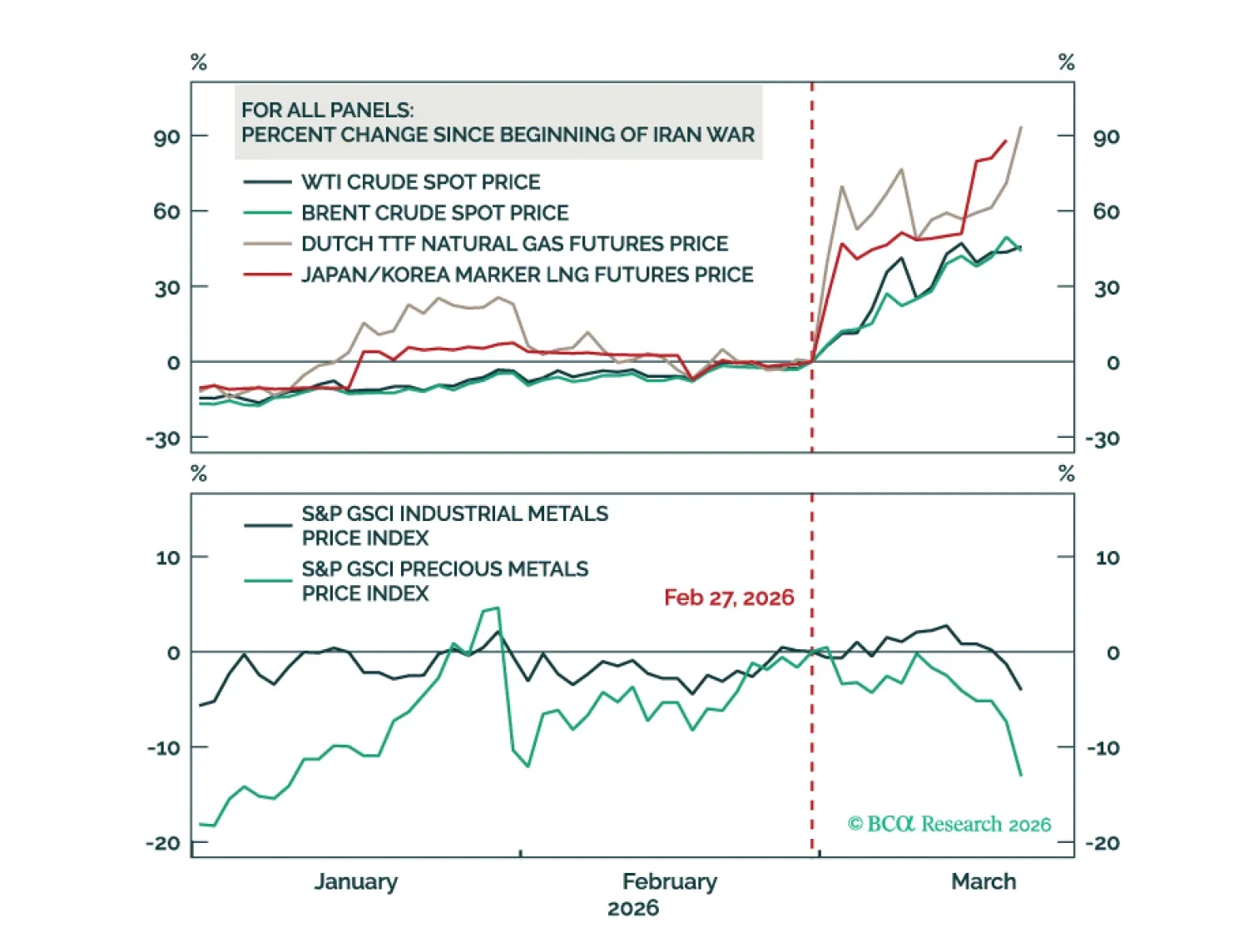

War momentum and escalating rhetoric around the Strait of Hormuz have pushed Brent above $100 and raised the risk of a broader supply shock. While parallels with 2022 offer a roadmap, today’s shock is likely shorter but more globally disruptive. Markets are repricing monetary tightening risks, though we see rate hikes as a mistake absent second-round inflation. Beyond oil, sulfur, helium, and fertilizer disruptions threaten food prices and the AI supply chain. Position defensively.

The spike in oil and gas prices has raised the odds of a global economic downturn. Combined with a more negative signal from our MacroQuant model, this warrants tactically downgrading stocks from neutral to underweight. Looking further ahead, the Iran war will lead to bigger defense budgets and a greater focus on energy self-sufficiency.

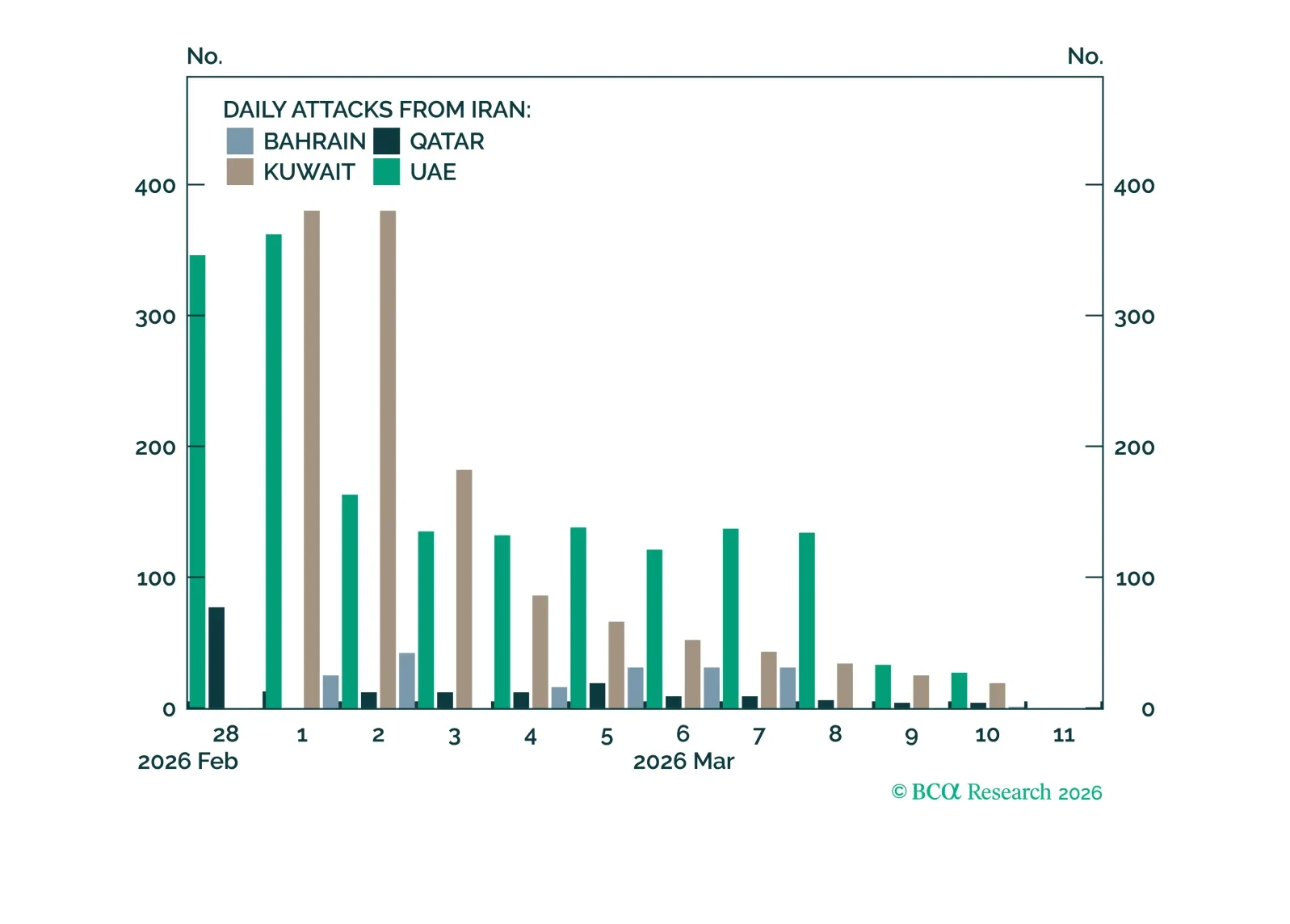

With all eyes on the Strait of Hormuz, BCA Research has created a dashboard of data for your convenience.

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.